You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Financial AccountingDocument746 pagesFinancial Accountingwakemeup143100% (4)

- 36) Montelibano v. Bacolod Murcia Milling 5 SCRA 36 (1962)Document5 pages36) Montelibano v. Bacolod Murcia Milling 5 SCRA 36 (1962)avatarboychrisNo ratings yet

- Corporation Code AnswersDocument2 pagesCorporation Code Answerssandra plantarNo ratings yet

- Board ResolutionDocument2 pagesBoard ResolutionFai Meile100% (1)

- Case Study May 23 - BookDocument91 pagesCase Study May 23 - Bookssssss100% (3)

- PCAB License (PCAB Categories)Document8 pagesPCAB License (PCAB Categories)Gie Bernal CamachoNo ratings yet

- Standard Operating ProcedureDocument11 pagesStandard Operating ProcedureMohamed SaiedNo ratings yet

- Loan Disbursement and Recovery SystemDocument64 pagesLoan Disbursement and Recovery SystemGeisha KNo ratings yet

- The Revised Corporation Code of The Philippines. Book of Atty. Domingo 1Document75 pagesThe Revised Corporation Code of The Philippines. Book of Atty. Domingo 1Tricia Angel P. Bantigue100% (1)

- 144 FLORIDO Pardo v. Hercules LumberDocument2 pages144 FLORIDO Pardo v. Hercules LumberjoyceNo ratings yet

- Post QualificationDocument4 pagesPost QualificationGie Bernal CamachoNo ratings yet

- Losing Weight Helped The Self-Conscious Dancer Regain Some of Her Lost ConfidenceDocument1 pageLosing Weight Helped The Self-Conscious Dancer Regain Some of Her Lost ConfidenceGie Bernal CamachoNo ratings yet

- Sample Aom - Delayed Bidding Beyond TimelinesDocument3 pagesSample Aom - Delayed Bidding Beyond TimelinesGie Bernal CamachoNo ratings yet

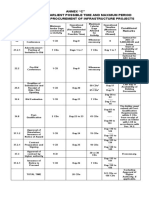

- Timelines InfrastructureDocument1 pageTimelines InfrastructureGie Bernal CamachoNo ratings yet

- 06-Exercise 2 - Appropriation, Recording and ReportingDocument10 pages06-Exercise 2 - Appropriation, Recording and ReportingGie Bernal CamachoNo ratings yet

- Question and Answer True or FalseDocument10 pagesQuestion and Answer True or FalseGie Bernal Camacho100% (1)

- Itinerary MsbernalDocument1 pageItinerary MsbernalGie Bernal CamachoNo ratings yet

- Reimbursement Espense Receipt: Appendix 46Document1 pageReimbursement Espense Receipt: Appendix 46Gie Bernal CamachoNo ratings yet

- Graphite Is Harmful Because Swallowing It Could Cause Damage To The BodyDocument1 pageGraphite Is Harmful Because Swallowing It Could Cause Damage To The BodyGie Bernal CamachoNo ratings yet

- Verb Tense: Nothing A Little Prozac Wouldn't CureDocument7 pagesVerb Tense: Nothing A Little Prozac Wouldn't CureGie Bernal CamachoNo ratings yet

- Brgy ResolutionDocument4 pagesBrgy ResolutionGie Bernal CamachoNo ratings yet

- Verb Tense: Nothing A Little Prozac Wouldn't CureDocument7 pagesVerb Tense: Nothing A Little Prozac Wouldn't CureGie Bernal CamachoNo ratings yet

- Reimbursement Espense Receipt: Appendix 46Document1 pageReimbursement Espense Receipt: Appendix 46Gie Bernal CamachoNo ratings yet

- A. Taxation As An Inherent Power of The StateDocument6 pagesA. Taxation As An Inherent Power of The StateGie Bernal CamachoNo ratings yet

- Office of The Municipal TreasurerDocument2 pagesOffice of The Municipal TreasurerGie Bernal CamachoNo ratings yet

- Stock Card and Property Card FormsDocument3 pagesStock Card and Property Card FormsGie Bernal CamachoNo ratings yet

