You might also like

- Statistical Yearbook 2022 2023Document79 pagesStatistical Yearbook 2022 2023Abcd123411100% (2)

- Join Us at Casino FataleDocument7 pagesJoin Us at Casino FataleAbcd123411No ratings yet

- 20 Different Recipes of Starch and Cereal DishesDocument44 pages20 Different Recipes of Starch and Cereal DishesLila Kyst93% (86)

- Original Doc of OSDocument57 pagesOriginal Doc of OSTom Joseph50% (2)

- Equity Research Report - Sun Pharma 2023Document8 pagesEquity Research Report - Sun Pharma 2023Dikshant Dahivaley100% (1)

- Synthite Company & Product ProfileDocument19 pagesSynthite Company & Product ProfileArun Sunny MNo ratings yet

- India Food & Drink Report - Q3 2020 PDFDocument87 pagesIndia Food & Drink Report - Q3 2020 PDFaashmeen25No ratings yet

- Case Study: Rooah Afza Presented By: Bushra SeharDocument27 pagesCase Study: Rooah Afza Presented By: Bushra SeharShamsher KhanNo ratings yet

- Ayurveda Industry Market Size, Strength and Way ForwardDocument52 pagesAyurveda Industry Market Size, Strength and Way ForwardManish Govil100% (1)

- Keto Breakfast and Lunch Meal Plans Under 1200 CaloriesDocument7 pagesKeto Breakfast and Lunch Meal Plans Under 1200 CaloriesRora11No ratings yet

- E-Contract Labour Management System (e-CLMS) : User ManualDocument20 pagesE-Contract Labour Management System (e-CLMS) : User Manualsrinivasyadav4No ratings yet

- Opportunities in Food Processing Sector in IndiaDocument24 pagesOpportunities in Food Processing Sector in IndiaPrakash KcNo ratings yet

- Centre For Entrepreneurship Development Madhya Pradesh (CEDMAP)Document31 pagesCentre For Entrepreneurship Development Madhya Pradesh (CEDMAP)Pramod ShrivastavaNo ratings yet

- Chai-Biskut Presentation ReportDocument54 pagesChai-Biskut Presentation ReportRajdeep Singh ChauhanNo ratings yet

- Spices Cryo-Grinding UnitDocument7 pagesSpices Cryo-Grinding Unitbenrakesh75No ratings yet

- Indian Mortgage Finance Market PDFDocument61 pagesIndian Mortgage Finance Market PDFmikecoreleonNo ratings yet

- Marketing Plan Strategy-Bombay Pav BhajiDocument7 pagesMarketing Plan Strategy-Bombay Pav BhajiAditi Mishra100% (1)

- NRI Investments in IndiaDocument3 pagesNRI Investments in IndiaRahul BediNo ratings yet

- Production and Export Performance Indian SpicesDocument13 pagesProduction and Export Performance Indian SpicesarcherselevatorsNo ratings yet

- Food Truck Financial Model Excel Template v1.8Document77 pagesFood Truck Financial Model Excel Template v1.8hanswuytsNo ratings yet

- Summer Internship Final ReportDocument57 pagesSummer Internship Final ReportRiya BhogadeNo ratings yet

- Index: S.No Date NO RemarksDocument23 pagesIndex: S.No Date NO RemarksSathya Kamaraj0% (1)

- Report On Dry FruitsDocument20 pagesReport On Dry Fruitsyahoo1088100% (1)

- India's declining global tea trade share and competitivenessDocument173 pagesIndia's declining global tea trade share and competitivenessPrakash KcNo ratings yet

- Financial Projection Model for Your Business Name HereDocument70 pagesFinancial Projection Model for Your Business Name HerenabayeelNo ratings yet

- Introduction of PatanjaliDocument14 pagesIntroduction of PatanjaliMukesh KumarNo ratings yet

- Food Survey of IndiaDocument258 pagesFood Survey of Indiameenx100% (1)

- DGM14 - D42010019 - Hitesh ParasharDocument10 pagesDGM14 - D42010019 - Hitesh ParasharHitesh ParasharNo ratings yet

- Religare's Financial Services OverviewDocument70 pagesReligare's Financial Services OverviewAmarbant Singh DNo ratings yet

- Food Processing Sector in IndiaDocument18 pagesFood Processing Sector in IndiaSuresh Kumar VengaliNo ratings yet

- Dabur India LTD Financial Analysis ProjectDocument10 pagesDabur India LTD Financial Analysis ProjectYaseenNo ratings yet

