You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Depreciation-2Document9 pagesDepreciation-2divya shindeNo ratings yet

- DepreciationDocument21 pagesDepreciationxvfidxwmgNo ratings yet

- Unit 2 - Accountingformanager - AnanduDocument52 pagesUnit 2 - Accountingformanager - Ananducraziestidiot31No ratings yet

- DepreciationDocument3 pagesDepreciationSumanth KumarNo ratings yet

- Depreciation and Its AccountingDocument4 pagesDepreciation and Its AccountingSatish SheoranNo ratings yet

- Unit-3Document27 pagesUnit-3v9510491No ratings yet

- CCP302Document13 pagesCCP302api-3849444No ratings yet

- Depreciation AccountingDocument22 pagesDepreciation AccountingRajat srivastavaNo ratings yet

- Calculate Depreciation Using Different MethodsDocument4 pagesCalculate Depreciation Using Different MethodsowaisNo ratings yet

- Depreciation AccountingDocument12 pagesDepreciation Accountingshreyu14796No ratings yet

- DepreciationDocument21 pagesDepreciationDark XYNo ratings yet

- Discount Bank Illustrations Calculate RebateDocument7 pagesDiscount Bank Illustrations Calculate RebateAikya GandhiNo ratings yet

- Problem - 2 (Redemption by Lumpsum) (S.M Book Problem No. 10)Document5 pagesProblem - 2 (Redemption by Lumpsum) (S.M Book Problem No. 10)Gopal DasNo ratings yet

- Depreciation Accounting for Class 11 StudentsDocument19 pagesDepreciation Accounting for Class 11 StudentsMithraNo ratings yet

- Journal Date Description Post REF. DebitDocument20 pagesJournal Date Description Post REF. DebitKanika SharmaNo ratings yet

- 11 Accountancy Notes ch05 Depreciation Provision and Reserves 02 PDFDocument18 pages11 Accountancy Notes ch05 Depreciation Provision and Reserves 02 PDFVigneshNo ratings yet

- BudgetDocument7 pagesBudgetvasanthgurusamynsNo ratings yet

- Topic 3 Lease TutorialDocument9 pagesTopic 3 Lease TutorialHakim AzmiNo ratings yet

- Classes Unit 4 Commerce DepreciationDocument25 pagesClasses Unit 4 Commerce Depreciationhappy lifeNo ratings yet

- Facultyid 4 Depreciation 1672490717Document50 pagesFacultyid 4 Depreciation 1672490717Dhanaseelan thailandNo ratings yet

- Aidcom Financial Accounting AnalysisDocument17 pagesAidcom Financial Accounting AnalysisAjmal K HussainNo ratings yet

- Depr Fixed AssetDocument6 pagesDepr Fixed AssetRanib Bhakta SainjuNo ratings yet

- Acc PoojaDocument7 pagesAcc PoojaMemer BabaNo ratings yet

- II PU AccountsDocument30 pagesII PU AccountsJanani Priya100% (2)

- Depreciation Provision ReservesDocument60 pagesDepreciation Provision ReservesjonesmbNo ratings yet

- Basic Principles of AccountingDocument3 pagesBasic Principles of Accounting22ba045No ratings yet

- Commerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Document12 pagesCommerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Ashok dore Ashok doreNo ratings yet

- Revaluation Problems Part 2Document32 pagesRevaluation Problems Part 2XNo ratings yet

- HIRE PURCHASE AND INSTALLAMENT SYSTEM (Autosaved)Document16 pagesHIRE PURCHASE AND INSTALLAMENT SYSTEM (Autosaved)Mujieh NkengNo ratings yet

- DEPRECIATIONDocument11 pagesDEPRECIATIONsiddhartha RajNo ratings yet

- Gerry's classes on partnership liquidationDocument6 pagesGerry's classes on partnership liquidationgankNo ratings yet

- Project Name - HR Connect # 5 Create A Project BudgetDocument3 pagesProject Name - HR Connect # 5 Create A Project BudgetShowri ReddyNo ratings yet

- Reading of Ledger AccountDocument18 pagesReading of Ledger Accountneeru79200050% (2)

- Christ CIA FM MidtermDocument6 pagesChrist CIA FM MidtermKSHITIZ CHOUDHARYNo ratings yet

- Far510 Test Dec 2020 SSDocument6 pagesFar510 Test Dec 2020 SS2022478048No ratings yet

- Test Far510 Sept 2019 SSDocument4 pagesTest Far510 Sept 2019 SS2022478048No ratings yet

- Chapter 6 ACCA F3Document12 pagesChapter 6 ACCA F3siksha100% (1)

