You might also like

- Follow Up QuestionsDocument27 pagesFollow Up QuestionsVishal PoduriNo ratings yet

- STEEM2 2021 Financial Modeling - Power Asset V1.1Document46 pagesSTEEM2 2021 Financial Modeling - Power Asset V1.1Oussama El Alami El HassaniNo ratings yet

- Clase 14 ITAM Financial Statements & Models Otoño 2017Document25 pagesClase 14 ITAM Financial Statements & Models Otoño 2017Gabriel Ruiz HerreraNo ratings yet

- The Corporate Objective Function: Saeid Samiei Portsmouth Business SchoolDocument72 pagesThe Corporate Objective Function: Saeid Samiei Portsmouth Business SchoolAnshul MishraNo ratings yet

- Value CreationDocument71 pagesValue CreationSolNo ratings yet

- Surakarta, 2010: Didiek S. Wiyono, ST, MTDocument15 pagesSurakarta, 2010: Didiek S. Wiyono, ST, MTvestereverNo ratings yet

- Introduction To Corporate FinanceDocument17 pagesIntroduction To Corporate Financem.gerryNo ratings yet

- Understanding Financial StatementsDocument32 pagesUnderstanding Financial StatementsLuis FernandezNo ratings yet

- Chapters 1 and 2Document36 pagesChapters 1 and 2Qing ShiNo ratings yet

- Research SupportDocument28 pagesResearch SupportVikãsh MishrâNo ratings yet

- Lecture 1.1 - SlidesDocument20 pagesLecture 1.1 - Slidessfalcao91No ratings yet

- Analysis of Reformulated Financial StatementsDocument46 pagesAnalysis of Reformulated Financial StatementsAkib Mahbub KhanNo ratings yet

- CCRA Session 1Document20 pagesCCRA Session 1VISHAL PATILNo ratings yet

- Ch. 1-3Document29 pagesCh. 1-3UjangNo ratings yet

- Introduction To Corporate FinanceDocument29 pagesIntroduction To Corporate FinanceYee Mon AungNo ratings yet

- FinTree - FRA Sixty Minute Guide PDFDocument38 pagesFinTree - FRA Sixty Minute Guide PDFkamleshNo ratings yet

- MGT 101 Financial Accounting: Chapter - 17Document36 pagesMGT 101 Financial Accounting: Chapter - 17itz ZaynNo ratings yet

- IntroductionDocument11 pagesIntroductionGokul BansalNo ratings yet

- Exam 1 Review Slides February 25 2022Document89 pagesExam 1 Review Slides February 25 2022bobNo ratings yet

- Understanding Balance SheetsDocument26 pagesUnderstanding Balance SheetsAli AhmedNo ratings yet

- Rps Bahan Ajar 9Document62 pagesRps Bahan Ajar 9GundamSeedNo ratings yet

- 03 - Introduction To BFDocument25 pages03 - Introduction To BFBilal Khan BangashNo ratings yet

- Chapter 4Document65 pagesChapter 4임재영No ratings yet

- (SAPP Academy) Tóm Tắt Kiến Thức Quan Trọng Môn FAF3 ACCADocument201 pages(SAPP Academy) Tóm Tắt Kiến Thức Quan Trọng Môn FAF3 ACCAhuyentran phamNo ratings yet

- Understanding and Analyzing Financial Statements: School of Inspired LeadershipDocument17 pagesUnderstanding and Analyzing Financial Statements: School of Inspired LeadershipSachin YadavNo ratings yet

- CF (Collected)Document76 pagesCF (Collected)Akhi Junior JMNo ratings yet

- Others 1667194749455Document17 pagesOthers 1667194749455Techboy RahulNo ratings yet

- SAP Financial Planning v1.0Document42 pagesSAP Financial Planning v1.0edoardo.dellaferreraNo ratings yet

- Three Basic Accounting Statements:: - Income StatementDocument14 pagesThree Basic Accounting Statements:: - Income Statementamedina8131No ratings yet

- Slides s2 PDFDocument43 pagesSlides s2 PDFWellington DanielNo ratings yet

- Session 1 - Introduction to Accounting and Balance SheetDocument32 pagesSession 1 - Introduction to Accounting and Balance Sheethieucaiminh155No ratings yet

- AFA2e Chapter03 PPTDocument50 pagesAFA2e Chapter03 PPTIzzy BNo ratings yet

- A 1 Financial StatementsDocument7 pagesA 1 Financial Statementsmohit0503No ratings yet

