You might also like

- Customer Value, Satisfaction & LoyaltyDocument27 pagesCustomer Value, Satisfaction & LoyaltyJalaj Mathur88% (8)

- Balance of Payment ParkinDocument37 pagesBalance of Payment ParkinHaroonNo ratings yet

- Essential Guide To Digital Signage Trends 2018 and BeyondDocument15 pagesEssential Guide To Digital Signage Trends 2018 and BeyondAntonio MUÑOZNo ratings yet

- CCS (Cca)Document42 pagesCCS (Cca)ANILKUMAR EMANI100% (1)

- In Re Tribune Company Fraudulent Conveyance LitigationDocument326 pagesIn Re Tribune Company Fraudulent Conveyance LitigationEmma Smith100% (1)

- 208 S. Akard Street SUİTE 2954 Dallas Texas TX 75202 0800-288-2020Document1 page208 S. Akard Street SUİTE 2954 Dallas Texas TX 75202 0800-288-2020elise starkNo ratings yet

- Andrews Pitchfork - 4 Top Trading Strategies For Today's MarketsDocument11 pagesAndrews Pitchfork - 4 Top Trading Strategies For Today's MarketsHaichu100% (1)

- Roland Berger Automotive ResearchDocument20 pagesRoland Berger Automotive ResearchHiifjxjNo ratings yet

- Indian IT Services - Sector Report 6mar09Document73 pagesIndian IT Services - Sector Report 6mar09BALAJI RAVISHANKARNo ratings yet

- A Report On Indian Infrastructure SectorDocument16 pagesA Report On Indian Infrastructure SectorhsinghaNo ratings yet

- Salonga Chap 3-8Document14 pagesSalonga Chap 3-8unicamor2No ratings yet

- Asian Paints: Volume Led Growth ContinuesDocument9 pagesAsian Paints: Volume Led Growth ContinuesanjugaduNo ratings yet

- IDirect MarutiSuzuki Q2FY19Document12 pagesIDirect MarutiSuzuki Q2FY19Rajani KantNo ratings yet

- Wto 2.2Document6 pagesWto 2.2Carol DanversNo ratings yet

- Maruti Suzuki India: Muted Quarter Volume Trough Seemingly in SightDocument12 pagesMaruti Suzuki India: Muted Quarter Volume Trough Seemingly in SightDushyant ChaturvediNo ratings yet

- Metrics ROA (%) ROE (%) ST Debt/Assets (%) LT Debt/Assets (%) Current Ratio (X) Firm Size Sales Growth (%) Tangibility (%)Document2 pagesMetrics ROA (%) ROE (%) ST Debt/Assets (%) LT Debt/Assets (%) Current Ratio (X) Firm Size Sales Growth (%) Tangibility (%)Dương Khánh VyNo ratings yet

- Maruti Suzuki India: Volume Decline in Offing, Expensive ValuationsDocument13 pagesMaruti Suzuki India: Volume Decline in Offing, Expensive ValuationsPulkit TalujaNo ratings yet

- Gulf Oil Lubricants: Stable Performance..Document8 pagesGulf Oil Lubricants: Stable Performance..Doshi VaibhavNo ratings yet

- Investor Digest: HighlightDocument13 pagesInvestor Digest: HighlightYua GeorgeusNo ratings yet

- Morning India 20210323 Mosl Motilal OswalDocument8 pagesMorning India 20210323 Mosl Motilal Oswalvikalp123123No ratings yet

- IDirect SKFIndia Q2FY20Document10 pagesIDirect SKFIndia Q2FY20praveensingh77No ratings yet

- JK Cement: Valuations Factor in Positive Downgrade To HOLDDocument9 pagesJK Cement: Valuations Factor in Positive Downgrade To HOLDShubham BawkarNo ratings yet

- Management Discussion and AnalysisDocument30 pagesManagement Discussion and Analysispanditak521No ratings yet

- Banco Products (India) LTD: Retail ResearchDocument15 pagesBanco Products (India) LTD: Retail Researcharun_algoNo ratings yet

- Eco Wrap SBIDocument3 pagesEco Wrap SBIVaibhav BhardwajNo ratings yet

- Escorts: CMP: INR1,107 TP: INR 1,175 (+6%) Strong Operating Performance Led by Cost ManagementDocument12 pagesEscorts: CMP: INR1,107 TP: INR 1,175 (+6%) Strong Operating Performance Led by Cost ManagementdfhjhdhdgfjhgdfjhNo ratings yet

- IDirect EicherMotors Q2FY20Document10 pagesIDirect EicherMotors Q2FY20Dushyant ChaturvediNo ratings yet

- State of Pakistan EconomyDocument8 pagesState of Pakistan EconomyMuhammad KashifNo ratings yet