- G. S. College of Commerce & Economics, Nagpur: Fundamentals of Accounting StandardsDocument3 pagesG. S. College of Commerce & Economics, Nagpur: Fundamentals of Accounting StandardsRanjhana SahuNo ratings yet

- AFA End Examination 2021-2022Document6 pagesAFA End Examination 2021-2022sebastian mlingwaNo ratings yet

- Internal Reconstruction Part-IIDocument13 pagesInternal Reconstruction Part-IIINTER SMARTIANSNo ratings yet

- Kts g11 - Principles of Accounts Final AdjustmentsDocument16 pagesKts g11 - Principles of Accounts Final AdjustmentsBupe Banda100% (1)

- Problem - 7: Problem On Redemption by Annual DrawingDocument5 pagesProblem - 7: Problem On Redemption by Annual DrawingGopal DasNo ratings yet

- Assignment 2Document9 pagesAssignment 2PoommalarNo ratings yet

- Hra 11J1919Document5 pagesHra 11J1919إسماعيل البلوشيNo ratings yet

- Income StatementDocument3 pagesIncome StatementBiswajit SarmaNo ratings yet

- CA Foundation Accounts A MTP 2 Dec 2022Document11 pagesCA Foundation Accounts A MTP 2 Dec 2022shagana212005No ratings yet

- T 4Document3 pagesT 4Muntasir AhmmedNo ratings yet

- Islam Is RealDocument5 pagesIslam Is Realhussnainali shahNo ratings yet

- DepreciationDocument3 pagesDepreciationSarath kumar CNo ratings yet

- Cash and Credit ManagementDocument11 pagesCash and Credit Managementaoishic2025No ratings yet

- Solution Ultimate Sample Paper 4Document5 pagesSolution Ultimate Sample Paper 4Karthick KarthickNo ratings yet

- Basic Principle of AccountingDocument3 pagesBasic Principle of Accounting22ba045No ratings yet

- Depreciation SolutionsDocument14 pagesDepreciation SolutionsAyush MadurwarNo ratings yet

- XI Accountancy Model Set 2078Document38 pagesXI Accountancy Model Set 2078kevin bhattaraiNo ratings yet

- Goodwill 2004 - 3,43,700 (Printing Mistake)Document9 pagesGoodwill 2004 - 3,43,700 (Printing Mistake)vasanthgurusamynsNo ratings yet

- CCP302Document11 pagesCCP302api-3849444No ratings yet

- Project Report On General StoreDocument10 pagesProject Report On General StoreApplication's ManagerNo ratings yet

- Depreciation Question and Answers 2Document2 pagesDepreciation Question and Answers 2AMIN BUHARI ABDUL KHADERNo ratings yet

- Strategic Accounting Ratios Help Fitness Club Improve PerformanceDocument12 pagesStrategic Accounting Ratios Help Fitness Club Improve PerformanceabhigoldyNo ratings yet

- RVV Yb 083Document136 pagesRVV Yb 083Priyank JainNo ratings yet

- Financial ManagementDocument2 pagesFinancial ManagementPriyank JainNo ratings yet

- An Introduction To Cogno Ai Chatbot: Priyank Jain Roll No: 6617Document6 pagesAn Introduction To Cogno Ai Chatbot: Priyank Jain Roll No: 6617Priyank JainNo ratings yet

- What Was The Time When You Faced A Tough Challenge in Life and You Emerged Successfully ?Document1 pageWhat Was The Time When You Faced A Tough Challenge in Life and You Emerged Successfully ?Priyank JainNo ratings yet

- One PlusDocument98 pagesOne PlusPriyank JainNo ratings yet

- An Introduction To Cogno Ai Chatbot: Priyank Jain Roll No: 6617Document6 pagesAn Introduction To Cogno Ai Chatbot: Priyank Jain Roll No: 6617Priyank JainNo ratings yet

- What Was The Time When You Faced A Tough Challenge in Life and You Emerged Successfully ?Document1 pageWhat Was The Time When You Faced A Tough Challenge in Life and You Emerged Successfully ?Priyank JainNo ratings yet

- DocumentDocument1 pageDocumentPriyank JainNo ratings yet

- Toaz - Info GD Pi Bible PRDocument69 pagesToaz - Info GD Pi Bible PRPriyank JainNo ratings yet

- Profitability IndexDocument1 pageProfitability IndexPriyank JainNo ratings yet

- MHRD Two Year Full Time Programme Course Structure and SyllabusDocument59 pagesMHRD Two Year Full Time Programme Course Structure and SyllabusPriyank JainNo ratings yet

