You might also like

- Designing An AirshipDocument100 pagesDesigning An AirshipFrik van der Merwe100% (2)

- Questioning ToolDocument6 pagesQuestioning ToolvbrajuNo ratings yet

- Moisture Control Guidance For Building Design, Construction and Maintenance (2013)Document144 pagesMoisture Control Guidance For Building Design, Construction and Maintenance (2013)Schreiber_Dieses100% (1)

- 1174 Franchise AgreementDocument32 pages1174 Franchise AgreementvbrajuNo ratings yet

- Moral Leadership 2019Document23 pagesMoral Leadership 2019vbrajuNo ratings yet

- 2020 Novartis Vas Narasimhan Jpmorgan PresentationDocument38 pages2020 Novartis Vas Narasimhan Jpmorgan Presentationy_esmatNo ratings yet

- Challenging Cognitive Distortions HealthyPsych - ComDocument1 pageChallenging Cognitive Distortions HealthyPsych - ComLeila MargaridaNo ratings yet

- Global Service Learning: M325D MH / M325D L MH Material HandlersDocument52 pagesGlobal Service Learning: M325D MH / M325D L MH Material Handlersanon_828943220100% (2)

- Amgen 2019 JP Morgan PresentationDocument32 pagesAmgen 2019 JP Morgan PresentationmedtechyNo ratings yet

- SDC RFP 2017 18 11jan2018Document472 pagesSDC RFP 2017 18 11jan2018vbraju100% (1)

- GPC Investor Prestentation August-2022Document31 pagesGPC Investor Prestentation August-2022ЛяховецДмитрийNo ratings yet

- SolidWorks Motion Tutorial 2010Document31 pagesSolidWorks Motion Tutorial 2010Hector Adan Lopez GarciaNo ratings yet

- Service Driven Logistics System - Basic Service CapabilityDocument12 pagesService Driven Logistics System - Basic Service CapabilityAnusha Sunkara80% (5)

- List of IncubatorsDocument44 pagesList of Incubatorsvbraju100% (1)

- Sri Veerabrahmendra The Precursor of KalkiDocument359 pagesSri Veerabrahmendra The Precursor of KalkiSantosh Kumar Ayalasomayajula77% (30)

- 2019 North America Investor Tour PresentationsDocument84 pages2019 North America Investor Tour PresentationsNoshan OneitoNo ratings yet

- Sealed Air Diversey Merger Acquisition Presentation Slides Deck PPT June 2011Document40 pagesSealed Air Diversey Merger Acquisition Presentation Slides Deck PPT June 2011Ala BasterNo ratings yet

- 2019 Annual ReportDocument104 pages2019 Annual ReportDasari PrabodhNo ratings yet

- InfosysDocument28 pagesInfosysAditya SoniNo ratings yet

- Iron Mountain: We Protect What You Value Most: Investor PresentationDocument33 pagesIron Mountain: We Protect What You Value Most: Investor PresentationrustedchainsawNo ratings yet

- RMK Aramark March 2006 PresentationDocument30 pagesRMK Aramark March 2006 PresentationAla BasterNo ratings yet

- DD Marketing Deck FEB 2023Document49 pagesDD Marketing Deck FEB 2023Yu-Chih LinNo ratings yet

- Albermarle November 2022 Investor Presentation v04Document39 pagesAlbermarle November 2022 Investor Presentation v04Guillaume De SouzaNo ratings yet

- MultiplesDocument49 pagesMultiplesDekov72No ratings yet

- Purolite Investor PresentationDocument17 pagesPurolite Investor PresentationQuốc Anh KhổngNo ratings yet

- Domtar Quarterly ReportDocument15 pagesDomtar Quarterly ReportWJHL News Channel ElevenNo ratings yet

- 2019 Summary Annual Report - UnlockedDocument58 pages2019 Summary Annual Report - UnlockedEmiliano ErrasquinNo ratings yet

- AB InBev 4Q20 Results PresentationDocument34 pagesAB InBev 4Q20 Results PresentationJesus MendozaNo ratings yet

