You might also like

- How to Prepare Business Cases: An essential guide for accountantsFrom EverandHow to Prepare Business Cases: An essential guide for accountantsNo ratings yet

- Dissertation On Ratio AnalysisDocument5 pagesDissertation On Ratio AnalysisHelpPaperCanada100% (1)

- Thesis Operational Risk ManagementDocument7 pagesThesis Operational Risk Managementjenniferwatsonmobile100% (2)

- Literature Review Capital StructureDocument4 pagesLiterature Review Capital Structureea793wsz100% (1)

- Thesis On Operational RiskDocument7 pagesThesis On Operational RiskRick Vogel100% (2)

- Dissertation On Ratio Analysis PDFDocument4 pagesDissertation On Ratio Analysis PDFWriteMyPaperApaStyleCanada100% (1)

- Operational Risk Dissertation TopicsDocument7 pagesOperational Risk Dissertation TopicsWriteMyPaperOneDaySingapore100% (1)

- Research Papers Operational Risk ManagementDocument4 pagesResearch Papers Operational Risk Managementc9jg5wx4100% (1)

- Capital structure and financial performance of listed Sri Lankan trading companiesDocument14 pagesCapital structure and financial performance of listed Sri Lankan trading companiesShamweel MugholNo ratings yet

- PHD Thesis On Financial Statement AnalysisDocument8 pagesPHD Thesis On Financial Statement Analysisljctxlgld100% (2)

- Ifrsinbrief Se 15may13Document3 pagesIfrsinbrief Se 15may13Leann TaguilasoNo ratings yet

- Determinants of Working Capital Investment: A Study of Malaysian Public Listed FirmsDocument25 pagesDeterminants of Working Capital Investment: A Study of Malaysian Public Listed FirmsEyock PierreNo ratings yet

- Business Failure Prediction 18 Sept 2010Document41 pagesBusiness Failure Prediction 18 Sept 2010Shariff MohamedNo ratings yet

- SEI OppRisk Book USDocument49 pagesSEI OppRisk Book USJCPAJONo ratings yet

- Thesis On Operational Risk ManagementDocument5 pagesThesis On Operational Risk Managementlesliesanchezanchorage100% (1)

- Sample Thesis Financial Performance AnalysisDocument4 pagesSample Thesis Financial Performance Analysissandraahnwashington100% (2)

- Outsourcisng PaperDocument60 pagesOutsourcisng PaperCfhunSaatNo ratings yet

- Final Original File For PlagDocument56 pagesFinal Original File For Plagaurorashiva1No ratings yet

- Project On Private Label of "Shopper Stop Limited": ContentDocument11 pagesProject On Private Label of "Shopper Stop Limited": ContentRakesh SamariyaNo ratings yet

- Bank Efficiency DissertationDocument4 pagesBank Efficiency DissertationCustomCollegePaperElgin100% (1)

- 2013IJBValuationmethodP590-2correctedDocument9 pages2013IJBValuationmethodP590-2correctedHana SupportNo ratings yet

- Dissertation Report On Portfolio InvestmentDocument8 pagesDissertation Report On Portfolio InvestmentWriteMyBusinessPaperSingapore100% (1)

- Thesis On Debt FinancingDocument8 pagesThesis On Debt Financingheidimaestassaltlakecity100% (2)

- Enterprise Risk Management Research PaperDocument6 pagesEnterprise Risk Management Research Paperb0siw1h1tab2100% (1)

- SVKM's Narsee Monjee Institute of Management Studies - BangaloreDocument3 pagesSVKM's Narsee Monjee Institute of Management Studies - BangaloreSaurabh Krishna SinghNo ratings yet

- Research Papers On Risk and ReturnDocument6 pagesResearch Papers On Risk and ReturnqzafzzhkfNo ratings yet

- Thesis On Investment AppraisalDocument6 pagesThesis On Investment AppraisalAmanda Summers100% (2)

- Research Paper Financial Risk ManagementDocument8 pagesResearch Paper Financial Risk Managementwpuzxcbkf100% (1)

- WiproDocument18 pagesWiprohealingfactor333No ratings yet

- KPMG DissertationDocument5 pagesKPMG Dissertationcreasimovel1987100% (1)

- Telecommunications 2012-01-01Document28 pagesTelecommunications 2012-01-01STEVENo ratings yet

