You might also like

- Tax Strategies for High Net-Worth Individuals: Save Money. Invest. Reduce Taxes.From EverandTax Strategies for High Net-Worth Individuals: Save Money. Invest. Reduce Taxes.Rating: 5 out of 5 stars5/5 (1)

- The Total Money Makeover by Dave Ramsey: Summary and AnalysisFrom EverandThe Total Money Makeover by Dave Ramsey: Summary and AnalysisRating: 4.5 out of 5 stars4.5/5 (7)

- Summary of I Will Teach You To Be Rich: by Ramit Sethi | Includes AnalysisFrom EverandSummary of I Will Teach You To Be Rich: by Ramit Sethi | Includes AnalysisRating: 4 out of 5 stars4/5 (5)

- How To InvestDocument13 pagesHow To InvestwritetoevvNo ratings yet

- How To Multiply Your Money FASTDocument7 pagesHow To Multiply Your Money FASTcoldbreeze9010% (1)

- Energy Institute AVIFF GuidelinesDocument236 pagesEnergy Institute AVIFF GuidelinesMohd Reza Mohsin100% (2)

- How to Become Wealthy: Low Risk Strategies to Start a Business and Build WealthFrom EverandHow to Become Wealthy: Low Risk Strategies to Start a Business and Build WealthRating: 4 out of 5 stars4/5 (6)

- Quickstart Guide TO: InvestingDocument21 pagesQuickstart Guide TO: InvestingAmir Syazwan Bin MohamadNo ratings yet

- Investing for Beginners: Minimize Risk, Maximize Returns, Grow Your Wealth, and Achieve Financial Freedom Through The Stock Market, Index Funds, Options Trading, Cryptocurrency, Real Estate, and More.From EverandInvesting for Beginners: Minimize Risk, Maximize Returns, Grow Your Wealth, and Achieve Financial Freedom Through The Stock Market, Index Funds, Options Trading, Cryptocurrency, Real Estate, and More.Rating: 5 out of 5 stars5/5 (49)

- The Everything Guide to Investing in Your 20s & 30s: Your Step-by-Step Guide to: * Understanding Stocks, Bonds, and Mutual Funds * Maximizing Your 401(k) * Setting Realistic Goals * Recognizing the Risks and Rewards of Cryptocurrencies * Minimizing Your Investment Tax LiabilityFrom EverandThe Everything Guide to Investing in Your 20s & 30s: Your Step-by-Step Guide to: * Understanding Stocks, Bonds, and Mutual Funds * Maximizing Your 401(k) * Setting Realistic Goals * Recognizing the Risks and Rewards of Cryptocurrencies * Minimizing Your Investment Tax LiabilityNo ratings yet

- E&i QC Inspector Resum and DocumentsDocument24 pagesE&i QC Inspector Resum and DocumentsIrfan 786pakNo ratings yet

- 7 Secrets To Becoming Wealthy in Your 20s and 30sDocument14 pages7 Secrets To Becoming Wealthy in Your 20s and 30sabel becheniNo ratings yet

- How To Be A BillionaireDocument11 pagesHow To Be A BillionairehauNo ratings yet

- Prosper!, Chapter6: Financial CapitalDocument28 pagesProsper!, Chapter6: Financial CapitalAdam Taggart33% (12)

- Slash Your Retirement Risk: How to Make Your Money Last with a Simple, Safe, and Secure Investment PlanFrom EverandSlash Your Retirement Risk: How to Make Your Money Last with a Simple, Safe, and Secure Investment PlanNo ratings yet

- The Boring Secret To Getting RichDocument9 pagesThe Boring Secret To Getting RichJose Guzman100% (1)

- Prosper Chapter6v2 PDFDocument28 pagesProsper Chapter6v2 PDFAdam Taggart100% (2)

- BTL - 5000 SWT - Service Manual PDFDocument158 pagesBTL - 5000 SWT - Service Manual PDFNuno Freitas BastosNo ratings yet

- International Standard: Industrial Valves - Pressure Testing of Metallic ValvesDocument20 pagesInternational Standard: Industrial Valves - Pressure Testing of Metallic Valvesmahboob_qayyumNo ratings yet

- Road Map For Investing SuccessDocument44 pagesRoad Map For Investing Successnguyentech100% (1)

- A Beginner's Guide to Growth Stock InvestingFrom EverandA Beginner's Guide to Growth Stock InvestingRating: 4 out of 5 stars4/5 (1)

