You might also like

- Chapter 07 AnsDocument5 pagesChapter 07 AnsDave Manalo100% (1)

- AainvtyDocument4 pagesAainvtyRodolfo SayangNo ratings yet

- Quiz 5 Acc 401Document10 pagesQuiz 5 Acc 401EML0% (1)

- CH 02 PDFDocument24 pagesCH 02 PDFAurcus JumskieNo ratings yet

- Manny Company: Required: Compute For The Balances of The Following On December 31, 2X14Document4 pagesManny Company: Required: Compute For The Balances of The Following On December 31, 2X14MauiNo ratings yet

- Local Media271226407970108268Document17 pagesLocal Media271226407970108268Jana Rose PaladaNo ratings yet

- TaxationDocument7 pagesTaxationDorothy ApolinarioNo ratings yet

- Joint and By-Product CostingDocument13 pagesJoint and By-Product CostingErlinda NavalloNo ratings yet

- AE 17 M8 ExercisesDocument46 pagesAE 17 M8 ExercisesKim FloresNo ratings yet

- Accounting Changes and ErrorsDocument3 pagesAccounting Changes and ErrorsJohn Emerson PatricioNo ratings yet

- Handout 1.0 ACC 123 Practice Problems For Cost Concepts and Cost BehaviorDocument2 pagesHandout 1.0 ACC 123 Practice Problems For Cost Concepts and Cost BehaviorFrancine Thea M. LantayaNo ratings yet

- Chapter 14 Advacc2Document58 pagesChapter 14 Advacc2Aimee DyingNo ratings yet

- Chapter 4 Caselette Audit of ReceivablesDocument37 pagesChapter 4 Caselette Audit of ReceivablesXXXXXXXXXXXXXXXXXXNo ratings yet

- Chapter 2 Problems - IADocument8 pagesChapter 2 Problems - IAKimochi SenpaiiNo ratings yet

- Labor Variance: By: Group 2Document24 pagesLabor Variance: By: Group 2Kris BayronNo ratings yet

- 1617 1stS MX NBergonia RevDocument11 pages1617 1stS MX NBergonia RevJames Louis BarcenasNo ratings yet

- Code of EthicsDocument54 pagesCode of EthicsPeter BanjaoNo ratings yet

- Chapter 15 Amended With AnswersDocument6 pagesChapter 15 Amended With AnswersIbn FaridNo ratings yet

- Solution Chapter 13Document22 pagesSolution Chapter 13xxxxxxxxx100% (3)

- Final Proj Sy2022-23 Agrigulay Corp.Document4 pagesFinal Proj Sy2022-23 Agrigulay Corp.Jan Elaine CalderonNo ratings yet

- What A ProblemDocument4 pagesWhat A ProblemEleazar SalazarNo ratings yet

- 221 ExamsDocument10 pages221 ExamsElla Mae AgoniaNo ratings yet

- Audit of Other Income Statement ComponentsDocument7 pagesAudit of Other Income Statement ComponentsIbratama Sukses PratamaNo ratings yet

- ch4 Solution21Document25 pagesch4 Solution21Melinda Amelia0% (1)

- On January 1 Accounintg ProlbemDocument3 pagesOn January 1 Accounintg Prolbemelsana philipNo ratings yet

- Quiz 3 Problem SolvingDocument7 pagesQuiz 3 Problem SolvingChristine Joyce BascoNo ratings yet

- Answer Value 800000Document1 pageAnswer Value 800000Kath LeynesNo ratings yet

- INVESTMENTSDocument9 pagesINVESTMENTSKrisan RiveraNo ratings yet

- An SME Prepared The Following Post Closing Trial Balance at YearDocument1 pageAn SME Prepared The Following Post Closing Trial Balance at YearRaca DesuNo ratings yet

- Assignment 2Document3 pagesAssignment 2Sajid RulesNo ratings yet

- Intermediate Accounting I Investment in Associate Part 2Document3 pagesIntermediate Accounting I Investment in Associate Part 2Fery AnnNo ratings yet

- Mahusay-Bsa-315-Module 3-CaseletsDocument15 pagesMahusay-Bsa-315-Module 3-CaseletsJeth MahusayNo ratings yet

- Father Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)Document10 pagesFather Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)marygraceomacNo ratings yet

- The Partnership of Frick, Wilson, and Clarke Has Elected To Cease All Operations and Liquidate Its Business PropertyDocument7 pagesThe Partnership of Frick, Wilson, and Clarke Has Elected To Cease All Operations and Liquidate Its Business PropertyKailash KumarNo ratings yet

