You might also like

- Reviewer Compilation (b5 Notebook)Document3 pagesReviewer Compilation (b5 Notebook)Jessica AlbaracinNo ratings yet

- Budgeting BasicsDocument4 pagesBudgeting BasicsFranz CampuedNo ratings yet

- 4.1 Budgeting For Planning and ControlDocument1 page4.1 Budgeting For Planning and ControlLea GerodiazNo ratings yet

- Controlling: Organization and ManagementDocument3 pagesControlling: Organization and ManagementSoleil CodmNo ratings yet

- Introduction To BudgetDocument15 pagesIntroduction To BudgetTushar PrasadNo ratings yet

- Chapter 12 Budgeting GuideDocument59 pagesChapter 12 Budgeting GuideCristineNo ratings yet

- Chapter 4 - Standard CostDocument8 pagesChapter 4 - Standard CostindahmuliasariNo ratings yet

- Week 5Document35 pagesWeek 5flora tasiNo ratings yet

- Accounting Chapter 8-Master Budgeting Flashcards - QuizletDocument7 pagesAccounting Chapter 8-Master Budgeting Flashcards - QuizletBisag AsaNo ratings yet

- Group 3 Topic 1: Significance FunctionDocument14 pagesGroup 3 Topic 1: Significance FunctionjsemlpzNo ratings yet

- GNB - 09 - 12e Profit PlanningDocument89 pagesGNB - 09 - 12e Profit PlanningAhmed Mostafa ElmowafyNo ratings yet

- Profit Planning: Mcgraw-Hill /irwinDocument89 pagesProfit Planning: Mcgraw-Hill /irwinXu FengNo ratings yet

- Group 11: Rosalia, Kareen Kaye Romay, John Lloyd Silongan, Shalleah MicheleDocument39 pagesGroup 11: Rosalia, Kareen Kaye Romay, John Lloyd Silongan, Shalleah MicheleAlex MercerNo ratings yet

- Palnning NotesDocument36 pagesPalnning NotesHPNo ratings yet

- Cost Reduction Plans: You Company NameDocument34 pagesCost Reduction Plans: You Company Namejomer_juan14No ratings yet

- Chap009Document82 pagesChap009Shimul HossainNo ratings yet

- MS 06-04 BudgetingDocument3 pagesMS 06-04 BudgetingxernathanNo ratings yet

- Cosman2 ReviewerDocument6 pagesCosman2 ReviewerAggi Rayne Sali BucoyNo ratings yet

- Master BudgetingDocument3 pagesMaster BudgetingmiglapadaNo ratings yet

- Eldenburg 4e PPT Ch10Document5 pagesEldenburg 4e PPT Ch10StaygoldNo ratings yet

- Synopsis - Chapter 8 - Session 2Document4 pagesSynopsis - Chapter 8 - Session 2sajedulNo ratings yet

- Since 1977 Management Advisory ServicesDocument6 pagesSince 1977 Management Advisory ServicesdaemonspadechocoyNo ratings yet

- MS 3406 Short-Term Budgeting Additional Financing Needed and ForecastingDocument7 pagesMS 3406 Short-Term Budgeting Additional Financing Needed and ForecastingMonica GarciaNo ratings yet

- pp08Document15 pagespp08cmardenboroughNo ratings yet

- Has To Do With The Neurological Part of The Company, From The Production Itself To The Expenses Involved in Offering The Product or ServiceDocument3 pagesHas To Do With The Neurological Part of The Company, From The Production Itself To The Expenses Involved in Offering The Product or ServicewendyNo ratings yet

- Performance Appraisal Sys - MANAGERS AND SUPERVISORS - GuidelinesDocument9 pagesPerformance Appraisal Sys - MANAGERS AND SUPERVISORS - GuidelinesCherry AldayNo ratings yet

- Strategic Plan - A Strategic Plan Is The Grand Plan ofDocument3 pagesStrategic Plan - A Strategic Plan Is The Grand Plan ofPrecious Nicole SantosNo ratings yet

- Two Day Programme On Finance For Non Finance ExecutivesDocument6 pagesTwo Day Programme On Finance For Non Finance ExecutivessandystaysNo ratings yet

- BUDGETARY CONTROL AND STANDARD COSTINGDocument15 pagesBUDGETARY CONTROL AND STANDARD COSTINGPratyay DasNo ratings yet

