You might also like

- Reasonable Expectations of Financial Statement UsersDocument13 pagesReasonable Expectations of Financial Statement UsersKaiWenNgNo ratings yet

- Political Standards: Corporate Interest, Ideology, and Leadership in the Shaping of Accounting Rules for the Market EconomyFrom EverandPolitical Standards: Corporate Interest, Ideology, and Leadership in the Shaping of Accounting Rules for the Market EconomyNo ratings yet

- Deegan Financial Accounting Theory - Deegan (1) - 62Document1 pageDeegan Financial Accounting Theory - Deegan (1) - 62Putri Arinda JeniantiNo ratings yet

- ACCT 372 Lecture 3 The Regulation of Financial AccountingDocument23 pagesACCT 372 Lecture 3 The Regulation of Financial AccountingDustin SmytheNo ratings yet

- Question 1 (15 Marks)Document11 pagesQuestion 1 (15 Marks)Li XiangNo ratings yet

- Discuss The Arguments For and Against Regulating The Financial Reporting SystemDocument9 pagesDiscuss The Arguments For and Against Regulating The Financial Reporting SystemArasen அரசன் பழனியாண்டி100% (10)

- Accounting Theory Chapter on Financial Reporting StandardsDocument12 pagesAccounting Theory Chapter on Financial Reporting StandardskateNo ratings yet

- IFRS Harmonization and Disclosure ChallengesDocument9 pagesIFRS Harmonization and Disclosure ChallengesJaashwne100% (1)

- IFRS Adoption Impact on Firm Risk and Earnings VolatilityDocument7 pagesIFRS Adoption Impact on Firm Risk and Earnings Volatilityabrori100% (1)

- Question 1 A 0b SolutionsDocument3 pagesQuestion 1 A 0b SolutionsAhmed Hussain100% (1)

- Scott Im Ch12Document37 pagesScott Im Ch12Icha YasmineNo ratings yet

- Accounting Policy Caveat Market ReactionDocument4 pagesAccounting Policy Caveat Market ReactionKristian TronikNo ratings yet

- ACT301 Week 6 Tutorial PDFDocument4 pagesACT301 Week 6 Tutorial PDFjulia chengNo ratings yet

- Topic 1 Suggested Review SolutionsDocument3 pagesTopic 1 Suggested Review SolutionsHoudet ElaineNo ratings yet

- BKAF 3083 Tutorial 2 Group G-4Document5 pagesBKAF 3083 Tutorial 2 Group G-4Alex YeapNo ratings yet

- Free Market Perspective on Accounting RegulationDocument3 pagesFree Market Perspective on Accounting RegulationAditya Nur PrasetyoNo ratings yet

- Financial Accounting Theory and Reporting Practices (BKAF5053)Document13 pagesFinancial Accounting Theory and Reporting Practices (BKAF5053)hajiagwaggo100% (2)

- Next 4Document10 pagesNext 4Nurhasanah Asyari100% (1)

- The Future of Accounting and Disclosure in An Evolving WorldDocument13 pagesThe Future of Accounting and Disclosure in An Evolving WorldAhmad RijalNo ratings yet

- Chapter 3 Applying Theory To AccountingDocument12 pagesChapter 3 Applying Theory To AccountingMbinjNo ratings yet

- Reforming Accounting Rules to Limit Systemic RiskDocument15 pagesReforming Accounting Rules to Limit Systemic Riskmaheld2007No ratings yet

- Accounts NotesDocument15 pagesAccounts NotessharadkulloliNo ratings yet

- 1 Advanced Financial AccountingDocument2 pages1 Advanced Financial AccountingashibhallauNo ratings yet

- Financial and Managerial Accounting StandardsDocument5 pagesFinancial and Managerial Accounting Standardsstarfish12No ratings yet

- Module 1 Financial Accounting For MBAs - 6th EditionDocument15 pagesModule 1 Financial Accounting For MBAs - 6th EditionjoshNo ratings yet

