You might also like

- DeepWeb LinkDocument16 pagesDeepWeb LinkLucas Javier75% (4)

- Labrel CasesDocument151 pagesLabrel CasesAmethyst Vivo TanioNo ratings yet

- The Offical DVSA Guide to Driving Goods Vehicles: DVSA Safe Driving for Life SeriesFrom EverandThe Offical DVSA Guide to Driving Goods Vehicles: DVSA Safe Driving for Life SeriesRating: 5 out of 5 stars5/5 (1)

- Office of The Punong BarangayDocument2 pagesOffice of The Punong BarangayIrismae Sobrevega100% (2)

- Canada Economy Case StudyDocument16 pagesCanada Economy Case StudyThe Myth TeacherNo ratings yet

- Tarif Tax TreatyDocument2 pagesTarif Tax TreatyJokoWidodo0% (1)

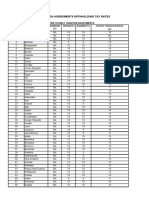

- Summary of WHT Rates Under Oman Tax Treaties in Force PDFDocument2 pagesSummary of WHT Rates Under Oman Tax Treaties in Force PDFMoneycomeNo ratings yet

- Indonesian Tax Treaties Quick Reference Guide - RevisedDocument7 pagesIndonesian Tax Treaties Quick Reference Guide - RevisedWahyuni LestariNo ratings yet

- Ringkasan Tarif P3B: Tax Learning: Tax Resume Ringkasan Tax TreatyDocument2 pagesRingkasan Tarif P3B: Tax Learning: Tax Resume Ringkasan Tax TreatyAchmad MudaniNo ratings yet

- IRCC M PRadmiss 0002 EDocument56 pagesIRCC M PRadmiss 0002 EArtur NaNo ratings yet

- Tarif Pasal 26Document2 pagesTarif Pasal 26lelaleria11No ratings yet

- Ghana Double Taxation and Double Taxation TreatiesDocument6 pagesGhana Double Taxation and Double Taxation Treatiesbr942vhj8xNo ratings yet

- TX Text Control WordsDocument2 pagesTX Text Control Wordsritter.sjdNo ratings yet

- List of Rates of Withholding Tax of Dividends, Interest and Royalties Under The Respective Tax TreatiesDocument2 pagesList of Rates of Withholding Tax of Dividends, Interest and Royalties Under The Respective Tax TreatiesvictorchangNo ratings yet

- Gics Map 2018Document52 pagesGics Map 2018KingJulienNo ratings yet

- Withholding Tax Rate - 195Document1 pageWithholding Tax Rate - 195avishal_jainNo ratings yet

- TDS Rates Under DTAA Treaties: DividendDocument3 pagesTDS Rates Under DTAA Treaties: DividendRani AryaNo ratings yet

- Rangkuman Tarif P3BDocument5 pagesRangkuman Tarif P3BJuni PrastyanggaNo ratings yet

- Double Taxation Agreement RatesDocument2 pagesDouble Taxation Agreement RatesNovialita RestutiNo ratings yet

- Industry ClassificationDocument24 pagesIndustry ClassificationvineminaiNo ratings yet

- Ethiopia Fiscal Guide 2015 2016Document11 pagesEthiopia Fiscal Guide 2015 2016nefassilk branchNo ratings yet

- Tds Rates As Per DtaaDocument3 pagesTds Rates As Per DtaamahiNo ratings yet

- Mini Test On Writing Parts 2+3 - 27-7-2022Document10 pagesMini Test On Writing Parts 2+3 - 27-7-2022Quảng ĐạiNo ratings yet

- Updated VDS Rate Through Finance Act 2020Document2 pagesUpdated VDS Rate Through Finance Act 2020Hossain RonyNo ratings yet

- Acca f6 Taxation Vietnam 2012 Dec QuestionDocument13 pagesAcca f6 Taxation Vietnam 2012 Dec QuestionNguyễn GiangNo ratings yet

- Midterm Assignment No. 3Document3 pagesMidterm Assignment No. 3XaxxyNo ratings yet

- A Guide To UK Taxation-WithdrawnDocument28 pagesA Guide To UK Taxation-WithdrawnEMMANUEL MVIE ATANGANA MELINGUINo ratings yet

- Us Index Group Tax Withholding TableDocument2 pagesUs Index Group Tax Withholding TableAnne G.No ratings yet

- NO Nation Branch Profit Tax Dividends BPT Rate Exception For SPC Dividends PortfolioDocument4 pagesNO Nation Branch Profit Tax Dividends BPT Rate Exception For SPC Dividends PortfolioSatrio YuliawanNo ratings yet

