You might also like

- Matter and Chemistry - Property Changes QuizDocument1 pageMatter and Chemistry - Property Changes Quizapi-368213959No ratings yet

- A Study of The Impact of 80-20 Rule On Social Media Marketing - Sameer A SawantDocument8 pagesA Study of The Impact of 80-20 Rule On Social Media Marketing - Sameer A SawantSawant SameerNo ratings yet

- Ey 2022 WCTG WebDocument2,010 pagesEy 2022 WCTG WebPedro J Contreras ContrerasNo ratings yet

- Poka Yoke PDFDocument62 pagesPoka Yoke PDFmartinNo ratings yet

- BCG Full Case PDFDocument11 pagesBCG Full Case PDFdwi andi rohmatika100% (1)

- Case Study TPM Jet AirwaysDocument15 pagesCase Study TPM Jet AirwaysSanjay Domdiya100% (1)

- Slavery in The Chocolate IndustryDocument1 pageSlavery in The Chocolate Industryannett_6164No ratings yet

- Writing A Case AnalysisDocument4 pagesWriting A Case AnalysisTun Thu LinNo ratings yet

- Audit of Warehouse and InventoryDocument51 pagesAudit of Warehouse and InventoryArun Karthikeyan100% (2)

- Use of Business / Accountancy Models: Annotated Examples of Research and Analysis - Topic 8Document2 pagesUse of Business / Accountancy Models: Annotated Examples of Research and Analysis - Topic 8Reznov KovacicNo ratings yet

- Case Study of Enron ScandalDocument8 pagesCase Study of Enron ScandalYawen Li67% (3)

- Writing A Case AnalysisDocument4 pagesWriting A Case AnalysisTun Thu Lin0% (1)

- Rule 4 Golden Arches Development VS ST FrancisDocument1 pageRule 4 Golden Arches Development VS ST FrancisJoh MadumNo ratings yet

- Fisher and RamanDocument15 pagesFisher and RamanTun Thu LinNo ratings yet

- Commercial Wire and Raceway Chart and FormulasDocument2 pagesCommercial Wire and Raceway Chart and FormulasRaul GuerraNo ratings yet

- Final PPC Module Ahmed Stone CrushingDocument26 pagesFinal PPC Module Ahmed Stone Crushingzain10684No ratings yet

- Yea-Tos-S606 11 ADocument1 pageYea-Tos-S606 11 AMikolaj KopernikNo ratings yet

- Base Character EXP Class EXPDocument13 pagesBase Character EXP Class EXPRandom UploadNo ratings yet

- Philippine Agricultural Engineering Standard PAES 305: 2000Document5 pagesPhilippine Agricultural Engineering Standard PAES 305: 2000Melanie Saldivar CapalunganNo ratings yet

- Libro1 ROKDocument3 pagesLibro1 ROKghostnetrdNo ratings yet

- ABB - R ContactorsDocument196 pagesABB - R Contactorstvrao161No ratings yet

- AWG - American Wire Gauge and Circular MilsDocument2 pagesAWG - American Wire Gauge and Circular Milssteve_yNo ratings yet

- AWG - American Wire Gauge and Circular MilsDocument2 pagesAWG - American Wire Gauge and Circular Milssteve_yNo ratings yet

- ABB Motor FLCDocument1 pageABB Motor FLCedalzurcNo ratings yet

- Generator KVA KW Amp ChartDocument2 pagesGenerator KVA KW Amp ChartSajid MahmoodNo ratings yet

- Generator kVA-kW-Amp Chart PDFDocument2 pagesGenerator kVA-kW-Amp Chart PDFAEE MHCH Sub Div 1stNo ratings yet

- Sales CV Divisi 1 MTD & Ytd Until 02 May, Mds Mandau 258Document1 pageSales CV Divisi 1 MTD & Ytd Until 02 May, Mds Mandau 258julio prathama nugrahaNo ratings yet

- Order Status Custom Date - Custom Date From 19/09/2021 To 19/09/2021Document12 pagesOrder Status Custom Date - Custom Date From 19/09/2021 To 19/09/2021sayem00001No ratings yet

- Iv. Realización Del Experimento Y Obtención de DatosDocument5 pagesIv. Realización Del Experimento Y Obtención de DatosJONAS CORREA PÉREZNo ratings yet

- Tugas Besar Struktur Baja Ii (HSKB 405)Document1 pageTugas Besar Struktur Baja Ii (HSKB 405)ROSA PHETY PERMATASARINo ratings yet