- Working Capital Policy Practice Evidence FR - 2012 - Procedia - Social and BehaDocument6 pagesWorking Capital Policy Practice Evidence FR - 2012 - Procedia - Social and BehaMadhura AbhyankarNo ratings yet

- 1 s2.0 S187704281500405X Main PDFDocument8 pages1 s2.0 S187704281500405X Main PDFafifahfauziyahNo ratings yet

- BBA4600 Test 2 2022Document9 pagesBBA4600 Test 2 2022GIVEN N SIPANJENo ratings yet

- Cash Holding in Manufacturing Companies: A Study of IndonesiaDocument10 pagesCash Holding in Manufacturing Companies: A Study of IndonesiaAngelia PhanjayaNo ratings yet

- Investment Consulting Business PlanDocument9 pagesInvestment Consulting Business Planbe_supercoolNo ratings yet

- Determinants of Working Capital Requirements inDocument12 pagesDeterminants of Working Capital Requirements inMahmood KhanNo ratings yet

- Financing and Corporate Growth Model with Repeated Moral HazardDocument24 pagesFinancing and Corporate Growth Model with Repeated Moral HazardGranillo RafaNo ratings yet

- Predicting Firms' Financial Distress: An Empirical Analysis Using The F-Score ModelDocument16 pagesPredicting Firms' Financial Distress: An Empirical Analysis Using The F-Score ModelKHOA NGUYEN ANHNo ratings yet

- Dissertation On Investment AppraisalDocument9 pagesDissertation On Investment AppraisalPaperWriterUK100% (2)

- 5 - Synopsis of Working Capital Management On Shri Ram Life Insurance Company LTD FinalDocument22 pages5 - Synopsis of Working Capital Management On Shri Ram Life Insurance Company LTD Finalvarunbhutani1211278267% (3)

- Management Thesis - I: SynopsisDocument6 pagesManagement Thesis - I: Synopsisarya2783No ratings yet

- Articles About Finance - HBS Working KnowledgeDocument98 pagesArticles About Finance - HBS Working KnowledgesaqawsaqawNo ratings yet

- Jurnal Tesis Fintech 1Document33 pagesJurnal Tesis Fintech 1stevanusNo ratings yet

- Research Paper On Accounting Information SystemsDocument6 pagesResearch Paper On Accounting Information Systemsfvffv0x7No ratings yet

- Research Paper On Private EquityDocument8 pagesResearch Paper On Private Equitytutozew1h1g2100% (1)

- Thesis On Determinants of Capital StructureDocument4 pagesThesis On Determinants of Capital Structuredwbeqxpb100% (2)

- Final Ratio AnalysisDocument40 pagesFinal Ratio AnalysisShruti PatilNo ratings yet

- 106 - Machine Learning and Credit Risk ModellingDocument8 pages106 - Machine Learning and Credit Risk Modellingwajih chtibaNo ratings yet

- THESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementDocument46 pagesTHESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementVon Ianelle AguilaNo ratings yet

- Published ResearchDocument9 pagesPublished ResearchcrushonarlolNo ratings yet

- PHD Thesis On Ratio AnalysisDocument5 pagesPHD Thesis On Ratio Analysisaflodnyqkefbbm100% (2)

- Ipo Dissertation TopicsDocument8 pagesIpo Dissertation TopicsHelpWritingACollegePaperSingapore100% (1)

- Operational Risk in Banks ThesisDocument7 pagesOperational Risk in Banks Thesispwqlnolkd100% (1)

- Shipping Finance DissertationDocument7 pagesShipping Finance DissertationHelpWithFilingDivorcePapersCanada100% (1)

- Why Is The Risk Analysis Essential in The Project Management Process?Document11 pagesWhy Is The Risk Analysis Essential in The Project Management Process?Hany Rashad DawoodNo ratings yet

- A Study On Capital Structure and Leverage of Tata Motors Limited: Its Role and Future ProspectsDocument14 pagesA Study On Capital Structure and Leverage of Tata Motors Limited: Its Role and Future ProspectsSanju ChopraNo ratings yet

- Thesis On Equity ValuationDocument6 pagesThesis On Equity Valuationmelanieericksonminneapolis100% (2)

- Hoberg and Maksimovic - 2015 - Redefining Financial Constraints A Text-Based Analysis - RFS2015Document41 pagesHoberg and Maksimovic - 2015 - Redefining Financial Constraints A Text-Based Analysis - RFS2015Karanveer SinghNo ratings yet

