You might also like

- Dgca Da42 Exam PaperDocument7 pagesDgca Da42 Exam PaperDharmendra YadavNo ratings yet

- MAS Final Preboard Solutions B93Document5 pagesMAS Final Preboard Solutions B93813 cafeNo ratings yet

- Feaps PortfolioDocument17 pagesFeaps Portfolioapi-317208189No ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Acct 108 Accounting For Business Combinations Quiz 4 - Intercompany Sales of AssetsDocument2 pagesAcct 108 Accounting For Business Combinations Quiz 4 - Intercompany Sales of AssetsGround ZeroNo ratings yet

- ACC 142-PeriodicalDocument11 pagesACC 142-PeriodicalRiezel PepitoNo ratings yet

- Chapter 20 Consolidated Fs Part 4 Afar Part 2Document22 pagesChapter 20 Consolidated Fs Part 4 Afar Part 2trishaNo ratings yet

- Shareholders' Equity-Contributed Capital or Paid in CapitalDocument4 pagesShareholders' Equity-Contributed Capital or Paid in CapitalJennifer AdvientoNo ratings yet

- Acc 142 - ReviewerDocument6 pagesAcc 142 - ReviewerRiezel PepitoNo ratings yet

- Translation of Foreign Currency StatementDocument5 pagesTranslation of Foreign Currency StatementPea Del Monte AñanaNo ratings yet

- Tax111 - Preferential Taxation Local Taxation Learning Exercises - StudentsDocument22 pagesTax111 - Preferential Taxation Local Taxation Learning Exercises - StudentsAimee Cute100% (1)

- Book 9Document2 pagesBook 9Actg SolmanNo ratings yet

- Jun Zen Ralph Yap BSA - 3 Year Let's CheckDocument2 pagesJun Zen Ralph Yap BSA - 3 Year Let's CheckJunzen Ralph YapNo ratings yet

- AFAR PartnershipDocument3 pagesAFAR PartnershipClyde RamosNo ratings yet

- Exam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)Document29 pagesExam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)jhean dabatosNo ratings yet

- ABC Co. Started Its OperationsDocument1 pageABC Co. Started Its OperationsQueen ValleNo ratings yet

- Auditing Problems SOLUTION v.1 - 2018Document12 pagesAuditing Problems SOLUTION v.1 - 2018Ramainne RonquilloNo ratings yet

- Fundamentals of Assurance Services - Docx'Document8 pagesFundamentals of Assurance Services - Docx'jhell dela cruzNo ratings yet

- Chapter 19 - Advacc Solman Chapter 19 - Advacc SolmanDocument16 pagesChapter 19 - Advacc Solman Chapter 19 - Advacc SolmanDrew BanlutaNo ratings yet

- Practical Accounting 1 First Pre-Board ExaminationDocument14 pagesPractical Accounting 1 First Pre-Board ExaminationKaren EloisseNo ratings yet

- ACCO 30033 LGUs With AnswersDocument3 pagesACCO 30033 LGUs With AnswersMika MolinaNo ratings yet

- Chapter 10 Insurance Contracts, Accounting For Build-Operate-Transfer (BOT) - PROFE01Document17 pagesChapter 10 Insurance Contracts, Accounting For Build-Operate-Transfer (BOT) - PROFE01Steffany RoqueNo ratings yet

- Quiz 1. Special Revenue RecognitionDocument6 pagesQuiz 1. Special Revenue RecognitionApolinar Alvarez Jr.No ratings yet

- Audit Equity AccountsDocument8 pagesAudit Equity AccountsEmerlyn Charlotte FonteNo ratings yet

- TG - Day 8 - BAM 213 - Banking LawsDocument4 pagesTG - Day 8 - BAM 213 - Banking LawsStrat CostNo ratings yet

- PUP Review Handout 3 OfficialDocument2 pagesPUP Review Handout 3 OfficialDonalyn CalipusNo ratings yet

- Auditor's Report on Financial StatementsDocument9 pagesAuditor's Report on Financial StatementsEm-em ValNo ratings yet

- AFAR-02 Corporate LiquidationDocument2 pagesAFAR-02 Corporate LiquidationRamainne RonquilloNo ratings yet

- AFAR 3 (Test Questions)Document4 pagesAFAR 3 (Test Questions)Lalaine BeatrizNo ratings yet

