You might also like

- Gas Compression Feb 2021Document52 pagesGas Compression Feb 2021chimmy chinNo ratings yet

- 6th City Gas Stakeholders PPT - GK Sharma - MGLDocument23 pages6th City Gas Stakeholders PPT - GK Sharma - MGLSHOBHIT KUMARNo ratings yet

- Elevator Modernization Case StudyDocument22 pagesElevator Modernization Case Studyvaratharajank100% (1)

- 14 ElectricityDocument21 pages14 ElectricityFlaaffy100% (1)

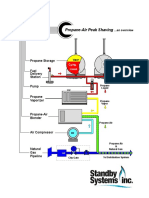

- Propane Peak Overview PDFDocument20 pagesPropane Peak Overview PDFAnonymous OktZOVjem7No ratings yet

- Design With Energy - The Conservation and Use of Energy in BuildingsDocument383 pagesDesign With Energy - The Conservation and Use of Energy in BuildingsStan Stefan100% (1)

- Process of LNG Plant PDFDocument26 pagesProcess of LNG Plant PDFodeinatus100% (3)

- HYUNDAI Mitsubishi Gas Compressor Joint VentureDocument16 pagesHYUNDAI Mitsubishi Gas Compressor Joint Venturechimmy chinNo ratings yet

- Solar Turbine Training PlanDocument34 pagesSolar Turbine Training Planchimmy chin100% (1)

- PGN Business Presentation 6M 2016 SingittttttDocument22 pagesPGN Business Presentation 6M 2016 Singittttttjulihardo parulian simarmataNo ratings yet

- BoilersDocument5 pagesBoilersSafety professionalNo ratings yet

- Perform Nursery OperationsDocument71 pagesPerform Nursery OperationsAllen Jade Pateña100% (1)

- John Crane Dry Gas Seal Example Inspection ReportDocument14 pagesJohn Crane Dry Gas Seal Example Inspection Reportchimmy chinNo ratings yet

- FOPHDocument42 pagesFOPHHariharasudhan AnnaduraiNo ratings yet

- Lab Manual Sp015 Sp025Document75 pagesLab Manual Sp015 Sp025HOO SYE PING MoeNo ratings yet

- Materi CSMS Tahap AdministrasiDocument52 pagesMateri CSMS Tahap Administrasiokta earlyNo ratings yet

- Materi CSMS Overview Untuk Vendor C&TDocument53 pagesMateri CSMS Overview Untuk Vendor C&TNdi FarhanNo ratings yet

- PS7202-Flexible AC Transmission Systems PDFDocument5 pagesPS7202-Flexible AC Transmission Systems PDF1balamanianNo ratings yet

- Design of PV SystemDocument146 pagesDesign of PV Systemanmn123100% (1)

- Sentralisasi It Untuk Mendukung Transformasi Bisnis Holding PT PertaminaDocument16 pagesSentralisasi It Untuk Mendukung Transformasi Bisnis Holding PT PertaminabrhamayudhaNo ratings yet

- Materi Distribusi Minyak Dan Gas PT Pertamina, University Pertamina - 02Document25 pagesMateri Distribusi Minyak Dan Gas PT Pertamina, University Pertamina - 02Muhammar Ridho MamarNo ratings yet

- Understanding Natural Gas and LNG Options October 11 2017 - 1Document248 pagesUnderstanding Natural Gas and LNG Options October 11 2017 - 1Tivani MphiniNo ratings yet

- Kawasaki Gas Compressor ManualDocument9 pagesKawasaki Gas Compressor Manualchimmy chinNo ratings yet

- Experiment 7 - Work and Energy On An Air TrackDocument16 pagesExperiment 7 - Work and Energy On An Air TrackMuhammad Usman MalikNo ratings yet

- RBI For Ageing PlantDocument250 pagesRBI For Ageing PlantaxlpceNo ratings yet

- LNG Small-Scale Distribution - HorekaDocument16 pagesLNG Small-Scale Distribution - Horekafian gustawan100% (1)

- Sharing Dan Diskusi Perkembangan Bisnis Gas CNG Mother Station Pertagas PertagasDocument11 pagesSharing Dan Diskusi Perkembangan Bisnis Gas CNG Mother Station Pertagas PertagasRaihan FuadNo ratings yet