- Accounting..... All Questions & Answer.Document13 pagesAccounting..... All Questions & Answer.MehediNo ratings yet

- Primer Equit-I 2020Document13 pagesPrimer Equit-I 2020Meera CNo ratings yet

- Enterp7a Financial MGMTDocument17 pagesEnterp7a Financial MGMTVanessa Tattao IsagaNo ratings yet

- ACT201 Chap001 NBNDocument18 pagesACT201 Chap001 NBNAudity PaulNo ratings yet

- FSAPreRead 210728 102848Document42 pagesFSAPreRead 210728 102848Anuj PrajapatiNo ratings yet

- Group Reporting II: Application of The Acquisition Method Under IFRS 3Document77 pagesGroup Reporting II: Application of The Acquisition Method Under IFRS 3Hà PhươngNo ratings yet

- AD1101 AY15 - 16 Sem 1 Lecture 1Document21 pagesAD1101 AY15 - 16 Sem 1 Lecture 1weeeeeshNo ratings yet

- FRA DossierDocument94 pagesFRA DossierRNo ratings yet

- jp02 Financial-Statements - BWDocument2 pagesjp02 Financial-Statements - BWJinwon KimNo ratings yet

- Lecture 3 - Slide-Deck of Pre-Recorded VideosDocument31 pagesLecture 3 - Slide-Deck of Pre-Recorded VideosYaonik HimmatramkaNo ratings yet

- Introduction To AccountingDocument23 pagesIntroduction To AccountingArkar.myanmar 2018No ratings yet

- Chapter 1 Introduction To FSADocument11 pagesChapter 1 Introduction To FSALuu Nhat MinhNo ratings yet

- Group Reporting II: Application of The Acquisition Method Under IFRS 3Document77 pagesGroup Reporting II: Application of The Acquisition Method Under IFRS 3فهد التويجريNo ratings yet

- Accounting For NPOsDocument16 pagesAccounting For NPOsMUSUNGU ANTONYNo ratings yet

- Session 1 An Overview of Corporate FinanceDocument16 pagesSession 1 An Overview of Corporate Financekrishna priyaNo ratings yet

- Module 2 - Assessing Financial Health of The Firm - Week 2 4Document14 pagesModule 2 - Assessing Financial Health of The Firm - Week 2 4maelyn calindongNo ratings yet

- Accounting For Business: Asso. Prof. Dr. Nguyen Thi Phuong HoaDocument37 pagesAccounting For Business: Asso. Prof. Dr. Nguyen Thi Phuong HoaTam DoNo ratings yet

- Overview MKDocument12 pagesOverview MKRelfi DevaNo ratings yet

- 1 Introduction To Corporate FinanceDocument18 pages1 Introduction To Corporate FinanceABHINAV AGRAWALNo ratings yet

- Investment Management: CAFTA WebinarDocument38 pagesInvestment Management: CAFTA WebinarAryan PandeyNo ratings yet

- chp4 SBMDocument28 pageschp4 SBMMercury's PlaceNo ratings yet

- 2Q - Fabm 2Document7 pages2Q - Fabm 2Alexandra Norin RodriguezNo ratings yet

- Financial Statements and Business DecisionsDocument37 pagesFinancial Statements and Business DecisionsHARMAN SINGHNo ratings yet

- ch1 Slides Students - ANDocument24 pagesch1 Slides Students - ANakshitnagpal9119No ratings yet

- Chapter 5 Review Questions and ProblemsDocument11 pagesChapter 5 Review Questions and ProblemsLars FriasNo ratings yet

- Financial Management: DR Yen Chen Topic 1: Financial Manager Reading: Brealey Ch.1Document22 pagesFinancial Management: DR Yen Chen Topic 1: Financial Manager Reading: Brealey Ch.1charithNo ratings yet

- Fig. 2.4bDocument1 pageFig. 2.4bSaurabh AwatiNo ratings yet

- e e e f F F (t) h h* i i J k k L L m MGY n r r R S t T T X x x = 0.01X, on condition that x ≤ 0.2. ω η λ β nDocument1 pagee e e f F F (t) h h* i i J k k L L m MGY n r r R S t T T X x x = 0.01X, on condition that x ≤ 0.2. ω η λ β nSaurabh AwatiNo ratings yet

- Figure 1. Breakdown of An Appliance Which Includes A Refrigeration System, With Its ModulesDocument1 pageFigure 1. Breakdown of An Appliance Which Includes A Refrigeration System, With Its ModulesSaurabh AwatiNo ratings yet

