You might also like

- Understanding Organizations (Business & Development)Document13 pagesUnderstanding Organizations (Business & Development)surprise MFNo ratings yet

- 3 Chapter-3Document16 pages3 Chapter-3surprise MFNo ratings yet

- Akanksha Rohilla - Mondelez International - Live ProjectDocument4 pagesAkanksha Rohilla - Mondelez International - Live Projectsurprise MFNo ratings yet

- Chapter 8: Tapping Into Global Markets: Deciding Which Markets To EnterDocument29 pagesChapter 8: Tapping Into Global Markets: Deciding Which Markets To Entersurprise MF100% (1)

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 361708380210620 Assessment Year: 2020-21Document7 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 361708380210620 Assessment Year: 2020-21surprise MFNo ratings yet

- DT 1-10Document247 pagesDT 1-10surprise MFNo ratings yet

- 1 Chapter-1Document35 pages1 Chapter-1surprise MFNo ratings yet

- Press Release Adani Agri Logistics (Harda) Limited: Details of Facilities in Annexure-1Document3 pagesPress Release Adani Agri Logistics (Harda) Limited: Details of Facilities in Annexure-1surprise MFNo ratings yet

- Section C - Group 6 - WonderChickenDocument18 pagesSection C - Group 6 - WonderChickensurprise MFNo ratings yet

- Press Release Adani Agri Logistics (Harda) LimitedDocument5 pagesPress Release Adani Agri Logistics (Harda) Limitedsurprise MFNo ratings yet

- Press Release Adani Agri Logistics (Harda) Limited: Rating Sensitivities: Positive Factors: Negative FactorsDocument4 pagesPress Release Adani Agri Logistics (Harda) Limited: Rating Sensitivities: Positive Factors: Negative Factorssurprise MFNo ratings yet

- Osd QuizDocument7 pagesOsd Quizsurprise MFNo ratings yet

- Session 10 StudentsDocument9 pagesSession 10 Studentssurprise MFNo ratings yet

- Modern DairiesDocument4 pagesModern Dairiessurprise MFNo ratings yet

- Finalists Adhyayan Seedworks Case Challenge: Congratulations Teams!!Document1 pageFinalists Adhyayan Seedworks Case Challenge: Congratulations Teams!!surprise MFNo ratings yet

- Kay Sunderland Case SolutionDocument3 pagesKay Sunderland Case Solutionsurprise MFNo ratings yet

- Ar 20200331Document368 pagesAr 20200331surprise MFNo ratings yet

- AMULDocument22 pagesAMULsurprise MFNo ratings yet

- Revised Academic Calendar 20210625115304Document1 pageRevised Academic Calendar 20210625115304surprise MFNo ratings yet

- Climate Change and Indian Agriculture:: Impacts, Coping Strategies, Programmes and PolicyDocument40 pagesClimate Change and Indian Agriculture:: Impacts, Coping Strategies, Programmes and Policysurprise MFNo ratings yet

- Ugbazaar Receipt 70378Document1 pageUgbazaar Receipt 70378surprise MFNo ratings yet

- 10 11648 J Ajpb 20200503 16Document9 pages10 11648 J Ajpb 20200503 16surprise MFNo ratings yet

- Institute of Rural Management AnandDocument2 pagesInstitute of Rural Management Anandsurprise MFNo ratings yet

- 8 Fao Monitoring and Evaluation of Climate-Smart AgricultureDocument41 pages8 Fao Monitoring and Evaluation of Climate-Smart Agriculturesurprise MFNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- AllptDocument26 pagesAllptKidlat0% (1)

- Chap 3 Development Process REM315Document78 pagesChap 3 Development Process REM315Shaleea ShaNo ratings yet

- Home Buyers Guide Standard BankDocument32 pagesHome Buyers Guide Standard Bank0796105632No ratings yet

- Literature Review On Gold Loan ProjectDocument5 pagesLiterature Review On Gold Loan Projectfahynavakel2100% (1)

