You might also like

- SSRN-id3122480 4Document20 pagesSSRN-id3122480 4Amin SonoghurNo ratings yet

- Role of Civil Society Institutions in Promoting Diversity and PluDocument5 pagesRole of Civil Society Institutions in Promoting Diversity and PluAmin SonoghurNo ratings yet

- Asset-Based Microfinance For Microenterprises: Evidence From PakistanDocument46 pagesAsset-Based Microfinance For Microenterprises: Evidence From PakistanAmin SonoghurNo ratings yet

- SSRN-id3122480 4Document20 pagesSSRN-id3122480 4Amin SonoghurNo ratings yet

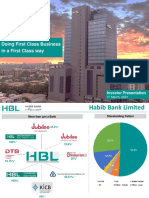

- Doing First Class Business in A First Class Way: Investor PresentationDocument25 pagesDoing First Class Business in A First Class Way: Investor PresentationAmin SonoghurNo ratings yet

- District Profile MalakandDocument15 pagesDistrict Profile MalakandAmin SonoghurNo ratings yet

- What Is Means of Literature? Sources of Literature Review?Document11 pagesWhat Is Means of Literature? Sources of Literature Review?Amin SonoghurNo ratings yet

- BS Lecture 5... Industrial Policy GeneralDocument21 pagesBS Lecture 5... Industrial Policy GeneralAmin SonoghurNo ratings yet

- WSN 141 (2020) 115-131Document17 pagesWSN 141 (2020) 115-131Amin SonoghurNo ratings yet

- Analysis of The Impact of Economic Growth On Income Inequality and Poverty in South Africa: The Case of Mpumalanga ProvinceDocument8 pagesAnalysis of The Impact of Economic Growth On Income Inequality and Poverty in South Africa: The Case of Mpumalanga ProvinceAmin SonoghurNo ratings yet

- BS Lecture 3.... Industrial ConcentrationDocument31 pagesBS Lecture 3.... Industrial ConcentrationAmin SonoghurNo ratings yet

- District Profile MalakandDocument15 pagesDistrict Profile MalakandAmin SonoghurNo ratings yet

- Effect of COVID PandemicDocument2 pagesEffect of COVID PandemicAmin SonoghurNo ratings yet

- Singapore's Industrial Policy Lessons for Busan on Cultivating CompetitivenessDocument24 pagesSingapore's Industrial Policy Lessons for Busan on Cultivating CompetitivenessAmin SonoghurNo ratings yet

- Why Nations Fail Daren Acemoglu and James A. RobinsonDocument14 pagesWhy Nations Fail Daren Acemoglu and James A. RobinsonAmin SonoghurNo ratings yet

- Lecture 1 How To Select Appropriate Topic For ResearchDocument11 pagesLecture 1 How To Select Appropriate Topic For ResearchAmin SonoghurNo ratings yet

- Singapore's Industrial Policy Lessons for Busan on Cultivating CompetitivenessDocument24 pagesSingapore's Industrial Policy Lessons for Busan on Cultivating CompetitivenessAmin SonoghurNo ratings yet

- Effect of COVID PandemicDocument2 pagesEffect of COVID PandemicAmin SonoghurNo ratings yet

- Tahir AzadDocument1 pageTahir AzadAmin SonoghurNo ratings yet

- Unit Root TestsDocument2 pagesUnit Root TestsAmin SonoghurNo ratings yet

- Analysis of The Impact of Economic Growth On Income Inequality and Poverty in South Africa: The Case of Mpumalanga ProvinceDocument8 pagesAnalysis of The Impact of Economic Growth On Income Inequality and Poverty in South Africa: The Case of Mpumalanga ProvinceAmin SonoghurNo ratings yet

- AminDocument4 pagesAminAmin SonoghurNo ratings yet

- AminDocument5 pagesAminAmin SonoghurNo ratings yet

- AminDocument4 pagesAminAmin SonoghurNo ratings yet

- ISlamic HistoryDocument9 pagesISlamic HistoryAmin SonoghurNo ratings yet

- AminDocument4 pagesAminAmin SonoghurNo ratings yet

- AminDocument4 pagesAminAmin SonoghurNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CPA Quantitative Techniques Notes: Probability Theory and DistributionsDocument8 pagesCPA Quantitative Techniques Notes: Probability Theory and DistributionsCaesarKamanziNo ratings yet

- Jawaban Soal Latihan Bab 4 - 6 BiostatistikaDocument94 pagesJawaban Soal Latihan Bab 4 - 6 BiostatistikaDennis SuhardiniNo ratings yet

- Professional Engineer Competency StandardDocument18 pagesProfessional Engineer Competency StandardMohammad Shoaib DanishNo ratings yet

