You might also like

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Financial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementDocument7 pagesFinancial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementAakash TiwariNo ratings yet

- Yield ObligasiDocument1 pageYield ObligasiGrace OliviaNo ratings yet

- Financial Management - Paper 1: Chapter: - Indian Financial SystemDocument23 pagesFinancial Management - Paper 1: Chapter: - Indian Financial SystemToyaj JaiswalNo ratings yet

- CH 2Document6 pagesCH 2Hemant GoyalNo ratings yet

- BF - Fourmulae - 2013Document3 pagesBF - Fourmulae - 2013AmiteshNo ratings yet

- Icfai FM Time Value of Money Ch. IiiDocument13 pagesIcfai FM Time Value of Money Ch. Iiiapi-3757629100% (3)

- FV PV (1+ K) : Fva PMT (1+k) - 1 1 - (1+ K)Document1 pageFV PV (1+ K) : Fva PMT (1+k) - 1 1 - (1+ K)tanyaNo ratings yet

- Time Value of Money Cheat Sheet: by ViaDocument3 pagesTime Value of Money Cheat Sheet: by ViaTechbotix AppsNo ratings yet

- 2022 Level I Key Facts and Formulas SheetDocument13 pages2022 Level I Key Facts and Formulas Sheetayesha ansari100% (2)

- Quiz 1 FormulasDocument2 pagesQuiz 1 FormulasCristina Beatrice MallariNo ratings yet

- CA5102 Q1 FORMULA SHEETDocument12 pagesCA5102 Q1 FORMULA SHEETDyra Mae OmegaNo ratings yet

- CSI FormulasDocument8 pagesCSI Formulasgrz7gtqq9bNo ratings yet

- ) K + 1 PV ( FV: PVGP PMT/ (K-G) (C+ (M-P) /N) / (M+P) /2 + + 2Document1 page) K + 1 PV ( FV: PVGP PMT/ (K-G) (C+ (M-P) /N) / (M+P) /2 + + 2Shubham AggarwalNo ratings yet

- Money Time RelationshipsDocument6 pagesMoney Time RelationshipsKevin KoNo ratings yet

- Hedging Interest Rate RiskDocument14 pagesHedging Interest Rate RiskVictor ManuelNo ratings yet

- FINA 7A10 - Review of ConceptsDocument2 pagesFINA 7A10 - Review of ConceptsEint PhooNo ratings yet

- Unit 5 Time Value of Money BBS Notes eduNEPAL - Info - PDFDocument3 pagesUnit 5 Time Value of Money BBS Notes eduNEPAL - Info - PDFTorreus AdhikariNo ratings yet

- FIN222 Equations NotesDocument49 pagesFIN222 Equations NotesSotiris HarisNo ratings yet

- Return: 4 - 1 - D e F I N I T I o N o F R I S K A N D R e T U R NDocument10 pagesReturn: 4 - 1 - D e F I N I T I o N o F R I S K A N D R e T U R NHenok FikaduNo ratings yet

- Formula Sheet Exam 1 PDFDocument2 pagesFormula Sheet Exam 1 PDFBlue DragonNo ratings yet

- ch1 Notes CfaDocument18 pagesch1 Notes Cfaashutosh JhaNo ratings yet

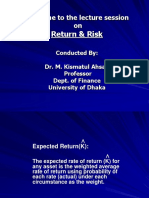

- Return & Risk: Welcome To The Lecture Session OnDocument13 pagesReturn & Risk: Welcome To The Lecture Session Onarman_277276271No ratings yet

- Tvom PDFDocument16 pagesTvom PDFgoyal_khushbu88No ratings yet

- Applications of Money-Time RelationshipsDocument52 pagesApplications of Money-Time RelationshipsGuangbeng LeeNo ratings yet

- Interest Rates That Vary With Time: I A I CWDocument3 pagesInterest Rates That Vary With Time: I A I CWTepe HolmNo ratings yet

- FV PV R: Finance Formula SheetDocument3 pagesFV PV R: Finance Formula Sheetkfir goldburdNo ratings yet

- Return & Risk Kismat Sir SlidesDocument13 pagesReturn & Risk Kismat Sir Slidessajal sazzadNo ratings yet

- Adms3530f18 Final Exam Formula Sheet PDFDocument6 pagesAdms3530f18 Final Exam Formula Sheet PDFSandy SandNo ratings yet

- Time Value of Money Project AppraisalDocument28 pagesTime Value of Money Project AppraisalKATERA DUNGANo ratings yet

- Time Value OF MoneyDocument16 pagesTime Value OF MoneyKomal AgarwalNo ratings yet

- Cong ThucDocument12 pagesCong ThucGiang Thái HươngNo ratings yet

- Corporate Finance Equations NotesDocument4 pagesCorporate Finance Equations NotesSotiris HarisNo ratings yet

- ANNUITY Afride Laskar 15Document10 pagesANNUITY Afride Laskar 15Afride LaskarNo ratings yet

- Nataliemoore Time Value of MoneyDocument4 pagesNataliemoore Time Value of MoneyMaurice AgbayaniNo ratings yet