- Financial System of PakistanDocument3 pagesFinancial System of Pakistaniftikharchughtai83% (12)

- JMHLL 8.75monthly Ine01a207112Document25 pagesJMHLL 8.75monthly Ine01a207112sumitkumtha123No ratings yet

- CB Insights Fintech Trends 2018Document118 pagesCB Insights Fintech Trends 2018DIana100% (1)

- Final Report Financial Institution OperationsDocument13 pagesFinal Report Financial Institution OperationsyeohzynguanNo ratings yet

- Tides Foundation 2006 990Document82 pagesTides Foundation 2006 990TheSceneOfTheCrimeNo ratings yet

- NPADocument15 pagesNPAREVA UniversityNo ratings yet

- BPLR & Base RateDocument25 pagesBPLR & Base Ratemermaid20052002No ratings yet

- Solution Manual For Accounting 9th Edition by HorngrenDocument99 pagesSolution Manual For Accounting 9th Edition by Horngrena2390059540% (1)

- Secondary Marketing Analyst Lock Desk Manager in Houston TX Resume Sharman BaumDocument2 pagesSecondary Marketing Analyst Lock Desk Manager in Houston TX Resume Sharman BaumSharmanBaumNo ratings yet

- Banking 101: By: Blake AldridgeDocument11 pagesBanking 101: By: Blake AldridgeBlake AldridgeNo ratings yet

- Npa ManagementDocument129 pagesNpa ManagementSANTOSH KUMARNo ratings yet

- Business Finance Prelim To Finals ReviewerDocument127 pagesBusiness Finance Prelim To Finals ReviewerMartin BaratetaNo ratings yet

- 106-8 Asset Sale Agreement of Church Street Health ManagementDocument261 pages106-8 Asset Sale Agreement of Church Street Health ManagementDentist The MenaceNo ratings yet

- Danske Bank Annual Report 2021Document236 pagesDanske Bank Annual Report 2021suedtNo ratings yet

- Housing Loan DeclarationDocument1 pageHousing Loan Declarationappsectesting3100% (1)

- Equifax ComplaintDocument23 pagesEquifax ComplaintDaily Kos100% (1)

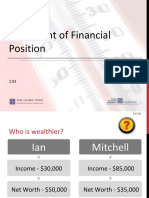

- Financial PositionDocument31 pagesFinancial PositionhaftamuNo ratings yet

- Project Report For 100 Stitching MachinesDocument11 pagesProject Report For 100 Stitching Machinesujjwal100% (1)

- Simple & Compound Interest - 700 - 800 Level QuestionsDocument2 pagesSimple & Compound Interest - 700 - 800 Level QuestionsramboriNo ratings yet

- About NMLS: System GoalsDocument1 pageAbout NMLS: System GoalsBOBNo ratings yet

- History of Usury Prohibition PDFDocument17 pagesHistory of Usury Prohibition PDFIryna BocaloNo ratings yet

- Newport Business Institute Lower Burrell CampusDocument60 pagesNewport Business Institute Lower Burrell CampuslowedogNo ratings yet

- Msme Reserve Bank of India PDFDocument6 pagesMsme Reserve Bank of India PDFAbhishek Singh ChauhanNo ratings yet

- Central Co-Operative Bank: A Summer Training Report at "Agriculture Loan"Document65 pagesCentral Co-Operative Bank: A Summer Training Report at "Agriculture Loan"Jasbir RanaNo ratings yet

- Kendriya Vidyalaya Sangthan, Ahmedabad Region Study Material For The Session 2020-21 Class X Multiple Choice and Descriptive Type QuestionsDocument53 pagesKendriya Vidyalaya Sangthan, Ahmedabad Region Study Material For The Session 2020-21 Class X Multiple Choice and Descriptive Type QuestionsAnajNo ratings yet

- Banking Customer RelationDocument79 pagesBanking Customer Relationra44993541No ratings yet