- Calculating reliability targets for mechanical systems using accelerated life testingDocument1 pageCalculating reliability targets for mechanical systems using accelerated life testingSaurabh AwatiNo ratings yet

- Metals 2019, 9, 38: Mech. Eng. 2015, 8, 222-234Document1 pageMetals 2019, 9, 38: Mech. Eng. 2015, 8, 222-234Saurabh AwatiNo ratings yet

- Financial Reporting and Analysis - Session 5 & 6 Financial Statements Analysis (Chapter No 22)Document43 pagesFinancial Reporting and Analysis - Session 5 & 6 Financial Statements Analysis (Chapter No 22)Saurabh AwatiNo ratings yet

- Lot of DtatDocument1 pageLot of DtatSaurabh AwatiNo ratings yet

- Improving Reliability of Mechanical Components That Fail Due to Repetitive StressDocument1 pageImproving Reliability of Mechanical Components That Fail Due to Repetitive StressSaurabh AwatiNo ratings yet

- A 3Document1 pageA 3Saurabh AwatiNo ratings yet

- Building: The Job No Leader Should DelegateDocument1 pageBuilding: The Job No Leader Should DelegateSaurabh AwatiNo ratings yet

- Revision of Session 5Document1 pageRevision of Session 5Saurabh AwatiNo ratings yet

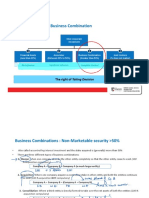

- Complete Control: Business Combination: The Right of Taking DecisionDocument17 pagesComplete Control: Business Combination: The Right of Taking DecisionSaurabh AwatiNo ratings yet

- Session 4Document1 pageSession 4Saurabh AwatiNo ratings yet

- Session 4Document1 pageSession 4Saurabh AwatiNo ratings yet

- Leaders Should Delegate Effectively to Develop TalentDocument1 pageLeaders Should Delegate Effectively to Develop TalentSaurabh AwatiNo ratings yet

- Session 3Document1 pageSession 3Saurabh AwatiNo ratings yet

- Building Block 3:: - Choosing The Sustainable Competitive AdvantageDocument1 pageBuilding Block 3:: - Choosing The Sustainable Competitive AdvantageSaurabh AwatiNo ratings yet

- Session 3Document1 pageSession 3Saurabh AwatiNo ratings yet

- Session 3Document1 pageSession 3Saurabh AwatiNo ratings yet

- Leaders: Don't Delegate Job Placements Without Careful ConsiderationDocument1 pageLeaders: Don't Delegate Job Placements Without Careful ConsiderationSaurabh AwatiNo ratings yet

- The Job No Leader Should Delegate: Choosing People for Competitive AdvantageDocument1 pageThe Job No Leader Should Delegate: Choosing People for Competitive AdvantageSaurabh AwatiNo ratings yet

- Session 6 Recap: Corporate, Business, Marketing, Financial, R&D StrategiesDocument1 pageSession 6 Recap: Corporate, Business, Marketing, Financial, R&D StrategiesSaurabh AwatiNo ratings yet

- Session 4Document1 pageSession 4Saurabh AwatiNo ratings yet

- SessionDocument1 pageSessionSaurabh AwatiNo ratings yet

- Getting Right People in The Right Jobs: Building Block 3: The Job No Leader Should DelegateDocument1 pageGetting Right People in The Right Jobs: Building Block 3: The Job No Leader Should DelegateSaurabh AwatiNo ratings yet

- Building Block 3: The Job No Leader Should Delegate (Cont... )Document1 pageBuilding Block 3: The Job No Leader Should Delegate (Cont... )Saurabh AwatiNo ratings yet

- Leaders: Don't Delegate Job Placements Without Careful ConsiderationDocument1 pageLeaders: Don't Delegate Job Placements Without Careful ConsiderationSaurabh AwatiNo ratings yet

- SessionDocument1 pageSessionSaurabh AwatiNo ratings yet

- SessionDocument1 pageSessionSaurabh AwatiNo ratings yet

- Atty Suspended for Certifying Deed with Dead SignatoriesDocument4 pagesAtty Suspended for Certifying Deed with Dead Signatoriesmondaytuesday17No ratings yet

- Republic Vs SerranoDocument2 pagesRepublic Vs SerranoArahbellsNo ratings yet

- role of the allama iqbal in the creation of pakistanDocument2 pagesrole of the allama iqbal in the creation of pakistandeadson03No ratings yet

