You might also like

- A Complete Pool Supply Store Business Plan: A Key Part Of How To Start A Pool & Spa Supply BusinessFrom EverandA Complete Pool Supply Store Business Plan: A Key Part Of How To Start A Pool & Spa Supply BusinessNo ratings yet

- Li - Ningco.ltd ReportDocument6 pagesLi - Ningco.ltd ReportzeebugNo ratings yet

- A Complete Mowing & Lawn Care Business Plan: A Key Part Of How To Start A Mowing BusinessFrom EverandA Complete Mowing & Lawn Care Business Plan: A Key Part Of How To Start A Mowing BusinessNo ratings yet

- RV Capital June 2015 LetterDocument8 pagesRV Capital June 2015 LetterCanadianValueNo ratings yet

- A Complete Landscaping Company Business Plan: A Key Part Of How To Start A Landscaping BusinessFrom EverandA Complete Landscaping Company Business Plan: A Key Part Of How To Start A Landscaping BusinessRating: 5 out of 5 stars5/5 (1)

- Big Lots Inc: Stock Report - July 23, 2016 - Nys Symbol: Big - Big Is in The S&P Midcap 400Document11 pagesBig Lots Inc: Stock Report - July 23, 2016 - Nys Symbol: Big - Big Is in The S&P Midcap 400Luis Fernando EscobarNo ratings yet

- How To Start A Pool Supply Store: A Complete Pool, Spa, and Hot Tub Equipment and Maintenance Supply Business PlanFrom EverandHow To Start A Pool Supply Store: A Complete Pool, Spa, and Hot Tub Equipment and Maintenance Supply Business PlanNo ratings yet

- 3Q16 Earnings PresentationDocument18 pages3Q16 Earnings PresentationmisterbeNo ratings yet

- Performance of Private Equity-Backed IPOs. Evidence from the UK after the financial crisisFrom EverandPerformance of Private Equity-Backed IPOs. Evidence from the UK after the financial crisisNo ratings yet

- Company Valuation P&G 2023Document16 pagesCompany Valuation P&G 2023santiagocorredor602No ratings yet

- A Complete Supplement Store Business Plan: A Key Part Of How To Start A Supplement & Health StoreFrom EverandA Complete Supplement Store Business Plan: A Key Part Of How To Start A Supplement & Health StoreNo ratings yet

- PG 2010 AnnualReportDocument82 pagesPG 2010 AnnualReportAdan OliveiraNo ratings yet

- Alert: Developments in Preparation, Compilation, and Review Engagements, 2017/18From EverandAlert: Developments in Preparation, Compilation, and Review Engagements, 2017/18No ratings yet

- Summary Report: RJET Task 1Document19 pagesSummary Report: RJET Task 1Hugo SolanoNo ratings yet

- AnandRathi Relaxo 05oct2012Document13 pagesAnandRathi Relaxo 05oct2012equityanalystinvestorNo ratings yet

- Pidilite Industries AnalysisDocument0 pagesPidilite Industries AnalysisAnitha Raja BNo ratings yet

- Ufa#Ed 2#Sol#Chap 06Document18 pagesUfa#Ed 2#Sol#Chap 06api-3824657No ratings yet

- GuessDocument87 pagesGuessharsh1881100% (1)

- Mac - 494 - 110508 - 224346 L&FDocument24 pagesMac - 494 - 110508 - 224346 L&FcaidahuihuiNo ratings yet

- Top 10 Companies That Pay More Than 25Document13 pagesTop 10 Companies That Pay More Than 25thryeeNo ratings yet

- Brand Finance Global 500 in 2016Document11 pagesBrand Finance Global 500 in 2016Andreea Alexandra BancuNo ratings yet

- 1 Main Capital Quarterly LetterDocument10 pages1 Main Capital Quarterly LetterYog MehtaNo ratings yet

- CFA Equity Research Challenge 2011 - Team 9Document15 pagesCFA Equity Research Challenge 2011 - Team 9Rohit KadamNo ratings yet

- Analyzing Mercury Athletic Footwear AcquisitionDocument5 pagesAnalyzing Mercury Athletic Footwear AcquisitionCuong NguyenNo ratings yet

- Artko Capital 2018 Q4 LetterDocument9 pagesArtko Capital 2018 Q4 LetterSmitty WNo ratings yet

- Proctor Gambles Ratio AnalysisDocument12 pagesProctor Gambles Ratio AnalysisSäKshï AhujaNo ratings yet

- Fin 320 Company Analysis 3Document10 pagesFin 320 Company Analysis 3api-319942276No ratings yet

- Gillette Pakistan Limited: Analysis of Financial StatementDocument19 pagesGillette Pakistan Limited: Analysis of Financial StatementElhemJavedNo ratings yet

- Golf Course Valuation TrendsDocument3 pagesGolf Course Valuation TrendsSarahNo ratings yet