- Online Trading and Stock Investing for Beginners: The Easy Way to Start Trading and Getting Rich in the Stock MarketFrom EverandOnline Trading and Stock Investing for Beginners: The Easy Way to Start Trading and Getting Rich in the Stock MarketRating: 5 out of 5 stars5/5 (1)

- Fidelity's: Top TipsDocument24 pagesFidelity's: Top Tipsmandar LawandeNo ratings yet

- Investing for Beginners: How To Be An Intelligent Investor And Make Money On Any MarketFrom EverandInvesting for Beginners: How To Be An Intelligent Investor And Make Money On Any MarketRating: 5 out of 5 stars5/5 (44)

- The Young Adult's Guide to Investing: A Practical Guide to Finance that Helps Young People Plan, Save, and Get AheadFrom EverandThe Young Adult's Guide to Investing: A Practical Guide to Finance that Helps Young People Plan, Save, and Get AheadNo ratings yet

- The Intelligent Investor: The Definitive Book on Value Investing. A Book of Practical CounselFrom EverandThe Intelligent Investor: The Definitive Book on Value Investing. A Book of Practical CounselNo ratings yet

- How To Make Money In Stocks Value Investing StrategiesFrom EverandHow To Make Money In Stocks Value Investing StrategiesNo ratings yet

- Investing For Beginners Book: Investing Basics and Investing 101From EverandInvesting For Beginners Book: Investing Basics and Investing 101No ratings yet

- Why Most Investors FailDocument2 pagesWhy Most Investors FailINo ratings yet

- Investing Made Simple: Strategies for Building a Profitable Investment Portfolio through Real Estate, Stocks, Options Trading, Index Funds, Bonds, REITs, Bitcoin, and Beyond.From EverandInvesting Made Simple: Strategies for Building a Profitable Investment Portfolio through Real Estate, Stocks, Options Trading, Index Funds, Bonds, REITs, Bitcoin, and Beyond.Rating: 5 out of 5 stars5/5 (57)

- Induction Water Bath HeaterDocument2 pagesInduction Water Bath Heatermahboob_qayyum100% (2)

- 20 Secrets How to Get Super Rich: The Smart Guide to High Net WorthFrom Everand20 Secrets How to Get Super Rich: The Smart Guide to High Net WorthRating: 1 out of 5 stars1/5 (1)

- First Time Investor: Grow and Protect Your MoneyFrom EverandFirst Time Investor: Grow and Protect Your MoneyRating: 4 out of 5 stars4/5 (1)

- Five Keys To Investing SuccessDocument12 pagesFive Keys To Investing Successr.jeyashankar9550No ratings yet

- How To Become Rich in 10 Easy WaysDocument38 pagesHow To Become Rich in 10 Easy Wayssileshi AngerasaNo ratings yet

- Setting and Targeting Investment GoalsDocument3 pagesSetting and Targeting Investment GoalsChris RhodesNo ratings yet

- Finance Your Future: 6 Things Every Newbie Investor Should DoDocument4 pagesFinance Your Future: 6 Things Every Newbie Investor Should DoBakhshish SinghNo ratings yet

- 19 RULES FOR GETTING RICH AND STAYING RICH DESPITE WALL STREETFrom Everand19 RULES FOR GETTING RICH AND STAYING RICH DESPITE WALL STREETNo ratings yet

- The 100 Year Savings Solution: How to Create the Financial Foundation for Yourself, Your Family, and Your LegacyFrom EverandThe 100 Year Savings Solution: How to Create the Financial Foundation for Yourself, Your Family, and Your LegacyNo ratings yet

- 10 Ways To Become A Millionaire: GobankingratesDocument5 pages10 Ways To Become A Millionaire: GobankingratesʟǟʊʀɛɛֆɛNo ratings yet

- WealthDocument2 pagesWealthEkle Onoja WilliamsNo ratings yet

- Chapter 13 Investments FundamentalsDocument11 pagesChapter 13 Investments Fundamentalssaleem razaNo ratings yet

- RichDocument6 pagesRichmanish.ee.2.718No ratings yet

- Ways of Getting RichDocument3 pagesWays of Getting RichAngel DurgaNo ratings yet

- Starting A Financial PlanDocument4 pagesStarting A Financial PlanElishaNo ratings yet

- We're $520k in Debt & He Hid It From Me!: 4. Increase Your IncomeDocument6 pagesWe're $520k in Debt & He Hid It From Me!: 4. Increase Your IncomeʟǟʊʀɛɛֆɛNo ratings yet