- Master Thesis Joint VentureDocument4 pagesMaster Thesis Joint Ventureaflnzraiaaetew100% (2)

- Return On Investment: Example of The ROI Formula CalculationDocument3 pagesReturn On Investment: Example of The ROI Formula CalculationMd Azim100% (1)

- What Is Life Cycle Costing?Document1 pageWhat Is Life Cycle Costing?Md AzimNo ratings yet

- Data Sources For ResearchDocument1 pageData Sources For ResearchMd AzimNo ratings yet

- What Is Transfer Pricing?Document2 pagesWhat Is Transfer Pricing?Md AzimNo ratings yet

- Throughput Accounting and The Theory of ConstraintsDocument8 pagesThroughput Accounting and The Theory of ConstraintsMd AzimNo ratings yet

- HeteroscedasticityDocument2 pagesHeteroscedasticityMd AzimNo ratings yet

- Problems of Target CostingDocument2 pagesProblems of Target CostingMd AzimNo ratings yet

- Accounting for Long-Term Asset RevisionsDocument8 pagesAccounting for Long-Term Asset RevisionsMd AzimNo ratings yet

- Probability and Statistics: Model AssumptionsDocument2 pagesProbability and Statistics: Model AssumptionsMd AzimNo ratings yet

- How To Know Fraud in AdvanceDocument6 pagesHow To Know Fraud in AdvanceMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Probability and Statistics: Model AssumptionsDocument2 pagesProbability and Statistics: Model AssumptionsMd AzimNo ratings yet

- Dematerialized SecuritiesDocument1 pageDematerialized SecuritiesMd AzimNo ratings yet

- Method of Predicting Corporate FailuresDocument1 pageMethod of Predicting Corporate FailuresMd AzimNo ratings yet

- Deductive Reasoning Vs Inductive ReasoningDocument2 pagesDeductive Reasoning Vs Inductive ReasoningMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Cover Letter For ManuscriptDocument1 pageCover Letter For ManuscriptMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- SamplingDocument7 pagesSamplingMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument4 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Probit Model: Conceptual FrameworkDocument1 pageProbit Model: Conceptual FrameworkMd AzimNo ratings yet

- Types of Random Sampling ExplainedDocument2 pagesTypes of Random Sampling ExplainedMd AzimNo ratings yet

- Empirical Analysis Prediction of Japanese Corporate Failure Japanese Corporate Failure - 1998 - Shirata PDFDocument19 pagesEmpirical Analysis Prediction of Japanese Corporate Failure Japanese Corporate Failure - 1998 - Shirata PDFMd AzimNo ratings yet

- Predicting Corporate Failure in UK - Multidimensional Scaling Approach - Neophytou - 2004 PDFDocument34 pagesPredicting Corporate Failure in UK - Multidimensional Scaling Approach - Neophytou - 2004 PDFMd AzimNo ratings yet

- Artificial Neural Network Model For Business Failure Prediction of Distressed Firms in Colombo Stock Exchanged - Sujeewa - 2014 PDFDocument18 pagesArtificial Neural Network Model For Business Failure Prediction of Distressed Firms in Colombo Stock Exchanged - Sujeewa - 2014 PDFMd AzimNo ratings yet

- A Hybrid Genetic Model For The Prediction of Corporate Failure - 2004 - Brabazon PDFDocument19 pagesA Hybrid Genetic Model For The Prediction of Corporate Failure - 2004 - Brabazon PDFMd AzimNo ratings yet

- Between Population: Difference MeansDocument2 pagesBetween Population: Difference MeansMd AzimNo ratings yet

- Logistic Regression Model For Business Failures Prediction of Technology Industry in Thailand - Puagwatanaa - 2012 PDFDocument6 pagesLogistic Regression Model For Business Failures Prediction of Technology Industry in Thailand - Puagwatanaa - 2012 PDFMd AzimNo ratings yet

- Empirical Analysis Prediction of Japanese Corporate Failure Japanese Corporate Failure - 1998 - Shirata PDFDocument19 pagesEmpirical Analysis Prediction of Japanese Corporate Failure Japanese Corporate Failure - 1998 - Shirata PDFMd AzimNo ratings yet

- A Hybrid Genetic Model For The Prediction of Corporate Failure - 2004 - Brabazon PDFDocument19 pagesA Hybrid Genetic Model For The Prediction of Corporate Failure - 2004 - Brabazon PDFMd AzimNo ratings yet

