You might also like

- Real Property Donation Documentary RequirementsDocument1 pageReal Property Donation Documentary RequirementsbiklatNo ratings yet

- Re - Estate Settlement ProceduresDocument7 pagesRe - Estate Settlement ProceduresRonadale Zapata-AcostaNo ratings yet

- Tax Free Exchange Process FlowDocument6 pagesTax Free Exchange Process FlowRoselle Asis- NapolesNo ratings yet

- Sec Registration RequirementsDocument25 pagesSec Registration Requirementsmay .No ratings yet

- Documentary Requirements: Estate TaxDocument19 pagesDocumentary Requirements: Estate TaxAubrey CaballeroNo ratings yet

- Sec RegDocument19 pagesSec RegseandagsNo ratings yet

- Sec Registration RequirementsDocument16 pagesSec Registration RequirementsBona Carmela BienNo ratings yet

- Requirement SEC RegistrationDocument14 pagesRequirement SEC RegistrationbrownboomerangNo ratings yet

- Estate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andDocument4 pagesEstate Tax Is A Tax On The Right of The Deceased Person To Transmit His/her Estate To His/her Lawful Heirs andRey PerosaNo ratings yet

- Estate TaxDocument4 pagesEstate TaxWuwu WuswewuNo ratings yet

- Estate Tax: BIR Form 1801Document13 pagesEstate Tax: BIR Form 1801Renalyn GardeNo ratings yet

- Bureau of Internal Revenue (Bir) Capital Gains Tax (BIR Form 1706) and Documentary Stamp Tax (2000-OT)Document3 pagesBureau of Internal Revenue (Bir) Capital Gains Tax (BIR Form 1706) and Documentary Stamp Tax (2000-OT)sheshe gamiaoNo ratings yet

- Estate Tax Filing RequirementsDocument9 pagesEstate Tax Filing Requirementsntcr11No ratings yet

- Capital Gains TaxDocument5 pagesCapital Gains TaxJAYAR MENDZNo ratings yet

- Estate Tax Return: MandatoryDocument1 pageEstate Tax Return: MandatoryYna Yna100% (1)

- TRANSFER OF LAND TITLEDocument8 pagesTRANSFER OF LAND TITLEAnonymous uMI5BmNo ratings yet

- Steps in Transferring TitleDocument4 pagesSteps in Transferring TitleMJ PerryNo ratings yet

- Documentary Requirements of Registration 2012 PDFDocument20 pagesDocumentary Requirements of Registration 2012 PDFRj RamosNo ratings yet

- SEC registration requirementsDocument44 pagesSEC registration requirementsChristian Lemuel Tangunan TanNo ratings yet

- BIR CGT RequirementsDocument3 pagesBIR CGT RequirementsGerald MesinaNo ratings yet

- Capital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsDocument6 pagesCapital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsCyrill L. MarkNo ratings yet

- Capital Gains Tax GuideDocument15 pagesCapital Gains Tax GuideWilma P.No ratings yet

- Transferring Land Title StepsDocument4 pagesTransferring Land Title Stepsabogado101No ratings yet

- Things To Consider Before Buying LandDocument4 pagesThings To Consider Before Buying LandGelo ArevaloNo ratings yet

- Additional Requirements Based On Kind of Payment For SubscriptionDocument4 pagesAdditional Requirements Based On Kind of Payment For SubscriptionJhoey Castillo BuenoNo ratings yet

- BIR Form 1800 RequirementsDocument1 pageBIR Form 1800 RequirementsjenNo ratings yet

- Annex B4Document1 pageAnnex B4Idan AguirreNo ratings yet

- S40 Checklist Annex BDocument2 pagesS40 Checklist Annex BTootsieNo ratings yet

- Required Document ChecklistDocument3 pagesRequired Document ChecklistFrederick Xavier LimNo ratings yet

- LRA FAQ How To RegisterDocument4 pagesLRA FAQ How To RegistergayleopsimaNo ratings yet