- Chapter 3 - Accounting Regulation and Politics A. Free Market PerspectiveDocument4 pagesChapter 3 - Accounting Regulation and Politics A. Free Market PerspectivenajaneNo ratings yet

- Financial Reporting Assignment 1Document2 pagesFinancial Reporting Assignment 1Peh Shao WeiNo ratings yet

- Audit and society: The changing role of auditorsDocument3 pagesAudit and society: The changing role of auditorsmayhemclubNo ratings yet

- 2nd Resume Alvianty 18102067 AS-BDocument9 pages2nd Resume Alvianty 18102067 AS-BAlviantyNo ratings yet

- Financial Accounting and Accounting StandardsDocument16 pagesFinancial Accounting and Accounting StandardsJayakrishna BommasamudramNo ratings yet

- Role of Accounting Standards and IFRS in Financial ReportingDocument5 pagesRole of Accounting Standards and IFRS in Financial ReportingTIZITAW MASRESHA100% (1)

- Accounting Concept and Principles - 20160822Document32 pagesAccounting Concept and Principles - 20160822jnyamandeNo ratings yet

- Dec 050512 Ob 02Document20 pagesDec 050512 Ob 02veemaswNo ratings yet

- Principles-Based Accounting Standards: A Message From The Ceos of The International Audit NetworksDocument23 pagesPrinciples-Based Accounting Standards: A Message From The Ceos of The International Audit NetworksdeividtobonNo ratings yet

- Accounting Concepts and Principles ExplainedDocument4 pagesAccounting Concepts and Principles ExplainedNicoleMendozaNo ratings yet

- Essay Type DDocument19 pagesEssay Type D丁昕No ratings yet

- Article 090ad - 1424502201Document32 pagesArticle 090ad - 1424502201henfaNo ratings yet

- Advanced Financial Reporting and Theory 26325 Module Leader: Pat MouldDocument8 pagesAdvanced Financial Reporting and Theory 26325 Module Leader: Pat MouldKaran ChopraNo ratings yet

- TUTORIAL SOLUTIONS (Week 1B)Document4 pagesTUTORIAL SOLUTIONS (Week 1B)PeterNo ratings yet

- UntitledDocument10 pagesUntitledCARLOS DELIGERO III (Caloy)No ratings yet

- Acc Theory Question Assignment 3Document13 pagesAcc Theory Question Assignment 3Stephanie HerlambangNo ratings yet

- Limited Attention Information DisclosureDocument59 pagesLimited Attention Information Disclosureanon_154643438No ratings yet

- An Effective Corporate Governance Framework Requires A Sound LegalDocument31 pagesAn Effective Corporate Governance Framework Requires A Sound LegalNigist WoldeselassieNo ratings yet

- Case Study - 1Document5 pagesCase Study - 1Jordan BimandamaNo ratings yet

- UK Study Finds Costly Accounting Overrides Harm PerformanceDocument30 pagesUK Study Finds Costly Accounting Overrides Harm PerformancerNo ratings yet

- Accounting Standard ResumeDocument7 pagesAccounting Standard ResumeIvana YustitiaNo ratings yet

- The Public Interest Theory, and The Interest Group Theory. The First Theory SuggestsDocument5 pagesThe Public Interest Theory, and The Interest Group Theory. The First Theory SuggestssaadNo ratings yet

- Accounting Theory AssignDocument13 pagesAccounting Theory AssignNana Okyere Boa TeneNo ratings yet

- The Greater Emphasis On The Conceptual FrameworkDocument10 pagesThe Greater Emphasis On The Conceptual FrameworkMuh Niswar AdhyatmaNo ratings yet

- A Conceptual Framework For Financial Accounting and ReportingDocument70 pagesA Conceptual Framework For Financial Accounting and ReportingAyesha ZakiNo ratings yet

- AAS CH1 2 1 - MergedDocument19 pagesAAS CH1 2 1 - MergedRoel PaisteNo ratings yet

