You might also like

- UsedcarDocument145 pagesUsedcarTim LaneNo ratings yet

- DR Gundry's Diet EvolutionDocument6 pagesDR Gundry's Diet EvolutionAlberto Cortes86% (22)

- 65 High Paying Affiliate Programs PDFDocument25 pages65 High Paying Affiliate Programs PDFMonty001100% (1)

- Get Your Ex Back NowDocument10 pagesGet Your Ex Back NowTim Lane100% (1)

- Candle Making Niche Report: Legal Disclaimer & Affiliate OpportunitiesDocument31 pagesCandle Making Niche Report: Legal Disclaimer & Affiliate OpportunitiesTim Lane100% (1)

- The Holistic Self Assessment 2 15 18Document36 pagesThe Holistic Self Assessment 2 15 18Tim Lane100% (2)

- A Course On Tarot DivinationDocument98 pagesA Course On Tarot DivinationAd LibNo ratings yet

- TQNDocument33 pagesTQNArry Rachman100% (1)

- Living ConsciouslyDocument2 pagesLiving ConsciouslyJimmy HendersonNo ratings yet

- Understanding Self Components of Self Self Concept Self Confidence Self Image Sabnam BasuDocument28 pagesUnderstanding Self Components of Self Self Concept Self Confidence Self Image Sabnam BasuRoldan Dela CruzNo ratings yet

- To Disrupt, Discredit and DestroyDocument89 pagesTo Disrupt, Discredit and DestroyMorpheus42100% (1)

- Max Pot GuideDocument23 pagesMax Pot GuideCharlieeMIFNo ratings yet

- Event Prep Carol SpecialDocument6 pagesEvent Prep Carol SpecialzbhabhaNo ratings yet

- Brochure MMDocument2 pagesBrochure MMMichel MathieuNo ratings yet

- The Success Codes Pocket Guide The Success Codes Pocket GuideDocument31 pagesThe Success Codes Pocket Guide The Success Codes Pocket GuideMirsada SijamicNo ratings yet

- Manifesting True SuccessDocument38 pagesManifesting True Successmarianaluca100% (1)

- The Marriage PlanDocument2 pagesThe Marriage Planejbaugh100% (1)

- Defining Spirituality/Religion: Symptom ManagementDocument3 pagesDefining Spirituality/Religion: Symptom ManagementGeorgie IbabaoNo ratings yet

- Your First 500+ Subscribers... 100% FREE!: Fast, Free & Easy List BuildingDocument34 pagesYour First 500+ Subscribers... 100% FREE!: Fast, Free & Easy List BuildingTim LaneNo ratings yet

- MINDFULNESS-BASED RELAPSE PREVENTION PROGRAMDocument43 pagesMINDFULNESS-BASED RELAPSE PREVENTION PROGRAMTheresa DimaanoNo ratings yet

- Credit CollectionDocument22 pagesCredit CollectionCassyDelaRosaNo ratings yet

- Building Internal Harmony with Yoga: The Heart ChakraDocument2 pagesBuilding Internal Harmony with Yoga: The Heart ChakraKimberley A HughesNo ratings yet

- The Infinite Benefits of MindfulnessDocument11 pagesThe Infinite Benefits of MindfulnessSreeja SujithNo ratings yet

- Money Mindset Mastery: Week 4 - Clearing The Money BlocksDocument4 pagesMoney Mindset Mastery: Week 4 - Clearing The Money BlocksChannel SignageNo ratings yet

- HOLISTIC COLLABORATION Series: Connecting Poetry - Body and Soul Nutrition: Holistic Collaboration, #1From EverandHOLISTIC COLLABORATION Series: Connecting Poetry - Body and Soul Nutrition: Holistic Collaboration, #1No ratings yet

- Shift Your Energy PDFDocument11 pagesShift Your Energy PDFAdrian DanNo ratings yet

- Idea Masterclass:: How To Come Up With A Great Idea For Your Online Business!Document10 pagesIdea Masterclass:: How To Come Up With A Great Idea For Your Online Business!Tim LaneNo ratings yet

- Angelic Plan For ProsperityDocument74 pagesAngelic Plan For ProsperityArchil GlurjidzeNo ratings yet

- Your Official Online Training Guide: 4 Simple Tips To Get The Most Out of This Live SessionDocument5 pagesYour Official Online Training Guide: 4 Simple Tips To Get The Most Out of This Live SessionAndre SenabNo ratings yet

