You might also like

- CF-Cost of CapitalDocument3 pagesCF-Cost of CapitalNoor PervezNo ratings yet

- Chapter 9 Intercompany Bond Holdings and Miscellaneous Topics-Consolidated Financial StatementsDocument45 pagesChapter 9 Intercompany Bond Holdings and Miscellaneous Topics-Consolidated Financial StatementsAchmad RizalNo ratings yet

- Suggested - Answer - CAP - II - June - 2011 4Document64 pagesSuggested - Answer - CAP - II - June - 2011 4Dipen Adhikari100% (1)

- Charging All Costs To Expense When IncurredDocument27 pagesCharging All Costs To Expense When IncurredAnonymous N9dx4ATEghNo ratings yet

- Paper18 Solution PDFDocument24 pagesPaper18 Solution PDFI'm Just FunnyNo ratings yet

- University of Mauritius: Faculty of Law and ManagementDocument9 pagesUniversity of Mauritius: Faculty of Law and ManagementMîñåk ŞhïïNo ratings yet

- Rohit TestDocument9 pagesRohit TestRohitNo ratings yet

- Advanced Accounting 2DDocument5 pagesAdvanced Accounting 2DHarusiNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Preparation of Financial Statements - QBDocument26 pagesPreparation of Financial Statements - QBHindutav arya100% (1)

- Intermediate Accounting IIDocument10 pagesIntermediate Accounting IILexNo ratings yet

- Group - I Paper - 1 Accounting V2 Chapter 2 PDFDocument56 pagesGroup - I Paper - 1 Accounting V2 Chapter 2 PDFShrinivas GirnarNo ratings yet

- 5th Sem Accounts Previous Year PapersDocument25 pages5th Sem Accounts Previous Year PapersViratNo ratings yet

- Exercise Ni ValewDocument4 pagesExercise Ni ValewALMA MORENANo ratings yet

- FR (New) A MTP Final Mar 2021Document17 pagesFR (New) A MTP Final Mar 2021ritz meshNo ratings yet

- ACCT 302 Financial Reporting II Tutorial Set 4-1Document8 pagesACCT 302 Financial Reporting II Tutorial Set 4-1Ohenewaa AppiahNo ratings yet

- 2018 Revision Fin Statements MEMO A1Document3 pages2018 Revision Fin Statements MEMO A1oersoncalebNo ratings yet

- Company Account SuggestionDocument34 pagesCompany Account SuggestionAYAN DATTANo ratings yet

- Corporate Reporting 2012Document4 pagesCorporate Reporting 2012Laskar REAZNo ratings yet

- HKICPA QP Exam (Module A) Feb2006 Question PaperDocument7 pagesHKICPA QP Exam (Module A) Feb2006 Question Papercynthia tsuiNo ratings yet

- Retained Earnings Exercise 19Document3 pagesRetained Earnings Exercise 19Honelyn JuatonNo ratings yet

- FR (New) A MTP Final Apr 2021Document16 pagesFR (New) A MTP Final Apr 2021ritz meshNo ratings yet

- LXL Gr12Accounting 08 Revision Interpretation-of-Financial-Statements 27mar2014 PDFDocument5 pagesLXL Gr12Accounting 08 Revision Interpretation-of-Financial-Statements 27mar2014 PDFNezer Byl P. VergaraNo ratings yet

- Syifa' Maulana-Midterm AKMDocument16 pagesSyifa' Maulana-Midterm AKMSyifak MaulanaNo ratings yet

- The Examiner's Answers F2 - Financial Management March 2013: Section ADocument18 pagesThe Examiner's Answers F2 - Financial Management March 2013: Section Amd salehinNo ratings yet

- Paper - 2: Strategic Financial Management Questions Merger and AcquisitionsDocument27 pagesPaper - 2: Strategic Financial Management Questions Merger and AcquisitionsObaid RehmanNo ratings yet

- FIN501 - Financial Management Mid Term Assignment - Zin Thet Nyo LwinDocument16 pagesFIN501 - Financial Management Mid Term Assignment - Zin Thet Nyo LwinZin Thet InwonderlandNo ratings yet

- CLWY Q1 2019 FinancialsDocument3 pagesCLWY Q1 2019 FinancialskdwcapitalNo ratings yet

- Trabajo de Contabilidad en InglesDocument5 pagesTrabajo de Contabilidad en Inglescarmen viquezNo ratings yet

- EXERCISE Cashflow of The CompanyDocument41 pagesEXERCISE Cashflow of The CompanyDev lakhaniNo ratings yet

- Akuntansi Keuangan 1Document15 pagesAkuntansi Keuangan 1Vincenttio le CloudNo ratings yet