- Week 5 ControllingDocument4 pagesWeek 5 ControllingRonica MendozaNo ratings yet

- BIA Best PracticesDocument17 pagesBIA Best Practicesbehraz100% (1)

- Standard Costing and Variance AnalysisDocument19 pagesStandard Costing and Variance AnalysisHardeep KaurNo ratings yet

- Management Accounting Environment (Final)Document3 pagesManagement Accounting Environment (Final)Mica R.No ratings yet

- Planning: Limosniro - Santos - TorreDocument22 pagesPlanning: Limosniro - Santos - TorreJulius de la CruzNo ratings yet

- 5 BudgetingDocument9 pages5 BudgetingXyril MañagoNo ratings yet

- Planning and Budgeting - PPT NotesDocument44 pagesPlanning and Budgeting - PPT NotesEmma WongNo ratings yet

- PLANNING AND WORKING CAPITAL MANAGEMENT (Chapter 3)Document3 pagesPLANNING AND WORKING CAPITAL MANAGEMENT (Chapter 3)Marie Nica J. GarciaNo ratings yet

- Cost Allocation: Learning ObjectivesDocument5 pagesCost Allocation: Learning ObjectivesHardy PutraNo ratings yet

- ControllingDocument8 pagesControllingrobNo ratings yet

- Managerial Accounting and The Business Environment: Chapter OneDocument35 pagesManagerial Accounting and The Business Environment: Chapter Oneraina mattNo ratings yet

- Solution Manual For Cornerstones of Cost Management 4th Edition Don R Hansen Maryanne M MowenDocument46 pagesSolution Manual For Cornerstones of Cost Management 4th Edition Don R Hansen Maryanne M MowenOliviaHarrisonobijq100% (76)

- Chapter IDocument44 pagesChapter IBereket DesalegnNo ratings yet

- Professional ethics and internal controlsDocument8 pagesProfessional ethics and internal controlsGlyzelle MellaNo ratings yet

- Solution Manual Managerial Accounting Hansen Mowen 8th Editions CH 8 DikonversiDocument44 pagesSolution Manual Managerial Accounting Hansen Mowen 8th Editions CH 8 Dikonversirizky aulia100% (1)

- Cost Chapter 7 PDFDocument1 pageCost Chapter 7 PDFDada ManatadNo ratings yet

- BudgetingDocument22 pagesBudgetingAashikkhan50% (2)

- 7 - Laboratory BudgetDocument1 page7 - Laboratory BudgetPORTUGAL JUSTINE ALLYSANo ratings yet

- Lesson 7Document103 pagesLesson 7henielh965No ratings yet

- Elec1 NotesDocument7 pagesElec1 NotesJames RavelaNo ratings yet

- F2-12 Budgeting - Nature, Purpose and Behavioural AspectsDocument12 pagesF2-12 Budgeting - Nature, Purpose and Behavioural AspectsJaved ImranNo ratings yet

- Budgeting Budgetary Systems 1. Rolling Budget: Shazwi Azid (SM'20)Document8 pagesBudgeting Budgetary Systems 1. Rolling Budget: Shazwi Azid (SM'20)Amir ArifNo ratings yet

- Budget: Prepared By: Joseph R. Mendoza CPA, MBADocument5 pagesBudget: Prepared By: Joseph R. Mendoza CPA, MBApot poootNo ratings yet

- Budgeting Management AccountingDocument9 pagesBudgeting Management AccountingYee Sin MeiNo ratings yet

- Topic 1 Aa025Document34 pagesTopic 1 Aa025viena patriciaNo ratings yet

- Introduction To CMDocument33 pagesIntroduction To CMHAKUNA MATATANo ratings yet

- Finance For Non Financial Managers BrochureDocument4 pagesFinance For Non Financial Managers Brochureenworld9No ratings yet

- Short-Term Planning or Profit Planning - 5 of Financial and Other Resources of The Company InaDocument3 pagesShort-Term Planning or Profit Planning - 5 of Financial and Other Resources of The Company InaAngela GarciaNo ratings yet

- Finance for Non Finance Executives_email_attachment1Document4 pagesFinance for Non Finance Executives_email_attachment1pradnyeyNo ratings yet

- BCP Risk Control PDFDocument7 pagesBCP Risk Control PDFMudassar PatelNo ratings yet