- STRESS MANAGEMENT PROGRAM - Seminar MaterialsDocument6 pagesSTRESS MANAGEMENT PROGRAM - Seminar MaterialsAlvin P. ManuguidNo ratings yet

- Ilonah Jean Tiodianco Activity 3Document5 pagesIlonah Jean Tiodianco Activity 3Ewan Mary Rose GalagalaNo ratings yet

- ISSA Professional Nutrition Coach How To Use These FormsDocument10 pagesISSA Professional Nutrition Coach How To Use These FormsAlexandra AresNo ratings yet

- 03 Budgeting and Your Financial HealthDocument75 pages03 Budgeting and Your Financial Healthlight247_1993100% (1)

- Edible Wild Plants of West Michigan Volume 1 PDFDocument12 pagesEdible Wild Plants of West Michigan Volume 1 PDFmrh0867No ratings yet

- 7 Ways To Begin Living Smarter: Build and Protect Your Wealth With Agora FinancialDocument9 pages7 Ways To Begin Living Smarter: Build and Protect Your Wealth With Agora FinancialTim LaneNo ratings yet

- Tip Sheet Teacher Self CareDocument4 pagesTip Sheet Teacher Self Careapi-254290610No ratings yet

- Kundalini Reiki 1Document12 pagesKundalini Reiki 1anivallNo ratings yet

- 3 Day Soul Alignment Initiation PDFDocument4 pages3 Day Soul Alignment Initiation PDFNikolina MårkoviNo ratings yet

- SMART Goal Template for Setting Clear ObjectivesDocument2 pagesSMART Goal Template for Setting Clear ObjectivesCristina GrigoreNo ratings yet

- Counterparty Credit Risk, Funding, Collateral and Capital, PDFDocument12 pagesCounterparty Credit Risk, Funding, Collateral and Capital, PDFOsama Shaheen0% (1)

- Performance Measurement ETFDocument32 pagesPerformance Measurement ETFbylenNo ratings yet

- The Stoic Handbook™Document14 pagesThe Stoic Handbook™skillzaal100% (1)

- How To Appy Holistic Care Talk 24Document22 pagesHow To Appy Holistic Care Talk 24Syifa FatiyaNo ratings yet

- 15 Budgeting TipsDocument13 pages15 Budgeting TipsWhel DeLima ConsueloNo ratings yet

- Coaching101pdf PDFDocument39 pagesCoaching101pdf PDFTim LaneNo ratings yet

- PMP Formulae: Earned Value ManagementDocument4 pagesPMP Formulae: Earned Value ManagementOmerZiaNo ratings yet

- 5 Secrets To Manifesting Your Own Destiny Author GlobeCoRe, Inc. - Psychological Global Consulting ServicesDocument8 pages5 Secrets To Manifesting Your Own Destiny Author GlobeCoRe, Inc. - Psychological Global Consulting Servicesهمسات رجل بالخمسينNo ratings yet

- Lover RETURN System 12Document11 pagesLover RETURN System 12CigebDias1982No ratings yet

- Alphabetical List of ProverbsDocument7 pagesAlphabetical List of Proverbsuyuayie100% (2)

- How to Build Habits and Achieve Goals by Understanding Your Brain's PathwaysDocument7 pagesHow to Build Habits and Achieve Goals by Understanding Your Brain's PathwaysMehdi TouahriNo ratings yet

- 1910Document2 pages1910Mohsin Khan50% (2)

- Breaking Limitations - Brand Avatar ReportDocument7 pagesBreaking Limitations - Brand Avatar ReportArsal Khan100% (1)

- Identify Your Stress Level and Your Key Stressors PDFDocument14 pagesIdentify Your Stress Level and Your Key Stressors PDFMyOdysseyNo ratings yet

- Noeleen Auto Mall LTD Recently Completed An Initial Public OfferingDocument1 pageNoeleen Auto Mall LTD Recently Completed An Initial Public OfferingHassan JanNo ratings yet

- Emotions Body MapDocument2 pagesEmotions Body MapGeraldine MatiasNo ratings yet

- Manage Yourself and Lead OthersDocument10 pagesManage Yourself and Lead OthersAhmad AlMowaffakNo ratings yet

- Characteristics of The Ten Bodies - 3HO FoundationDocument8 pagesCharacteristics of The Ten Bodies - 3HO FoundationBorisNo ratings yet

