You might also like

- Karkits Corporation Excel Copy PasteDocument2 pagesKarkits Corporation Excel Copy PasteCoke Aidenry SaludoNo ratings yet

- Trial Balance Adjustments Profit or Loss Financial PositionDocument3 pagesTrial Balance Adjustments Profit or Loss Financial PositionCoke Aidenry Saludo100% (1)

- Fundamentals of Human Behavior 1Document4 pagesFundamentals of Human Behavior 1Coke Aidenry SaludoNo ratings yet

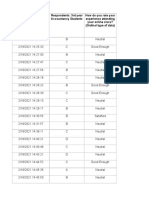

- Timestamp Respondents: 3rd Year Accountancy Students How Do You Rate Your Experience Attending Your Online Class? (Ordinal Type of Data)Document6 pagesTimestamp Respondents: 3rd Year Accountancy Students How Do You Rate Your Experience Attending Your Online Class? (Ordinal Type of Data)Coke Aidenry SaludoNo ratings yet

- Auditing Multiple Choice Questions: StudyDocument73 pagesAuditing Multiple Choice Questions: StudyCoke Aidenry SaludoNo ratings yet

- Auditing Report CASE11Document18 pagesAuditing Report CASE11Coke Aidenry Saludo0% (1)

- Good Day EveryoneDocument6 pagesGood Day EveryoneCoke Aidenry SaludoNo ratings yet

- Notes Complete On Managerial EconomicsDocument37 pagesNotes Complete On Managerial EconomicsCoke Aidenry SaludoNo ratings yet

- Quizlet Week 4 LisudDocument57 pagesQuizlet Week 4 LisudCoke Aidenry SaludoNo ratings yet

- Managerial Economics (Ec 403) Managerial EconomicsDocument6 pagesManagerial Economics (Ec 403) Managerial EconomicsCoke Aidenry SaludoNo ratings yet

- Capital Budgeting HandoutsDocument13 pagesCapital Budgeting HandoutsCoke Aidenry SaludoNo ratings yet

- Saludo, Coke Aidenry E. THEO 3b-B The Bible (Movie Reflection)Document1 pageSaludo, Coke Aidenry E. THEO 3b-B The Bible (Movie Reflection)Coke Aidenry SaludoNo ratings yet

- The Nature of Managerial Economics Economics EssayDocument86 pagesThe Nature of Managerial Economics Economics EssayCoke Aidenry SaludoNo ratings yet

- B. Pricing StrategyDocument4 pagesB. Pricing StrategyCoke Aidenry SaludoNo ratings yet

- Chapter 4: The Fundamental Principles of Ethics: Reporter 1: Obinguar, Ma. Angelica UDocument5 pagesChapter 4: The Fundamental Principles of Ethics: Reporter 1: Obinguar, Ma. Angelica UCoke Aidenry SaludoNo ratings yet

- Final Exams Agency and Credit TransactionsDocument3 pagesFinal Exams Agency and Credit TransactionsCoke Aidenry SaludoNo ratings yet

- Math 10: 1 Quarter Weekly ModuleDocument17 pagesMath 10: 1 Quarter Weekly ModuleCoke Aidenry SaludoNo ratings yet

- MS ACCESS TutorialDocument94 pagesMS ACCESS TutorialCoke Aidenry SaludoNo ratings yet

- TLE 10 Week 2Document18 pagesTLE 10 Week 2Coke Aidenry SaludoNo ratings yet

- Saludo, Coke Aidenry E. Bsa 3-A Theo 3-ADocument6 pagesSaludo, Coke Aidenry E. Bsa 3-A Theo 3-ACoke Aidenry SaludoNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Customer Segmentation MatrixDocument4 pagesCustomer Segmentation MatrixRA ArafatNo ratings yet

- Order Appealed Against 2Document27 pagesOrder Appealed Against 2Jyoti MeenaNo ratings yet