- Bca Sy SyllabusDocument27 pagesBca Sy SyllabusomssNo ratings yet

- VTU Model Question Paper 18EC44 1Document3 pagesVTU Model Question Paper 18EC44 1Sandeep RNo ratings yet

- EDA and Hypothesis Testing On KC Housing Data: Daniele Sammarco - Exploratory Data Analysis For Machine Learning by IBMDocument9 pagesEDA and Hypothesis Testing On KC Housing Data: Daniele Sammarco - Exploratory Data Analysis For Machine Learning by IBMjoeNo ratings yet

- Machine Learning Lecture 1 (UW)Document45 pagesMachine Learning Lecture 1 (UW)Jerome WongNo ratings yet

- Effective Copywriting BlueprintDocument17 pagesEffective Copywriting BlueprintAndy ChauNo ratings yet

- Kajian Tindakan BiDocument33 pagesKajian Tindakan BiKoman SpanarNo ratings yet

- Statistics and Probability Homework SheetDocument4 pagesStatistics and Probability Homework Sheet3milleadNo ratings yet

- Enhancing Mathematical Skills of The Students Through Digi-Tech AppsDocument13 pagesEnhancing Mathematical Skills of The Students Through Digi-Tech Appskeza joy diazNo ratings yet

- Stages of Test Construction and Monitoring Student ProgressDocument3 pagesStages of Test Construction and Monitoring Student ProgressFleur De Liz Jagolino100% (1)

- Local and Global Learning Methods For Predicting Power of A Combined Gas & Steam TurbineDocument7 pagesLocal and Global Learning Methods For Predicting Power of A Combined Gas & Steam TurbineDavid Omar Torres GutierrezNo ratings yet

- 1 Introduction To Biostatistics PDFDocument20 pages1 Introduction To Biostatistics PDFYounas BhattiNo ratings yet

- Writings in Music Theory by James TenneyDocument505 pagesWritings in Music Theory by James Tenneymorphessor100% (3)

- Metropolitan Research Inc. ReportDocument8 pagesMetropolitan Research Inc. ReportYati GuptaNo ratings yet

- Data Science Online TrainingDocument2 pagesData Science Online TrainingPravalika ShineyNo ratings yet

- MM16 Module 1Document13 pagesMM16 Module 1Jayson PajaresNo ratings yet

- Statistical Model For IC50 Determination of Acetylcholinesterase Enzyme For Alzheimer's DiseaseDocument9 pagesStatistical Model For IC50 Determination of Acetylcholinesterase Enzyme For Alzheimer's DiseaseIJPHSNo ratings yet

- Krishna Raj P.M., Ankith Mohan, Srinivasa K.G. - Practical Social Network Analysis With Python-Springer (2018)Document355 pagesKrishna Raj P.M., Ankith Mohan, Srinivasa K.G. - Practical Social Network Analysis With Python-Springer (2018)matirva456No ratings yet

- M1112sp-Ivb - 1,2Document4 pagesM1112sp-Ivb - 1,2chingferdie_111No ratings yet

- Math 204 Final 2017-2018 V2 PDFDocument8 pagesMath 204 Final 2017-2018 V2 PDFJad Abou AssalyNo ratings yet

- Econ1310 ExamDocument15 pagesEcon1310 ExamNick DrysdaleNo ratings yet

- Chap15 Demand Management and ForecastingDocument51 pagesChap15 Demand Management and ForecastingRanbir KapoorNo ratings yet

- Machine Learning Approaches To Condition MonitoringDocument28 pagesMachine Learning Approaches To Condition MonitoringArundas PurakkatNo ratings yet

- Chapter 2-01 Discrete & Continuous Random Variables 12SPIII - A1Document3 pagesChapter 2-01 Discrete & Continuous Random Variables 12SPIII - A1Manilyn Mugatar Mayang100% (2)

- Chapter 5 - Summary, Finding, Conclusions & RecommendationsDocument3 pagesChapter 5 - Summary, Finding, Conclusions & RecommendationsJM NoynayNo ratings yet

- Journal of Statistical Software: Reviewer: Tim Downie Beuth University of Applied Sciences BerlinDocument4 pagesJournal of Statistical Software: Reviewer: Tim Downie Beuth University of Applied Sciences BerlinInfinitum Gym StoreNo ratings yet

- Validity and Internal Consistency of The New Knee Society KneeDocument8 pagesValidity and Internal Consistency of The New Knee Society KneeSantiago Mondragon RiosNo ratings yet

- MBA SyllabusDocument89 pagesMBA SyllabusMAADHAV HAIEBTTENo ratings yet