- Relative Growth & Opportunity of FPOs in GujaratDocument102 pagesRelative Growth & Opportunity of FPOs in GujaratSayan100% (2)

- LIQUIDITY AND SOLVENCY RATIOSDocument26 pagesLIQUIDITY AND SOLVENCY RATIOSDeep KrishnaNo ratings yet

- Cerulli Report - Targeting The Affluent and The Emerging AffluentDocument25 pagesCerulli Report - Targeting The Affluent and The Emerging AffluentJoin RiotNo ratings yet

- All Bank Name and Their Full Form ListDocument5 pagesAll Bank Name and Their Full Form ListD BtyNo ratings yet

- Start a Namkeen FactoryDocument69 pagesStart a Namkeen FactoryVishal Govind ChakrawarNo ratings yet

- 4.database CosmeticsDocument21 pages4.database CosmeticsYash 906100% (1)

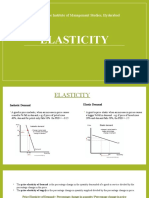

- Elasticity: Narsee Monjee Institute of Management Studies, HyderabadDocument5 pagesElasticity: Narsee Monjee Institute of Management Studies, HyderabadAishwaryaNo ratings yet

- Modern Foods-Case StudyDocument6 pagesModern Foods-Case StudyAnurag BharatNo ratings yet

- Agri Clinics & Agribusiness Centers ReportDocument36 pagesAgri Clinics & Agribusiness Centers Reportveenaa somashekar0% (1)

- Aachi MasalaDocument8 pagesAachi MasalaPrabu EswaranNo ratings yet

- Market Report BriteDocument46 pagesMarket Report Britesyedtahashah0% (2)

- CMA FormatDocument21 pagesCMA Formatapi-377123878% (9)

- Terms & ConditionsDocument1 pageTerms & ConditionsAlhjee YousifNo ratings yet

- Long Term Sources of Finance for WayCool FoodsDocument6 pagesLong Term Sources of Finance for WayCool FoodsHarshita Sharma0% (1)

- Anand RathiDocument3 pagesAnand RathiShilpa EdarNo ratings yet

- By K.Anbazhagan M0208004 Magnus School of Business Bangalore Faculty Guide Prof. Brindha VenkateshDocument15 pagesBy K.Anbazhagan M0208004 Magnus School of Business Bangalore Faculty Guide Prof. Brindha VenkateshanbubalrajNo ratings yet

- Maharashtra Wine IndustryDocument13 pagesMaharashtra Wine IndustrymeerasagarNo ratings yet

- Gujarat State Fertilizer & Chemicals LimitedDocument33 pagesGujarat State Fertilizer & Chemicals LimitedPRATIKNo ratings yet

- Pay1 - Proposal For Merchant LendingDocument6 pagesPay1 - Proposal For Merchant LendingAdhe IdhiNo ratings yet

- Restaurant Startup Costs - 2022117215548Document5 pagesRestaurant Startup Costs - 2022117215548Naison StanleyNo ratings yet

- What Is Equity Market? - Meaning, Benefits & TypesDocument27 pagesWhat Is Equity Market? - Meaning, Benefits & TypeskoppulaNo ratings yet

- Green Tea Survey Questions and AnswersDocument2 pagesGreen Tea Survey Questions and AnswersSidrah Parwaiz Qureshi100% (2)

- Schemes For MsmeDocument68 pagesSchemes For MsmeGanesh N100% (1)

- Real-Estate Sector TrendDocument67 pagesReal-Estate Sector TrendAnjaiah PittalaNo ratings yet

- Kolkata Data - MerchantsDocument6 pagesKolkata Data - MerchantskamleshNo ratings yet

- Apollo Hospital Case 2 Study 020522Document9 pagesApollo Hospital Case 2 Study 020522Vagabond DonNo ratings yet

- Funding Your Startup (May 9 by Naz)Document32 pagesFunding Your Startup (May 9 by Naz)Ryansyah Ramadhan AdjuNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- AvendusDocument27 pagesAvendusSrishti KukrejaNo ratings yet

- ABinbev KArthikDocument4 pagesABinbev KArthikKarthik MNo ratings yet

- Group 12 MM2Document12 pagesGroup 12 MM2SURAJ KUMAR-DM 21DM203No ratings yet

- Tata Consumer Products' Genesis and Journey So FarDocument39 pagesTata Consumer Products' Genesis and Journey So FarKartik SharmaNo ratings yet