- FAQs LRA Land Registration Authority Frequently Asked QuestionsDocument3 pagesFAQs LRA Land Registration Authority Frequently Asked QuestionsPrateik RyukiNo ratings yet

- Sec RequirementsDocument5 pagesSec RequirementsJM Manicap-OtomanNo ratings yet

- Capital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsDocument11 pagesCapital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsGrace G. ServanoNo ratings yet

- Capital Gains Tax CTT ReviewDocument7 pagesCapital Gains Tax CTT ReviewRommel RoyceNo ratings yet

- SEC Amendment - Increase in Authorized CapitalDocument4 pagesSEC Amendment - Increase in Authorized CapitalGerryNo ratings yet

- Step by Step - Transfer of TitleDocument4 pagesStep by Step - Transfer of TitleRommyr P. Caballero100% (2)

- Tax Rates Description Tax Form Documentary Requirements Procedures Deadlines Related Revenue Issuances Codal Reference Frequently Asked QuestionsDocument10 pagesTax Rates Description Tax Form Documentary Requirements Procedures Deadlines Related Revenue Issuances Codal Reference Frequently Asked Questionsshawn7800No ratings yet

- Registration of Partnerships and CorporationsDocument6 pagesRegistration of Partnerships and CorporationsPaolo LimNo ratings yet

- Titling 1. File and Secure The Documentary Requirements at The Bureau of Internal Revenue Regional District Office (BIR RDDocument3 pagesTitling 1. File and Secure The Documentary Requirements at The Bureau of Internal Revenue Regional District Office (BIR RDara abuNo ratings yet

- Guideline in The Transfer of Titles of Real PropertyDocument4 pagesGuideline in The Transfer of Titles of Real PropertyLeolaida AragonNo ratings yet

- Extrajudicial Settlement of Estate - SAKLAWDocument7 pagesExtrajudicial Settlement of Estate - SAKLAWRC Farms TalakagNo ratings yet

- Extrajudicial Settlement of Estate - SAKLAWDocument7 pagesExtrajudicial Settlement of Estate - SAKLAWRC Farms TalakagNo ratings yet

- A. Steps in Casual Sale of Real Estate: Fees To Be IncurredDocument9 pagesA. Steps in Casual Sale of Real Estate: Fees To Be IncurredMinmin WaganNo ratings yet

- Tax Free Exchanges - Corp-TaxDocument7 pagesTax Free Exchanges - Corp-TaxutaknghenyoNo ratings yet

- BIR Form 1707Document3 pagesBIR Form 1707catherine joy sangilNo ratings yet

- Basic Requirements For Registering Properties in The PhilippinesDocument2 pagesBasic Requirements For Registering Properties in The Philippinescrixzam100% (1)

- Estate TaxDocument2 pagesEstate TaxNaomi CartagenaNo ratings yet

- Checklist of Documentary Requirements - Issuance by BIR of CARDocument1 pageChecklist of Documentary Requirements - Issuance by BIR of CARLRMNo ratings yet

- Administrative TitlingDocument12 pagesAdministrative TitlingDebra BraciaNo ratings yet

- Estate Tax Requirements and RatesDocument4 pagesEstate Tax Requirements and RatesRichel888No ratings yet

- Rmo 32-01Document5 pagesRmo 32-01matinikkiNo ratings yet

- SEC REGISTRATION GUIDEDocument67 pagesSEC REGISTRATION GUIDERheneir MoraNo ratings yet

- Requirements Involving Land TransactionsDocument3 pagesRequirements Involving Land TransactionsRAPHY T ALANNo ratings yet

- FAQs - Land Registration AuthorityDocument4 pagesFAQs - Land Registration Authorityarkina_sunshineNo ratings yet

- Requirements and Procedures in Paying Capital Gain TaxDocument2 pagesRequirements and Procedures in Paying Capital Gain TaxDrizza FerrerNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- The Book of the Morris Minor and the Morris Eight - A Complete Guide for Owners and Prospective Purchasers of All Morris Minors and Morris EightsFrom EverandThe Book of the Morris Minor and the Morris Eight - A Complete Guide for Owners and Prospective Purchasers of All Morris Minors and Morris EightsNo ratings yet