- Credicorp Pronostica "Caída Significativa" en Precio de La Acción de Nutresa Después de La OPADocument10 pagesCredicorp Pronostica "Caída Significativa" en Precio de La Acción de Nutresa Después de La OPASemanaNo ratings yet

- Flex Packaging Film - 2 Pager Teaser (Wout Watermark)Document3 pagesFlex Packaging Film - 2 Pager Teaser (Wout Watermark)izzatesaNo ratings yet

- CM20220429 5abae 1adc1Document116 pagesCM20220429 5abae 1adc1Liora Vanessa DopacioNo ratings yet

- Ford Report on Climate Change Impact on BusinessDocument23 pagesFord Report on Climate Change Impact on BusinessRajeev GopinathNo ratings yet

- Dl Presentation Deutsche TelekomDocument69 pagesDl Presentation Deutsche TelekomOmar BenaichaNo ratings yet

- Ops 2 - COS Dynamics - HandoutDocument20 pagesOps 2 - COS Dynamics - HandoutAjayi Adebayo Ebenezer-SuccessNo ratings yet

- CHP 3Q20 Presentation (FINAL) 10.29.2020Document24 pagesCHP 3Q20 Presentation (FINAL) 10.29.2020Jep TangNo ratings yet

- Clothing Retailing - UK - 2022 - BrochureDocument4 pagesClothing Retailing - UK - 2022 - BrochureMainak PaulNo ratings yet

- Driving The Global Cannabis Industry: February 2019Document22 pagesDriving The Global Cannabis Industry: February 2019Sameer MahomedNo ratings yet

- FISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020Document25 pagesFISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020sl7789No ratings yet

- Which Resulted in The First Integrated Gas and Electricity Company in Spain 17,229 People, Over 50% of Whom Work Outside of SpainDocument3 pagesWhich Resulted in The First Integrated Gas and Electricity Company in Spain 17,229 People, Over 50% of Whom Work Outside of SpainAmos YuanNo ratings yet

- Changing World: Sustained Values: Our Sustainability ReviewDocument20 pagesChanging World: Sustained Values: Our Sustainability ReviewcattleyajenNo ratings yet

- ITC Limited: Ratings Reaffirmed: Summary of Rating ActionDocument6 pagesITC Limited: Ratings Reaffirmed: Summary of Rating ActionSatish RajNo ratings yet

- Fruit - US - 2021 - BrochureDocument7 pagesFruit - US - 2021 - BrochureTiên Nguyễn ThủyNo ratings yet

- GPC Investor Presentation November 2022Document31 pagesGPC Investor Presentation November 2022lucio ReisNo ratings yet

- Investment Banking - Securities Dealing in The US Industry ReportDocument42 pagesInvestment Banking - Securities Dealing in The US Industry ReportEldar Sedaghatparast SalehNo ratings yet

- 2023_01_YPF Investor Presentation Q1 2023Document22 pages2023_01_YPF Investor Presentation Q1 2023dsv.newNo ratings yet

- 05 Performance ChemicalsDocument10 pages05 Performance ChemicalsMarcos De Castro OsórioNo ratings yet

- Global Overview of The Forestry Wood and Paper IndustryDocument51 pagesGlobal Overview of The Forestry Wood and Paper IndustryMẫn NgôNo ratings yet

- CEO Dirk Van De Put Strategy ExecutionDocument57 pagesCEO Dirk Van De Put Strategy ExecutionMy Ha KieuNo ratings yet

- Nov 2019 PresentationDocument39 pagesNov 2019 PresentationCatarinaNhuNo ratings yet

- Berry Plastics Group Investor Presentation August 2019 - FINALDocument42 pagesBerry Plastics Group Investor Presentation August 2019 - FINALAndyNo ratings yet

- HMSP - Public Expose - 3Q2020Document19 pagesHMSP - Public Expose - 3Q2020Ershad SNo ratings yet

- IRBT Investor Presentation Baird111120Document31 pagesIRBT Investor Presentation Baird111120ABermNo ratings yet

- Direksi PT Bursa Efek IndonesiaDocument20 pagesDireksi PT Bursa Efek IndonesiakaremiaNo ratings yet