- Porter Is Not EnoughDocument62 pagesPorter Is Not EnoughLuke Robert HemmingsNo ratings yet

- BAFINAR - SW 1 ConsignmentDocument3 pagesBAFINAR - SW 1 ConsignmentRoy Mitz Aggabao Bautista V100% (1)

- Construction ContractsDocument4 pagesConstruction ContractsAnjelica MarcoNo ratings yet

- Chap 8 - Responsibility AccountingDocument51 pagesChap 8 - Responsibility AccountingKrisdeo Pardillo67% (3)

- Intro - Sustainability and Strategic AuditDocument36 pagesIntro - Sustainability and Strategic AuditLuke Robert HemmingsNo ratings yet

- Relationship between Accounts Receivable Management Practices and Growth of SMEs in Kakamega CountyDocument165 pagesRelationship between Accounts Receivable Management Practices and Growth of SMEs in Kakamega CountyLuke Robert HemmingsNo ratings yet

- Business Combination by DayagDocument37 pagesBusiness Combination by Dayagkristian Garcia85% (13)

- AFAR C1 MC AnswersDocument39 pagesAFAR C1 MC Answersheyhey84% (19)

- PAS 23 - Borrowing Cost PDFDocument16 pagesPAS 23 - Borrowing Cost PDFGeoff MacarateNo ratings yet

- Agency AccountingDocument27 pagesAgency AccountingAurcus Jumskie33% (3)

- Toaz - Info Quiz On Foreign Transactions PRDocument4 pagesToaz - Info Quiz On Foreign Transactions PRoizys131No ratings yet

- Sales agency net income and cost of sales calculationDocument27 pagesSales agency net income and cost of sales calculationKandiz89% (9)

- Quiz-Chapter1 Partnership Formation and OperationsDocument2 pagesQuiz-Chapter1 Partnership Formation and Operationsalellie100% (1)

- Agency AccountingDocument27 pagesAgency AccountingAurcus Jumskie33% (3)

- Budgeting and Cash Flow ManagementDocument4 pagesBudgeting and Cash Flow ManagementYaj Cruzada100% (1)

- Bankrupty Liquidation and ReorDocument31 pagesBankrupty Liquidation and ReorLuke Robert HemmingsNo ratings yet

- Law NotesDocument21 pagesLaw NotesVic FabeNo ratings yet

- BudgetingDocument28 pagesBudgetingJade Gomez50% (2)

- Intermediate Accounting - Practical Accounting 1Document72 pagesIntermediate Accounting - Practical Accounting 1Luke Robert HemmingsNo ratings yet

- AuditingDocument30 pagesAuditingMary Rose Mendoza91% (11)

- BudgetingDocument23 pagesBudgetingShiela Marquez100% (6)

- Law On Partnership and Corporation by Hector de LeonDocument113 pagesLaw On Partnership and Corporation by Hector de LeonShiela Marie Vics75% (12)

- Activity-Based Cost SystemDocument15 pagesActivity-Based Cost SystemLuke Robert HemmingsNo ratings yet

- Responsibility Accounting and Transfer Pricing (C. Variable Costing & Segmented ReportingDocument7 pagesResponsibility Accounting and Transfer Pricing (C. Variable Costing & Segmented ReportingDhanylane Phole Librea SeraficaNo ratings yet

- Chapter 8 35 PDF FreeDocument7 pagesChapter 8 35 PDF FreeLuke Robert HemmingsNo ratings yet

- Answer Key For EmpleoDocument17 pagesAnswer Key For EmpleoAdrian Montemayor100% (2)

- Calculate Cash and Cash EquivalentsDocument54 pagesCalculate Cash and Cash EquivalentsMARJORIE BAMBALAN86% (14)

- Answer Key For EmpleoDocument17 pagesAnswer Key For EmpleoAdrian Montemayor100% (2)

- Accounting For SMEs Illustrative ProblemsDocument5 pagesAccounting For SMEs Illustrative ProblemsKate AlvarezNo ratings yet

- Bni Organization ChartDocument1 pageBni Organization ChartVickyRahadianNo ratings yet

- Max AR Final 130812 PDFDocument731 pagesMax AR Final 130812 PDFsnjv2621No ratings yet

- Factory Accounting RulesDocument61 pagesFactory Accounting RulesMitthu KumarNo ratings yet