- Echap09 Vol2Document21 pagesEchap09 Vol2Abhinav VohraNo ratings yet

- Eicher Motors - Company Update 03-04-18 - SBICAP SecDocument6 pagesEicher Motors - Company Update 03-04-18 - SBICAP SecdarshanmadeNo ratings yet

- Maldives: Economic Update 2019Document33 pagesMaldives: Economic Update 2019MoinNo ratings yet

- Pidilite Industries (PIDIND) : High Raw Material Prices Hit MarginDocument10 pagesPidilite Industries (PIDIND) : High Raw Material Prices Hit MarginSiddhant SinghNo ratings yet

- CHP Col ResearchDocument10 pagesCHP Col ResearchJun GomezNo ratings yet

- Lombard Fy19Document21 pagesLombard Fy19Sriram RajaramNo ratings yet

- The Race To Win How Automakers Can Succeed in A Post Pandemic China VFDocument36 pagesThe Race To Win How Automakers Can Succeed in A Post Pandemic China VFJonathan WenNo ratings yet

- Services Sector Performance in India: An OverviewDocument23 pagesServices Sector Performance in India: An OverviewDevendraNo ratings yet

- IDirect Polycab CoUpdate Jun20 PDFDocument10 pagesIDirect Polycab CoUpdate Jun20 PDFkishore13No ratings yet

- 2022-Q4 Vehicle Pricing Index-TransUnionDocument9 pages2022-Q4 Vehicle Pricing Index-TransUnionsygmacorpNo ratings yet

- Coal India: CMP: INR234 Sputtering Production Growth Impacting VolumesDocument10 pagesCoal India: CMP: INR234 Sputtering Production Growth Impacting Volumessaran21No ratings yet

- NESG Manufacturing Policy Brief May 2021Document11 pagesNESG Manufacturing Policy Brief May 2021uchenna joel iconNo ratings yet

- Final Report Mahindra & MahindraDocument11 pagesFinal Report Mahindra & MahindraDurgesh TamhaneNo ratings yet

- DFG Analysis - 2021-22 - Science&TechnologyDocument9 pagesDFG Analysis - 2021-22 - Science&TechnologybteuNo ratings yet

- Q2Fy21 GDP: Investments Fared Better Than Consumption FY21E GDP Retained at - 5% To - 7%Document5 pagesQ2Fy21 GDP: Investments Fared Better Than Consumption FY21E GDP Retained at - 5% To - 7%Raghvendra N DhootNo ratings yet

- MOSL Subros 201809 Initiating CoverageDocument18 pagesMOSL Subros 201809 Initiating Coveragerchawdhry123No ratings yet

- Investor Digest 17 Januari 2020 PDFDocument11 pagesInvestor Digest 17 Januari 2020 PDFRyanNo ratings yet

- Stock Report On Baja Auto in India Ma 23 2020Document12 pagesStock Report On Baja Auto in India Ma 23 2020PranavPillaiNo ratings yet

- Wipro LTD (WIPRO) : Growth and Margin Visibility Improving..Document13 pagesWipro LTD (WIPRO) : Growth and Margin Visibility Improving..ashok yadavNo ratings yet

- United Breweries: CMP: INR1,048 TP: INR700 (-33%) Worsening Outlook, Expensive Valuations Maintain SellDocument10 pagesUnited Breweries: CMP: INR1,048 TP: INR700 (-33%) Worsening Outlook, Expensive Valuations Maintain Selldnwekfnkfnknf skkjdbNo ratings yet

- Review of JLR's 2020 and 2021 Business ResultsDocument7 pagesReview of JLR's 2020 and 2021 Business Resultsvalentin.borisavljevicNo ratings yet

- Macroeconomic Report May 2020 Economic DivisionDocument22 pagesMacroeconomic Report May 2020 Economic DivisionTim SheldonNo ratings yet

- Global Automotive Sector - Euler ReportDocument14 pagesGlobal Automotive Sector - Euler ReportAkshay SatijaNo ratings yet

- Tvs Motors LTD: Company OverviewDocument3 pagesTvs Motors LTD: Company OverviewJOEL JOHNSONNo ratings yet

- Project On Saudi Stock ExchangeDocument9 pagesProject On Saudi Stock ExchangeNishat FarhatNo ratings yet

- Ecowrap - 20190830 - Q1fy20 GDP at 25 Quarters LowDocument2 pagesEcowrap - 20190830 - Q1fy20 GDP at 25 Quarters LowSanjoySahaNo ratings yet

- Cummins India (KKC IN) : Analyst Meet UpdateDocument5 pagesCummins India (KKC IN) : Analyst Meet UpdateADNo ratings yet

- Total Factor Productivity For Major Industries - 2022Document15 pagesTotal Factor Productivity For Major Industries - 2022Novica SupicNo ratings yet

- Automotive - Summer 2020: Industry InsightsDocument22 pagesAutomotive - Summer 2020: Industry InsightsshountyNo ratings yet