- f6vnm 2007 Dec QDocument9 pagesf6vnm 2007 Dec QPhạm Hùng DũngNo ratings yet

- Taxation in Uganda: Tax AdministrationDocument9 pagesTaxation in Uganda: Tax AdministrationJeff QueiroNo ratings yet

- Taxation (Malawi) : Tuesday 2 December 2014Document12 pagesTaxation (Malawi) : Tuesday 2 December 2014angaNo ratings yet

- Acca f6 Taxation Vietnam 2012 Jun QuestionDocument12 pagesAcca f6 Taxation Vietnam 2012 Jun QuestionNguyễn GiangNo ratings yet

- Ots 24 24071 Presenta MaheswarDocument3 pagesOts 24 24071 Presenta Maheswarapi-3774915No ratings yet

- ALL RAIL FREIGHT TARIFF Wef 14 April 2016 EXIMDocument1 pageALL RAIL FREIGHT TARIFF Wef 14 April 2016 EXIMpravinreddyNo ratings yet

- C4-June 2015Document22 pagesC4-June 2015Biplob K. SannyasiNo ratings yet

- C. Summary of Final Tax Rates On Different Taxpayers: From PCSO and Lotto Amounting To P10,000 or Less-ExemptDocument1 pageC. Summary of Final Tax Rates On Different Taxpayers: From PCSO and Lotto Amounting To P10,000 or Less-ExemptNajira HassanNo ratings yet

- Corporate TaxDocument2 pagesCorporate TaxAnungo KaveleNo ratings yet

- Analysis SrinuDocument10 pagesAnalysis Srinuklumba2027No ratings yet

- The Australian EconomyDocument35 pagesThe Australian Economybiangbiang bangNo ratings yet

- NBFC Non NBFC RFQ Recd: Rishi Laser LTDDocument3 pagesNBFC Non NBFC RFQ Recd: Rishi Laser LTDSunil JoshiNo ratings yet

- 1.GST PPT Sessions1-2Document61 pages1.GST PPT Sessions1-2robertNo ratings yet

- Corporate Tax Rates Table - KPMG - GLOBAL PDFDocument5 pagesCorporate Tax Rates Table - KPMG - GLOBAL PDFBGBG11No ratings yet

- Taxation (Malawi) : Specimen Questions For June 2015Document10 pagesTaxation (Malawi) : Specimen Questions For June 2015angaNo ratings yet

- Chart PackDocument35 pagesChart Packxyan.zohar7No ratings yet

- Tax TreatyDocument54 pagesTax TreatyDevin WinataNo ratings yet

- F6mwi QPDocument15 pagesF6mwi QPangaNo ratings yet

- Acca f6 Taxation Vietnam 2011 Dec QuestionDocument14 pagesAcca f6 Taxation Vietnam 2011 Dec QuestionNguyễn GiangNo ratings yet

- Group 6 Tax AssignmentDocument14 pagesGroup 6 Tax Assignmentdianaowani2No ratings yet

- Pestal Analysis of Uk (United Kingdom)Document16 pagesPestal Analysis of Uk (United Kingdom)ganesh aNo ratings yet

- Correction in GST 27.05.2023Document11 pagesCorrection in GST 27.05.2023Lalli DeviNo ratings yet

- Taxation (Malawi) : Tuesday 3 June 2014Document11 pagesTaxation (Malawi) : Tuesday 3 June 2014angaNo ratings yet

- List of Services For Withholding VATDocument2 pagesList of Services For Withholding VATMd Joinal AbedinNo ratings yet

- TX VNM Examdocs 2018Document3 pagesTX VNM Examdocs 2018hung789No ratings yet

- All Rail Freight TariffDocument1 pageAll Rail Freight Tariffsoumyarm942No ratings yet

- Taxation (Malawi) : Tuesday 4 June 2013Document10 pagesTaxation (Malawi) : Tuesday 4 June 2013angaNo ratings yet

- All CountriesDocument3 pagesAll CountriesbrnjarcevskiNo ratings yet

- Revenue Statistics Asia and Pacific SingaporeDocument2 pagesRevenue Statistics Asia and Pacific SingaporeMiguel AguadoNo ratings yet

- Guide To Invest in IndonesiaDocument14 pagesGuide To Invest in IndonesiaMeliaMarliantySenjaIraniNo ratings yet

