You might also like

- The Battle For Value FedEx UPSDocument23 pagesThe Battle For Value FedEx UPSHeo Mam100% (1)

- GST Council 43rd Meeting Key RecommendationsDocument6 pagesGST Council 43rd Meeting Key Recommendationssuhani singhNo ratings yet

- ST ND: 1 - Ca Shubham Khaitan S.Khaitan and AssociatesDocument9 pagesST ND: 1 - Ca Shubham Khaitan S.Khaitan and AssociatesTaruna BajajNo ratings yet

- Press Release Part A. Law and Procedure Related Changes: Form Gstr-9 Form Gstr-9C Form Gstr-1 Form GSTR-1 Form Gstr-1Document3 pagesPress Release Part A. Law and Procedure Related Changes: Form Gstr-9 Form Gstr-9C Form Gstr-1 Form GSTR-1 Form Gstr-1CA Ishu BansalNo ratings yet

- Budget Analysis 2012Document26 pagesBudget Analysis 2012Rajpreet KaurNo ratings yet

- Task 8Document23 pagesTask 8Anooja SajeevNo ratings yet

- Vinuth Hegde and Co - Finance Budget Lega - Feb 2023Document6 pagesVinuth Hegde and Co - Finance Budget Lega - Feb 2023Raghav HNo ratings yet

- Composition SchemeDocument4 pagesComposition Schemecloudstorage567No ratings yet

- Finance Budget 2023Document4 pagesFinance Budget 2023SakshamNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Budget 2021 Highlights SummaryDocument10 pagesBudget 2021 Highlights Summarybackup mypcNo ratings yet

- Salient Features For The Budget 2010-11Document11 pagesSalient Features For The Budget 2010-11kaashifhassanNo ratings yet

- Changes in GSTDocument4 pagesChanges in GSTRanjodh KaurNo ratings yet

- Chemexcil: Key Highlights & Provisions For Exports/ Chemicals SectorDocument6 pagesChemexcil: Key Highlights & Provisions For Exports/ Chemicals SectorRRSNo ratings yet

- Press Information Bureau Government of India Ministry of FinanceDocument3 pagesPress Information Bureau Government of India Ministry of Financekumar45caNo ratings yet

- Public Economics Assignment by Group EDocument22 pagesPublic Economics Assignment by Group EShreya DubeyNo ratings yet

- Taxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTDocument5 pagesTaxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTTheEnigmatic AccountantNo ratings yet

- Federal & Provincial Finance Acts, 2022 SummaryDocument61 pagesFederal & Provincial Finance Acts, 2022 SummaryABODE PVT LIMITEDNo ratings yet

- Analysis of 10 Important Changes in GST From 1st October 2022 - Taxguru - in PDFDocument4 pagesAnalysis of 10 Important Changes in GST From 1st October 2022 - Taxguru - in PDFPawan AswaniNo ratings yet

- Goods and Service Tax NoDocument5 pagesGoods and Service Tax NonitinNo ratings yet

- Financial Budget 2013Document9 pagesFinancial Budget 2013Mitesh PanchalNo ratings yet

- AFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)Document14 pagesAFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)salahuddin ahmedNo ratings yet

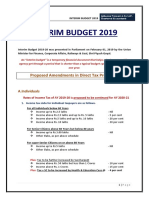

- Interim Budget 2019: Proposed Amendments in Direct Tax ProvisionsDocument4 pagesInterim Budget 2019: Proposed Amendments in Direct Tax ProvisionsaaNo ratings yet

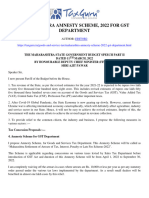

- Maharashtra Amnesty Scheme, 2022 for GST Department- taxguru.inDocument4 pagesMaharashtra Amnesty Scheme, 2022 for GST Department- taxguru.inDINESH CHANCHALANINo ratings yet

- GST Update125 PDFDocument6 pagesGST Update125 PDFTharun RajNo ratings yet

- Budget 2023 - SummaryDocument2 pagesBudget 2023 - SummaryAliNo ratings yet

- QRMP Scheme Under GSTDocument7 pagesQRMP Scheme Under GSTshraddhaNo ratings yet

- Tax Alert, National Budget Synopsis 2023Document7 pagesTax Alert, National Budget Synopsis 2023bhim.dhamiNo ratings yet

- Press Release 52 GST CouncilDocument6 pagesPress Release 52 GST CouncilCA Thirumalesu ENo ratings yet

