You might also like

- Doing Financial ProjectionsDocument6 pagesDoing Financial ProjectionsJitendra Nagvekar50% (2)

- Seven Habits FSADocument6 pagesSeven Habits FSAWaseem AkhtarNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- How To Forecast Financial StatementsDocument8 pagesHow To Forecast Financial StatementsHsin Wua ChiNo ratings yet

- Stock Analysis - Learn To Analyse A Stock In-DepthDocument19 pagesStock Analysis - Learn To Analyse A Stock In-DepthLiew Chee KiongNo ratings yet

- General Presentation GuidelinesDocument3 pagesGeneral Presentation GuidelinesMD Abu Hanif ShekNo ratings yet

- Build Business Value: Take Action Now, Increase the Value of your Business, Get the Most when you SellFrom EverandBuild Business Value: Take Action Now, Increase the Value of your Business, Get the Most when you SellNo ratings yet

- Business 7 Habits EffectsDocument6 pagesBusiness 7 Habits Effectssaba4533No ratings yet

- Analyzing The Income StatementDocument2 pagesAnalyzing The Income StatementHardian Buchori BarkahNo ratings yet

- Other Stock NotesDocument13 pagesOther Stock NotesManish GuptaNo ratings yet

- What Forecasts Should I Make First?: Sales ForecastDocument4 pagesWhat Forecasts Should I Make First?: Sales Forecastsadmansabbir sadmanNo ratings yet

- FinanceDocument32 pagesFinanceAkriti SinghNo ratings yet

- Tools of Fundamental AnalysisDocument7 pagesTools of Fundamental Analysisdverma1227No ratings yet

- Stock Valuation MethodsDocument5 pagesStock Valuation MethodsgoodthoughtsNo ratings yet

- DocumentDocument15 pagesDocumentharryreturnNo ratings yet

- 2020-06-16 The Income Statement MeasuresDocument5 pages2020-06-16 The Income Statement MeasuresAndres CruzNo ratings yet

- Case No.4Document9 pagesCase No.4Dipali SinghNo ratings yet

- Fundamental AnalysisDocument7 pagesFundamental AnalysisArpit JainNo ratings yet

- Case Analysis Isn't Always BetterDocument13 pagesCase Analysis Isn't Always BetterZion EliNo ratings yet

- Ratios Tell A Story F16Document3 pagesRatios Tell A Story F16Zihan ZhuangNo ratings yet

- The Importance of Sales ForecastingDocument12 pagesThe Importance of Sales ForecastingMukesh KumarNo ratings yet

- Finding Growth Stock Winners: Focus On 8 Fundamental FactorsDocument4 pagesFinding Growth Stock Winners: Focus On 8 Fundamental FactorsjpbankzNo ratings yet

- Financial Ratios 2Document7 pagesFinancial Ratios 2Mohammed UsmanNo ratings yet

- Financial Section of Business PlanDocument3 pagesFinancial Section of Business PlanFLORAH WAITHERA WANJOHINo ratings yet

- Investor Diary Stock Analysis Excel: How To Use This Spreadsheet?Document57 pagesInvestor Diary Stock Analysis Excel: How To Use This Spreadsheet?anuNo ratings yet

- Edgar L KsDocument22 pagesEdgar L KsProsenjit BhowmikNo ratings yet

- Fundamental Analysis Is The Process of Looking at A Business at The Basic or Fundamental Financial LevelDocument6 pagesFundamental Analysis Is The Process of Looking at A Business at The Basic or Fundamental Financial LevelAsghar ZaidiNo ratings yet

- How To Read and Analyze An Income StatementDocument5 pagesHow To Read and Analyze An Income StatementsaketNo ratings yet

- CAT Business AcumenDocument13 pagesCAT Business AcumenAftab AhmadNo ratings yet

- Earnings: The Indispensable Element of General Stocks: Elements of Stock Market & AnalysisDocument20 pagesEarnings: The Indispensable Element of General Stocks: Elements of Stock Market & AnalysisjosesmnNo ratings yet

- Ratios Made Simple: A beginner's guide to the key financial ratiosFrom EverandRatios Made Simple: A beginner's guide to the key financial ratiosRating: 4 out of 5 stars4/5 (5)

- Profitability and LiquidityDocument5 pagesProfitability and LiquidityEdu TainmentNo ratings yet

- Net Block DefinitionsDocument16 pagesNet Block DefinitionsSabyasachi MohapatraNo ratings yet

- Fundamental Analysis: by Investorguide StaffDocument4 pagesFundamental Analysis: by Investorguide StaffsimmishwetaNo ratings yet

- Receivables Turnover RatioDocument69 pagesReceivables Turnover RatioJulie UgsodNo ratings yet

- Walk Away Wealthy: The Entrepreneur's Exit-Planning PlaybookFrom EverandWalk Away Wealthy: The Entrepreneur's Exit-Planning PlaybookRating: 5 out of 5 stars5/5 (2)