- Marico: PRICE: 530.95Document7 pagesMarico: PRICE: 530.95Shresth GuptaNo ratings yet

- PROJECT COCO FreshDocument10 pagesPROJECT COCO FreshSyed ArslanNo ratings yet

- 2020 - Interactive Ecommerce-1 PDFDocument53 pages2020 - Interactive Ecommerce-1 PDFTee Shi FengNo ratings yet

- Bain Report Unlocking The Future of Commerce in IndiaDocument37 pagesBain Report Unlocking The Future of Commerce in IndiadanishNo ratings yet

- PhonePe PulseDocument49 pagesPhonePe PulseAbcd123411No ratings yet

- Deloitte NL Fsi Fintech Report 1Document30 pagesDeloitte NL Fsi Fintech Report 1ANIRBAN BISWASNo ratings yet

- Logistics Sector Update: Delhivery - Investor InteractionDocument11 pagesLogistics Sector Update: Delhivery - Investor InteractionSaurav KumarNo ratings yet

- Investment Associate Job at Lightrock IndiaDocument1 pageInvestment Associate Job at Lightrock IndiaAbcd123411No ratings yet

- Klub RBF roleDocument2 pagesKlub RBF roleAbcd123411No ratings yet

- IVP SaaSHandbookPDF 6 2021Document25 pagesIVP SaaSHandbookPDF 6 2021Abcd123411No ratings yet

- State OF Mobile 2 0 2 1: App AnnieDocument55 pagesState OF Mobile 2 0 2 1: App AnnieAbcd123411No ratings yet

- DoorDash 2014-03-31 Series A Memo Redacted FINALDocument4 pagesDoorDash 2014-03-31 Series A Memo Redacted FINALAbcd123411No ratings yet

- Snapchat Seed Memo: Business Description & TeamDocument1 pageSnapchat Seed Memo: Business Description & TeamAbcd123411No ratings yet

- India Fintech Report 2021Document29 pagesIndia Fintech Report 2021Abcd123411No ratings yet

- 2020 SaaS Benchmarks Deck VFINALDocument53 pages2020 SaaS Benchmarks Deck VFINALAbcd123411No ratings yet

- Ey 3q20 Mobility Quarterly FinalDocument4 pagesEy 3q20 Mobility Quarterly FinalAbcd123411No ratings yet

- Global Wealth Report 2020 en PDFDocument56 pagesGlobal Wealth Report 2020 en PDFHoa DangNo ratings yet

- Blume Investment Report 16 Q3 2015 Edited Version PDFDocument3 pagesBlume Investment Report 16 Q3 2015 Edited Version PDFAbcd123411No ratings yet

- Vol 1 - State of Indian Tech in 2020 - What Is Reliance Jio's Plan? (1.0)Document39 pagesVol 1 - State of Indian Tech in 2020 - What Is Reliance Jio's Plan? (1.0)Abcd123411No ratings yet

- Murder Mystery Games Online - Video Chat & Game MechanicsDocument1 pageMurder Mystery Games Online - Video Chat & Game MechanicsAbcd123411No ratings yet

- CF 02 InvitationDocument4 pagesCF 02 InvitationAbcd123411No ratings yet

- Blume Investment Report 16 Q3 2015 PDFDocument3 pagesBlume Investment Report 16 Q3 2015 PDFAbcd123411No ratings yet

- Playing A Murder Mystery Game: © 2019 Freeform Games LLPDocument1 pagePlaying A Murder Mystery Game: © 2019 Freeform Games LLPAbcd123411No ratings yet

- Digital Identification A Key To Inclusive Growth PDFDocument32 pagesDigital Identification A Key To Inclusive Growth PDFDiego Angel GomezNo ratings yet

- Paris News: Let The Good Times Roll!Document2 pagesParis News: Let The Good Times Roll!Abcd123411No ratings yet

- Bessemer Whitepaper Data Privacy EngineeringDocument10 pagesBessemer Whitepaper Data Privacy EngineeringRobialmay NaufalmahdyNo ratings yet

- Turner Novak - The Past, Present, And: Future of Consumer Social CompaniesDocument25 pagesTurner Novak - The Past, Present, And: Future of Consumer Social CompaniesAbcd123411No ratings yet

- The Past, Present and Future of SaaS According to Benchmark's Eric VishriaDocument23 pagesThe Past, Present and Future of SaaS According to Benchmark's Eric VishriaAbcd123411No ratings yet