- Biological AssetDocument2 pagesBiological AssetMary Dale Joie BocalaNo ratings yet

- Far TB2Document195 pagesFar TB2MarieJoiaNo ratings yet

- Cash and Acrrual Basis QUIZDocument2 pagesCash and Acrrual Basis QUIZMarii M.100% (1)

- MAS 2017 01 Management Accounting Concepts Techniques For Planning and ControlDocument5 pagesMAS 2017 01 Management Accounting Concepts Techniques For Planning and ControlMitch Delgado EmataNo ratings yet

- B. Woods Chapter 15Document42 pagesB. Woods Chapter 15Ludia Daniel100% (1)

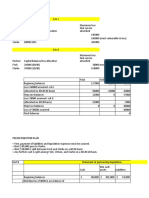

- Atlas Retail Company Analysis of Prepaid Expense AccountDocument5 pagesAtlas Retail Company Analysis of Prepaid Expense AccountEizzel SamsonNo ratings yet

- Ia3 BSDocument5 pagesIa3 BSMary Joy CabilNo ratings yet

- Auditing Problems1Document45 pagesAuditing Problems1Ronnel TagalogonNo ratings yet

- Borrowing Cost (PAS 23)Document6 pagesBorrowing Cost (PAS 23)CharléNo ratings yet

- Chapter 15 PDFDocument5 pagesChapter 15 PDFRenzo RamosNo ratings yet

- Practical Accounting 2Document4 pagesPractical Accounting 2Steph BorinagaNo ratings yet

- Standard Quantity Standard Price Standard or Rate CostDocument4 pagesStandard Quantity Standard Price Standard or Rate CostRabie HarounNo ratings yet

- 8904 - Partnership LiquidationDocument4 pages8904 - Partnership Liquidationxara mizpahNo ratings yet

- OR1Document135 pagesOR1Shresth BhatiaNo ratings yet

- M36 - Quizzer 1 PDFDocument8 pagesM36 - Quizzer 1 PDFJoshua DaarolNo ratings yet

- Chapter 5Document11 pagesChapter 5Ro-Anne LozadaNo ratings yet

- Problem: I - Statement of Affairs and Deficiency AccountDocument1 pageProblem: I - Statement of Affairs and Deficiency AccountAnn Marie GabayNo ratings yet

- IA2 Pre Finals 2Document4 pagesIA2 Pre Finals 2Cy CyNo ratings yet

- Partnerships Liquidation: Advanced Accounting, Fifth EditionDocument33 pagesPartnerships Liquidation: Advanced Accounting, Fifth Editionhasan jabrNo ratings yet

- Retrospectively in The First Set of Financial Statements Authorized For Issue AfterDocument7 pagesRetrospectively in The First Set of Financial Statements Authorized For Issue Aftermax pNo ratings yet

- 1235Document3 pages1235Alexis AlipudoNo ratings yet

- Advanced Accounting Baker Test Bank - Chap004Document56 pagesAdvanced Accounting Baker Test Bank - Chap004donkazotey90% (10)

- Chapter 4 - Test BankDocument21 pagesChapter 4 - Test Bankgilli1tr80% (5)

- 12 y 72Document5 pages12 y 72Alexis AlipudoNo ratings yet

- Chapter 04 Consolidation of Wholly Owned Subsidiaries: Answer KeyDocument31 pagesChapter 04 Consolidation of Wholly Owned Subsidiaries: Answer KeyAurcus JumskieNo ratings yet

- Chapter 5 - Test BankDocument17 pagesChapter 5 - Test Bankhipduggy100% (2)

- CASE ANALYSIS - Don Masters and Assoicates Law OfficeDocument1 pageCASE ANALYSIS - Don Masters and Assoicates Law OfficeMelanie Samsona0% (1)

- Financial Statement Analysis ExerciseDocument5 pagesFinancial Statement Analysis ExerciseMelanie SamsonaNo ratings yet

- Samsona-Case-Act 122 5 - 3GDocument4 pagesSamsona-Case-Act 122 5 - 3GMelanie Samsona100% (2)

- Specialized Industry HospitalDocument44 pagesSpecialized Industry HospitalMelanie SamsonaNo ratings yet

- Case Analysis - Hockey Camp-CvpDocument2 pagesCase Analysis - Hockey Camp-CvpMelanie SamsonaNo ratings yet