- Salient Features For Income TaxDocument6 pagesSalient Features For Income TaxRimsha AslamNo ratings yet

- GST Council Recommends Relief for Small BusinessesDocument2 pagesGST Council Recommends Relief for Small BusinessesSaurabh SinghNo ratings yet

- PressRelease 22ndGSTCMeetingDocument2 pagesPressRelease 22ndGSTCMeetingShail MehtaNo ratings yet

- Press Release: Composition SchemeDocument2 pagesPress Release: Composition SchemeRojalin BiswsasNo ratings yet

- Amity Global Business School, PuneDocument15 pagesAmity Global Business School, PuneChand KalraNo ratings yet

- Salient Features Income Tax)Document5 pagesSalient Features Income Tax)bbaahmad89No ratings yet

- Project Report On BUDGET (2022-23) : Computer Applications in BusinessDocument15 pagesProject Report On BUDGET (2022-23) : Computer Applications in BusinessDeepu yadavNo ratings yet

- Budget 2010 in Small Scale IndustriesDocument9 pagesBudget 2010 in Small Scale Industriesurz_spiderman2630No ratings yet

- GST Amendment For June 2023 Part 3Document3 pagesGST Amendment For June 2023 Part 3rajbhanushali3981No ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- Central Taxes Replaced by GSTDocument6 pagesCentral Taxes Replaced by GSTBijosh ThomasNo ratings yet

- RSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Document17 pagesRSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Rohan JainNo ratings yet

- GST Amendments For June 22 Students by CA Vivek GabaDocument6 pagesGST Amendments For June 22 Students by CA Vivek GabayashNo ratings yet

- The Financial Kaleidoscope - July 19 PDFDocument8 pagesThe Financial Kaleidoscope - July 19 PDFhemanth1128No ratings yet

- GST Amendments For Circulation - Nov 2018 UploadedDocument20 pagesGST Amendments For Circulation - Nov 2018 UploadedJay SuchakNo ratings yet

- Fiscal Policy of BangladeshDocument12 pagesFiscal Policy of BangladeshMd HarunNo ratings yet

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 pagesCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsNo ratings yet

- Budget Chemistry 2010Document44 pagesBudget Chemistry 2010Aq SalmanNo ratings yet

- Chapter 8 Composition Scheme Under GSTDocument12 pagesChapter 8 Composition Scheme Under GSTDR. PREETI JINDALNo ratings yet

- Budget Highlights Athena Law-R1Document4 pagesBudget Highlights Athena Law-R1Ashar AkhtarNo ratings yet

- 1.0 Direct Taxes: India Budget 2014 - 15 - in A NutshellDocument3 pages1.0 Direct Taxes: India Budget 2014 - 15 - in A Nutshell61srinihemaNo ratings yet

- Tax Reform For Acceleration and Inclusion (Train) Act (RA # 10963)Document4 pagesTax Reform For Acceleration and Inclusion (Train) Act (RA # 10963)thepoetsedgeNo ratings yet

- Do You Know GST - August 2021Document11 pagesDo You Know GST - August 2021CA Ranjan MehtaNo ratings yet

- Nepal Budget Highlights - 79-80 - APM & AssociatesDocument89 pagesNepal Budget Highlights - 79-80 - APM & Associatesaasthapoddar155No ratings yet

- Changes in GtaDocument5 pagesChanges in GtaTushar SuriNo ratings yet

- Budget 2021Document9 pagesBudget 2021VRINDA GUPTANo ratings yet

- Special Updates For Prihatin Tambahan and Income Tax Matter During Movement Control Order PeriodDocument4 pagesSpecial Updates For Prihatin Tambahan and Income Tax Matter During Movement Control Order Periodshah7592No ratings yet

- 37th GST Council Meet Final Press Release GSTPW 20092019Document2 pages37th GST Council Meet Final Press Release GSTPW 20092019AVASTNo ratings yet

- 37 Meeting of The GST Council, Goa 20 September, 2019 Press ReleaseDocument2 pages37 Meeting of The GST Council, Goa 20 September, 2019 Press ReleasePranay SaxenaNo ratings yet

- 37th GSTC Meeting - 02Document2 pages37th GSTC Meeting - 02Sahil ShahNo ratings yet

- AcvdvdDocument4 pagesAcvdvdvivek kasamNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Taxation of Gains From Share Sales: A Guide to Capital Gains Tax RulesDocument5 pagesTaxation of Gains From Share Sales: A Guide to Capital Gains Tax Rulesphani raja kumarNo ratings yet