- Vegan Recipe BookDocument71 pagesVegan Recipe Bookzambilina100% (1)

- Fbs Chapter5 Menu ManagementDocument19 pagesFbs Chapter5 Menu ManagementKenneth SantosNo ratings yet

- (S1-5 Ming Hong) Hawker CultureDocument1 page(S1-5 Ming Hong) Hawker CultureTan Ming Hong (Spectrasec)No ratings yet

- New York City Restaurant Openings and News - The New York TimesDocument2 pagesNew York City Restaurant Openings and News - The New York TimesCesar Augusto CarmenNo ratings yet

- Rooftop Breakfast SOP GuideDocument45 pagesRooftop Breakfast SOP GuideBhisma AirlanggaNo ratings yet

- DLP JOY ANNEDocument17 pagesDLP JOY ANNEFernandez Joy Anne T.No ratings yet

- Classic French Baguette Recipe - Bless This MessDocument2 pagesClassic French Baguette Recipe - Bless This MessJk YepNo ratings yet

- Food Storage For Safety and Quality: Quick FactsDocument5 pagesFood Storage For Safety and Quality: Quick FactsJin Laude FernandezNo ratings yet

- Major Pests and Diseases of Shallots and Control Measures in Brebes, Central JavaDocument6 pagesMajor Pests and Diseases of Shallots and Control Measures in Brebes, Central JavaMuhammad UmarNo ratings yet

- Unit Produce/Ingredient S Cost Price Per UNIT Quantit Y (Gros)Document67 pagesUnit Produce/Ingredient S Cost Price Per UNIT Quantit Y (Gros)Issaraporn PunyawongNo ratings yet

- 4 EclairsDocument2 pages4 EclairsSridhar ManickamNo ratings yet

- Cookery 10 - Quarter 1 Module 2 WEEK 2Document18 pagesCookery 10 - Quarter 1 Module 2 WEEK 2Serenity VertesNo ratings yet

- Sweet Potato Corner Introduces New Fries VarietyDocument4 pagesSweet Potato Corner Introduces New Fries VarietyIrasna AbmiugNo ratings yet

- Restaurant Role PlayDocument16 pagesRestaurant Role PlayMauricio GuzmanNo ratings yet

- Want To Live A Longer Life Try Eating Like A CentenarianDocument2 pagesWant To Live A Longer Life Try Eating Like A CentenarianAurel AchilNo ratings yet

- Sandra QuinteroDocument6 pagesSandra Quinteroresidenteutpinternativos internativosNo ratings yet

- Zayka Ka Tadka - April 2022 - MagazineDocument58 pagesZayka Ka Tadka - April 2022 - Magazinepreeti chourishi100% (1)

- 3 - Fine Cooking 033Document84 pages3 - Fine Cooking 033darkNo ratings yet

- Spiral Dessert Recipe - How to Make Burma TatlisiDocument5 pagesSpiral Dessert Recipe - How to Make Burma Tatlisilarime60No ratings yet

- Chocolate Lava CakesDocument1 pageChocolate Lava CakesAntony Rosero FloresNo ratings yet

- Britain Food and DrinksDocument15 pagesBritain Food and DrinksAnny NamelessNo ratings yet

- Petes Patisserie BrochureDocument18 pagesPetes Patisserie BrochureFabio Santos75% (4)

- Brownies .For This Essay I Chose To Write About How To Make Brownies. I Chose To Write About BrowniesDocument3 pagesBrownies .For This Essay I Chose To Write About How To Make Brownies. I Chose To Write About BrowniesJerchel Chloe Trinidad BaynasNo ratings yet

- Scheme of Work - Culinary Basic Techniques 1 and 2Document68 pagesScheme of Work - Culinary Basic Techniques 1 and 2Jimmy NyangeNo ratings yet

- Coffee & Chocolate Blend ReviewDocument2 pagesCoffee & Chocolate Blend ReviewRobbie ChanNo ratings yet

- PARAISO DE SIARGAO Resort Boasts A Private Beach Area ThatDocument5 pagesPARAISO DE SIARGAO Resort Boasts A Private Beach Area ThatSanie Grace Lipao BermudezNo ratings yet

- Fresh Pako Salad Recipe from Filipino WebsiteDocument10 pagesFresh Pako Salad Recipe from Filipino WebsiteROWENA PALACIONo ratings yet

- SITHCCC012 Student Assessment Tasks 3Document29 pagesSITHCCC012 Student Assessment Tasks 3Priyanka DeviNo ratings yet