- Wireless Power Transmission Final ReportDocument22 pagesWireless Power Transmission Final ReportAkhil Rastogi43% (7)

- PIASEREpppDocument28 pagesPIASEREppprieza_fNo ratings yet

- Standard Abbreviation List by Siemens 23Document1 pageStandard Abbreviation List by Siemens 23Pendl PendlNo ratings yet

- Solutions For Gas Networks DigitalisationDocument16 pagesSolutions For Gas Networks Digitalisationsohrab25No ratings yet

- Investor-Presentation-Sep2019 94f7b3afab PDFDocument38 pagesInvestor-Presentation-Sep2019 94f7b3afab PDFAshutosh GuptaNo ratings yet

- BoQ - Insulation Works (Group 2)Document4 pagesBoQ - Insulation Works (Group 2)Bhavanishankar ShettyNo ratings yet

- Statistics 2022Document4 pagesStatistics 2022Parfait BiboumNo ratings yet

- Green Zone ActivityDocument9 pagesGreen Zone ActivityMahesh ParabNo ratings yet

- Week-3-The Business of Gas and LNG TransportationDocument31 pagesWeek-3-The Business of Gas and LNG TransportationsoumyaNo ratings yet

- Narsum 2 - Bpk. Nanang (Pertamina)Document7 pagesNarsum 2 - Bpk. Nanang (Pertamina)Fikri Barry AlfianNo ratings yet

- Gujarat Gas: Best Bet Among City Gas Distribution PlayersDocument12 pagesGujarat Gas: Best Bet Among City Gas Distribution PlayersshahavNo ratings yet

- Tiago & Tigor CNGDocument1 pageTiago & Tigor CNGSaurabh BishtNo ratings yet

- Budget MineDocument1 pageBudget MineEli MayNo ratings yet

- 5b - AMNS - Track Record - LSAW Non Sour ServiceDocument4 pages5b - AMNS - Track Record - LSAW Non Sour ServiceMr ElEcTrOnNo ratings yet

- GREEN ZONE - CNG ActivityDocument7 pagesGREEN ZONE - CNG ActivityMahesh ParabNo ratings yet

- Gas Ratefinder: December 2020 Volume 48-G, No. 12Document27 pagesGas Ratefinder: December 2020 Volume 48-G, No. 12rrr44No ratings yet

- City Gas Distribution Projects: 8 Petro IndiaDocument22 pagesCity Gas Distribution Projects: 8 Petro Indiavijay240483No ratings yet

- Scaffolding Rental - One Oasis Cdo BLDG 2Document3 pagesScaffolding Rental - One Oasis Cdo BLDG 2Ronell SolijonNo ratings yet

- Introduciton of LP-FGSS For WinGD - 180829 (R0)Document26 pagesIntroduciton of LP-FGSS For WinGD - 180829 (R0)wdyouQNo ratings yet

- Daily KWHR Report-JAN-24Document134 pagesDaily KWHR Report-JAN-24Engineer Atif Rasul ChoudhryNo ratings yet

- LPG Gas Detection SystemsDocument4 pagesLPG Gas Detection SystemsVarshaNo ratings yet

- Gujarat Gas - IC - HDFC Sec-201905311810331546623Document30 pagesGujarat Gas - IC - HDFC Sec-201905311810331546623Avijoy SenguptaNo ratings yet

- Peran Geothermal Dalam Kebijakan Energi Nasional: Current Challenges, Commitment and PLN's Long-Term VisionDocument16 pagesPeran Geothermal Dalam Kebijakan Energi Nasional: Current Challenges, Commitment and PLN's Long-Term VisionjejeNo ratings yet

- Choice MNODocument14 pagesChoice MNOYu DhaNo ratings yet

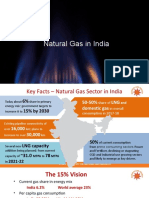

- Natural Gas in IndiaDocument19 pagesNatural Gas in IndiaAnkit PandeyNo ratings yet

- Khurmala Field Field Department Drilling Deve. Oil Wells Project TU LocationDocument9 pagesKhurmala Field Field Department Drilling Deve. Oil Wells Project TU LocationAhmedNo ratings yet