- General Instructions for the Guidance of Post Office Inspectors in the Dominion of CanadaFrom EverandGeneral Instructions for the Guidance of Post Office Inspectors in the Dominion of CanadaNo ratings yet

- Property & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsFrom EverandProperty & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsNo ratings yet

- RememberDocument2 pagesRememberCyrill L. MarkNo ratings yet

- Philippine Nursing Laws GuideDocument2 pagesPhilippine Nursing Laws GuideCyrill L. MarkNo ratings yet

- Notice of DeathDocument1 pageNotice of DeathCyrill L. MarkNo ratings yet

- Basics in Starting Up A CorporationDocument4 pagesBasics in Starting Up A CorporationCyrill L. MarkNo ratings yet

- Certification of ErasureDocument1 pageCertification of ErasureCyrill L. MarkNo ratings yet

- DEED OF SALE Motor VehicleDocument2 pagesDEED OF SALE Motor VehicleCyrill L. MarkNo ratings yet

- Petition For Cancellation of EntryDocument1 pagePetition For Cancellation of EntryCyrill L. MarkNo ratings yet

- Petitioners: Appeals Most Respectfully StatesDocument3 pagesPetitioners: Appeals Most Respectfully StatesCyrill L. MarkNo ratings yet

- Capital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsDocument6 pagesCapital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsCyrill L. MarkNo ratings yet

- Affidavit of ConsentDocument3 pagesAffidavit of ConsentCyrill L. MarkNo ratings yet

- Affidavit of Loss - MagdadaroDocument2 pagesAffidavit of Loss - MagdadaroLyanneNo ratings yet

- Promissory Note for P17,000 Loan Due DateDocument1 pagePromissory Note for P17,000 Loan Due DateCyrill L. MarkNo ratings yet

- CERTIFICATION of ERASUREDocument1 pageCERTIFICATION of ERASURECyrill L. MarkNo ratings yet

- Affidavit of EXTRAJUDICIAL SETTLEMENT OF ESTATEDocument3 pagesAffidavit of EXTRAJUDICIAL SETTLEMENT OF ESTATECyrill L. MarkNo ratings yet

- Laws Affecting Nursing PracticeDocument3 pagesLaws Affecting Nursing PracticeCyrill L. MarkNo ratings yet

- The Philippine NUrsing Act of 2002 Aka R.A. 9173Document7 pagesThe Philippine NUrsing Act of 2002 Aka R.A. 9173Rho Vince Caño MalagueñoNo ratings yet

- Negligence and MalpracticeDocument6 pagesNegligence and MalpracticeCyrill L. MarkNo ratings yet

- Annex A.2 - Full ApplicationDocument25 pagesAnnex A.2 - Full ApplicationBalša CvetkovićNo ratings yet

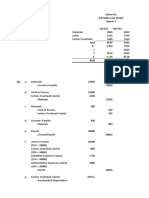

- Juarez Inc Job Order Cost Sheets (1) March 1 Job 621 Job 622Document3 pagesJuarez Inc Job Order Cost Sheets (1) March 1 Job 621 Job 622ramaNo ratings yet

- Auditing Revenue Cycle HandoutDocument8 pagesAuditing Revenue Cycle HandoutwinidsolmanNo ratings yet

- Concurrent Audit ProcessDocument7 pagesConcurrent Audit Processsukumar basuNo ratings yet

- 360 Supreme Court Reports Annotated: ING Bank N.V. vs. Commissioner of Internal RevenueDocument44 pages360 Supreme Court Reports Annotated: ING Bank N.V. vs. Commissioner of Internal RevenueFrancis ManuelNo ratings yet

- Peoples Insurance PLC Integrated Report 12768b PDFDocument308 pagesPeoples Insurance PLC Integrated Report 12768b PDFjayuse ofwadoNo ratings yet