- Tabla Dosificación, SQMDocument1 pageTabla Dosificación, SQMJimmyHansNo ratings yet

- AADT & Growth RateDocument6 pagesAADT & Growth Ratesuddhashil purkaitNo ratings yet

- Statement of DAMDocument7 pagesStatement of DAMSunny SinghNo ratings yet

- Diffractogram PG-190034-2 41562Document2 pagesDiffractogram PG-190034-2 41562aditya haryantoNo ratings yet

- Audi Fact Pack q4 - 2021Document15 pagesAudi Fact Pack q4 - 2021Alejandrina Salazar gonzalesNo ratings yet

- Tahu N Curah Hujan Andalan Pada Bulan (MM) Jan Feb Mar Apr Mei Jun Jul Agus Sep Okt Nov DesDocument10 pagesTahu N Curah Hujan Andalan Pada Bulan (MM) Jan Feb Mar Apr Mei Jun Jul Agus Sep Okt Nov Desdewi fatmawatiNo ratings yet

- FUNGILAB Patrones de Viscosidad para Usos GeneralesDocument5 pagesFUNGILAB Patrones de Viscosidad para Usos GeneralesOscar Guzman CastroNo ratings yet

- Nss WF Ibeam TableDocument5 pagesNss WF Ibeam TableNico ScheggiaNo ratings yet

- A Contactors ABB CatalogDocument78 pagesA Contactors ABB CatalogSami SalmanNo ratings yet

- 1SBC100179C0201 Main Catalog Motor Protection and ControlDocument160 pages1SBC100179C0201 Main Catalog Motor Protection and ControlTSA METERING RUV BALIKPAPANNo ratings yet

- Marketing Dashboard: Total Leads This MonthDocument12 pagesMarketing Dashboard: Total Leads This Monthmaya bangunNo ratings yet

- NPV Mining Schedule April 09Document14 pagesNPV Mining Schedule April 09Agus BudiluhurNo ratings yet

- 01 - Summary of 2022 Power StatisticsDocument2 pages01 - Summary of 2022 Power StatisticsLealyn V. MadayagNo ratings yet

- Card LVL XP Class XP Number Total XP Total CXPDocument6 pagesCard LVL XP Class XP Number Total XP Total CXPKenneth BuñagNo ratings yet

- Project1 CustomDashboardDocument12 pagesProject1 CustomDashboardmimikrose82No ratings yet

- Assets & Liabilities Committee Report: Performance Management & MonitoringDocument15 pagesAssets & Liabilities Committee Report: Performance Management & MonitoringMichael OseleNo ratings yet

- QTR PVB 12-720 PVB 34-720 PVB 1-720 PVB 34-420 PVB 1-420: TotalDocument3 pagesQTR PVB 12-720 PVB 34-720 PVB 1-720 PVB 34-420 PVB 1-420: TotalSaswata ChoudhuryNo ratings yet

- Articulo Num OF Fecha Proceso FormatoDocument4 pagesArticulo Num OF Fecha Proceso Formatoerika cubidesNo ratings yet

- Abaque Coullissant I H U v1Document4 pagesAbaque Coullissant I H U v1lhabsNo ratings yet

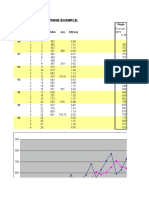

- Exponential Smoothing Example:: Single Years Quarter Period Sales Avg A (T) /avgDocument6 pagesExponential Smoothing Example:: Single Years Quarter Period Sales Avg A (T) /avgchikomborero maranduNo ratings yet

- Calculos TotalDocument29 pagesCalculos TotalMaria De Los Angeles YomeyeNo ratings yet

- ABB Styczniki enDocument196 pagesABB Styczniki enIñaki PereaNo ratings yet

- Full Load AmpsDocument2 pagesFull Load AmpsambuenaflorNo ratings yet

- ABB Short Form Motor Protection and ControlDocument180 pagesABB Short Form Motor Protection and Controlmansa122No ratings yet

- Ies Indoor Report Photometric Filename: Bs101Ecoled4Sawt40120V-277V - P.Ies DESCRIPTION INFORMATION (From Photometric File)Document11 pagesIes Indoor Report Photometric Filename: Bs101Ecoled4Sawt40120V-277V - P.Ies DESCRIPTION INFORMATION (From Photometric File)Ankit JainNo ratings yet

- Apdx A SectionsDocument15 pagesApdx A SectionsMongkol JirawacharadetNo ratings yet