- Cylinder Receipt and Storage ProceduresDocument4 pagesCylinder Receipt and Storage ProceduresNishit SuvaNo ratings yet

- Session 12-Balance of PaymentsDocument19 pagesSession 12-Balance of PaymentsJai GaneshNo ratings yet

- Att-2.1 SowDocument5 pagesAtt-2.1 SowAgung FitrillaNo ratings yet

- reading_sample_sap_press_reporting_with_sap_s4hanaDocument32 pagesreading_sample_sap_press_reporting_with_sap_s4hanaCharles SantosNo ratings yet

- MICE - A New Paradigm For TourismDocument69 pagesMICE - A New Paradigm For TourismRoy Cabarles100% (1)

- PAS 141:2010 Specification For The Processing For Reuse of Waste and Used Electrical and Electronic Equipment (WEEE and UEEE)Document20 pagesPAS 141:2010 Specification For The Processing For Reuse of Waste and Used Electrical and Electronic Equipment (WEEE and UEEE)Ivan TtofimchukNo ratings yet

- JPMorgan Chase London Whale GDocument15 pagesJPMorgan Chase London Whale GMaksym ShodaNo ratings yet

- Tax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanDocument1 pageTax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanAshihsNo ratings yet

- Mesfin MuluDocument103 pagesMesfin MuluCanlor Lopes100% (1)

- Construction of Health Center ProjectDocument50 pagesConstruction of Health Center ProjectChinangNo ratings yet

- Philips V NLRC PDFDocument7 pagesPhilips V NLRC PDFIoa WnnNo ratings yet

- INTERVIEW GUIDE For BMADocument6 pagesINTERVIEW GUIDE For BMAJale Ann A. EspañolNo ratings yet

- CARGO Establishment ListDocument3 pagesCARGO Establishment ListRanjith PNo ratings yet

- 3.5 Additional Changes To Support Merchant and Acquirer Address in Visa Direct TransactionsDocument15 pages3.5 Additional Changes To Support Merchant and Acquirer Address in Visa Direct TransactionsYasir RoniNo ratings yet

- WillaWare v Jesichris ManufacturingDocument2 pagesWillaWare v Jesichris ManufacturingloschudentNo ratings yet

- Seminar On Central Bank of IndiaDocument23 pagesSeminar On Central Bank of IndiaHarshkinder SainiNo ratings yet

- The Shadow Money Lenders - Significance of Fed's Zirp PolicyDocument8 pagesThe Shadow Money Lenders - Significance of Fed's Zirp Policyasksigma6No ratings yet

- BP B1P Tests U2 LCCIDocument1 pageBP B1P Tests U2 LCCIHải NguyễnNo ratings yet

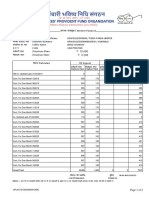

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- M.C. Shukla - A Manual of Mercantile LawDocument742 pagesM.C. Shukla - A Manual of Mercantile LawMd Ahsan-Ul- KabirNo ratings yet

- Final Ruckus ProposalDocument29 pagesFinal Ruckus Proposalapi-609740598No ratings yet

- Chip Mong Noro Mall: Property OverviewDocument4 pagesChip Mong Noro Mall: Property OverviewHe VansakNo ratings yet

- Vinamilk Yogurt Report 2019: CTCP Sữa Việt Nam (Vinamilk)Document24 pagesVinamilk Yogurt Report 2019: CTCP Sữa Việt Nam (Vinamilk)Nguyễn Hoàng TrườngNo ratings yet

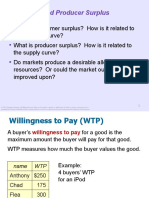

- CS, PS and EfficiencyDocument45 pagesCS, PS and EfficiencySubodh MohapatroNo ratings yet

- BSBMGT516 ASSEMENT UNIT Written Knowledge QestionsDocument8 pagesBSBMGT516 ASSEMENT UNIT Written Knowledge QestionsChathuri De Alwis50% (2)

- Certificado Reparación Carcasas Bombas y CompresoresDocument3 pagesCertificado Reparación Carcasas Bombas y CompresoresdanyNo ratings yet

- Impact of The Civil Rights Movement On Human ServicesDocument15 pagesImpact of The Civil Rights Movement On Human ServicesRacial Equity, Diversity and InclusionNo ratings yet