- Time ValueDocument11 pagesTime ValueHelen BNo ratings yet

- Finanical Management Ch4Document60 pagesFinanical Management Ch4Chucky ChungNo ratings yet

- Financial Markets Final ExamDocument31 pagesFinancial Markets Final ExamdavidcarmovNo ratings yet

- Corporate Finance Lecture 2Document19 pagesCorporate Finance Lecture 2Nelly EL HassaniNo ratings yet

- Formula Sheet - PDF For Week 10Document2 pagesFormula Sheet - PDF For Week 10Nat Siow100% (1)

- The FRM Part I: Formula Guide: Value and Risk ModelsDocument10 pagesThe FRM Part I: Formula Guide: Value and Risk ModelsJavneet KaurNo ratings yet

- FinanceDocument246 pagesFinanceLuis Munguía LandinNo ratings yet

- Chapter Three: Interest Rates and Security ValuationDocument40 pagesChapter Three: Interest Rates and Security ValuationOwncoebdiefNo ratings yet

- Quantitative MethodsDocument9 pagesQuantitative Methodsumushtaq005No ratings yet

- AFM Formula SheetDocument15 pagesAFM Formula Sheetganesh bhaiNo ratings yet

- Equation Formula: 1 1 FV PMT 1Document3 pagesEquation Formula: 1 1 FV PMT 1JMSB09No ratings yet

- FM 03 Time Value of MoneyDocument14 pagesFM 03 Time Value of MoneyPrathmesh JoshiNo ratings yet

- BEC CPA Formulas November 2015 Becker CPA Review PDFDocument20 pagesBEC CPA Formulas November 2015 Becker CPA Review PDFsasyedaNo ratings yet

- FV PV: LN LN (1)Document2 pagesFV PV: LN LN (1)Danneek BillingsNo ratings yet

- 365+careers Formula+Sheet PART+1Document27 pages365+careers Formula+Sheet PART+1Narmin MirzayevaNo ratings yet

- Crib SheetDocument3 pagesCrib SheetabboussyNo ratings yet

- Exam Cheat Sheet VSJDocument3 pagesExam Cheat Sheet VSJMinh ANhNo ratings yet

- M-I-2.Time Value of MoneyDocument26 pagesM-I-2.Time Value of Moneymonalisha mishraNo ratings yet

- Sample Level 1 Wiley Formula Sheets PDFDocument10 pagesSample Level 1 Wiley Formula Sheets PDFMuhammed RafiudeenNo ratings yet

- FINMAR - Time Value of MoneyDocument2 pagesFINMAR - Time Value of MoneySean Patrick C. WONGNo ratings yet

- 1 FV Annuity C× 1+r - 1 R FV Annuity $100,000 C 1 1 1+r - 1 1.004868 - 1 R 0.004868 $615.47 Per Month.Document2 pages1 FV Annuity C× 1+r - 1 R FV Annuity $100,000 C 1 1 1+r - 1 1.004868 - 1 R 0.004868 $615.47 Per Month.nino nakashidzeNo ratings yet

- Risk and Return Formula SheetDocument7 pagesRisk and Return Formula SheetMaha Bianca Charisma CastroNo ratings yet

- Cheat Sheet FinanceDocument1 pageCheat Sheet FinanceGhitaNo ratings yet

- Executive Summary of Finance 430Document31 pagesExecutive Summary of Finance 430Ein LuckyNo ratings yet

- Deepak Nitrite ContentDocument1 pageDeepak Nitrite ContentAritra ChatterjeeNo ratings yet

- Performance Refers To A Product's Primary Operating Characteristics. For An AutomobileDocument1 pagePerformance Refers To A Product's Primary Operating Characteristics. For An AutomobileAritra ChatterjeeNo ratings yet

- Fedex Scs Has Offered Returns Management Solutions To The High-Tech Industry For Over SevenDocument2 pagesFedex Scs Has Offered Returns Management Solutions To The High-Tech Industry For Over SevenAritra ChatterjeeNo ratings yet

- 4 Case StudiesDocument4 pages4 Case StudiesAritra ChatterjeeNo ratings yet

- HDFC Bank IntroductionDocument1 pageHDFC Bank IntroductionAritra ChatterjeeNo ratings yet

- Improve Customer Experience and Enhance EfficienciesDocument1 pageImprove Customer Experience and Enhance EfficienciesAritra ChatterjeeNo ratings yet

- Q2 0Document1 pageQ2 0Aritra ChatterjeeNo ratings yet

- 4 Case StudiesDocument4 pages4 Case StudiesAritra ChatterjeeNo ratings yet

- HDFC BankDocument1 pageHDFC BankAritra ChatterjeeNo ratings yet

- HDFC BankDocument1 pageHDFC BankAritra ChatterjeeNo ratings yet

- Q1 Ans: What Is Present Value Analysis? How Do You Calculate Present Value ExampleDocument41 pagesQ1 Ans: What Is Present Value Analysis? How Do You Calculate Present Value ExampleAritra ChatterjeeNo ratings yet