- SL No. Company Country of Origin Industry 41 Orange S.A. Food & Beverage FranceDocument5 pagesSL No. Company Country of Origin Industry 41 Orange S.A. Food & Beverage FranceSadia Islam 1925181660No ratings yet

- Withholding VAT Guideline 2015-2016Document20 pagesWithholding VAT Guideline 2015-2016banglauserNo ratings yet

- P Data Extract From World Development IndicatorsDocument14 pagesP Data Extract From World Development Indicatorseva gonzalez diazNo ratings yet

- Publication TaxationMYSDocument2 pagesPublication TaxationMYSsitinorasmat7275No ratings yet

- Taxi & Limousine Service Revenues World Summary: Market Values & Financials by CountryFrom EverandTaxi & Limousine Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Sfom Impl B2ceDocument28 pagesSfom Impl B2cesergio paredesNo ratings yet

- MM 0001Document3 pagesMM 0001belachew guwisoNo ratings yet

- Dr. Ibha Rani - New Product DevelopmentDocument25 pagesDr. Ibha Rani - New Product DevelopmentIbha RaniNo ratings yet

- Bbap2103 (Sample 3) PDFDocument10 pagesBbap2103 (Sample 3) PDFFaidz FuadNo ratings yet

- LESSON 1 (Week 1)Document6 pagesLESSON 1 (Week 1)Wilmark PalmaNo ratings yet

- Internship ProgrammingDocument3 pagesInternship ProgrammingJahangir ashrafNo ratings yet

- Reflection Paper: Laborers in The PhilippinesDocument6 pagesReflection Paper: Laborers in The PhilippinesJv ManuelNo ratings yet

- A Study On Online Payment Methods Among College Students With Special Reference To Christ CollegeDocument60 pagesA Study On Online Payment Methods Among College Students With Special Reference To Christ CollegeAnjaliNo ratings yet

- Tanmay Hagawane TYBBADocument19 pagesTanmay Hagawane TYBBAHetik PatelNo ratings yet

- Sci PDF 1710857465640Document65 pagesSci PDF 1710857465640kasarmama7No ratings yet

- JD 60 13Document13 pagesJD 60 13nlrbdocsNo ratings yet

- 04 Materials 2030 Initiative INL Lars MonteliusDocument22 pages04 Materials 2030 Initiative INL Lars MonteliusGenci TepelenaNo ratings yet

- December 2022 InvoiceDocument2 pagesDecember 2022 InvoiceMegha NandiwalNo ratings yet

- Lecture 10 - Spending and Output in Short-Run-1Document25 pagesLecture 10 - Spending and Output in Short-Run-1Othniel MalikebuNo ratings yet

- Sources of Finance Opted by Reliance Industries: Share CapitalDocument4 pagesSources of Finance Opted by Reliance Industries: Share Capitalabhishek anandNo ratings yet

- PART 1 An Overview of Strategic Retail Management 21: Chapter 1 An Introduction To Retailing 22Document1 pagePART 1 An Overview of Strategic Retail Management 21: Chapter 1 An Introduction To Retailing 22AlesmanNo ratings yet

- Macro EcomomicsDocument120 pagesMacro EcomomicsHATCATENo ratings yet

- Guidelines On PD and LGD Estimation (EBA-GL-2017-16) - Chapters 1,2,3 (Only PD Estimation Part) PDFDocument200 pagesGuidelines On PD and LGD Estimation (EBA-GL-2017-16) - Chapters 1,2,3 (Only PD Estimation Part) PDFShankar RavichandranNo ratings yet

- Mohibur Rahman Bank Savings New 4pageDocument4 pagesMohibur Rahman Bank Savings New 4pageUmasankarNo ratings yet

- Gold Hofer BrochureDocument31 pagesGold Hofer BrochuresalaverriaNo ratings yet

- G Ym 6 F 8 HEtoev 4 GEbDocument6 pagesG Ym 6 F 8 HEtoev 4 GEbPrakhar AgarwalNo ratings yet

- Religare Report Print PDFDocument50 pagesReligare Report Print PDFumeshtyagi011233% (3)

- Statement of PurposeDocument2 pagesStatement of PurposeSandra ThomasNo ratings yet

- SR - No. Security - Name Isin Scrip - ID Intraday Stock ListDocument10 pagesSR - No. Security - Name Isin Scrip - ID Intraday Stock ListSashang S VNo ratings yet

- REFERENCESDocument10 pagesREFERENCESRona Faith TanduyanNo ratings yet

- Consumer Reactions To Sustainable PackagingDocument10 pagesConsumer Reactions To Sustainable Packagingxi si xingNo ratings yet