- 6x25fi Iwrc 2012Document1 page6x25fi Iwrc 2012ELZEKKIWIRENo ratings yet

- Table 5 - BridgesDocument1 pageTable 5 - Bridgesjubin funterNo ratings yet

- Tabla. A-21e MariaDocument4 pagesTabla. A-21e MariaMARIA BELEN VARELA MENDOZANo ratings yet

- WindDocument5 pagesWindCarlos Tadeo CapistranNo ratings yet

- X F FX FX F / (N: Chapter 20, Page 1/29Document30 pagesX F FX FX F / (N: Chapter 20, Page 1/29Carlos SanchezNo ratings yet

- Lab 6 - Industry ReportDocument6 pagesLab 6 - Industry ReportKen NgNo ratings yet

- Cost Per MeterDocument14 pagesCost Per MeternaseebNo ratings yet

- Perú: Producto Bruto Interno Según Actividad Económica (Nivel 9), 1994-2019Document3 pagesPerú: Producto Bruto Interno Según Actividad Económica (Nivel 9), 1994-2019FBANo ratings yet

- Data ReleaseDocument5 pagesData ReleaseAfiq de WinnerNo ratings yet

- UntitledDocument11 pagesUntitledNina Keith DimayugaNo ratings yet

- Hidrostatic Bonjean - 0216030029 - Abdul Azis Rev2 - Area 20m2Document43 pagesHidrostatic Bonjean - 0216030029 - Abdul Azis Rev2 - Area 20m2Abdul AzisNo ratings yet

- Data Dipole-Dipole IpDocument48 pagesData Dipole-Dipole IpDinanNo ratings yet

- Eurpe Optionnov Dec January February March A Ab Au Aa Aq Ay TotalDocument3 pagesEurpe Optionnov Dec January February March A Ab Au Aa Aq Ay TotalReza Pria UtamaNo ratings yet

- 2017 Enrolled and Graduates by Region, Type of Provider and SexDocument4 pages2017 Enrolled and Graduates by Region, Type of Provider and SexPaul BautistaNo ratings yet

- Drive Load Date /time /duration Igv/Bpc: Unit#3 Performance Data Feb 2020Document40 pagesDrive Load Date /time /duration Igv/Bpc: Unit#3 Performance Data Feb 2020kattukoluNo ratings yet

- Cuadro 026Document1 pageCuadro 026dgmamanigomezNo ratings yet

- Example Holt Winter S Additive ModelDocument7 pagesExample Holt Winter S Additive Modelthanusha selvamanyNo ratings yet

- Optical and Electronic Properties of Mo:Zno Thin Films Deposited Using RF Magnetron Sputtering With Different Process ParametersDocument10 pagesOptical and Electronic Properties of Mo:Zno Thin Films Deposited Using RF Magnetron Sputtering With Different Process ParametersTun Thu LinNo ratings yet

- Studi Kasus Hewlett Packard Company DeskDocument2 pagesStudi Kasus Hewlett Packard Company DeskTun Thu LinNo ratings yet

- How To Advance Theory Through Literature Reviews in Logistics and Supply Chain ManagementDocument18 pagesHow To Advance Theory Through Literature Reviews in Logistics and Supply Chain ManagementTun Thu LinNo ratings yet

- An Overview of Blockchain in Supply Chain Management: Benefits and IssuesDocument11 pagesAn Overview of Blockchain in Supply Chain Management: Benefits and IssuesTun Thu LinNo ratings yet

- HP Deskjet Printer Supply Chain: Operations ManagementDocument7 pagesHP Deskjet Printer Supply Chain: Operations ManagementTun Thu LinNo ratings yet

- Fisher and Raman - 2Document14 pagesFisher and Raman - 2Tun Thu LinNo ratings yet

- Detail Report ObermeyerDocument33 pagesDetail Report ObermeyerTun Thu LinNo ratings yet

- Correlation Minor Norms, Entanglement Detection and Discord: Bar Y. Peled, Amit Te'eni, Avishy Carmi & Eliahu CohenDocument10 pagesCorrelation Minor Norms, Entanglement Detection and Discord: Bar Y. Peled, Amit Te'eni, Avishy Carmi & Eliahu CohenTun Thu LinNo ratings yet

- Quantum Entanglement Maintained by Virtual Excitations in An U LTR Ast Ron Gly Co Upl Ed Oscillator SystemDocument13 pagesQuantum Entanglement Maintained by Virtual Excitations in An U LTR Ast Ron Gly Co Upl Ed Oscillator SystemTun Thu LinNo ratings yet