- 16 Tips For InvestorsDocument40 pages16 Tips For InvestorsRahul VNo ratings yet

- Where To Put Your Money: Question: Where Should I Put My Money? in A Bank, Property, Business or Stocks?Document14 pagesWhere To Put Your Money: Question: Where Should I Put My Money? in A Bank, Property, Business or Stocks?zharonneNo ratings yet

- 10 Golden Rules of Investing: How To Secure Your Financial FutureDocument21 pages10 Golden Rules of Investing: How To Secure Your Financial FutureAmbar PurohitNo ratings yet

- Diez Razones Por Las Que Alguien Nunca Será RicoDocument4 pagesDiez Razones Por Las Que Alguien Nunca Será RicoJorge Arturo Cantú TorresNo ratings yet

- Property Profits: A Lazy Investor's Guide to Making Money in Real Estate Even if You Don't Have Time or Patience for All the B.S.From EverandProperty Profits: A Lazy Investor's Guide to Making Money in Real Estate Even if You Don't Have Time or Patience for All the B.S.No ratings yet

- Navigating The American Retirement Crisis Schaeffer CabotDocument9 pagesNavigating The American Retirement Crisis Schaeffer CabotAdnan ShaukatNo ratings yet

- 1 Learn To Earn 21042023 105748 AMDocument3 pages1 Learn To Earn 21042023 105748 AMmrumar7850No ratings yet

- You Are Never Too Young or Old To Start InvestingDocument40 pagesYou Are Never Too Young or Old To Start InvestingMaxNo ratings yet

- Registered Investment Advisor or InstitutionsDocument6 pagesRegistered Investment Advisor or InstitutionspublicfundinvestmentNo ratings yet

- The 80/20 Blueprint: A Millennial's Guide to Lifelong Financial ProsperityFrom EverandThe 80/20 Blueprint: A Millennial's Guide to Lifelong Financial ProsperityNo ratings yet

- Saving or InvestingDocument5 pagesSaving or InvestingLuana GaloiuNo ratings yet

- "Oh Shit, I Wish I Had Realized This Earlier": 1. Present Financial Fitness and ConditionDocument2 pages"Oh Shit, I Wish I Had Realized This Earlier": 1. Present Financial Fitness and ConditionammarNo ratings yet

- 20 yearsInvestmentJourneyNaveenJulianRego-CFPDocument3 pages20 yearsInvestmentJourneyNaveenJulianRego-CFPprajwal.bNo ratings yet

- AARM PSX Lesson 7Document7 pagesAARM PSX Lesson 7mahboob_qayyumNo ratings yet

- Valves & Controls: FCT Trunnion Mounted Split Body Ball ValvesDocument16 pagesValves & Controls: FCT Trunnion Mounted Split Body Ball ValvesadrianioantomaNo ratings yet

- AARM PSX Lesson 8Document7 pagesAARM PSX Lesson 8mahboob_qayyumNo ratings yet

- AARM PSX Lesson 4Document11 pagesAARM PSX Lesson 4mahboob_qayyumNo ratings yet

- Aarm PSX Lesson 5Document14 pagesAarm PSX Lesson 5mahboob_qayyumNo ratings yet

- AARM PSX Lesson 3Document6 pagesAARM PSX Lesson 3mahboob_qayyumNo ratings yet

- AARM PSX Lesson 3Document6 pagesAARM PSX Lesson 3mahboob_qayyumNo ratings yet

- AARM PSX Lesson 4Document11 pagesAARM PSX Lesson 4mahboob_qayyumNo ratings yet

- Aarm PSX Lesson 1 Why To Invest in Stock MarketDocument7 pagesAarm PSX Lesson 1 Why To Invest in Stock Marketmahboob_qayyumNo ratings yet

- Vol. 2 CapDocument13 pagesVol. 2 Capmahboob_qayyumNo ratings yet

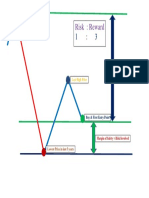

- Risk: Reward: Highest Price in Last 5 YearsDocument1 pageRisk: Reward: Highest Price in Last 5 Yearsmahboob_qayyumNo ratings yet

- User Manual - Wellwash ACDocument99 pagesUser Manual - Wellwash ACAlexandrNo ratings yet

- Bangalore Escorts Services - Riya ShettyDocument11 pagesBangalore Escorts Services - Riya ShettyRiya ShettyNo ratings yet