- 15分鐘告訴你回報率在15%或更多的保險類股票Document15 pages15分鐘告訴你回報率在15%或更多的保險類股票jjy1234No ratings yet

- Godrej Financial AnalysisDocument16 pagesGodrej Financial AnalysisVaibhav Jain100% (1)

- Singapore Container Firm Goodpack Research ReportDocument3 pagesSingapore Container Firm Goodpack Research ReportventriaNo ratings yet

- HSBC Holdings PLC, H1 2018 Earnings Call, Aug 06, 2018Document16 pagesHSBC Holdings PLC, H1 2018 Earnings Call, Aug 06, 2018MKNo ratings yet

- Competitive Analysis of Athletic Footwear IndustryDocument9 pagesCompetitive Analysis of Athletic Footwear IndustryvickyNo ratings yet

- Second Quarter 2019 Investor Letter: Third Point LLC 390 Park Avenue New York, NY 10022 Tel 212 715 3880Document10 pagesSecond Quarter 2019 Investor Letter: Third Point LLC 390 Park Avenue New York, NY 10022 Tel 212 715 3880Yui ChuNo ratings yet

- Bata Report 2021Document11 pagesBata Report 2021Tanzil IslamNo ratings yet

- Craig Hallum Research ReportDocument5 pagesCraig Hallum Research Reportgrkyiasou33No ratings yet

- Analysis of Kohinoor Foods Annual ReportsDocument4 pagesAnalysis of Kohinoor Foods Annual ReportshardikgosaiNo ratings yet

- What We Don'T Own: Greenhaven Road CapitalDocument11 pagesWhat We Don'T Own: Greenhaven Road Capitall chanNo ratings yet

- Financial Analysis Task 1 Passed Submitted 4-25-13Document24 pagesFinancial Analysis Task 1 Passed Submitted 4-25-13mdjoseNo ratings yet

- M&S PLC Analysis: Strategy, Value Drivers, Critical SuccessDocument8 pagesM&S PLC Analysis: Strategy, Value Drivers, Critical Successoptimus457No ratings yet

- Thesis Summary Week 9Document4 pagesThesis Summary Week 9api-278033882No ratings yet

- Board of Directors and LeadershipDocument108 pagesBoard of Directors and LeadershipSiva KumarNo ratings yet

- Piramal Enterprises Limited Investor Presentation Nov 2016 20161108025005Document74 pagesPiramal Enterprises Limited Investor Presentation Nov 2016 20161108025005ratan203No ratings yet

- Delarue ErDocument98 pagesDelarue ErShawn PantophletNo ratings yet

- Business Strategy Game, BSI AnalyzedDocument6 pagesBusiness Strategy Game, BSI AnalyzedFrederic_PattynNo ratings yet

- FinanceDocument3 pagesFinanceVũ Hải YếnNo ratings yet

- Adidas AG, Nine Months 2014 Earnings Call, Nov 06, 2014Document16 pagesAdidas AG, Nine Months 2014 Earnings Call, Nov 06, 2014Videt JaiswalNo ratings yet

- Gap IncDocument62 pagesGap IncwillxjNo ratings yet

- HBS Case2 ToyRUs LBODocument22 pagesHBS Case2 ToyRUs LBOTam NguyenNo ratings yet

- Aditya Birla Fashion & Retail LTD Management DiscussionsDocument9 pagesAditya Birla Fashion & Retail LTD Management DiscussionsArchanaSharmaNo ratings yet

- 2023 - First - Half - Pre-Close - Trading - Update and New Regional DisclosureDocument12 pages2023 - First - Half - Pre-Close - Trading - Update and New Regional DisclosureJonathan KinnearNo ratings yet

- Screenshot 2022-11-16 at 12.56.45Document29 pagesScreenshot 2022-11-16 at 12.56.45Cornelia EsanuNo ratings yet

- 2015CAGNY Final ToShare PDFDocument68 pages2015CAGNY Final ToShare PDFArvind RachamaduguNo ratings yet

- P&Amp GNews Events, Multimedia, PublicRelations P&Amp GRespondstoTrianFundManagement, L.P. 2017-07-17Document3 pagesP&Amp GNews Events, Multimedia, PublicRelations P&Amp GRespondstoTrianFundManagement, L.P. 2017-07-17Local12WKRCNo ratings yet

- Equity Research Interview QuestionsDocument23 pagesEquity Research Interview QuestionsShubhamShekharSinhaNo ratings yet

- PumKash Footwear Strategy AnalysisDocument11 pagesPumKash Footwear Strategy Analysistconn827650% (4)

- FundCommentary Q3 2016 FinalDocument13 pagesFundCommentary Q3 2016 FinalJim BowermanNo ratings yet