- HDFC Bank IntroductionDocument1 pageHDFC Bank IntroductionAritra ChatterjeeNo ratings yet

- Improve Customer Experience and Enhance EfficienciesDocument1 pageImprove Customer Experience and Enhance EfficienciesAritra ChatterjeeNo ratings yet

- HDFC BankDocument1 pageHDFC BankAritra ChatterjeeNo ratings yet

- HDFC BankDocument1 pageHDFC BankAritra ChatterjeeNo ratings yet

- Fundamental Analysis of StocksDocument34 pagesFundamental Analysis of StocksPrajwal nayakNo ratings yet

- ECO Ebook by CA Mayank KothariDocument404 pagesECO Ebook by CA Mayank KothariHemanthNo ratings yet

- Kaizen: A Lean Manufacturing Tool For Continuous ImprovementDocument24 pagesKaizen: A Lean Manufacturing Tool For Continuous ImprovementSamrudhi PetkarNo ratings yet

- Art 1473 1548 Summary CruxDocument11 pagesArt 1473 1548 Summary CruxCruxzelle Bajo100% (1)

- Assistant AccountantDocument4 pagesAssistant AccountantfahadNo ratings yet

- Unit 1 Iot An Architectural Overview 1.1 Building An ArchitectureDocument43 pagesUnit 1 Iot An Architectural Overview 1.1 Building An Architecturedurvesh turbhekarNo ratings yet

- Target Shots I-UnlockedDocument257 pagesTarget Shots I-Unlockedsaumya ranjan nayakNo ratings yet

- Sir Jeff FX GuideDocument143 pagesSir Jeff FX GuideMadafaka MarobozuNo ratings yet

- Guide To SQL 9th Edition by Pratt Last Solution ManualDocument13 pagesGuide To SQL 9th Edition by Pratt Last Solution Manualcatherinebergtjkxfanwod100% (25)

- Model LLP AgreementDocument20 pagesModel LLP AgreementSoumitra Chawathe71% (21)

- SMP A3 PDFDocument6 pagesSMP A3 PDFMarlyn OrticioNo ratings yet

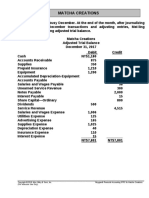

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Practice Continuti Agreement Flexi Consultancy LTDDocument3 pagesPractice Continuti Agreement Flexi Consultancy LTDrajguruprajakta26No ratings yet

- Change Management at UnileverDocument10 pagesChange Management at UnileverAnika JahanNo ratings yet

- Philippine Duplicators, Inc. vs. NLRC and Philippine Duplicators Employees Union-TupasDocument2 pagesPhilippine Duplicators, Inc. vs. NLRC and Philippine Duplicators Employees Union-TupasDennis Jay Dencio ParasNo ratings yet

- A Study On The Usage of E-Payment System and Its in Uence To Digital Financial Inclusion in Coimbatore District, Tamil NaduDocument11 pagesA Study On The Usage of E-Payment System and Its in Uence To Digital Financial Inclusion in Coimbatore District, Tamil NaduResearch SolutionsNo ratings yet

- Management Information SystemDocument1 pageManagement Information Systemgomsan7No ratings yet

- IHG® Frontline - GM Implementation Guide (Americas)Document20 pagesIHG® Frontline - GM Implementation Guide (Americas)Julie AnnaNo ratings yet

- ChatGPT PromptsDocument105 pagesChatGPT PromptsJohn ErichNo ratings yet

- Food DayDocument15 pagesFood DaydigdagNo ratings yet

- Construction ContractDocument17 pagesConstruction ContractYvonne Gam-oyNo ratings yet

- Option Valuation Black ScholesDocument18 pagesOption Valuation Black ScholessanchiNo ratings yet

- DIVYA VISHWAKARMA Construction IndustryDocument87 pagesDIVYA VISHWAKARMA Construction IndustryNITISH CHANDRA PANDEYNo ratings yet

- The Bond Market: Financial Markets and Institutions, Mishkin & EakinsDocument26 pagesThe Bond Market: Financial Markets and Institutions, Mishkin & EakinsKhondoker ShidurNo ratings yet

- Organization Development and Change: Chapter Five: Diagnosing OrganizationsDocument20 pagesOrganization Development and Change: Chapter Five: Diagnosing OrganizationsIsra AmeliaaNo ratings yet

- Consolidated Financial Statement Excercise 3-4Document2 pagesConsolidated Financial Statement Excercise 3-4Winnie TanNo ratings yet

- Sample Business Impact AssessmentDocument2 pagesSample Business Impact AssessmentbdfbgrdfbbuiwefNo ratings yet

- MIFID Best-Execution-Hot-TopicDocument8 pagesMIFID Best-Execution-Hot-TopicPranay Kumar SahuNo ratings yet

- British Policies That Led To The Exploitation of The Indian EconomyDocument3 pagesBritish Policies That Led To The Exploitation of The Indian EconomyAyushi MishraNo ratings yet

- Data Dictionary+Document4 pagesData Dictionary+Abirami SivakumarNo ratings yet