- CRTO 101 - Mar 2021Document122 pagesCRTO 101 - Mar 2021bruno.augustoNo ratings yet

- Strategy Update: Reimagining MedicineDocument23 pagesStrategy Update: Reimagining MedicineramezNo ratings yet

- Stern Stewart (01) Research (En 69) Global Packaging InsightsDocument22 pagesStern Stewart (01) Research (En 69) Global Packaging InsightsPaulo Nicoletti de FragaNo ratings yet

- DL Presentation Deutsche TelekomDocument49 pagesDL Presentation Deutsche Telekomimam arifuddinNo ratings yet

- Global Legal Advisory Mergers & Acquisitions Rankings 2010Document48 pagesGlobal Legal Advisory Mergers & Acquisitions Rankings 2010pal2789No ratings yet

- 6 - NEW - ALB 2022 May Investor Presentation VFDocument47 pages6 - NEW - ALB 2022 May Investor Presentation VFkhairul ihsanNo ratings yet

- P&G's Risks in International Business in ChinaDocument30 pagesP&G's Risks in International Business in Chinamohamed mostafaNo ratings yet

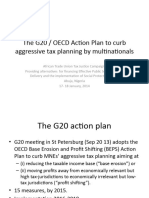

- Tax Planning by MultinationalsDocument18 pagesTax Planning by Multinationalsgunjan2791993No ratings yet

- Q1 FY20 Press Presentation Highlights Revenue GrowthDocument11 pagesQ1 FY20 Press Presentation Highlights Revenue GrowthParvathi M LNo ratings yet

- SAP - EN-Corporate Presentation - August 3Document57 pagesSAP - EN-Corporate Presentation - August 3kishoreNo ratings yet

- FY21 Q2 Financial Results: Rs 4,897 Cr Revenue, Rs 762 Cr PATDocument13 pagesFY21 Q2 Financial Results: Rs 4,897 Cr Revenue, Rs 762 Cr PATPharma researchNo ratings yet

- Teva Q1-2023 Earnings-Presentation FinalDocument42 pagesTeva Q1-2023 Earnings-Presentation FinalRutvik ShahNo ratings yet

- Tata Consumer Products' Genesis and Journey So FarDocument39 pagesTata Consumer Products' Genesis and Journey So FarKartik SharmaNo ratings yet

- Strategic Management - Grant - Chapter 2Document18 pagesStrategic Management - Grant - Chapter 2Jake20No ratings yet

- TOST Investor Presentation Q3FY23Document28 pagesTOST Investor Presentation Q3FY23carlosNo ratings yet

- W To Agreement On Agriculture and Its Impact OnDocument38 pagesW To Agreement On Agriculture and Its Impact Onvishal vlogsNo ratings yet

- SIBUR - 1H 2020 - Results - PresentationDocument22 pagesSIBUR - 1H 2020 - Results - Presentation757rustamNo ratings yet

- KPMG Newsletter (Issue 1) - Economic Impact and Pandemic Planning PDFDocument4 pagesKPMG Newsletter (Issue 1) - Economic Impact and Pandemic Planning PDFSNo ratings yet

- Connectors & Interconnections World Summary: Market Values & Financials by CountryFrom EverandConnectors & Interconnections World Summary: Market Values & Financials by CountryNo ratings yet

- Wp1605 What Iot Brings To BankingDocument15 pagesWp1605 What Iot Brings To Bankingvbraju100% (1)

- 288 40521 Tender DocumentsDocument203 pages288 40521 Tender Documentsvbraju100% (1)

- Legal Issues Franchising IndiaDocument25 pagesLegal Issues Franchising IndiaTonmoy BorahNo ratings yet

- Startups IPRFacilitation 22april2016Document20 pagesStartups IPRFacilitation 22april2016vbrajuNo ratings yet

- Indian Fertilizer SCENARIO-2014Document246 pagesIndian Fertilizer SCENARIO-2014singhsachinkumarNo ratings yet

- Overlay ARDocument14 pagesOverlay ARvbrajuNo ratings yet

- ArthakrantiDocument73 pagesArthakrantimastpawanNo ratings yet

- 2014 15 District Sheet CalendarDocument1 page2014 15 District Sheet CalendarvbrajuNo ratings yet