- Accounts Important Questions by Rajat Jain SirDocument31 pagesAccounts Important Questions by Rajat Jain SirRajiv JhaNo ratings yet

- Lesson 5c Pro-Forma Statement of EquityDocument3 pagesLesson 5c Pro-Forma Statement of EquityBEN CLADONo ratings yet

- Case 3Document13 pagesCase 3Prezi Toli100% (1)

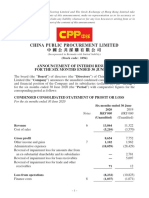

- China Public Procurement Limited 中 國 公 共 採 購 有 限 公 司Document37 pagesChina Public Procurement Limited 中 國 公 共 採 購 有 限 公 司in resNo ratings yet

- Sqpms Accountancy Part2 Xii 2010Document17 pagesSqpms Accountancy Part2 Xii 2010Ujjwal SubbaNo ratings yet

- Q.P. Code: 62202: Managerial AccountingDocument6 pagesQ.P. Code: 62202: Managerial Accountinganshul bhutangeNo ratings yet

- HKICPA QP Exam (Module A) Feb2008 AnswerDocument10 pagesHKICPA QP Exam (Module A) Feb2008 Answercynthia tsui100% (1)

- Consolidation BasicsDocument5 pagesConsolidation Basicspoonamemrith22No ratings yet

- CASH FLOW Revision-1 PDFDocument12 pagesCASH FLOW Revision-1 PDFBHUMIKA JAINNo ratings yet

- Orca Share Media1522073458763 PDFDocument15 pagesOrca Share Media1522073458763 PDFHannah Yncierto100% (1)

- 10Q1Q2012Document131 pages10Q1Q2012Biswa Mohan PatiNo ratings yet

- Standlone Cash Flow StatementDocument2 pagesStandlone Cash Flow StatementVaibhav SìňghNo ratings yet

- 027 Practice Test 09 Accounting Test Solution Subjective Udesh RegularDocument6 pages027 Practice Test 09 Accounting Test Solution Subjective Udesh Regulardeathp006No ratings yet

- 57096bos46250finalnew p1 A PDFDocument18 pages57096bos46250finalnew p1 A PDFAayush LaddhaNo ratings yet

- 01 - Exercises Session 1 - EmptyDocument4 pages01 - Exercises Session 1 - EmptyAgustín RosalesNo ratings yet

- Suggested Answers Assignment Notes PayableDocument4 pagesSuggested Answers Assignment Notes PayableKeikoNo ratings yet

- Framework - QB PDFDocument6 pagesFramework - QB PDFHindutav aryaNo ratings yet

- Problem Sets Finacc Chapter 9Document19 pagesProblem Sets Finacc Chapter 9Reg LagartejaNo ratings yet

- Fin Reporting and FSA-fund Flow Statment 6th Sem by VS (Vinay Shaw0 For MorningDocument12 pagesFin Reporting and FSA-fund Flow Statment 6th Sem by VS (Vinay Shaw0 For MorningSarfraz AhmedNo ratings yet

- Intermediate Accounting 2 Activity: Compound Financial InstrumentDocument2 pagesIntermediate Accounting 2 Activity: Compound Financial InstrumentMitch Tokong MinglanaNo ratings yet

- Announcement of Interim Results For The Six Months Ended 30 June 2020Document19 pagesAnnouncement of Interim Results For The Six Months Ended 30 June 2020in resNo ratings yet

- Solutions: D SC - Ordinary Share Premium Retained Earnings Treasury SharesDocument2 pagesSolutions: D SC - Ordinary Share Premium Retained Earnings Treasury SharesQueen ValleNo ratings yet

- MODULE 4 - DiscussionDocument11 pagesMODULE 4 - DiscussionYess poooNo ratings yet

- NAV-Questions-25 7 20Document43 pagesNAV-Questions-25 7 20anubhav pathakNo ratings yet

- Financial ReportDocument62 pagesFinancial ReportThành HoàngNo ratings yet

- Company Accounts, Cost and Management AccountingDocument10 pagesCompany Accounts, Cost and Management AccountingmeetwithsanjayNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- FEDAct, 2005updatedupto30 06 2020Document97 pagesFEDAct, 2005updatedupto30 06 2020ZahidNo ratings yet

- Mock Exam 2Document7 pagesMock Exam 2ZahidNo ratings yet

- Consolidation Qst.Document2 pagesConsolidation Qst.ZahidNo ratings yet

- Operating Segments PDFDocument12 pagesOperating Segments PDFZahidNo ratings yet