- New FVU Changes and Enhancements in SaralTDS v15.07Document3 pagesNew FVU Changes and Enhancements in SaralTDS v15.07phani raja kumarNo ratings yet

- Check Email Settings in Saral TDSDocument1 pageCheck Email Settings in Saral TDSphani raja kumarNo ratings yet

- Vat 112Document2 pagesVat 112phani raja kumarNo ratings yet

- Star Health Assure - One Pager - Version 1.0 - April - 2022Document3 pagesStar Health Assure - One Pager - Version 1.0 - April - 2022Shihb100% (1)

- I Disabled HiberfilDocument3 pagesI Disabled Hiberfilphani raja kumarNo ratings yet

- Compendium of MSMEDocument65 pagesCompendium of MSMEChaitra KatragaddaNo ratings yet

- ACT Invoice FOR JANDocument2 pagesACT Invoice FOR JANphani raja kumarNo ratings yet

- Affidavit Declaring Free Rent for Society LocationDocument1 pageAffidavit Declaring Free Rent for Society Locationphani raja kumarNo ratings yet

- Leelavati Service Tax ReturnDocument6 pagesLeelavati Service Tax Returnphani raja kumarNo ratings yet

- Socieity Registration Required DetailsDocument1 pageSocieity Registration Required Detailsphani raja kumarNo ratings yet

- Channels ListDocument2 pagesChannels Listphani raja kumarNo ratings yet

- Stampduty For Firm ReconstitutionDocument2 pagesStampduty For Firm Reconstitutionphani raja kumarNo ratings yet

- Practical Aspects of Availing Credit in Respect of Invoices Not Appearing in Form GSTR 2A or GSTR 2BDocument6 pagesPractical Aspects of Availing Credit in Respect of Invoices Not Appearing in Form GSTR 2A or GSTR 2Bphani raja kumarNo ratings yet

- Income Tax Scrutiny NormsDocument6 pagesIncome Tax Scrutiny Normsphani raja kumarNo ratings yet

- Impact of Non Submission of Export Intimation Within The Prescribed Time in Case of ct-3Document6 pagesImpact of Non Submission of Export Intimation Within The Prescribed Time in Case of ct-3phani raja kumarNo ratings yet

- Incorporation of CompanyDocument4 pagesIncorporation of Companyphani raja kumarNo ratings yet

- Compensation Under RR Act and Vijayawada Rural DetailsDocument2 pagesCompensation Under RR Act and Vijayawada Rural Detailsphani raja kumarNo ratings yet

- How To Claim Income Tax Refund of TDS For Last Six YearsDocument1 pageHow To Claim Income Tax Refund of TDS For Last Six Yearsphani raja kumarNo ratings yet

- Q1. Whether HUF can do business in its own nameDocument16 pagesQ1. Whether HUF can do business in its own namephani raja kumarNo ratings yet

- Verification of Applicant in Case of Form DIN-1 As Per Annexure I of The DIN RulesDocument1 pageVerification of Applicant in Case of Form DIN-1 As Per Annexure I of The DIN Rulesphani raja kumarNo ratings yet

- Central Excise Duty Rates Chapter Wise Changes in Budget 2015-16Document34 pagesCentral Excise Duty Rates Chapter Wise Changes in Budget 2015-16phani raja kumarNo ratings yet

- GOODS SOLD ON MRP BASIS IS EXEMPTED FROM SERVICE TAX Circular No.173 - 8 - 2013 - ST, Dated 07-10-2013Document1 pageGOODS SOLD ON MRP BASIS IS EXEMPTED FROM SERVICE TAX Circular No.173 - 8 - 2013 - ST, Dated 07-10-2013phani raja kumarNo ratings yet

- ICSI E-Bulletin MAY - JUNE 2014Document59 pagesICSI E-Bulletin MAY - JUNE 2014phani raja kumarNo ratings yet

- Central Excise Job Work RulesDocument3 pagesCentral Excise Job Work RulesSameer HusainNo ratings yet

- Revision of CST Assessments for 2005-06 and 2006-07Document1 pageRevision of CST Assessments for 2005-06 and 2006-07phani raja kumarNo ratings yet

- Rectification ManualDocument25 pagesRectification Manualwww.TdsTaxIndia.comNo ratings yet

- Cost Inflation Index Notified by Indian Government 1981-2012Document1 pageCost Inflation Index Notified by Indian Government 1981-2012Ritesh AgarwalNo ratings yet