- Physics 5Document13 pagesPhysics 5Tun Thu LinNo ratings yet

- Writing A Case AnalysisDocument4 pagesWriting A Case AnalysisTun Thu LinNo ratings yet

- Physics 1Document11 pagesPhysics 1Tun Thu LinNo ratings yet

- Hewlett-Packard: Deskjet Printer Supply ChainDocument18 pagesHewlett-Packard: Deskjet Printer Supply ChainTun Thu LinNo ratings yet

- Assignment 1B - HP Case Study Assignment 1B - HP Case StudyDocument5 pagesAssignment 1B - HP Case Study Assignment 1B - HP Case StudyTun Thu LinNo ratings yet

- Hewlett Hewlett - Packard Co. Packard Co.: Deskjet Deskjet Printer Supply Chain Printer Supply ChainDocument31 pagesHewlett Hewlett - Packard Co. Packard Co.: Deskjet Deskjet Printer Supply Chain Printer Supply ChainTun Thu LinNo ratings yet

- EPGP HP Desk Jet Supply Chain Group 6 EPGP HP Desk Jet Supply Chain Group 6Document8 pagesEPGP HP Desk Jet Supply Chain Group 6 EPGP HP Desk Jet Supply Chain Group 6Tun Thu LinNo ratings yet

- Electronic Reservation Slip (ERS) : 2100858446 12056/Ndls Janshtabdi Second Sitting (RESERVED) (2S)Document3 pagesElectronic Reservation Slip (ERS) : 2100858446 12056/Ndls Janshtabdi Second Sitting (RESERVED) (2S)vineetkr.2349No ratings yet

- Servicenow Interview Question and AnswersDocument72 pagesServicenow Interview Question and Answersswapneshsurwade29No ratings yet

- Option Pricing Using Artificial Neural NetworksDocument201 pagesOption Pricing Using Artificial Neural NetworksemmunarNo ratings yet

- Microbankingbulletin Spring09 PDFDocument98 pagesMicrobankingbulletin Spring09 PDFMuhammad Salman ArrifqyNo ratings yet

- YSEALI PFP 2024 Recruitment FlyerDocument3 pagesYSEALI PFP 2024 Recruitment Flyerjenlyhau01No ratings yet

- Corporate StrategyDocument15 pagesCorporate StrategyAbhilasha BagariyaNo ratings yet

- The Good, The Bad, and The Ugly of Extract Transform Load (Etl)Document5 pagesThe Good, The Bad, and The Ugly of Extract Transform Load (Etl)JyothiMNo ratings yet

- ICAEW Accounting QB 2023Document80 pagesICAEW Accounting QB 2023daolengan03No ratings yet

- Mis 5 5Th Edition Bidgoli Solutions Manual Full Chapter PDFDocument22 pagesMis 5 5Th Edition Bidgoli Solutions Manual Full Chapter PDFvictoredanajdnk9100% (8)

- Inb 304Document10 pagesInb 304Rebaka Alam KhanNo ratings yet

- KMRC MTN 2021 Information Memorandum January 2022Document142 pagesKMRC MTN 2021 Information Memorandum January 2022K MNo ratings yet

- Meeting 3-Group 2-How Do Firms Adapt To Discontinuous Change PDFDocument24 pagesMeeting 3-Group 2-How Do Firms Adapt To Discontinuous Change PDFArdian MustofaNo ratings yet

- Ba 4055 Warehouse ManagementDocument40 pagesBa 4055 Warehouse ManagementDEAN RESEARCH AND DEVELOPMENT100% (1)

- 5.8 Motivation and Reward in The Age of Continuous Improvement.Document5 pages5.8 Motivation and Reward in The Age of Continuous Improvement.NPR CETNo ratings yet

- Test Bank For Valuation Measuring and Managing The Value of Companies 6th by KollerDocument5 pagesTest Bank For Valuation Measuring and Managing The Value of Companies 6th by KollerJohn Ngo100% (24)

- Standard Terms and Conditions Senheng - APPLE IPHONE 12 1.0 Promotion PeriodDocument2 pagesStandard Terms and Conditions Senheng - APPLE IPHONE 12 1.0 Promotion PeriodcikgutiNo ratings yet

- 2020dec18 AgendaDocument206 pages2020dec18 AgendanikerNo ratings yet

- DTDCDocument1 pageDTDCAbdullah siddikiNo ratings yet

- 23 W Group 8 Final Project CapstoneDocument14 pages23 W Group 8 Final Project CapstoneQwertNo ratings yet