- Guided Meditation On Relative BodhcittaDocument14 pagesGuided Meditation On Relative Bodhcittaplgv2000No ratings yet

- Sweetheart I'm Pregnant The Miracle of ProcreationDocument57 pagesSweetheart I'm Pregnant The Miracle of ProcreationSannie Remotin100% (1)

- Teachings of Phra Ajahn Surasak KhemarangsiDocument66 pagesTeachings of Phra Ajahn Surasak KhemarangsiAstusNo ratings yet

- Meditation and Reiki PrinciplesDocument7 pagesMeditation and Reiki Principlesapi-3723602No ratings yet

- ASBB 02 - Energy Management Is KeyDocument17 pagesASBB 02 - Energy Management Is KeygmeadesNo ratings yet

- Healing of Memories: BridgesDocument12 pagesHealing of Memories: BridgesKoreen Torio Mangalao-BaculiNo ratings yet

- Positive Thinking Through Bach Flower RemediesDocument364 pagesPositive Thinking Through Bach Flower RemediesZvonko Šuljak100% (1)

- Guided Workbook PreviewDocument6 pagesGuided Workbook PreviewsusyNo ratings yet

- Peer Counseling Programs Research Paper StarterDocument9 pagesPeer Counseling Programs Research Paper StarterJoe J. LamNo ratings yet

- Stress & Stress Management: Produced by Klinic Community Health CentreDocument31 pagesStress & Stress Management: Produced by Klinic Community Health CentreVinay ShuklaNo ratings yet

- Essential Oils Components As A New Path To Understand Ion ChannelDocument5 pagesEssential Oils Components As A New Path To Understand Ion ChannelCarol Carvalho CorreiaNo ratings yet

- Quantum KineDocument16 pagesQuantum KineGianna Barcelli FantappieNo ratings yet

- Motivational Interviewing: Helping People Make ChangesDocument40 pagesMotivational Interviewing: Helping People Make Changesapi-130253013No ratings yet

- Prayer To ArchangelsDocument1 pagePrayer To ArchangelsnageshsriramNo ratings yet

- Get Your Inner Power Back!: Blueprint to Stop Binge Eating Taking over Your Life While Reconnecting with Your SoulFrom EverandGet Your Inner Power Back!: Blueprint to Stop Binge Eating Taking over Your Life While Reconnecting with Your SoulNo ratings yet

- Be in One Peace: Essential Skills for Thriving in the New WorldFrom EverandBe in One Peace: Essential Skills for Thriving in the New WorldNo ratings yet

- FreeReport Claim Your SpotlightDocument19 pagesFreeReport Claim Your SpotlightTim LaneNo ratings yet

- ImmunitionDocument14 pagesImmunitionTim LaneNo ratings yet

- Buyers GuideDocument24 pagesBuyers GuideTim LaneNo ratings yet

- The Simple Life by Cliff Hsia PDFDocument22 pagesThe Simple Life by Cliff Hsia PDFTim LaneNo ratings yet

- Looking For Extra IncomeDocument12 pagesLooking For Extra IncomeTim LaneNo ratings yet

- 4 Day Cash Machine EXPOSED - Swipe FilesDocument9 pages4 Day Cash Machine EXPOSED - Swipe FilesTim LaneNo ratings yet

- 407-Shane-and-Jocelyn-Sams FlippedlifestyleDocument38 pages407-Shane-and-Jocelyn-Sams FlippedlifestyleTim LaneNo ratings yet

- Understanding Treatments For Gout: ReportsDocument8 pagesUnderstanding Treatments For Gout: ReportsTim LaneNo ratings yet

- FreeReport Claim Your SpotlightDocument19 pagesFreeReport Claim Your SpotlightTim LaneNo ratings yet

- 2014 Chevrolet Captiva Sport New For 2014Document5 pages2014 Chevrolet Captiva Sport New For 2014Tim LaneNo ratings yet

- 5 Little Guys That Got Rich in Bad TimesDocument6 pages5 Little Guys That Got Rich in Bad TimesTim LaneNo ratings yet

- Reading Noah and The Flood Through The Source Theory LensDocument8 pagesReading Noah and The Flood Through The Source Theory LensTim LaneNo ratings yet

- Buyers GuideDocument24 pagesBuyers GuideTim LaneNo ratings yet

- StopLadderClimbing-StartLeaping FINALDocument27 pagesStopLadderClimbing-StartLeaping FINALTim LaneNo ratings yet

