You might also like

- SA 200 300 SeriesDocument9 pagesSA 200 300 SeriesfgbrtbryhtyNo ratings yet

- Saflowcharts PDFDocument21 pagesSaflowcharts PDFdoopumail231No ratings yet

- Clearpar - Distressed Loan Trade SettlementDocument2 pagesClearpar - Distressed Loan Trade SettlementAyaz AhmedNo ratings yet

- Chapter 9 (3) : Completing The AuditDocument1 pageChapter 9 (3) : Completing The AuditARMIZAWANI BINTI MOHAMED BUANG BMNo ratings yet

- Aars Isa 300 Series Flowcharts by Sir Jamshaid AkhtarDocument13 pagesAars Isa 300 Series Flowcharts by Sir Jamshaid AkhtarahmadNo ratings yet

- Pa 2Document8 pagesPa 2Trần Ngọc NhưNo ratings yet

- Procedure Manual For QMS and ISO 9001:2015: Process Title: Processing of Complaints Related To Sites TitlingDocument2 pagesProcedure Manual For QMS and ISO 9001:2015: Process Title: Processing of Complaints Related To Sites TitlingTin MiguelNo ratings yet

- Midterm Solution cs302Document9 pagesMidterm Solution cs302Abdul WahabNo ratings yet

- Gathering Appropriate Audit Evidence: by Laura Morgan, Examiner - Professional 2 Audit PracticeDocument4 pagesGathering Appropriate Audit Evidence: by Laura Morgan, Examiner - Professional 2 Audit PracticeGodfrey MakurumureNo ratings yet

- Planning An Audit ISA 300: EP: Engagement Partner ET: Engagement TeamDocument2 pagesPlanning An Audit ISA 300: EP: Engagement Partner ET: Engagement TeamMuhammad AslamNo ratings yet

- 4 PDFDocument2 pages4 PDFsaket lohiaNo ratings yet

- Planning Phase - Guidelines For Observation of Physical InventoriesDocument5 pagesPlanning Phase - Guidelines For Observation of Physical InventoriesSelva Bavani SelwaduraiNo ratings yet

- Accounting Presentation: Group MembersDocument80 pagesAccounting Presentation: Group MembersvjyaserNo ratings yet

- Treasury Process FlowchartDocument7 pagesTreasury Process FlowchartNarayan KulkarniNo ratings yet

- Ghana KYC BusinessBankingDocument2 pagesGhana KYC BusinessBankingYulandi Strachan GerickeNo ratings yet

- Status of Actionable Points Raised by Internal Auditors in The Previous Audit Committee Meeting As UnderDocument2 pagesStatus of Actionable Points Raised by Internal Auditors in The Previous Audit Committee Meeting As Undersalini jhaNo ratings yet

- Comparison IFAC Other Jurisdictions 070127Document23 pagesComparison IFAC Other Jurisdictions 070127nemo2727No ratings yet

- Grading System (Refer To Course Plan) Forms of Business Sole ProprietorshipDocument24 pagesGrading System (Refer To Course Plan) Forms of Business Sole ProprietorshipDANIELLE TORRANCE ESPIRITUNo ratings yet

- 01 Property, Plant - EquipmentsDocument21 pages01 Property, Plant - EquipmentsRuwan GunarathnaNo ratings yet

- RPT Standalone Mar23Document2 pagesRPT Standalone Mar23Amit KumarNo ratings yet

- Cheat Sheet For Final Summary PDFDocument2 pagesCheat Sheet For Final Summary PDFQuy TranNo ratings yet

- G4 - Corporate Laws & Secretarial Practices Corporate Laws & Secretarial Practices Corporate Laws & Secretarial PracticesDocument3 pagesG4 - Corporate Laws & Secretarial Practices Corporate Laws & Secretarial Practices Corporate Laws & Secretarial Practicesfawad aslamNo ratings yet

- Mind Map 4Document1 pageMind Map 4darylle roblesNo ratings yet

- Audit and Assurance PrincipleDocument2 pagesAudit and Assurance PrincipleIsabell CastroNo ratings yet

- Internal Audit's Role in Third Party Risk Management (TPRM) : Jon Pastore, Nick FullmerDocument27 pagesInternal Audit's Role in Third Party Risk Management (TPRM) : Jon Pastore, Nick FullmerRoslan.Affandi2351100% (1)

- Annex 1 FLowchart Internal Communication PDFDocument1 pageAnnex 1 FLowchart Internal Communication PDFMadalina Croitoru RisteaNo ratings yet