- Christy Company Operates in The EntertainmentDocument6 pagesChristy Company Operates in The EntertainmentDoreenNo ratings yet

- On Tax AuditDocument148 pagesOn Tax AuditAnmol KumarNo ratings yet

- Independent Audit Report (Aud 339)Document7 pagesIndependent Audit Report (Aud 339)ain madihahNo ratings yet

- Himachal Pradesh PWD Job ProfilesDocument32 pagesHimachal Pradesh PWD Job ProfilesJitender KumarNo ratings yet

- IATF 16949 Update: Transition to New StandardDocument3 pagesIATF 16949 Update: Transition to New StandardVaspeoNo ratings yet

- At.01 Fundamentals of Assurance and Non Assurance EngagementsDocument3 pagesAt.01 Fundamentals of Assurance and Non Assurance EngagementsAngelica Sanchez de VeraNo ratings yet

- Corporate Governance Success Stories MENA PDFDocument64 pagesCorporate Governance Success Stories MENA PDFVarsha BhootraNo ratings yet

- Prasarana Group KPIs 2011 (Print)Document15 pagesPrasarana Group KPIs 2011 (Print)anon_216090584No ratings yet

- AMLCFT Prakas EnglishDocument24 pagesAMLCFT Prakas EnglishThol LynaNo ratings yet

- Finance (Allowances) Department: G.O.No. 106, DATED 28 Apr Il, 201 4Document2 pagesFinance (Allowances) Department: G.O.No. 106, DATED 28 Apr Il, 201 4Papu KuttyNo ratings yet

- 2021 San Miguel Corporation Parent Audited Financial Statement (04.25.2022)Document109 pages2021 San Miguel Corporation Parent Audited Financial Statement (04.25.2022)Gemmalyn BautistaNo ratings yet

- Annual dividend and AGM noticeDocument100 pagesAnnual dividend and AGM noticeZIA UL REHMANNo ratings yet

- MBI7211 - Sserumaga James and Hamdi Omar OsmanDocument4 pagesMBI7211 - Sserumaga James and Hamdi Omar Osmanjonas sserumagaNo ratings yet

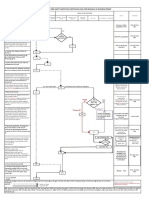

- BFP Flowchart For Fire Safety Inspection Certificate Fsic For New Business PermitDocument1 pageBFP Flowchart For Fire Safety Inspection Certificate Fsic For New Business PermitRomel RagasaNo ratings yet

- Audit II CH 4 Nov 2020Document10 pagesAudit II CH 4 Nov 2020padmNo ratings yet

- Internal Audit Standard - Yellow Book Vs Red Book FINALDocument69 pagesInternal Audit Standard - Yellow Book Vs Red Book FINALoneday_onmay7541100% (2)

- How To Create A WorksheetDocument3 pagesHow To Create A WorksheetMary100% (2)

- AUD 2 Audit of Cash and Cash EquivalentDocument14 pagesAUD 2 Audit of Cash and Cash EquivalentJayron NonguiNo ratings yet

- Corio Annual Report 2013 Highlights Strategy and Performance ChangesDocument134 pagesCorio Annual Report 2013 Highlights Strategy and Performance ChangesJasper Laarmans Teixeira de MattosNo ratings yet

- Integrated Model For Entrepreneurship Development in PakistanDocument23 pagesIntegrated Model For Entrepreneurship Development in PakistanMuhammad Shahzad KhanNo ratings yet

- 122208Document17 pages122208lieselenaNo ratings yet

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument8 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelAlaska DavisNo ratings yet

- Cost Accounting: Introduction and Key ConceptsDocument60 pagesCost Accounting: Introduction and Key ConceptspujaskawaleNo ratings yet

- ASEAN Guidelines On Public ProcurementDocument50 pagesASEAN Guidelines On Public ProcurementKhem LactuanNo ratings yet