- 5TH ActivityDocument15 pages5TH ActivityMelanie SamsonaNo ratings yet

- FilmmakingDocument10 pagesFilmmakingMelanie Samsona100% (1)

- CombinepdfDocument3 pagesCombinepdfMelanie SamsonaNo ratings yet

- Case Analysis - Hockey Camp-CvpDocument2 pagesCase Analysis - Hockey Camp-CvpMelanie Samsona100% (1)

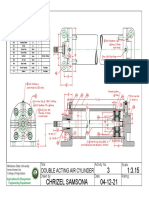

- Double Acting Air CylinderDocument1 pageDouble Acting Air CylinderMelanie SamsonaNo ratings yet

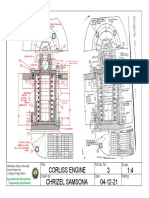

- Corliss EngineDocument1 pageCorliss EngineMelanie SamsonaNo ratings yet

- Module 4 Estate Taxation 3Document4 pagesModule 4 Estate Taxation 3Melanie SamsonaNo ratings yet

- Stress: Normal Stress Shearing Stress Bearing StressDocument23 pagesStress: Normal Stress Shearing Stress Bearing StressMelanie SamsonaNo ratings yet

- Impact of Time On StudentsDocument10 pagesImpact of Time On StudentsMelanie SamsonaNo ratings yet

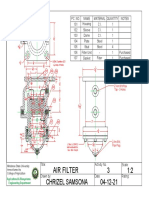

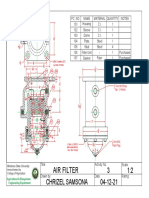

- Air FilterDocument1 pageAir FilterMelanie SamsonaNo ratings yet

- Impact of Time On Students' Academic PerformanceDocument14 pagesImpact of Time On Students' Academic PerformanceMelanie SamsonaNo ratings yet

- STRAINDocument30 pagesSTRAINMelanie SamsonaNo ratings yet

- Grade 11-TVL 3 Aviso 2018-2019Document42 pagesGrade 11-TVL 3 Aviso 2018-2019Melanie SamsonaNo ratings yet

- Senior High School Electronic Class Record: InstructionsDocument39 pagesSenior High School Electronic Class Record: InstructionsMelanie SamsonaNo ratings yet

- Koronadal National Comprehensive High School-Senior High SchoolDocument60 pagesKoronadal National Comprehensive High School-Senior High SchoolMelanie SamsonaNo ratings yet

- Stress: Normal Stress Shearing Stress Bearing StressDocument79 pagesStress: Normal Stress Shearing Stress Bearing StressMelanie Samsona100% (1)

- ENS 164 SyllabusDocument1 pageENS 164 SyllabusMelanie SamsonaNo ratings yet

- TORSIONDocument25 pagesTORSIONMelanie SamsonaNo ratings yet

- Grade 11-Abm 3 HamiltonDocument45 pagesGrade 11-Abm 3 HamiltonMelanie SamsonaNo ratings yet

- Happy MeDocument1 pageHappy MeMelanie SamsonaNo ratings yet

- ABE051 - 2nd MAjor ExamDocument1 pageABE051 - 2nd MAjor ExamMelanie SamsonaNo ratings yet

- Agricultural and Biosystems Engineering Department: College of AgricultureDocument1 pageAgricultural and Biosystems Engineering Department: College of AgricultureMelanie SamsonaNo ratings yet

- ENS 181 - Seatwork No. 1 - Samsona - A1Document1 pageENS 181 - Seatwork No. 1 - Samsona - A1Melanie SamsonaNo ratings yet

- Module 4 Estate Taxation 2Document4 pagesModule 4 Estate Taxation 2Melanie SamsonaNo ratings yet

- ENS181 Seatwork 10 - Samsona - A1Document12 pagesENS181 Seatwork 10 - Samsona - A1Melanie SamsonaNo ratings yet

- TermsKFS 7652940900Document11 pagesTermsKFS 7652940900pankajprajapati000078666No ratings yet

- Process Flow Diagram (For Subscribers Who Visits Merchant Business Premises)Document2 pagesProcess Flow Diagram (For Subscribers Who Visits Merchant Business Premises)Lovelyn ArokhamoniNo ratings yet

- 09 Assignment SolutionsDocument2 pages09 Assignment SolutionsAhmed Ameen Nour EldinNo ratings yet