- Ledger TemplateDocument7 pagesLedger TemplateIts SaoirseNo ratings yet

- LSE AC444 Analysis PDFDocument256 pagesLSE AC444 Analysis PDFHu HeNo ratings yet

- IFRS 8 Operating Segments GuideDocument18 pagesIFRS 8 Operating Segments GuideDaryll DecanoNo ratings yet

- COMEX1 TAX REVIEW Canvas-1Document18 pagesCOMEX1 TAX REVIEW Canvas-1Angel RosalesNo ratings yet

- North Mountain NurseryDocument1 pageNorth Mountain Nurserychandel08No ratings yet

- Accounting exam questions on corporate accounts and costingDocument3 pagesAccounting exam questions on corporate accounts and costingd.cNo ratings yet

- Income Statement Analysis of Ford Motor CompanyDocument5 pagesIncome Statement Analysis of Ford Motor CompanyMoses MachariaNo ratings yet

- Entrepreneurship Resources Notes FinalDocument7 pagesEntrepreneurship Resources Notes FinalHSFXHFHXNo ratings yet

- CHAPTER VI - Long-Term FinancingDocument55 pagesCHAPTER VI - Long-Term FinancingMan TKNo ratings yet

- Audit Investments ChapterDocument34 pagesAudit Investments ChapterMr.AccntngNo ratings yet

- Seasons Construction estimates and costs for building projectDocument5 pagesSeasons Construction estimates and costs for building projectCarlo ParasNo ratings yet

- Business License Fees for Tobacco, Wholesale, Retail, and Other IndustriesDocument2 pagesBusiness License Fees for Tobacco, Wholesale, Retail, and Other Industriesjason camachoNo ratings yet

- Proposed 51% Asset Purchase Structure for $823,140Document1 pageProposed 51% Asset Purchase Structure for $823,140SebiNo ratings yet

- YTL Corporation: Earnings Momentum To ContinueDocument17 pagesYTL Corporation: Earnings Momentum To Continuephantom78No ratings yet

- Annexure Form for MSE Loan ApplicationDocument24 pagesAnnexure Form for MSE Loan ApplicationShakeer HussainNo ratings yet

- Info 0824Document442 pagesInfo 0824Amal RoyNo ratings yet

- Project Report Format For Bank LoanDocument7 pagesProject Report Format For Bank LoanRaju Ramjeli70% (10)

- Analysis of Banking Industry & Janata Bank: An Internship ReportDocument71 pagesAnalysis of Banking Industry & Janata Bank: An Internship ReportTareq AlamNo ratings yet

- Ac2102 RaDocument9 pagesAc2102 RaNors PataytayNo ratings yet

- Market Makers' Methods of Stock ManipulationDocument4 pagesMarket Makers' Methods of Stock Manipulationhkless100% (3)

- Due Diligence Checklist For An ASSET PurchaseDocument2 pagesDue Diligence Checklist For An ASSET PurchaseDerek Noble50% (2)

- Banking BreakdownDocument2 pagesBanking Breakdownjnn sNo ratings yet

- 17C - Jollibee Foods Corporation Press Release For 2ndQ 2021 FinalDocument7 pages17C - Jollibee Foods Corporation Press Release For 2ndQ 2021 FinalElla HermonioNo ratings yet

- This Study Resource Was: FAR Ocampo/Cabarles/Soliman/Ocampo Quiz No. 3 Set A OCTOBER 2019Document3 pagesThis Study Resource Was: FAR Ocampo/Cabarles/Soliman/Ocampo Quiz No. 3 Set A OCTOBER 2019ChjxksjsgskNo ratings yet

- Business PlanDocument10 pagesBusiness Planjoseph nsamaNo ratings yet

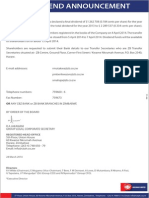

- CBZ Dividend AnnouncementDocument1 pageCBZ Dividend AnnouncementBusiness Daily ZimbabweNo ratings yet

- Sollution Accounting Chapter # 03 KeisoDocument79 pagesSollution Accounting Chapter # 03 KeisoUmair CHNo ratings yet

- Chapter - 03 - PPT (Supplementary To ISpace)Document43 pagesChapter - 03 - PPT (Supplementary To ISpace)kjw 2No ratings yet

- Fund Fact Sheets - Prosperity Index FundDocument1 pageFund Fact Sheets - Prosperity Index FundJohh-RevNo ratings yet

- Millennium Company - Projected Financial StatementDocument2 pagesMillennium Company - Projected Financial StatementKathleenCusipagNo ratings yet