- Adjusted SG&ADocument6 pagesAdjusted SG&AJOHN KAISERNo ratings yet

- Tata Motors Profitability AnalysisDocument72 pagesTata Motors Profitability AnalysisBhanu PrakashNo ratings yet

- Additional Theory Financial SystemDocument11 pagesAdditional Theory Financial SystemBinayak GhimireNo ratings yet

- Understanding Organizational GoalsDocument15 pagesUnderstanding Organizational GoalsBinayak GhimireNo ratings yet

- Detials Marketing Plan EvidhyaDocument13 pagesDetials Marketing Plan EvidhyaBinayak GhimireNo ratings yet

- Principels of Management (Question)Document5 pagesPrincipels of Management (Question)Binayak GhimireNo ratings yet

- Accretion Dilution-AnalysisDocument5 pagesAccretion Dilution-AnalysisBinayak GhimireNo ratings yet

- Final ScriptDocument2 pagesFinal ScriptBinayak GhimireNo ratings yet

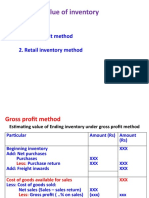

- Inventory EstimationDocument12 pagesInventory EstimationBinayak GhimireNo ratings yet

- Risk & Return (Assignment-III Group 1)Document8 pagesRisk & Return (Assignment-III Group 1)Binayak GhimireNo ratings yet

- Risk & Return (Assignment-III Group 1)Document8 pagesRisk & Return (Assignment-III Group 1)Binayak GhimireNo ratings yet

- Finance Assignment III Group 1Document23 pagesFinance Assignment III Group 1Binayak GhimireNo ratings yet

- Finance Assignment III Group 1Document23 pagesFinance Assignment III Group 1Binayak GhimireNo ratings yet

- Risk & Return (Assignment-III Group 1)Document8 pagesRisk & Return (Assignment-III Group 1)Binayak GhimireNo ratings yet

- Finance Assignment III Group 1Document23 pagesFinance Assignment III Group 1Binayak GhimireNo ratings yet

- Unit 2.3 Database ConceptDocument85 pagesUnit 2.3 Database ConceptBinayak GhimireNo ratings yet

- Transportation ProblemDocument32 pagesTransportation ProblemBinayak GhimireNo ratings yet

- Transportation ProblemDocument32 pagesTransportation ProblemBinayak GhimireNo ratings yet

- Some Good Words To ShareDocument37 pagesSome Good Words To ShareBinayak GhimireNo ratings yet

- VEC CAseDocument4 pagesVEC CAseBinayak GhimireNo ratings yet

- Unit 2.3 Database ConceptDocument85 pagesUnit 2.3 Database ConceptBinayak GhimireNo ratings yet

- Some Good Words To ShareDocument37 pagesSome Good Words To ShareBinayak GhimireNo ratings yet

- VEC CAseDocument4 pagesVEC CAseBinayak GhimireNo ratings yet

- Finance Assignment Case AnalysisDocument6 pagesFinance Assignment Case AnalysisBinayak GhimireNo ratings yet

- ManpowerGroup offers Gaurav Choudhary fixed-term contractDocument6 pagesManpowerGroup offers Gaurav Choudhary fixed-term contractGaurav ChoudharyNo ratings yet

- Currency ConversionDocument6 pagesCurrency Conversiontatyanna weaverNo ratings yet

- A Comprehensive Study of Financial Strength of Bata shoes company LtdDocument91 pagesA Comprehensive Study of Financial Strength of Bata shoes company LtdamitNo ratings yet

- Exportación de Aguaymanto o Golden BerryDocument52 pagesExportación de Aguaymanto o Golden Berrymasacre002No ratings yet

- Finance Case StudyDocument4 pagesFinance Case StudyKelvin CharlesNo ratings yet

- 11 Activity 2 OMDocument1 page11 Activity 2 OMBea Catherine Laguitao0% (1)

- Reading Material - EPF Act, 1952Document4 pagesReading Material - EPF Act, 1952Kaushik BoseNo ratings yet

- 4 PlanningDocument3 pages4 Planningnaeem_whdNo ratings yet

- Russ Dalbey ComplaintDocument33 pagesRuss Dalbey ComplaintMichael_Lee_RobertsNo ratings yet

- LELE21M880POD22001056Document4 pagesLELE21M880POD22001056Bhavik KakkaNo ratings yet

- Print - Udyam Registration Certificate1234Document3 pagesPrint - Udyam Registration Certificate1234Jaydipsinh SolankiNo ratings yet

- Ecc427 BlessinginusaDocument2 pagesEcc427 Blessinginusainusa blessingNo ratings yet

- Islamic Crowd Funding Platform Grows in SE AsiaDocument7 pagesIslamic Crowd Funding Platform Grows in SE AsiaKetoisophorone WongNo ratings yet

- Strategic Brand ManagementDocument4 pagesStrategic Brand Managementivan rickyNo ratings yet