- Basava Weekly ReportDocument5 pagesBasava Weekly Reportbasava prasadNo ratings yet

- BHP Group PLCDocument20 pagesBHP Group PLCKishor JhaNo ratings yet

- Kelompok 15 - Artikel Peran LPKSMDocument19 pagesKelompok 15 - Artikel Peran LPKSMRomeo NovaldyNo ratings yet

- Resistant Flooring Solutions For Biscuit Plant: Mondelez - Casablanca, MoroccoDocument2 pagesResistant Flooring Solutions For Biscuit Plant: Mondelez - Casablanca, Moroccobassem kooliNo ratings yet

- Test tiếng anhDocument4 pagesTest tiếng anh03 Lê Thị Kim Chi 12A6100% (1)

- Factors Influencing Customer Satisfaction Towards Lazada Online Shopping in MalaysiaDocument24 pagesFactors Influencing Customer Satisfaction Towards Lazada Online Shopping in MalaysiaSharwiniRajenthiranNo ratings yet

- Decision Making at Igate and Patni ComputersDocument16 pagesDecision Making at Igate and Patni ComputersAnkita NirolaNo ratings yet

- TOApr May 23Document24 pagesTOApr May 23buzbonNo ratings yet

- 1.3 CET 402 Quantity Surveying and ValuationDocument12 pages1.3 CET 402 Quantity Surveying and ValuationOwsu KurianNo ratings yet

- Pictet-Human-R EUR - FACTSHEET - LU2247920262 - EN - DEFAULT - 31jan2022Document4 pagesPictet-Human-R EUR - FACTSHEET - LU2247920262 - EN - DEFAULT - 31jan2022ATNo ratings yet

- The Learners Independently Prepare and Cook Vegetable DishesDocument4 pagesThe Learners Independently Prepare and Cook Vegetable DishesJunelyn SabrosoNo ratings yet

- Legal Form and Ownership SurveyDocument60 pagesLegal Form and Ownership Surveypooja kumariNo ratings yet

- BELONIO QUEENIE ALICABA DoneDocument7 pagesBELONIO QUEENIE ALICABA DoneDaryl OrtizNo ratings yet

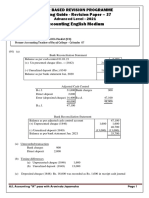

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- Corporation Code Part 4 - Title IV Powers of A CorporationDocument11 pagesCorporation Code Part 4 - Title IV Powers of A CorporationJynxNo ratings yet

- Marketing The New Venture: OutlineDocument41 pagesMarketing The New Venture: OutlineAnkit SinghNo ratings yet

- Essentials of Entrepreneurship and Small Business Management 9th Edition Scarborough Test BankDocument20 pagesEssentials of Entrepreneurship and Small Business Management 9th Edition Scarborough Test Banksarahhant7t86100% (23)

- How To Get Powerful Testimonials That SellDocument10 pagesHow To Get Powerful Testimonials That SellMobile MentorNo ratings yet

- Com502 Getubig-1te4Document2 pagesCom502 Getubig-1te4EastNo ratings yet

- Ch03 - The Environment and Corporate CultureDocument28 pagesCh03 - The Environment and Corporate CultureRISRIS RISMAYANINo ratings yet

- Literature ReviewDocument2 pagesLiterature ReviewLokesh SharmaNo ratings yet

- Special TopicsDocument89 pagesSpecial TopicsPeter Banjao100% (2)

- Generic 5S ChecklistDocument2 pagesGeneric 5S Checklistswamireddy100% (1)

- Field inspection plan for structural steel erectionDocument1 pageField inspection plan for structural steel erectionDelta akathehusky100% (1)

- ACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamDocument41 pagesACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamNathalie Faye TajaNo ratings yet

- Janice Suyo MergedDocument23 pagesJanice Suyo MergedLolzNo ratings yet

- Economics of Strategy (Rješenja)Document227 pagesEconomics of Strategy (Rješenja)Antonio Hrvoje ŽupićNo ratings yet

- PPB Module A Retail and Wholesale Banking ProductsDocument17 pagesPPB Module A Retail and Wholesale Banking Productskamalray75_188704880No ratings yet

- Simple 9/30 Moving Average Trading StrategyDocument3 pagesSimple 9/30 Moving Average Trading StrategybhushanNo ratings yet

- Strategic Management First ActivityDocument3 pagesStrategic Management First ActivityGio DaleNo ratings yet