- Financial Accounting and Reporting-IIDocument5 pagesFinancial Accounting and Reporting-IIZahidNo ratings yet

- Caf 7 Far2 QB PDFDocument262 pagesCaf 7 Far2 QB PDFZahid100% (1)

- Caf 7 Far2 ST PDFDocument278 pagesCaf 7 Far2 ST PDFZahidNo ratings yet

- Assignment 1-IFRSDocument14 pagesAssignment 1-IFRSZahidNo ratings yet

- Financial Accounting and Reporting-IIDocument6 pagesFinancial Accounting and Reporting-IIZahidNo ratings yet

- Borang Ambulans CallDocument2 pagesBorang Ambulans Callleo89azman100% (1)

- in Strategic Management What Are The Problems With Maintaining A High Inventory As Experienced Previously With Apple?Document5 pagesin Strategic Management What Are The Problems With Maintaining A High Inventory As Experienced Previously With Apple?Priyanka MurthyNo ratings yet

- FM 2030Document18 pagesFM 2030renaissancesamNo ratings yet

- Unit 16 - Monitoring, Review and Audit by Allan WatsonDocument29 pagesUnit 16 - Monitoring, Review and Audit by Allan WatsonLuqman OsmanNo ratings yet

- AlpaGasus: How To Train LLMs With Less Data and More AccuracyDocument6 pagesAlpaGasus: How To Train LLMs With Less Data and More AccuracyMy SocialNo ratings yet

- Ob NotesDocument8 pagesOb NotesRahul RajputNo ratings yet

- Tetralogy of FallotDocument8 pagesTetralogy of FallotHillary Faye FernandezNo ratings yet

- Huawei R4815N1 DatasheetDocument2 pagesHuawei R4815N1 DatasheetBysNo ratings yet

- Career Level Diagram - V5Document1 pageCareer Level Diagram - V5Shivani RaikwarNo ratings yet

- Turning PointsDocument2 pagesTurning Pointsapi-223780825No ratings yet

- Dalasa Jibat MijenaDocument24 pagesDalasa Jibat MijenaBelex ManNo ratings yet

- PED003Document1 pagePED003ely mae dag-umanNo ratings yet

- Hdfs Default XML ParametersDocument14 pagesHdfs Default XML ParametersVinod BihalNo ratings yet

- Obesity - The Health Time Bomb: ©LTPHN 2008Document36 pagesObesity - The Health Time Bomb: ©LTPHN 2008EVA PUTRANTO100% (2)

- Lithuania DalinaDocument16 pagesLithuania DalinaStunt BackNo ratings yet

- Waterstop TechnologyDocument69 pagesWaterstop TechnologygertjaniNo ratings yet

- Test ScienceDocument2 pagesTest Sciencejam syNo ratings yet

- Chemistry: Crash Course For JEE Main 2020Document18 pagesChemistry: Crash Course For JEE Main 2020Sanjeeb KumarNo ratings yet

- KP Tevta Advertisement 16-09-2019Document4 pagesKP Tevta Advertisement 16-09-2019Ishaq AminNo ratings yet

- Project ManagementDocument11 pagesProject ManagementBonaventure NzeyimanaNo ratings yet

- SMR 13 Math 201 SyllabusDocument2 pagesSMR 13 Math 201 SyllabusFurkan ErisNo ratings yet

- WEB DESIGN WITH AUSTINE-converted-1Document9 pagesWEB DESIGN WITH AUSTINE-converted-1JayjayNo ratings yet

- Science7 - q1 - Mod3 - Distinguishing Mixtures From Substances - v5Document25 pagesScience7 - q1 - Mod3 - Distinguishing Mixtures From Substances - v5Bella BalendresNo ratings yet

- Golf Croquet Refereeing Manual - Croquet AustraliaDocument78 pagesGolf Croquet Refereeing Manual - Croquet AustraliaSenorSushi100% (1)

- DQ Vibro SifterDocument13 pagesDQ Vibro SifterDhaval Chapla67% (3)

- Partes de La Fascia Opteva Y MODULOSDocument182 pagesPartes de La Fascia Opteva Y MODULOSJuan De la RivaNo ratings yet

- WL-80 FTCDocument5 pagesWL-80 FTCMr.Thawatchai hansuwanNo ratings yet

- Opc PPT FinalDocument22 pagesOpc PPT FinalnischalaNo ratings yet

- Electro Fashion Sewable LED Kits WebDocument10 pagesElectro Fashion Sewable LED Kits WebAndrei VasileNo ratings yet

- Sindi and Wahab in 18th CenturyDocument9 pagesSindi and Wahab in 18th CenturyMujahid Asaadullah AbdullahNo ratings yet