- Chapter 10Document16 pagesChapter 10Mikylla Rodriguez VequisoNo ratings yet

- Group C ActivityDocument3 pagesGroup C ActivityGerard Andrei B. DeinlaNo ratings yet

- HRM Chapter 5Document19 pagesHRM Chapter 5Rajat ManandharNo ratings yet

- Computer Aided Production Planning: Module 4 - Load On Individual ResourcesDocument17 pagesComputer Aided Production Planning: Module 4 - Load On Individual ResourcesSushmita Verma50% (2)

- Oracle Flexcube CoreDocument2 pagesOracle Flexcube Corealexpio2k100% (1)

- Advisory 7 API Licensee Code of Conduct 20160413 MandarinDocument3 pagesAdvisory 7 API Licensee Code of Conduct 20160413 MandarinairlinemembershipNo ratings yet

- FWD: Nesl - Request To Authenticate: Nesliu@Nesl - Co.InDocument2 pagesFWD: Nesl - Request To Authenticate: Nesliu@Nesl - Co.InSagar GuptaNo ratings yet

- Thesis No Page FinalDocument10 pagesThesis No Page FinalColeen EstebanNo ratings yet

- Zambia Bata Shoe Company PLC Swot Analysis BacDocument13 pagesZambia Bata Shoe Company PLC Swot Analysis Bacphilipmwangala0No ratings yet

- BY: - Minaz Khan Sakina Kapadia Sandeep Arora Shailja SinghDocument18 pagesBY: - Minaz Khan Sakina Kapadia Sandeep Arora Shailja SinghSandiip AroraNo ratings yet

- Construction Company Profile TemplateDocument1 pageConstruction Company Profile Templatebyamukama josephNo ratings yet

- LDFA 1-27-09 Board Meeting PacketDocument120 pagesLDFA 1-27-09 Board Meeting PacketMatt HampelNo ratings yet

- Partnership Dissolution: QuizDocument5 pagesPartnership Dissolution: QuizLee SuarezNo ratings yet

- Importance of Labor Law Knowledge To The HRDocument5 pagesImportance of Labor Law Knowledge To The HRMohammad Khaled100% (1)

- BodyDocument83 pagesBodyarunantony100% (1)

- Od InterventionsDocument63 pagesOd Interventionsdeepalisharma94% (17)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (82)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- Sacred Success: A Course in Financial MiraclesFrom EverandSacred Success: A Course in Financial MiraclesRating: 5 out of 5 stars5/5 (15)

- Improve Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouFrom EverandImprove Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouRating: 5 out of 5 stars5/5 (5)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- Minding Your Own Business: A Common Sense Guide to Home Management and IndustryFrom EverandMinding Your Own Business: A Common Sense Guide to Home Management and IndustryRating: 5 out of 5 stars5/5 (1)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantFrom EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantRating: 4 out of 5 stars4/5 (104)

- How To Budget And Manage Your Money In 7 Simple StepsFrom EverandHow To Budget And Manage Your Money In 7 Simple StepsRating: 5 out of 5 stars5/5 (4)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationFrom EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationRating: 4.5 out of 5 stars4.5/5 (18)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonFrom EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonRating: 5 out of 5 stars5/5 (9)

- The New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningFrom EverandThe New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningRating: 4.5 out of 5 stars4.5/5 (8)

- Happy Go Money: Spend Smart, Save Right and Enjoy LifeFrom EverandHappy Go Money: Spend Smart, Save Right and Enjoy LifeRating: 5 out of 5 stars5/5 (4)

- Money Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayFrom EverandMoney Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayRating: 3.5 out of 5 stars3.5/5 (2)

- Minimalist Living Strategies and Habits: The Practical Guide To Minimalism To Declutter, Organize And Simplify Your Life For A Better And Meaningful LivingFrom EverandMinimalist Living Strategies and Habits: The Practical Guide To Minimalism To Declutter, Organize And Simplify Your Life For A Better And Meaningful LivingNo ratings yet

- Retirement Reality Check: How to Spend Your Money and Still Leave an Amazing LegacyFrom EverandRetirement Reality Check: How to Spend Your Money and Still Leave an Amazing LegacyNo ratings yet

- Budgeting: The Ultimate Guide for Getting Your Finances TogetherFrom EverandBudgeting: The Ultimate Guide for Getting Your Finances TogetherRating: 5 out of 5 stars5/5 (14)

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyFrom EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyRating: 5 out of 5 stars5/5 (1)

- Heart and Hustle: Use your passion. Build your brand. Achieve your dreams.From EverandHeart and Hustle: Use your passion. Build your brand. Achieve your dreams.Rating: 3.5 out of 5 stars3.5/5 (3)

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)From EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Rating: 3.5 out of 5 stars3.5/5 (9)