- APPT RegistrationDocument2 pagesAPPT Registrationphani raja kumarNo ratings yet

- Chapter 61 Central ExciseDocument1 pageChapter 61 Central Excisephani raja kumarNo ratings yet

- Ci Awb Sample Rootcroop Ofi 28.07.2023Document3 pagesCi Awb Sample Rootcroop Ofi 28.07.2023hendy febrianiNo ratings yet

- Merchandising ADocument2 pagesMerchandising AHesham Am-LiNo ratings yet

- Accounting For Share Capital (2019-20)Document20 pagesAccounting For Share Capital (2019-20)niyatiagarwal25No ratings yet

- United States v. Brosnan, 363 U.S. 237 (1960)Document20 pagesUnited States v. Brosnan, 363 U.S. 237 (1960)Scribd Government DocsNo ratings yet

- LA Statute SpouseDocument4 pagesLA Statute SpouseRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- NSTP ReqDocument13 pagesNSTP ReqChristine EspantoNo ratings yet

- FedEx Malaysia International Export RatesDocument11 pagesFedEx Malaysia International Export RatesnanananacmonNo ratings yet

- MSCI Feb11 IndexCalcMethodologyDocument103 pagesMSCI Feb11 IndexCalcMethodologybboyvnNo ratings yet

- Y Combinator S Pocket Guide To Seed Fundraising 1692908038Document1 pageY Combinator S Pocket Guide To Seed Fundraising 1692908038DanNo ratings yet

- The President's Committee on Urban Housing ReportDocument264 pagesThe President's Committee on Urban Housing ReportGabrielGaunyNo ratings yet

- Rockman Industries Jan 2020 ICRADocument9 pagesRockman Industries Jan 2020 ICRAPuneet367No ratings yet

- Grimaldo, Marvin: Kawanihan NG Rentas Internas For Compensation Payment With or Without Tax WithheldDocument2 pagesGrimaldo, Marvin: Kawanihan NG Rentas Internas For Compensation Payment With or Without Tax WithheldFranc Anthony GalaoNo ratings yet

- Auditing: Integral To The Economy: Chapter 1Document48 pagesAuditing: Integral To The Economy: Chapter 1Alain Fung Land MakNo ratings yet

- SQB 1017020Document290 pagesSQB 1017020Екатерина ПетроваNo ratings yet

- 10 Redington ImmunizationDocument13 pages10 Redington ImmunizationderNo ratings yet

- Capital Gain Tax-CGT System: NCCPLDocument49 pagesCapital Gain Tax-CGT System: NCCPLNaveed KhanNo ratings yet

- Icici BankDocument108 pagesIcici Bankmultanigazal_4254062100% (3)

- VLS Cooper at Risk Reactor ReportDocument47 pagesVLS Cooper at Risk Reactor ReportRuss ZimmerNo ratings yet

- Slater Best Guess Issue 2 Article For WebsiteDocument2 pagesSlater Best Guess Issue 2 Article For Websiteapi-400507461No ratings yet

- Abyssinia Bank Charts Noteworthy Profit, Dividend ClimbDocument7 pagesAbyssinia Bank Charts Noteworthy Profit, Dividend ClimbBernabasNo ratings yet

- ZICA T6 - ManagementDocument91 pagesZICA T6 - ManagementMongu Rice100% (7)

- Cash and Cash Equivalents Reconciliation ProblemsDocument50 pagesCash and Cash Equivalents Reconciliation ProblemsAnne EstrellaNo ratings yet

- Social Housing Programme Feasibility StudyDocument61 pagesSocial Housing Programme Feasibility StudyNitin Chandra100% (1)

- Internship Report On Loan & Deposit Policy of HBLDocument52 pagesInternship Report On Loan & Deposit Policy of HBLLochan Khanal100% (3)

- Finance Formula SheetDocument4 pagesFinance Formula Sheetdjlyfe100% (1)

- Procedures On Pag-IBIG Online Registration - OdtDocument3 pagesProcedures On Pag-IBIG Online Registration - OdtKrishia Mae VillalunaNo ratings yet

- Impact of Cashless Economy On Common Man in India: Pappu B. Metri & Doddayallappa JindappaDocument3 pagesImpact of Cashless Economy On Common Man in India: Pappu B. Metri & Doddayallappa Jindappajasleen kaurNo ratings yet

- Reliable Taxi Service Business PlanDocument31 pagesReliable Taxi Service Business PlanHarry H Gaiya100% (2)