- Analyzing Financial Statements for Business ValuationDocument5 pagesAnalyzing Financial Statements for Business ValuationDardan BalajNo ratings yet

- Chapter 06 - Answer PDFDocument6 pagesChapter 06 - Answer PDFjhienellNo ratings yet

- TUTORIAL SOLUTIONS (Week 2A)Document3 pagesTUTORIAL SOLUTIONS (Week 2A)PeterNo ratings yet

- ACCT 10001 Accounting Reports & Analysis Review Questions - Topic 1 Chapter 1: Introduction To Accounting and Business Decision MakingDocument5 pagesACCT 10001 Accounting Reports & Analysis Review Questions - Topic 1 Chapter 1: Introduction To Accounting and Business Decision MakingHui Ying LimNo ratings yet

- Assessment Ii,,,,prince's GroupDocument14 pagesAssessment Ii,,,,prince's GroupTafadzwaNo ratings yet

- Effective Financial Reporting and Auditing Importance and LimitationsDocument5 pagesEffective Financial Reporting and Auditing Importance and LimitationsŞtefania FcSbNo ratings yet

- The Case For Accounting Regulation: A Theoretical Approach: SearchDocument5 pagesThe Case For Accounting Regulation: A Theoretical Approach: SearchbabylovelylovelyNo ratings yet

- SBR 2020 NotesDocument39 pagesSBR 2020 NotesGlebNo ratings yet

- Week 2 Tutorial QuestionsDocument2 pagesWeek 2 Tutorial QuestionsChand DivneshNo ratings yet

- Week 2 Tutorial SolutionDocument3 pagesWeek 2 Tutorial SolutionChand DivneshNo ratings yet

- Week 2 Tutorial SolutionDocument3 pagesWeek 2 Tutorial SolutionChand DivneshNo ratings yet

- Af 201 Forum 2Document1 pageAf 201 Forum 2Chand DivneshNo ratings yet

- Week 2 Tutorial SolutionDocument3 pagesWeek 2 Tutorial SolutionChand DivneshNo ratings yet

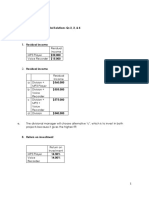

- USP Accounting and Finance AF201 Mid-Semester TestDocument10 pagesUSP Accounting and Finance AF201 Mid-Semester TestChand DivneshNo ratings yet

- Week 3 Tutorial Question Refer To Godfrey Chapter 2 Part A Questions: 5, 8,13, 14 (From Godfrey Textbook) Part BDocument1 pageWeek 3 Tutorial Question Refer To Godfrey Chapter 2 Part A Questions: 5, 8,13, 14 (From Godfrey Textbook) Part BChand DivneshNo ratings yet

- Week 4 Tutorial SolutionDocument1 pageWeek 4 Tutorial SolutionChand DivneshNo ratings yet

- Week 4 Tutorial Question Refer To Deegan Chapter 3 Part A Questions: 3.2, 3.10, 3.19, 3.24 (From Deegan Textbook) Part BDocument1 pageWeek 4 Tutorial Question Refer To Deegan Chapter 3 Part A Questions: 3.2, 3.10, 3.19, 3.24 (From Deegan Textbook) Part BChand DivneshNo ratings yet

- AF201 revision package final exam S2 2020Document12 pagesAF201 revision package final exam S2 2020Chand DivneshNo ratings yet

- Af201 Mid-Semester Test Outline s1, 2021 Online ModeDocument4 pagesAf201 Mid-Semester Test Outline s1, 2021 Online ModeChand DivneshNo ratings yet

- Fiji Airways launches direct Suva-Apia flightsDocument4 pagesFiji Airways launches direct Suva-Apia flightsChand DivneshNo ratings yet

- Week 9: Tutorial 08 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Document3 pagesWeek 9: Tutorial 08 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNo ratings yet

- Project Scope Management TutorialDocument1 pageProject Scope Management TutorialChand DivneshNo ratings yet