- Comparison of LNG Contractual Frameworks and Fiscal Systems SPEDocument6 pagesComparison of LNG Contractual Frameworks and Fiscal Systems SPEipali4christ_5308248No ratings yet

- Unigaz Corporate Presentation (With References)Document36 pagesUnigaz Corporate Presentation (With References)MeraNo ratings yet

- Blacklion TBR Catalog 2016Document19 pagesBlacklion TBR Catalog 2016RHaryanti0% (1)

- Suction Scrubber Discharge Scrubber: Production SeparatorDocument2 pagesSuction Scrubber Discharge Scrubber: Production SeparatorHtoo Htoo KyawNo ratings yet

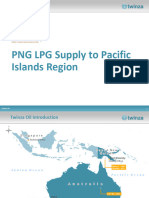

- Twinza Oil 2017Document19 pagesTwinza Oil 2017millotNo ratings yet

- Gas Production and Flares Reporting TemplateDocument1 pageGas Production and Flares Reporting TemplateEmmanuelNo ratings yet

- Auctresults 1816Document1 pageAuctresults 1816Fuaad DodooNo ratings yet

- Tips On CuttingDocument2 pagesTips On Cuttingdev-nullNo ratings yet

- Penyaluran DD Dan BLT-DD (2 November 2023)Document1 pagePenyaluran DD Dan BLT-DD (2 November 2023)Muhammad IqbalNo ratings yet

- Gujarat Gas: CMP: INR407 Strong As A Hulk!Document8 pagesGujarat Gas: CMP: INR407 Strong As A Hulk!dashNo ratings yet

- 165-4-BQE-002, Rev.C0Document6 pages165-4-BQE-002, Rev.C0Muhmmad udassirNo ratings yet

- SAGA's Corporate Brochure - Latest - LDocument16 pagesSAGA's Corporate Brochure - Latest - LAnoopNo ratings yet

- ATS by Change Meker PDFDocument1 pageATS by Change Meker PDFrizviNo ratings yet

- Price 16.03.2022Document1 pagePrice 16.03.2022jitu2968No ratings yet

- Price 16.10.2023Document1 pagePrice 16.10.2023jitu2968No ratings yet

- GD 2008Document8 pagesGD 2008asanNo ratings yet

- Testing and Commissioning HVAC System: Water BalanceDocument5 pagesTesting and Commissioning HVAC System: Water BalancemohamednavaviNo ratings yet

- Updated Gas Genset Fuel LineDocument1 pageUpdated Gas Genset Fuel Linemohsin awanNo ratings yet

- Khurmala Field Field Department Drilling Deve. Oil Wells Project TU LocationDocument9 pagesKhurmala Field Field Department Drilling Deve. Oil Wells Project TU LocationAhmedNo ratings yet

- Mr. S. N. Pandey O&G, IOCDocument30 pagesMr. S. N. Pandey O&G, IOCtarangtusharNo ratings yet

- Niger Delta Power Holding Company Limited (NDPHC) : Gas ProjectsDocument2 pagesNiger Delta Power Holding Company Limited (NDPHC) : Gas ProjectsgodwinNo ratings yet

- 6 Months, 12 Months and 18 Months ROI Contest - I3investorDocument24 pages6 Months, 12 Months and 18 Months ROI Contest - I3investorchimmy chinNo ratings yet

- Arrangements Made To Bring Jumbo Home From Sri Lanka - I3investorDocument8 pagesArrangements Made To Bring Jumbo Home From Sri Lanka - I3investorchimmy chinNo ratings yet

- Junta-Backed Media Slams Rotten' UN - I3investorDocument8 pagesJunta-Backed Media Slams Rotten' UN - I3investorchimmy chinNo ratings yet

- Oracle CloudDocument1 pageOracle Cloudchimmy chinNo ratings yet

- Australian Senator David Van Quits Liberal Party After Allegations of Misconduct - I3investorDocument8 pagesAustralian Senator David Van Quits Liberal Party After Allegations of Misconduct - I3investorchimmy chinNo ratings yet

- Morning: High Court Sentences Isa Samad To Six Years in Jail, Slaps RM15.45m FineDocument23 pagesMorning: High Court Sentences Isa Samad To Six Years in Jail, Slaps RM15.45m Finechimmy chinNo ratings yet