- WP BlueprintDocument31 pagesWP BlueprintTim LaneNo ratings yet

- Money Edition EbookDocument37 pagesMoney Edition EbookTim LaneNo ratings yet

- Two Week Meal PlanDocument13 pagesTwo Week Meal PlanTim LaneNo ratings yet

- JVRecruitingDocument25 pagesJVRecruitingTim LaneNo ratings yet

- AVT Natural Products LTD 2014-15Document101 pagesAVT Natural Products LTD 2014-15Anonymous NnVgCXDwNo ratings yet

- Real Estate Finance Presentation PDFDocument10 pagesReal Estate Finance Presentation PDFEsther LeeNo ratings yet

- Black BookDocument41 pagesBlack BookMoazza QureshiNo ratings yet

- Intrinsic Values and Stock Prices PDFDocument2 pagesIntrinsic Values and Stock Prices PDFPhil Singleton100% (1)

- S & P 500 IndexDocument4 pagesS & P 500 IndexAastha TandonNo ratings yet

- Turning Point Brands: Release Date: 10 July 2019Document24 pagesTurning Point Brands: Release Date: 10 July 2019Anonymous 2nAj0N9MxqNo ratings yet

- Finance Chapter 18Document35 pagesFinance Chapter 18courtdubs100% (1)

- Finance and Treasury Centre Incentive: Singapore Economic Development Board ("EDB") WWW - Edb.gov - SGDocument2 pagesFinance and Treasury Centre Incentive: Singapore Economic Development Board ("EDB") WWW - Edb.gov - SGK58-ANH 2-KTDN NGUYỄN THỊ PHƯƠNG THẢONo ratings yet

- FBAR Cases: Prosecution For Failure To Declare Foreign Bank Accounts To The US TreasuryDocument432 pagesFBAR Cases: Prosecution For Failure To Declare Foreign Bank Accounts To The US TreasurypunktlichNo ratings yet

- Topic 1 Financial EnvironmentDocument26 pagesTopic 1 Financial EnvironmentThorapioMayNo ratings yet

- Walter's Model and Gordon's Theory on Dividend PolicyDocument15 pagesWalter's Model and Gordon's Theory on Dividend PolicyEviya Jerrin KoodalyNo ratings yet

- Module 11-Inventory Cost FlowDocument8 pagesModule 11-Inventory Cost FlowCreative BeautyNo ratings yet

- Policy Value Calculation and Recursive FormulasDocument44 pagesPolicy Value Calculation and Recursive FormulasĐặng Thị TrâmNo ratings yet

- Gitman 4e Ch. 2 SPR - SolDocument8 pagesGitman 4e Ch. 2 SPR - SolDaniel Joseph SitoyNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- Accounting for Tax Amnesty Assets and LiabilitiesDocument13 pagesAccounting for Tax Amnesty Assets and LiabilitiesHeriyanto MonmonNo ratings yet

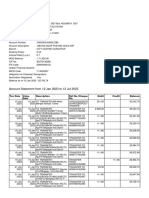

- Account Statement From 12 Jan 2023 To 12 Jul 2023Document10 pagesAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyNo ratings yet

- 2011 National Corn Yield GuideDocument48 pages2011 National Corn Yield GuideNational Corn Growers AssociationNo ratings yet

- MD Shohag Al-Mamun MBS ACMADocument6 pagesMD Shohag Al-Mamun MBS ACMATaslima AktarNo ratings yet

- FTFM - Final - MagandaDocument573 pagesFTFM - Final - MagandaJewelyn C. Espares-CioconNo ratings yet

- ACC622 Assignment 2021Document5 pagesACC622 Assignment 2021Nosisa SithebeNo ratings yet

- SFO Feb11Document96 pagesSFO Feb11AbgreenNo ratings yet

- Mortgage Lab Signature AssignmentDocument15 pagesMortgage Lab Signature Assignmentapi-385294359No ratings yet

- General Elective Course List SEMESTER 1, 2021 Hanoi Campus: Please Click For Course Guide InformationDocument3 pagesGeneral Elective Course List SEMESTER 1, 2021 Hanoi Campus: Please Click For Course Guide InformationQuynh NguyenNo ratings yet

- FABM 1.module 5 PDFDocument34 pagesFABM 1.module 5 PDFSHIERY MAE FALCONITINNo ratings yet

- NCR Tranche177 061121 (ND)Document39 pagesNCR Tranche177 061121 (ND)Bryan LebasnonNo ratings yet