- AF201Final Exam - Suggested Solution - s1, 2019 - Final Qs 2, 3, 4Document3 pagesAF201Final Exam - Suggested Solution - s1, 2019 - Final Qs 2, 3, 4Chand DivneshNo ratings yet

- S2 2019 FINAL EXAM Q3-4 PARTIALDocument2 pagesS2 2019 FINAL EXAM Q3-4 PARTIALChand DivneshNo ratings yet

- AF201 Final Exam - Suggested Solution - s1, 2018 - Final Qs 1, 2, 3Document2 pagesAF201 Final Exam - Suggested Solution - s1, 2018 - Final Qs 1, 2, 3Chand DivneshNo ratings yet

- Tutorial 04 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Document2 pagesTutorial 04 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNo ratings yet

- Af201 Final Exam Revision Package - S2, 2020 Face-to-Face & Blended Modes Suggested Partial SolutionsDocument9 pagesAf201 Final Exam Revision Package - S2, 2020 Face-to-Face & Blended Modes Suggested Partial SolutionsChand DivneshNo ratings yet

- Project Scope Management TutorialDocument1 pageProject Scope Management TutorialChand DivneshNo ratings yet

- Week 9: Tutorial 08 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Document3 pagesWeek 9: Tutorial 08 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNo ratings yet

- Tutorial 09: Questions With Possible SolutionsDocument4 pagesTutorial 09: Questions With Possible SolutionsChand DivneshNo ratings yet

- Mid-Semester Exam: Af 302 - Information SystemsDocument14 pagesMid-Semester Exam: Af 302 - Information SystemsChand DivneshNo ratings yet

- AF210 Unit 4 Tutorial SolutionsDocument5 pagesAF210 Unit 4 Tutorial SolutionsChand DivneshNo ratings yet

- Tutorial 05 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Document3 pagesTutorial 05 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNo ratings yet

- Tutorial 03: Questions With Partial SolutionsDocument4 pagesTutorial 03: Questions With Partial SolutionsChand DivneshNo ratings yet

- AF302 SEMESTER 1 – 2017 MID-TEST SOLUTIONSDocument9 pagesAF302 SEMESTER 1 – 2017 MID-TEST SOLUTIONSChand DivneshNo ratings yet

- Strategic Project Management TutorialDocument3 pagesStrategic Project Management TutorialShretha RamNo ratings yet

- Unit 4 - Reviewed - Recorded PDFDocument11 pagesUnit 4 - Reviewed - Recorded PDFRajneetChandNo ratings yet

- Tutorial 01 Questions With Possible SolutionsDocument3 pagesTutorial 01 Questions With Possible SolutionsChand DivneshNo ratings yet

- Ker & Co, Ltd. LingadDocument1 pageKer & Co, Ltd. Lingadamareia yapNo ratings yet

- Series-A Investment Opportunity: International Payments Service ProviderDocument3 pagesSeries-A Investment Opportunity: International Payments Service ProviderDhiraj KhotNo ratings yet

- SUDIPDocument1 pageSUDIPSai Kumar SedmakiNo ratings yet

- Part Five - Maintaining and Retaining Human ResourcesDocument34 pagesPart Five - Maintaining and Retaining Human ResourcesMehari Yohannes Hailemariam100% (3)

- 201014GMMGlobalReportXiaomi Team5 FinalDocument31 pages201014GMMGlobalReportXiaomi Team5 FinalStella Avinca TantraNo ratings yet

- Banco Filipino v. Monetary Board Liquidation Authority CaseDocument2 pagesBanco Filipino v. Monetary Board Liquidation Authority CasexxxaaxxxNo ratings yet

- Migrating Lotus Notes Applications To SharePointDocument8 pagesMigrating Lotus Notes Applications To SharePointparvesh2001No ratings yet