- Section 321 Second OpinionDocument1 pageSection 321 Second Opinionsaqlain khanNo ratings yet

- 19e (12-00) Develop The Audit Program - Prepaid Expenses and Other AssetsDocument2 pages19e (12-00) Develop The Audit Program - Prepaid Expenses and Other AssetsTran AnhNo ratings yet

- Finance Roles and ResponsibilitiesDocument10 pagesFinance Roles and ResponsibilitiesmmpetcoffNo ratings yet

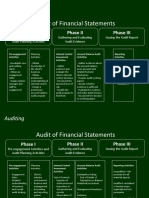

- Audit of Financial Statements: AuditingDocument3 pagesAudit of Financial Statements: AuditingAnjjjjNo ratings yet

- Substantive Procedures (1-Page Summary)Document2 pagesSubstantive Procedures (1-Page Summary)Alizeh IfthikharNo ratings yet

- General Ledger Reconciliation Process FlowchartDocument6 pagesGeneral Ledger Reconciliation Process FlowchartNarayan KulkarniNo ratings yet

- Audit EngagementsDocument1 pageAudit EngagementsBishow MaharjanNo ratings yet

- Sym14 01cDocument20 pagesSym14 01cJulio MedeirosNo ratings yet

- 1.0 Notes Cash and Cash Equivalents 1.0 Notes Cash and Cash EquivalentsDocument5 pages1.0 Notes Cash and Cash Equivalents 1.0 Notes Cash and Cash EquivalentsLawrence YusiNo ratings yet

- Forensic Investigation - ReportDocument6 pagesForensic Investigation - Reportjhon DavidNo ratings yet

- 6 MA Cheat SheetDocument1 page6 MA Cheat SheetYASH MAKADIYANo ratings yet

- Acca - JamesDocument2 pagesAcca - Jamesellisa ramliNo ratings yet

- ESTP Cours DI - Cas Pratique Mazars PDFDocument25 pagesESTP Cours DI - Cas Pratique Mazars PDFmouad soubkiNo ratings yet

- Tugas Manajemen Keuangan: Dosen Pengampu: Dedi Cristianto SE, Msi, AKA, ACPADocument238 pagesTugas Manajemen Keuangan: Dosen Pengampu: Dedi Cristianto SE, Msi, AKA, ACPAArdi CBNo ratings yet

- 19f (12-00) Develop The Audit Program - Property, Plant and EquipmentDocument2 pages19f (12-00) Develop The Audit Program - Property, Plant and EquipmentTran AnhNo ratings yet

- Audit Tutorial 2 AnswersDocument7 pagesAudit Tutorial 2 AnswersMarcus LiawNo ratings yet

- Unit 2: Effective Supplier Management and Collaboration: Week 2: From Today To TomorrowDocument5 pagesUnit 2: Effective Supplier Management and Collaboration: Week 2: From Today To TomorrowTUHIN GHOSALNo ratings yet

- Scop IatfDocument1 pageScop IatfJeevanandhamNo ratings yet

- Online Permitting ProcedureDocument17 pagesOnline Permitting ProcedureEs SyNo ratings yet

- QMS 04 A Interested Parties FreeDocument5 pagesQMS 04 A Interested Parties FreeLisardo ConstelaNo ratings yet

- LS 3.80 - PSA 550. Related PartiesDocument5 pagesLS 3.80 - PSA 550. Related PartiesSkye LeeNo ratings yet

- Auditing 1 Chapter 12 13Document49 pagesAuditing 1 Chapter 12 13Nathalie GetinoNo ratings yet

- Fabmlt 1Document3 pagesFabmlt 1lemonNo ratings yet

- Global Risk Control Matrix - GuideDocument119 pagesGlobal Risk Control Matrix - Guidemelo landry100% (1)

- Advanced Audit and Assurance: Acca AaaDocument4 pagesAdvanced Audit and Assurance: Acca AaaZainabNo ratings yet

- Advanced Audit and Assurance EthicsDocument14 pagesAdvanced Audit and Assurance EthicsAdilah AzamNo ratings yet

- Roles and Responsibilities - Office ManagerDocument10 pagesRoles and Responsibilities - Office ManagertrainershipsolutionsNo ratings yet

- SOX Deficiencies TraiingDocument49 pagesSOX Deficiencies TraiingSridhair IyengarNo ratings yet

- The Same Exp. Form But The Original One Where You Can Fully See My Duties PDFDocument1 pageThe Same Exp. Form But The Original One Where You Can Fully See My Duties PDFMuhammad AbduNo ratings yet