- Linkedin George Lee KelantanDocument3 pagesLinkedin George Lee Kelantanchimmy chinNo ratings yet

- Dresser Rand Bundle Repair Overhaul CompressorDocument5 pagesDresser Rand Bundle Repair Overhaul Compressorchimmy chinNo ratings yet

- 2 July 2021 Open VaccineDocument1 page2 July 2021 Open Vaccinechimmy chinNo ratings yet

- TMC-BHGE-NovaLT - Gas Turbine - BrochureDocument17 pagesTMC-BHGE-NovaLT - Gas Turbine - Brochurechimmy chinNo ratings yet

- Kawasaki Japan Research Tamu Gas TurbineDocument6 pagesKawasaki Japan Research Tamu Gas Turbinechimmy chinNo ratings yet

- Machinery Engineer Exxonmobil SingaporeDocument1 pageMachinery Engineer Exxonmobil Singaporechimmy chinNo ratings yet

- Pigeon Receive FreeDocument2 pagesPigeon Receive Freechimmy chinNo ratings yet

- Enthalpy For Pyrolysis For Several Types of BiomassDocument7 pagesEnthalpy For Pyrolysis For Several Types of BiomassSwiftTGSolutionsNo ratings yet

- Green House Gas Emissions in Refineries and Its Mitigation MeasuresDocument42 pagesGreen House Gas Emissions in Refineries and Its Mitigation MeasuresSarah DeanNo ratings yet

- Guide On Supercapacitor Leakage Current Behavior in EH ApplicationsDocument4 pagesGuide On Supercapacitor Leakage Current Behavior in EH ApplicationsCazimir BostanNo ratings yet

- INT69 Motor Protector: ® ApplicationDocument2 pagesINT69 Motor Protector: ® ApplicationmrcndoruNo ratings yet

- Asia Pacific Area: Offshore Wind ProjectsDocument1 pageAsia Pacific Area: Offshore Wind ProjectsKenginNo ratings yet

- CJBD-2828-6M 1/3: Characteristic Curve and Acoustics at 1.2Kg/MDocument2 pagesCJBD-2828-6M 1/3: Characteristic Curve and Acoustics at 1.2Kg/MRashedNo ratings yet

- PAGV2Document734 pagesPAGV2Leonardo Marín100% (1)

- 19.2 - Potential Difference and PowerDocument4 pages19.2 - Potential Difference and PowerDellaNo ratings yet

- h05vv FDocument1 pageh05vv FVishwanath JayaramNo ratings yet

- 9A21603 Aerospace Propulsion - IIDocument4 pages9A21603 Aerospace Propulsion - IIsivabharathamurthyNo ratings yet

- Harga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) November 2019Document8 pagesHarga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) November 2019Adnan NstNo ratings yet

- Cyberpower Ds Cp1300-1500epfclcd Nema en v2Document2 pagesCyberpower Ds Cp1300-1500epfclcd Nema en v2jimbeam2100% (1)

- In This Test, You Will Apply What You Have Learned in The Unit. Please Answer The Questions Below. Submit The Test To Your Teacher When You Are DoneDocument8 pagesIn This Test, You Will Apply What You Have Learned in The Unit. Please Answer The Questions Below. Submit The Test To Your Teacher When You Are DoneSid MathurNo ratings yet

- Heating Controls Delta Dore WebDocument32 pagesHeating Controls Delta Dore WebOlu A KujoreNo ratings yet

- Ed Ail: Voltage Loss Compensator (VLC) Three-Phase 125 - 500 kVADocument7 pagesEd Ail: Voltage Loss Compensator (VLC) Three-Phase 125 - 500 kVAwempy kurniawanNo ratings yet

- Solar TrackerDocument15 pagesSolar TrackerYash MittalNo ratings yet

- Collision Theory - WJDocument16 pagesCollision Theory - WJFilzahtuln Farihah100% (1)

- The Flowing System Gasdynamics Part 1: On Static Head in The Pipe Flowing ElementDocument3 pagesThe Flowing System Gasdynamics Part 1: On Static Head in The Pipe Flowing ElementMarc AnmellaNo ratings yet

- GCBDocument2 pagesGCBMAHIPALNo ratings yet