- Test Bank For International Business Environments Operations 14 e 14th Edition John Daniels Lee Radebaugh Daniel SullivanDocument26 pagesTest Bank For International Business Environments Operations 14 e 14th Edition John Daniels Lee Radebaugh Daniel Sullivannataliebuckdbpnrtjfsa100% (24)

- Aditya Premkumar: Professional SummaryDocument3 pagesAditya Premkumar: Professional SummaryDivya NinaweNo ratings yet

- New Kyung Dong Bus Schedule from Yongsan to Osan and HumphreysDocument2 pagesNew Kyung Dong Bus Schedule from Yongsan to Osan and HumphreysClair AllenNo ratings yet

- Fast TrackDocument45 pagesFast TrackSAUMYA MNo ratings yet

- Full Download Management Accounting Information For Decision Making and Strategy Execution Atkinson 6th Edition Test Bank PDF Full ChapterDocument36 pagesFull Download Management Accounting Information For Decision Making and Strategy Execution Atkinson 6th Edition Test Bank PDF Full Chaptersloppy.obsidian.v8ovu100% (18)

- Constitution of IndiaDocument7 pagesConstitution of IndiaRITIKANo ratings yet

- Ferguson v. Countrywide Credit Industries, Inc.Document2 pagesFerguson v. Countrywide Credit Industries, Inc.crlstinaaa100% (3)

- DronesStartupLandscapeGlobal 192 26-Jul-2016 PDFDocument255 pagesDronesStartupLandscapeGlobal 192 26-Jul-2016 PDFprodigy1000% (1)

- Expression of Interest (Consultancy) (BDC)Document4 pagesExpression of Interest (Consultancy) (BDC)Brave zizNo ratings yet

- 10.1007@978 3 030 31646 4 PDFDocument363 pages10.1007@978 3 030 31646 4 PDFUncleleo100% (2)

- A. UNIQLO ProductDocument10 pagesA. UNIQLO ProductHải Đoànnn100% (1)

- Indian Labour Market Outline: Regional Dimension and Employment StatusDocument11 pagesIndian Labour Market Outline: Regional Dimension and Employment StatusAnurag JayswalNo ratings yet

- English 2 - Directions Vocabulary - MapDocument3 pagesEnglish 2 - Directions Vocabulary - MapMariana MirandaNo ratings yet

- Ch01 Introduction To SPMDocument35 pagesCh01 Introduction To SPMShrutismita MishraNo ratings yet

- Comparative Balance SheetDocument8 pagesComparative Balance Sheet1028No ratings yet

- Apple Capital StructureDocument4 pagesApple Capital Structurekevin kipkemoiNo ratings yet

- MGT211 Assignment 1 Solution Spring 2021Document5 pagesMGT211 Assignment 1 Solution Spring 2021Beaming Kids Model schoolNo ratings yet

- American Friends Final ShowDocument23 pagesAmerican Friends Final Showmoses njengaNo ratings yet

- Tvs Motor Company LimitedDocument10 pagesTvs Motor Company LimitedFakrudeen Ali Ahamed PNo ratings yet

- Data & Analytics Lead Consultant ProfileDocument5 pagesData & Analytics Lead Consultant ProfileAjay KumarNo ratings yet

- N-LC-01 Bank of America v. CADocument2 pagesN-LC-01 Bank of America v. CAKobe Lawrence VeneracionNo ratings yet

- Abstracti ON: (Using Our Illustrative Problem, The Labahan Laundry Services, The FollowingDocument11 pagesAbstracti ON: (Using Our Illustrative Problem, The Labahan Laundry Services, The FollowingAkosi NoynoypiNo ratings yet

- Unit 4 High Rise BuildingsDocument22 pagesUnit 4 High Rise BuildingsInfanta mary100% (3)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Business Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsFrom EverandBusiness Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsNo ratings yet

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Emprender un Negocio: Paso a Paso Para PrincipiantesFrom EverandEmprender un Negocio: Paso a Paso Para PrincipiantesRating: 3 out of 5 stars3/5 (1)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)