- Task 1 - ModelAnswerDocument2 pagesTask 1 - ModelAnswerAryanNo ratings yet

- Korn Ferry Core Job Model 2019 - Job Profiles - Ref LevelsDocument525 pagesKorn Ferry Core Job Model 2019 - Job Profiles - Ref LevelsAbdulaziz AlzahraniNo ratings yet

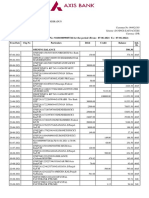

- Statement of Axis Account No:921010009005726 For The Period (From: 07-06-2021 To: 07-06-2022)Document22 pagesStatement of Axis Account No:921010009005726 For The Period (From: 07-06-2021 To: 07-06-2022)TusharNo ratings yet

- Conept of RetailingDocument13 pagesConept of RetailingAniSh ThapaNo ratings yet

- Build BacklinksDocument17 pagesBuild BacklinksKashif NaeemNo ratings yet

- Exide Life Insurance - PO 1200011572Document16 pagesExide Life Insurance - PO 1200011572Joan AliNo ratings yet

- The Political Economy of Growth in Vietnam BetweenDocument29 pagesThe Political Economy of Growth in Vietnam BetweenrexNo ratings yet

- Bs-Delhi 25-9-2020Document15 pagesBs-Delhi 25-9-2020mutaia pandianNo ratings yet

- Chap 005Document153 pagesChap 005Kim NgânNo ratings yet

- (5032) - OFFICIALLY Assignment 1Document19 pages(5032) - OFFICIALLY Assignment 1Nguyen Khanh Ly (FGW HN)No ratings yet

- Cfi 5102 Final 2016Document5 pagesCfi 5102 Final 2016MukandionaNo ratings yet

- Gem Terms & ConditionsDocument2 pagesGem Terms & ConditionsJaydeepNo ratings yet

- Final Atendee List - MuskaanDocument5 pagesFinal Atendee List - MuskaanKunwar SaigalNo ratings yet

- Online Shopping (Complete File)Document2 pagesOnline Shopping (Complete File)Muhammad UsmanNo ratings yet

- Entrepreneurship Module 8 10 OrinayDocument16 pagesEntrepreneurship Module 8 10 OrinayIra Jane CaballeroNo ratings yet

- Mouse PadDocument2 pagesMouse Pad20MA32 - PRABAVATHI TNo ratings yet

- Basic of Sap MMDocument12 pagesBasic of Sap MMRooplata NayakNo ratings yet

- GROUP 4 - HPG Financial Statement - 21.09Document27 pagesGROUP 4 - HPG Financial Statement - 21.09Hoàng ThànhNo ratings yet

- PPIC-6-REVIEW-Order Quantity Example 18 Maret 2020 PDFDocument80 pagesPPIC-6-REVIEW-Order Quantity Example 18 Maret 2020 PDFDaffa JNo ratings yet

- 3113 4 Zero Rated TransactionsDocument5 pages3113 4 Zero Rated TransactionsConic DurangparangNo ratings yet

- This Study Resource Was: Chapter 8-Profitability QuizDocument5 pagesThis Study Resource Was: Chapter 8-Profitability Quizfatima mohamedNo ratings yet

- Chapter Six Ba 315-Lpc Umsl: (Contribution Margin)Document53 pagesChapter Six Ba 315-Lpc Umsl: (Contribution Margin)NAZHIM KERENNo ratings yet

- Finding The Right International MixDocument3 pagesFinding The Right International MixКсения БорисоваNo ratings yet

- Capitalmind Financial Shenanigans Part 1Document17 pagesCapitalmind Financial Shenanigans Part 1abhinavnarayanNo ratings yet

- DocxDocument6 pagesDocxLeo Sandy Ambe CuisNo ratings yet

- Consort Utilizing Consolidation To Lower Transport CostsDocument12 pagesConsort Utilizing Consolidation To Lower Transport CostsDenis Mendoza QuispeNo ratings yet

- MA Handbook Brazil 2023Document189 pagesMA Handbook Brazil 2023João Vitor MoralesNo ratings yet

- Instagram and Facebook MarketingDocument6 pagesInstagram and Facebook Marketingaadarsh mahajanNo ratings yet