- TM-3534 AVEVA 12-1 - Diagrams AdministrationDocument108 pagesTM-3534 AVEVA 12-1 - Diagrams AdministrationWelingtonMoraesNo ratings yet

- As Que Ftca 21.05.2022Document5 pagesAs Que Ftca 21.05.2022AmirdavarshiniNo ratings yet

- Midterms Gov AccountingDocument72 pagesMidterms Gov AccountingEloisa JulieanneNo ratings yet

- Cadastral Act ReviewerDocument2 pagesCadastral Act ReviewerArla Agrupis100% (1)

- Question On Oliver With Answer (1-29)Document12 pagesQuestion On Oliver With Answer (1-29)hoda69% (13)

- L/epublit Of: TBT BtlippintgDocument8 pagesL/epublit Of: TBT BtlippintgCesar ValeraNo ratings yet

- q57-52 Derivatives, Week10, ch29Document30 pagesq57-52 Derivatives, Week10, ch29s yanNo ratings yet

- Skripsi: Implementasi Kebijakan Disiplin Pegawai Negeri Sipil Di Distrik Navigasi Kelas I PalembangDocument25 pagesSkripsi: Implementasi Kebijakan Disiplin Pegawai Negeri Sipil Di Distrik Navigasi Kelas I PalembangsichluzNo ratings yet

- Heirs of Spouses Teofilo M. Reterta and Elisa Reterta vs. Spouses Lorenzo Mores and Virginia Lopez, 655 SCRA 580, August 17, 2011Document20 pagesHeirs of Spouses Teofilo M. Reterta and Elisa Reterta vs. Spouses Lorenzo Mores and Virginia Lopez, 655 SCRA 580, August 17, 2011TNVTRLNo ratings yet

- Tax.3105 - Capital Asset VS Ordinary Asset and CGTDocument10 pagesTax.3105 - Capital Asset VS Ordinary Asset and CGTZee QBNo ratings yet

- ANMs Multi Purpose Health Assistant (Female) (GR III) PDFDocument31 pagesANMs Multi Purpose Health Assistant (Female) (GR III) PDFNIKHIL MODINo ratings yet

- Devin Kelley Report of Trial 5.3.2018Document610 pagesDevin Kelley Report of Trial 5.3.2018AmmoLand Shooting Sports NewsNo ratings yet

- Assignment OF: Competition LawDocument3 pagesAssignment OF: Competition Lawaruba ansariNo ratings yet

- FULL Download Ebook PDF International Corporate Governance by Marc Goergen PDF EbookDocument37 pagesFULL Download Ebook PDF International Corporate Governance by Marc Goergen PDF Ebookdwayne.lancaster40797% (30)

- 18 Financial StatementsDocument35 pages18 Financial Statementswsahmed28No ratings yet

- Munit Blue Manual 1.8 enDocument21 pagesMunit Blue Manual 1.8 engiambi-1No ratings yet

- Engineering Report - Chemical Anchor Suspended Glass Pemasangan Angkur Samping (H 5 M, 2 FTRS M10 + FIS VS)Document10 pagesEngineering Report - Chemical Anchor Suspended Glass Pemasangan Angkur Samping (H 5 M, 2 FTRS M10 + FIS VS)Febrinaldo HidayahNo ratings yet

- Bar GlassesDocument31 pagesBar GlassesLyka GazminNo ratings yet

- 2019 - Pooja - Social Media Ethical Challenges PDFDocument15 pages2019 - Pooja - Social Media Ethical Challenges PDFNeha sharmaNo ratings yet

- Volume 42, Issue 5 - February 4, 2011Document48 pagesVolume 42, Issue 5 - February 4, 2011BladeNo ratings yet

- WEB Threat AssessmentDocument3 pagesWEB Threat AssessmentWilliam N. GriggNo ratings yet

- Computer Age Management Services LimitedDocument1 pageComputer Age Management Services LimitedAbhishek JainNo ratings yet

- C C CC CCC !"#C CDocument4 pagesC C CC CCC !"#C CmojagminaNo ratings yet

- How I LAWFULLY Claimed 4 Houses Free and ClearDocument75 pagesHow I LAWFULLY Claimed 4 Houses Free and ClearSonof Godd100% (4)

- Table of CourtsDocument21 pagesTable of CourtsFakhri AzimNo ratings yet

- S06 e 1 Usha DeepDocument3 pagesS06 e 1 Usha DeepVinay SrivastavaNo ratings yet