- DT RevDocument40 pagesDT RevHagere EthiopiaNo ratings yet

- Sa Aug09 CampbellDocument4 pagesSa Aug09 CampbellFahad ZahedNo ratings yet

- Introduction To AuditingDocument2 pagesIntroduction To Auditinglied27106No ratings yet

- Perform AML Check (Corporate)Document1 pagePerform AML Check (Corporate)Ram Mohan MishraNo ratings yet

- Class Definition:: Class Keyword (Small Case)Document9 pagesClass Definition:: Class Keyword (Small Case)Abdul WahabNo ratings yet

- Muhammad Sufyan CVDocument1 pageMuhammad Sufyan CVAbdul WahabNo ratings yet

- CS304 Part 1Document9 pagesCS304 Part 1Abdul WahabNo ratings yet

- Object Oriented Programming (Cs304) VuDocument7 pagesObject Oriented Programming (Cs304) VuAbdul WahabNo ratings yet

- CS304 Part 2Document11 pagesCS304 Part 2Abdul WahabNo ratings yet

- Muhammad Sufyan CVDocument1 pageMuhammad Sufyan CVAbdul WahabNo ratings yet

- File - PAKISTAN. INDUSTRIAL RELATIONS ORDINANCE, 1969 Part IIIDocument5 pagesFile - PAKISTAN. INDUSTRIAL RELATIONS ORDINANCE, 1969 Part IIIAbdul WahabNo ratings yet

- FontsDocument1 pageFontsAbdul WahabNo ratings yet

- File - PAKISTAN. INDUSTRIAL RELATIONS ORDINANCE, 1969 Part IIDocument5 pagesFile - PAKISTAN. INDUSTRIAL RELATIONS ORDINANCE, 1969 Part IIAbdul WahabNo ratings yet

- File - PAKISTAN. INDUSTRIAL RELATIONS ORDINANCE, 1969 Part IDocument10 pagesFile - PAKISTAN. INDUSTRIAL RELATIONS ORDINANCE, 1969 Part IAbdul WahabNo ratings yet

- Special Fonts FileDocument1 pageSpecial Fonts FileAbdul WahabNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Productive All-In-One Wide Format SolutionDocument5 pagesProductive All-In-One Wide Format SolutionAbdul WahabNo ratings yet

- InstallDocument1 pageInstallJorge B RucobaNo ratings yet

- Expense Sheet Formate: Head Office ApprovalDocument1 pageExpense Sheet Formate: Head Office ApprovalAbdul WahabNo ratings yet

- Xerox XD100 102 104 Service ManualDocument308 pagesXerox XD100 102 104 Service ManualatalincNo ratings yet

- CS302 Short NotesDocument13 pagesCS302 Short NotesAbdul WahabNo ratings yet

- Solved FIA Inspector PapersssDocument9 pagesSolved FIA Inspector PapersssAbdul WahabNo ratings yet

- Midterm Solution cs302Document9 pagesMidterm Solution cs302Abdul WahabNo ratings yet

- FIA Sub Inspector Past Papers For PreparatonDocument10 pagesFIA Sub Inspector Past Papers For PreparatonAbdul WahabNo ratings yet

- FIA Sub Inspector Past Papers For PreparatonDocument10 pagesFIA Sub Inspector Past Papers For PreparatonAbdul WahabNo ratings yet

- Generate Certificate 1624278625593Document1 pageGenerate Certificate 1624278625593Abdul WahabNo ratings yet

- Cs302 Lec10Document30 pagesCs302 Lec10Abdul WahabNo ratings yet

- Magicolor 1690mfDocument90 pagesMagicolor 1690mfAbdul WahabNo ratings yet

- Spring 2021 - CS302 - 2Document2 pagesSpring 2021 - CS302 - 2Abdul Wahab100% (1)

- Spring 2021 - CS302 - 2Document2 pagesSpring 2021 - CS302 - 2Abdul Wahab100% (1)

- ReadmeDocument2 pagesReadmeAbdul WahabNo ratings yet

- CS101 Assignment 2 Spring 2021 SolutionDocument4 pagesCS101 Assignment 2 Spring 2021 SolutionAbdul WahabNo ratings yet

- Bizhub Pro 920Document640 pagesBizhub Pro 920Abdul WahabNo ratings yet

- Module 4 1st Quarter EntrepreneurshipDocument14 pagesModule 4 1st Quarter EntrepreneurshipnattoykoNo ratings yet