- Agitation After TBIDocument120 pagesAgitation After TBIvbrajuNo ratings yet

- Brain Injury Stages RecoveryDocument7 pagesBrain Injury Stages RecoveryvbrajuNo ratings yet

- Regulatory ReformDocument5 pagesRegulatory ReformvbrajuNo ratings yet

- IsotopesDocument35 pagesIsotopesAddisu Amare Zena 18BML0104No ratings yet

- Reviewer in EntrepreneurshipDocument3 pagesReviewer in EntrepreneurshipJazz Add100% (1)

- Adb Doc Easa Reliance 8 Centerline Stopbar Declaracao de Conformidade EasaDocument2 pagesAdb Doc Easa Reliance 8 Centerline Stopbar Declaracao de Conformidade Easagiant360No ratings yet

- Bayes Slides1Document146 pagesBayes Slides1Panagiotis KarathymiosNo ratings yet

- Industry Standard: What Are The Benefits For You?Document4 pagesIndustry Standard: What Are The Benefits For You?Zarnimyomyint MyintNo ratings yet

- Affidavit Defends Wife's InnocenceDocument6 pagesAffidavit Defends Wife's InnocenceGreggy LawNo ratings yet

- A Study On Consumer Changing Buying Behaviour From Gold Jewellery To Diamond JewelleryDocument9 pagesA Study On Consumer Changing Buying Behaviour From Gold Jewellery To Diamond JewellerynehaNo ratings yet

- OPTION STRATEGIES PAYOFF CALCULATOR v2Document9 pagesOPTION STRATEGIES PAYOFF CALCULATOR v2Jay KewatNo ratings yet

- Iwan Lab Guide v1.1 FinalDocument63 pagesIwan Lab Guide v1.1 FinalRicardo SicheranNo ratings yet

- Republic of The Philippines, Petitioner, vs. Sandiganbayan, Major General Josephus Q. Ramas and Elizabeth Dimaano, RespondentsDocument23 pagesRepublic of The Philippines, Petitioner, vs. Sandiganbayan, Major General Josephus Q. Ramas and Elizabeth Dimaano, RespondentsKenzo RodisNo ratings yet

- AfghanistanLML OnlinDocument117 pagesAfghanistanLML Onlinعارف حسینNo ratings yet

- No or Islamic Bank OurStory EnglishDocument45 pagesNo or Islamic Bank OurStory EnglishTalib ZaidiNo ratings yet

- ACL Reconstruction BookDocument18 pagesACL Reconstruction BookSergejs JaunzemsNo ratings yet

- PACiS GTW EN O C80Document170 pagesPACiS GTW EN O C80paradiseparasNo ratings yet

- More User Manuals OnDocument78 pagesMore User Manuals OnNicolae HincuNo ratings yet

- Storytelling Tips from Salesforce CEO Marc BenioffDocument2 pagesStorytelling Tips from Salesforce CEO Marc BenioffvsrajkumarNo ratings yet

- mPassBook 161022 150423 2918Document4 pagesmPassBook 161022 150423 2918Ashish kumarNo ratings yet

- 20-Sdms-02 (Overhead Line Accessories) Rev01Document15 pages20-Sdms-02 (Overhead Line Accessories) Rev01Haytham BafoNo ratings yet

- Ari Globe Valve SupraDocument26 pagesAri Globe Valve SupraAi-samaNo ratings yet

- Analyzing Air Asia in Business Competition Era: AirasiaDocument14 pagesAnalyzing Air Asia in Business Competition Era: Airasiashwaytank10No ratings yet

- EIE Resume FormatDocument1 pageEIE Resume FormatRakesh MandalNo ratings yet

- Module 3 - Design RulesDocument19 pagesModule 3 - Design RulesSamNo ratings yet

- Bangladesh Premier League 2024 Schedule, Live Scores and ResultsDocument5 pagesBangladesh Premier League 2024 Schedule, Live Scores and Resultsmoslahuddin2022No ratings yet

- CIMA Introduction To NLPDocument4 pagesCIMA Introduction To NLPsambrefoNo ratings yet