- Chap 1 - 3 TestbankDocument9 pagesChap 1 - 3 TestbankDiane CabiscuelasNo ratings yet

- AST FinalsDocument20 pagesAST FinalsMica Ella San DiegoNo ratings yet

- Quiz On Audit Report and DocumentationDocument6 pagesQuiz On Audit Report and DocumentationTrisha Mae AlburoNo ratings yet

- FAR 103 ACCOUNTING FOR RECEIVABLES AND NOTES RECEIVABLE PDF PDFDocument4 pagesFAR 103 ACCOUNTING FOR RECEIVABLES AND NOTES RECEIVABLE PDF PDFvhhhNo ratings yet

- ACTExamsDocument36 pagesACTExamsKaguraNo ratings yet

- Mid PS3Document8 pagesMid PS3heyNo ratings yet

- Accounting controls for special transactionsDocument12 pagesAccounting controls for special transactionsRNo ratings yet

- LNU-AA-23-02-01-18 ExamDocument13 pagesLNU-AA-23-02-01-18 ExamAmie Jane MirandaNo ratings yet

- Adv. Accounting. Business Comb. MCQDocument13 pagesAdv. Accounting. Business Comb. MCQalmira garciaNo ratings yet

- Tax Test Banks Taxation Special TopicsDocument13 pagesTax Test Banks Taxation Special TopicsKrystelle GallegoNo ratings yet

- Conso FS Part 2Document5 pagesConso FS Part 2moNo ratings yet

- Accounting For Special TransactionsDocument3 pagesAccounting For Special TransactionsnovyNo ratings yet

- REO CPA Review: Business CombinationDocument9 pagesREO CPA Review: Business CombinationRoldan Hiano ManganipNo ratings yet

- Afst Practice Set 03 Pfrs 15Document4 pagesAfst Practice Set 03 Pfrs 15Alain CopperNo ratings yet

- 92 Final PB Aud Sep 2022 Solutions 2Document4 pages92 Final PB Aud Sep 2022 Solutions 2Alliah Mae AcostaNo ratings yet

- Final ExamDocument11 pagesFinal Examdar •No ratings yet

- Chapter 3 Liquidation ValueDocument11 pagesChapter 3 Liquidation ValueJIL Masapang Victoria ChapterNo ratings yet

- LTCCDocument2 pagesLTCCN JoNo ratings yet

- Auditing Theories and Problems Quiz WEEK 2Document16 pagesAuditing Theories and Problems Quiz WEEK 2Van MateoNo ratings yet

- Consolidated Financial FormulasDocument3 pagesConsolidated Financial FormulasNiña Rica PunzalanNo ratings yet

- 91 - Final Preaboard Afar (Weekends)Document18 pages91 - Final Preaboard Afar (Weekends)Joris YapNo ratings yet

- Additional Problems On MergerDocument6 pagesAdditional Problems On MergerkakeguruiNo ratings yet

- Construction Contracts-My NotesDocument3 pagesConstruction Contracts-My Notesjhaeus enajNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Perez Long Quiz Auditing and Assurance Concepts and ApplicationDocument7 pagesPerez Long Quiz Auditing and Assurance Concepts and ApplicationMitch MinglanaNo ratings yet

- Partnership Accounting QuestionsDocument15 pagesPartnership Accounting QuestionsNhel AlvaroNo ratings yet

- Exercise DrillDocument6 pagesExercise DrillAbigail Ann PasiliaoNo ratings yet

- Afar 02 P'ship Operation QuizDocument4 pagesAfar 02 P'ship Operation QuizJohn Laurence LoplopNo ratings yet

- Home Office and Branch Accounting: Solutions To Multiple Choice Problems Problem 1Document6 pagesHome Office and Branch Accounting: Solutions To Multiple Choice Problems Problem 1Jason BautistaNo ratings yet

- Advanced Financial Accounting and Reporting: G.P. CostaDocument27 pagesAdvanced Financial Accounting and Reporting: G.P. CostaryanNo ratings yet

- Home Office, Branch Accounting & Business CombinationDocument5 pagesHome Office, Branch Accounting & Business CombinationPaupauNo ratings yet

- Additional Practice Exam Solution Updated Nov 19Document7 pagesAdditional Practice Exam Solution Updated Nov 19Shaunny BravoNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