- SAP IAG Admin GuideDocument182 pagesSAP IAG Admin GuidegadesigerNo ratings yet

- Vedic Town Planning ConceptsDocument17 pagesVedic Town Planning ConceptsyaminiNo ratings yet

- Filtomat M300Document4 pagesFiltomat M300Sasa Jadrovski100% (1)

- BCSS Sec Unit 1 Listening and Speaking SkillsDocument16 pagesBCSS Sec Unit 1 Listening and Speaking Skillsjiny benNo ratings yet

- Nationalisation of Insurance BusinessDocument12 pagesNationalisation of Insurance BusinessSanjay Ram Diwakar50% (2)

- Business Maths Chapter 5Document9 pagesBusiness Maths Chapter 5鄭仲抗No ratings yet

- Kharrat Et Al., 2007 (Energy - Fuels)Document4 pagesKharrat Et Al., 2007 (Energy - Fuels)Leticia SakaiNo ratings yet

- Put Them Into A Big Bowl. Serve The Salad in Small Bowls. Squeeze Some Lemon Juice. Cut The Fruits Into Small Pieces. Wash The Fruits. Mix The FruitsDocument2 pagesPut Them Into A Big Bowl. Serve The Salad in Small Bowls. Squeeze Some Lemon Juice. Cut The Fruits Into Small Pieces. Wash The Fruits. Mix The FruitsNithya SweetieNo ratings yet

- Data Base Format For Company DetailsDocument12 pagesData Base Format For Company DetailsDexterJacksonNo ratings yet

- T-61.246 Digital Signal Processing and Filtering T-61.246 Digitaalinen Signaalink Asittely Ja Suodatus Description of Example ProblemsDocument35 pagesT-61.246 Digital Signal Processing and Filtering T-61.246 Digitaalinen Signaalink Asittely Ja Suodatus Description of Example ProblemsDoğukan TuranNo ratings yet

- 04 - Crystallogaphy III Miller Indices-Faces-Forms-EditedDocument63 pages04 - Crystallogaphy III Miller Indices-Faces-Forms-EditedMaisha MujibNo ratings yet

- Strategi Meningkatkan Kapasitas Penangkar Benih Padi Sawah (Oriza Sativa L) Dengan Optimalisasi Peran Kelompok TaniDocument24 pagesStrategi Meningkatkan Kapasitas Penangkar Benih Padi Sawah (Oriza Sativa L) Dengan Optimalisasi Peran Kelompok TaniHilmyTafantoNo ratings yet

- Financial/ Accounting Ratios: Sebi Grade A & Rbi Grade BDocument10 pagesFinancial/ Accounting Ratios: Sebi Grade A & Rbi Grade Bneevedita tiwariNo ratings yet

- 面向2035的新材料强国战略研究 谢曼Document9 pages面向2035的新材料强国战略研究 谢曼hexuan wangNo ratings yet

- 05271/MFP YPR SPL Sleeper Class (SL)Document2 pages05271/MFP YPR SPL Sleeper Class (SL)Rdx BoeNo ratings yet

- Material List Summary-WaptechDocument5 pagesMaterial List Summary-WaptechMarko AnticNo ratings yet

- UN Layout Key For Trade DocumentsDocument92 pagesUN Layout Key For Trade DocumentsСтоян ТитевNo ratings yet

- ALA - Assignment 3 2Document2 pagesALA - Assignment 3 2Ravi VedicNo ratings yet

- Dhulikhel RBB PDFDocument45 pagesDhulikhel RBB PDFnepalayasahitya0% (1)

- Anin, Cris Adrian U. Experiment Water Flirtation ELECTIVE 103Document2 pagesAnin, Cris Adrian U. Experiment Water Flirtation ELECTIVE 103Cris Adrian Umadac AninNo ratings yet

- Plant Gardening AerationDocument4 pagesPlant Gardening Aerationut.testbox7243No ratings yet

- E10.unit 3 - Getting StartedDocument2 pagesE10.unit 3 - Getting Started27. Nguyễn Phương LinhNo ratings yet

- Bylaws of A Texas CorporationDocument34 pagesBylaws of A Texas CorporationDiego AntoliniNo ratings yet

- CFA L1 Ethics Questions and AnswersDocument94 pagesCFA L1 Ethics Questions and AnswersMaulik PatelNo ratings yet

- Anzsco SearchDocument6 pagesAnzsco SearchytytNo ratings yet

- Oracle® Secure Backup: Installation and Configuration Guide Release 10.4Document178 pagesOracle® Secure Backup: Installation and Configuration Guide Release 10.4andrelmacedoNo ratings yet