- DPS Quarterly Exam Grade 9Document3 pagesDPS Quarterly Exam Grade 9Michael EstrellaNo ratings yet

- Supermarkets - UK - November 2015 - Executive SummaryDocument8 pagesSupermarkets - UK - November 2015 - Executive Summarymaxime78540No ratings yet

- Psychology Essay IntroductionDocument3 pagesPsychology Essay Introductionfesegizipej2100% (2)

- Philippine Phoenix Surety vs. WoodworksDocument1 pagePhilippine Phoenix Surety vs. WoodworksSimon James SemillaNo ratings yet

- Hilti 2016 Company-Report ENDocument72 pagesHilti 2016 Company-Report ENAde KurniawanNo ratings yet

- Đề Cương CK - QuestionsDocument2 pagesĐề Cương CK - QuestionsDiệu Phương LêNo ratings yet

- Mboce - Enforcement of International Arbitral Awards - Public Policy Limitation in KenyaDocument100 pagesMboce - Enforcement of International Arbitral Awards - Public Policy Limitation in KenyaIbrahim Abdi AdanNo ratings yet

- Memorandum1 PDFDocument65 pagesMemorandum1 PDFGilbert Gabrillo JoyosaNo ratings yet

- DAP-1160 A1 Manual 1.20Document71 pagesDAP-1160 A1 Manual 1.20Cecilia FerronNo ratings yet

- Tok SB Ibdip Ch1Document16 pagesTok SB Ibdip Ch1Luis Andrés Arce SalazarNo ratings yet

- Certified Data Centre Professional CDCPDocument1 pageCertified Data Centre Professional CDCPxxxxxxxxxxxxxxxxxxxxNo ratings yet

- Special Power of Attorney: Know All Men by These PresentsDocument1 pageSpecial Power of Attorney: Know All Men by These PresentsTonie NietoNo ratings yet

- Vodafone Training Induction PPT UpdatedDocument39 pagesVodafone Training Induction PPT Updatedeyad mohamadNo ratings yet

- Test Bank: Corporate RestructuringDocument3 pagesTest Bank: Corporate RestructuringYoukayzeeNo ratings yet

- Evergreen Park Arrests 07-22 To 07-31-2016Document5 pagesEvergreen Park Arrests 07-22 To 07-31-2016Lorraine SwansonNo ratings yet

- Keys For Change - Myles Munroe PDFDocument46 pagesKeys For Change - Myles Munroe PDFAndressi Label100% (2)

- UntitledDocument18 pagesUntitledjake ruthNo ratings yet

- Roads of Enlightenment GuideDocument5 pagesRoads of Enlightenment GuideMicNo ratings yet

- Civics: Our Local GovernmentDocument24 pagesCivics: Our Local GovernmentMahesh GavasaneNo ratings yet

- Public Service Application For ForgivenessDocument9 pagesPublic Service Application For ForgivenessLateshia SpencerNo ratings yet

- Financial Management: Usaid Bin Arshad BBA 182023Document10 pagesFinancial Management: Usaid Bin Arshad BBA 182023Usaid SiddiqueNo ratings yet

- Republic of The Philippines vs. Bagtas, 6 SCRA 262, 25 October 1962Document2 pagesRepublic of The Philippines vs. Bagtas, 6 SCRA 262, 25 October 1962DAblue ReyNo ratings yet

- Adobe Scan 04 Feb 2024Document1 pageAdobe Scan 04 Feb 2024biswajitrout13112003No ratings yet

- Case 1. Is Morality Relative? The Variability of Moral CodesDocument2 pagesCase 1. Is Morality Relative? The Variability of Moral CodesalyssaNo ratings yet

- A Melody of Life: Espiritu Santo Parochial School of Manila, Inc. 1913 Rizal Avenue, Sta. Cruz, ManilaDocument4 pagesA Melody of Life: Espiritu Santo Parochial School of Manila, Inc. 1913 Rizal Avenue, Sta. Cruz, ManilaIrene Carmela Empress ParkNo ratings yet

- AssignmentDocument25 pagesAssignmentPrashan Shaalin FernandoNo ratings yet

- NRes1 Work Activity 1 - LEGARTEDocument4 pagesNRes1 Work Activity 1 - LEGARTEJuliana LegarteNo ratings yet

- People vs. Tampus DigestDocument2 pagesPeople vs. Tampus Digestcmv mendozaNo ratings yet

- Sbi Rural PubDocument6 pagesSbi Rural PubAafrinNo ratings yet