- Capitalmind Financial Shenanigans Part 1Document17 pagesCapitalmind Financial Shenanigans Part 1abhinavnarayanNo ratings yet

- Tally Assignment BookDocument76 pagesTally Assignment Bookvihanjangid223No ratings yet

- Lesson 10 (Printer-Friendly Version)Document8 pagesLesson 10 (Printer-Friendly Version)gretatamaraNo ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- How To Write A Financial PlanDocument6 pagesHow To Write A Financial PlanGokul SoodNo ratings yet

- Financial AnalysisDocument18 pagesFinancial AnalysisNyssa AdiNo ratings yet

- AnswerDocument2 pagesAnswerAimen KhanNo ratings yet

- Steps To A Basic Company Financial AnalysisDocument21 pagesSteps To A Basic Company Financial AnalysisIvana PopovicNo ratings yet

- Analysis of Annual ReportDocument8 pagesAnalysis of Annual ReportyrockonuNo ratings yet

- Cash Flow Statement Quarter Income StatementDocument3 pagesCash Flow Statement Quarter Income StatementjaydipdesaiNo ratings yet

- Tip Sheet - 3rd Progress Report1Document2 pagesTip Sheet - 3rd Progress Report1PETRE ARANGINo ratings yet

- Financial Modelling and Analysis Using Microsoft Excel - For Non Finance PersonnelFrom EverandFinancial Modelling and Analysis Using Microsoft Excel - For Non Finance PersonnelNo ratings yet

- Free Cash FlowDocument6 pagesFree Cash FlowAnh KietNo ratings yet

- Start Up Capital (Start Up Budget) and Its SourcesDocument19 pagesStart Up Capital (Start Up Budget) and Its SourcesJaymilyn Rodas SantosNo ratings yet

- 8 Condensed ARM Approach QuestionnaireDocument48 pages8 Condensed ARM Approach Questionnairepataa0No ratings yet

- Everything About Venture CapitalistDocument13 pagesEverything About Venture Capitalisti20ayushimNo ratings yet

- (Seth Godin) If You'Re Clueless About AccountingDocument268 pages(Seth Godin) If You'Re Clueless About AccountingDaveNo ratings yet

- Interpretation of AccountDocument36 pagesInterpretation of AccountRomeo OOhlalaNo ratings yet

- Equity Valuation.Document70 pagesEquity Valuation.prashant1889No ratings yet

- Analyze Stocks Using Fundamental and Technical Data From MarketSmith PDFDocument7 pagesAnalyze Stocks Using Fundamental and Technical Data From MarketSmith PDFSwarna BhavanicharanprasadNo ratings yet

- Cash Flow AnalysisDocument14 pagesCash Flow AnalysisReza HaryoNo ratings yet

- Valves & Controls: FCT Trunnion Mounted Split Body Ball ValvesDocument16 pagesValves & Controls: FCT Trunnion Mounted Split Body Ball ValvesadrianioantomaNo ratings yet

- AARM PSX Lesson 7Document7 pagesAARM PSX Lesson 7mahboob_qayyumNo ratings yet

- AARM PSX Lesson 3Document6 pagesAARM PSX Lesson 3mahboob_qayyumNo ratings yet

- AARM PSX Lesson 4Document11 pagesAARM PSX Lesson 4mahboob_qayyumNo ratings yet

- AARM PSX Lesson 8Document7 pagesAARM PSX Lesson 8mahboob_qayyumNo ratings yet

- AARM PSX Lesson 4Document11 pagesAARM PSX Lesson 4mahboob_qayyumNo ratings yet

- Aarm PSX Lesson 1 Why To Invest in Stock MarketDocument7 pagesAarm PSX Lesson 1 Why To Invest in Stock Marketmahboob_qayyumNo ratings yet

- AARM PSX Lesson 3Document6 pagesAARM PSX Lesson 3mahboob_qayyumNo ratings yet

- Aarm PSX Lesson 1 Why To Invest in Stock MarketDocument7 pagesAarm PSX Lesson 1 Why To Invest in Stock Marketmahboob_qayyumNo ratings yet

- International Standard: Industrial Valves - Pressure Testing of Metallic ValvesDocument20 pagesInternational Standard: Industrial Valves - Pressure Testing of Metallic Valvesmahboob_qayyumNo ratings yet

- Energy Institute AVIFF GuidelinesDocument236 pagesEnergy Institute AVIFF GuidelinesMohd Reza Mohsin100% (2)

- Vol. 2 CapDocument13 pagesVol. 2 Capmahboob_qayyumNo ratings yet

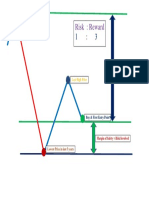

- Risk: Reward: Highest Price in Last 5 YearsDocument1 pageRisk: Reward: Highest Price in Last 5 Yearsmahboob_qayyumNo ratings yet