- 7 ElevenDocument9 pages7 ElevenJoshua TingabngabNo ratings yet

- PFRS 9Document7 pagesPFRS 9Carissa CestinaNo ratings yet

- IX. Directory of BEML's Officers and Employees: Chairman and Managing DirectorDocument4 pagesIX. Directory of BEML's Officers and Employees: Chairman and Managing Directoraman33270% (1)

- 35TH Annual Report MRLDocument61 pages35TH Annual Report MRLmayankNo ratings yet

- Status of Primary Market Response in Nepal: Jas Bahadur GurungDocument13 pagesStatus of Primary Market Response in Nepal: Jas Bahadur GurungSonam ShahNo ratings yet

- Marketing ManagementDocument22 pagesMarketing ManagementMakungu ShirindaNo ratings yet

- Soa 0457Document4 pagesSoa 0457Sunil SDNo ratings yet

- Bill of LadingDocument1 pageBill of LadingboyNo ratings yet

- BOB Revised Service ChargesDocument36 pagesBOB Revised Service ChargesKulbhushan SinghNo ratings yet

- Microeconomics (Monopoly, CH 10)Document32 pagesMicroeconomics (Monopoly, CH 10)Vikram SharmaNo ratings yet

- DEPSDocument2 pagesDEPSvietdung25112003No ratings yet

- London JetsDocument346 pagesLondon JetsQwertyNo ratings yet

- Olmstead Corporation S Capital Structure Is As Follows The Following Additional InformationDocument1 pageOlmstead Corporation S Capital Structure Is As Follows The Following Additional InformationHassan JanNo ratings yet

- Dealers Perception About Sanghi CementnewDocument10 pagesDealers Perception About Sanghi CementnewpujanswetalNo ratings yet

- 2007 Budget Statement and Economic Policy of GhanaDocument508 pages2007 Budget Statement and Economic Policy of GhanaFuaad DodooNo ratings yet

- BS Delhi 22-02-2024Document20 pagesBS Delhi 22-02-2024Lokesh KatalNo ratings yet

- Anthem GroupDocument3 pagesAnthem GroupRebuild BoholNo ratings yet

- Buscom Quiz: Book Value Fair ValueDocument2 pagesBuscom Quiz: Book Value Fair ValueNairah M. TambieNo ratings yet

- Logistics 1Document36 pagesLogistics 1Quỳnh Nguyễn NhưNo ratings yet

- Unit 7Document18 pagesUnit 7ShubhamkumarsharmaNo ratings yet

- RE Appt of Successor Trustee 8-31-2011 With Detailed ExplanationDocument14 pagesRE Appt of Successor Trustee 8-31-2011 With Detailed ExplanationAlice Jean Logan100% (2)

- Louie Anne Lim - 09 Quiz 1Document1 pageLouie Anne Lim - 09 Quiz 1Louie Anne LimNo ratings yet

- Lesson 3 Customer Relationship ManagementDocument36 pagesLesson 3 Customer Relationship ManagementKyla Mae Fulache LevitaNo ratings yet

- International Economics 8th Edition Appleyard Solutions ManualDocument25 pagesInternational Economics 8th Edition Appleyard Solutions ManualMariaHowelloatq100% (56)

- Global Business EnvironmentDocument15 pagesGlobal Business EnvironmentSANDEEP SINGH63% (8)

- Consumer Information:: Name: Date of Birth: GenderDocument3 pagesConsumer Information:: Name: Date of Birth: GendermohitNo ratings yet

- Unit 1 MCQDocument7 pagesUnit 1 MCQHan Nwe OoNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!From EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Rating: 4.5 out of 5 stars4.5/5 (8)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Excel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsFrom EverandExcel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsNo ratings yet

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitFrom EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitRating: 4.5 out of 5 stars4.5/5 (9)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- The Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackFrom EverandThe Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackRating: 1 out of 5 stars1/5 (1)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Your First CFO: The Accounting Cure for Small Business OwnersFrom EverandYour First CFO: The Accounting Cure for Small Business OwnersRating: 4 out of 5 stars4/5 (2)

- Project Control Methods and Best Practices: Achieving Project SuccessFrom EverandProject Control Methods and Best Practices: Achieving Project SuccessNo ratings yet

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Attention Pays: How to Drive Profitability, Productivity, and AccountabilityFrom EverandAttention Pays: How to Drive Profitability, Productivity, and AccountabilityNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Accounting All-in-One For Dummies, with Online PracticeFrom EverandAccounting All-in-One For Dummies, with Online PracticeRating: 3 out of 5 stars3/5 (1)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)