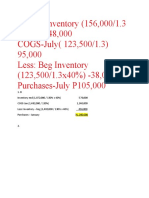

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Silent Spring: What's InsideDocument22 pagesSilent Spring: What's InsideDelina TedrosNo ratings yet

- THE END - MagDocument164 pagesTHE END - MagRozze AngelNo ratings yet

- HIST 1010 EXAM 3 TEST PREP (With Answers)Document2 pagesHIST 1010 EXAM 3 TEST PREP (With Answers)Ophelia ThorntonNo ratings yet

- Bindura University of Science Education March - August 2015 Admissions PDFDocument12 pagesBindura University of Science Education March - August 2015 Admissions PDFLuke MadzikotoNo ratings yet

- Case 26 Star River Electronics - Group Thạch Trung Chương HiểnDocument12 pagesCase 26 Star River Electronics - Group Thạch Trung Chương HiểnTrương ThạchNo ratings yet

- Physics II Eight Chapter Wise TestDocument3 pagesPhysics II Eight Chapter Wise TestSyed Waqas AhmedNo ratings yet

- Q 0092r1 - Mastersizer 3000 MAZ6222 2022 Kimia FarmaDocument4 pagesQ 0092r1 - Mastersizer 3000 MAZ6222 2022 Kimia FarmaCapital ExpenditureNo ratings yet

- Cissp NotesDocument83 pagesCissp NotesRobert Mota HawksNo ratings yet

- Effect of land use change on property valuesDocument3 pagesEffect of land use change on property valueseesuola akinyemiNo ratings yet

- Surface Modification of Titanium Orthodontic ImplaDocument30 pagesSurface Modification of Titanium Orthodontic ImplaMary SmileNo ratings yet

- D 3 Econo SPP 2110 1 eDocument123 pagesD 3 Econo SPP 2110 1 eMargarida MoreiraNo ratings yet

- Iranian Food Enquiries ReportDocument22 pagesIranian Food Enquiries Reportswapnilrane03100% (1)

- Grade 10 - Module 1Document3 pagesGrade 10 - Module 1Dypsy Pearl A. PantinopleNo ratings yet

- Activity 2EE56L FINALDocument6 pagesActivity 2EE56L FINALLUAÑA ALMARTNo ratings yet

- School Annual Data For Financial YearDocument3 pagesSchool Annual Data For Financial YearRamesh Singh100% (1)

- 2.1 Conditional Logic: Ladder ProgrammingDocument10 pages2.1 Conditional Logic: Ladder ProgrammingLuka NikitovicNo ratings yet

- C++ Classes and ObjectsDocument4 pagesC++ Classes and ObjectsAll TvwnzNo ratings yet

- COPD medications and interventionsDocument34 pagesCOPD medications and interventionssaroberts2202100% (1)

- CH9-Diversification and AcquisitionsDocument9 pagesCH9-Diversification and AcquisitionsVincent LeruthNo ratings yet

- Karla Maganda PDFDocument29 pagesKarla Maganda PDFKalay Tolentino CedoNo ratings yet

- Handley MouleDocument4 pagesHandley MouleAnonymous vcdqCTtS9No ratings yet

- Knowledge (2) Comprehension (3) Application (4) Analysis (5) Synthesis (6) EvaluationDocument5 pagesKnowledge (2) Comprehension (3) Application (4) Analysis (5) Synthesis (6) EvaluationxtinNo ratings yet

- PTR 326 Theoretical Lecture 1Document14 pagesPTR 326 Theoretical Lecture 1muhammedariwanNo ratings yet

- Easy Eight's Battleground World War II Normandy NightmareDocument97 pagesEasy Eight's Battleground World War II Normandy NightmareAdolfo JoseNo ratings yet

- Process Payments & ReceiptsDocument12 pagesProcess Payments & ReceiptsAnne FrondaNo ratings yet

- Project-Report-Cps-Report-At-Insplore (1) - 053856Document46 pagesProject-Report-Cps-Report-At-Insplore (1) - 053856Navdeep Singh0% (2)

- Insurance - Unit 3&4Document20 pagesInsurance - Unit 3&4Dhruv GandhiNo ratings yet

- Salary Income Tax Calculation in EthiopiaDocument4 pagesSalary Income Tax Calculation in EthiopiaMulatu Teshome95% (37)