- Induction Water Bath HeaterDocument2 pagesInduction Water Bath Heatermahboob_qayyum100% (2)

- Modern Management in The Global Mining IndustryDocument35 pagesModern Management in The Global Mining IndustryRupesh AnnalaNo ratings yet

- Impact of Goods and Services Tax (GST) On Indian EconomyDocument5 pagesImpact of Goods and Services Tax (GST) On Indian EconomyMCOM 2050 MAMGAIN RAHUL PRASADNo ratings yet

- Manpower PlanningDocument14 pagesManpower PlanningAchintya MehrotraNo ratings yet

- Book HumanResourceManagementDocument232 pagesBook HumanResourceManagementTiara SafitriNo ratings yet

- Letter of Credit AmityDocument33 pagesLetter of Credit AmitySudhir Kochhar Fema AuthorNo ratings yet

- IDX LQ45 February 2018Document184 pagesIDX LQ45 February 2018Aprilia Dwi PurwaniNo ratings yet

- Course Syllabus - Strama 1st Sem Ay 2017-2018Document10 pagesCourse Syllabus - Strama 1st Sem Ay 2017-2018api-1942418250% (1)

- Governance and Interaction of The State, Business and Civil Society - Ok PDFDocument2 pagesGovernance and Interaction of The State, Business and Civil Society - Ok PDFPaul Laurence DocejoNo ratings yet

- Ecp0803334.pdf0t SDocument11 pagesEcp0803334.pdf0t SkotakmeghaNo ratings yet

- Yogesh Alp-CvDocument6 pagesYogesh Alp-CvAnindya SharmaNo ratings yet

- Chapter 10 Question ReviewDocument11 pagesChapter 10 Question ReviewHípPôNo ratings yet

- SBADocument21 pagesSBAJamella BraithwaiteNo ratings yet

- DAP 229 - Financial Management: Capital Budgeting Techniques / MethodDocument12 pagesDAP 229 - Financial Management: Capital Budgeting Techniques / MethodJezibel MendozaNo ratings yet

- 2nd Meeting - Mind Map C. 2 - Introduction To Cost Terms and Cost Purposes - A3 PDFDocument1 page2nd Meeting - Mind Map C. 2 - Introduction To Cost Terms and Cost Purposes - A3 PDFIsna Fauziah BiljannahNo ratings yet

- Experiences - The 7th Era of Marketing (Robert Rose Carla Johnson) (Z-Library)Document320 pagesExperiences - The 7th Era of Marketing (Robert Rose Carla Johnson) (Z-Library)Rezika lisdza natasyaNo ratings yet

- Take Home Exam 1 Cash and Cash EquivalentsDocument2 pagesTake Home Exam 1 Cash and Cash EquivalentsJi Eun VinceNo ratings yet

- Mizuho - AssociationsDocument4 pagesMizuho - AssociationsNaresh KumarNo ratings yet

- Narendra Jadhav - Monetary Policy, Financial Stability & Central BankingDocument4 pagesNarendra Jadhav - Monetary Policy, Financial Stability & Central Bankingr d0% (2)

- Deregulation of Petrol PricesDocument16 pagesDeregulation of Petrol PricesKumar AnandNo ratings yet

- Philippine Policy Towards Regional Cooperation in Southeast AsiaDocument450 pagesPhilippine Policy Towards Regional Cooperation in Southeast AsiaMariano RentomesNo ratings yet

- Plagiarism Declaration Form (T-DF)Document12 pagesPlagiarism Declaration Form (T-DF)Nur HidayahNo ratings yet

- Research DataDocument168 pagesResearch DataAli KayaniNo ratings yet

- Assessment of Mission Statement On Nine FactorsDocument4 pagesAssessment of Mission Statement On Nine FactorsSheikh ShahidNo ratings yet

- Statement 1Document4 pagesStatement 1donaldlinkous100% (1)

- How Will You Measure Your LifeDocument19 pagesHow Will You Measure Your LifeSpencerNo ratings yet

- Most Important Terms and Conditions (A) Schedule of Fees and Charges 1. Joining Fee, Annual Fees, Renewal FeesDocument8 pagesMost Important Terms and Conditions (A) Schedule of Fees and Charges 1. Joining Fee, Annual Fees, Renewal FeesbashasaruNo ratings yet

- Guagua National Colleges Graduate School Master's in Business AdministrationDocument25 pagesGuagua National Colleges Graduate School Master's in Business AdministrationLee K.No ratings yet

- Value Chain AnalysisDocument76 pagesValue Chain AnalysisA B M Rafiqul Hasan Khan67% (3)

- Template Feasibility StudyDocument26 pagesTemplate Feasibility StudyJewel Jane Marquez MartinezNo ratings yet

- A Study On Consumer Satisfaction Towards Ashok LeylandDocument9 pagesA Study On Consumer Satisfaction Towards Ashok LeylandMukesh kannan MahiNo ratings yet