- Trimegah CF 20231124 ASII - A Mid-2024 PlayDocument12 pagesTrimegah CF 20231124 ASII - A Mid-2024 PlayMuhammad ErnandaNo ratings yet

- Kendrion, 2019 Q2Document18 pagesKendrion, 2019 Q2Jasper Laarmans Teixeira de MattosNo ratings yet

- MOSL Ashok Leyland Comprehensive ReportDocument34 pagesMOSL Ashok Leyland Comprehensive Reportrchawdhry123No ratings yet

- Quang Ninh Research Report 2020Document26 pagesQuang Ninh Research Report 2020Architecte UrbanisteNo ratings yet

- Industry and InfrastructureDocument48 pagesIndustry and Infrastructuresudip dhuriNo ratings yet

- TTK Prestige 16082019 PDFDocument7 pagesTTK Prestige 16082019 PDFSujith VichuNo ratings yet

- Wipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityDocument14 pagesWipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityPramod KulkarniNo ratings yet

- Cement February 2019Document9 pagesCement February 2019Mohammed Aaquib MubeenNo ratings yet

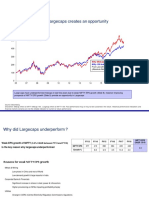

- Equity Markets Review Underperformance of Largecaps Creates An OpportunityDocument8 pagesEquity Markets Review Underperformance of Largecaps Creates An OpportunitysumeetNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- Worshipping God Again: (Keys To Refocusing The Object and Subject of OurDocument28 pagesWorshipping God Again: (Keys To Refocusing The Object and Subject of OurMica Gay TagtagonNo ratings yet

- An Overview of Organic ReactionsDocument80 pagesAn Overview of Organic Reactions110003551 110ANo ratings yet

- Dramaturgy, Ethnomethodology, PhenomenologygyDocument8 pagesDramaturgy, Ethnomethodology, PhenomenologygyLoeyNo ratings yet

- Effect of Corona On Common ManDocument2 pagesEffect of Corona On Common ManMUSKAN DUBEYNo ratings yet

- Social Studies EssayDocument5 pagesSocial Studies Essayapi-315960690No ratings yet

- A Glossary of Kumarajiva's Translation of The Lotus SutraDocument580 pagesA Glossary of Kumarajiva's Translation of The Lotus SutraSammacittaNo ratings yet

- Controles Iso 27001-2013Document9 pagesControles Iso 27001-2013Juan Carlos Torres AlvarezNo ratings yet

- B.C. Liquor Control and Licensing Branch Documents About The 2011 Stanley Cup RiotDocument98 pagesB.C. Liquor Control and Licensing Branch Documents About The 2011 Stanley Cup RiotBob MackinNo ratings yet

- Succession Main Theme - C Minor - notesDocument9 pagesSuccession Main Theme - C Minor - notessakkuturdeNo ratings yet

- Week 5Document2 pagesWeek 5Kym QuirogaNo ratings yet

- United KingdomDocument5 pagesUnited KingdommuskanNo ratings yet

- Act 163 Extra Territorial Offences Act 1976Document8 pagesAct 163 Extra Territorial Offences Act 1976Adam Haida & CoNo ratings yet

- Quad Plus and Indo-Pacific - The ChangingDocument313 pagesQuad Plus and Indo-Pacific - The ChangingAngelica StaszewskaNo ratings yet

- Theopoetics Is The RageDocument9 pagesTheopoetics Is The Rageblackpetal1No ratings yet

- Chapter 12Document25 pagesChapter 12varunjajooNo ratings yet

- SBI Current Account Form For Other Than Sole Proprietorship FirmDocument16 pagesSBI Current Account Form For Other Than Sole Proprietorship FirmKartik KumarNo ratings yet

- The RegisterDocument22 pagesThe RegisterMadalina ScipanovNo ratings yet

- Tattler May 2015 Mayor's Dick Pic SelfieDocument2 pagesTattler May 2015 Mayor's Dick Pic SelfieEric J BrewerNo ratings yet

- Alphabets, Letters and Diacritics in European Languages: AlbanianDocument8 pagesAlphabets, Letters and Diacritics in European Languages: AlbanianNilmalvila Blue Lilies PondNo ratings yet

- Cha v. CA 277 SCRA 690Document4 pagesCha v. CA 277 SCRA 690Justine UyNo ratings yet

- Foundations of Entrepreneurship: Module - 1Document29 pagesFoundations of Entrepreneurship: Module - 1Prathima GirishNo ratings yet

- Offer Letter - Executive M.Tech2022Document2 pagesOffer Letter - Executive M.Tech2022Aditya NehraNo ratings yet

- Kajiado West Technical: AND Vocational CollegeDocument11 pagesKajiado West Technical: AND Vocational CollegeSimon MungaiNo ratings yet