- (Municipalities of Aroroy, Baleno, Milagros & Mobo) : Commission On AuditDocument1 page(Municipalities of Aroroy, Baleno, Milagros & Mobo) : Commission On AuditGie Bernal CamachoNo ratings yet

- Memo92 780 ROSADocument2 pagesMemo92 780 ROSAGie Bernal CamachoNo ratings yet

- Before The Securities Made Available To The Public They Must Be Registered With SECDocument2 pagesBefore The Securities Made Available To The Public They Must Be Registered With SECGie Bernal CamachoNo ratings yet

- COA Findings On BaseyDocument7 pagesCOA Findings On BaseyGie Bernal CamachoNo ratings yet

- Coa M2013-007 PDFDocument8 pagesCoa M2013-007 PDFGie Bernal CamachoNo ratings yet

- Title 1 Crimes Against National Security Ans Laws of NationDocument14 pagesTitle 1 Crimes Against National Security Ans Laws of NationGie Bernal CamachoNo ratings yet

- A-37 Property CardDocument1 pageA-37 Property CardGie Bernal CamachoNo ratings yet

- A-36 - Stock CardDocument1 pageA-36 - Stock CardGie Bernal CamachoNo ratings yet

- Dr. Ewing's Complaint With N.M. Secretary of StateDocument9 pagesDr. Ewing's Complaint With N.M. Secretary of StateKatie BieriNo ratings yet

- Executive Branch Ministry of Finance and Public CreditDocument21 pagesExecutive Branch Ministry of Finance and Public CreditJuan Domingo Padilla VazquezNo ratings yet

- Demerger LegalDocument33 pagesDemerger LegalAnupama GoswamiNo ratings yet

- Daya Summer Training ReportDocument81 pagesDaya Summer Training ReportAditya BhardwajNo ratings yet

- Lawsuit Filed by Dr. Akram Boutros Against MetroHealth (Amended 12-15-22)Document28 pagesLawsuit Filed by Dr. Akram Boutros Against MetroHealth (Amended 12-15-22)WKYC.comNo ratings yet

- KOBAY Financial Annual Report 2011Document100 pagesKOBAY Financial Annual Report 2011Rg ChandraNo ratings yet

- Checklist For Secretarial CompliancesDocument6 pagesChecklist For Secretarial CompliancesAkash AgarwalNo ratings yet

- Law2485 Group AssignmentDocument3 pagesLaw2485 Group Assignmentroll_wititNo ratings yet

- Business OrganisationsDocument3 pagesBusiness OrganisationsAnca PandeleaNo ratings yet

- Besa Vs PNBDocument4 pagesBesa Vs PNBVincent OngNo ratings yet

- BUSL301 SummaryDocument33 pagesBUSL301 Summarydavinci0317100% (1)

- John Gokongwei VS SecuritiesDocument3 pagesJohn Gokongwei VS SecuritiesWina FillomenaNo ratings yet

- Lao vs. LaoDocument16 pagesLao vs. LaoKayelyn LatNo ratings yet

- Beml Conduct-Discipline & Rules PDFDocument42 pagesBeml Conduct-Discipline & Rules PDFKamlesh KumarNo ratings yet

- Order in The Respect of Shamken Multifab Limited and OrsDocument15 pagesOrder in The Respect of Shamken Multifab Limited and OrsShyam SunderNo ratings yet

- Check List For Director ReportDocument3 pagesCheck List For Director ReportAbhishek SharmaNo ratings yet

- Teak WoodDocument10 pagesTeak WoodFransy AlbertoNo ratings yet

- COC - Annual Report Template - July 2019Document36 pagesCOC - Annual Report Template - July 2019Gabriel BuzziNo ratings yet

- National Clearing Company of Pakistan LimitedDocument96 pagesNational Clearing Company of Pakistan LimitedArslan AhmadNo ratings yet

- Complete BB Project 5 SHWETADocument75 pagesComplete BB Project 5 SHWETAAbhishek JainNo ratings yet

- Policy and Dividend Distribution of Trident Ltd. - Prerna NarwalDocument7 pagesPolicy and Dividend Distribution of Trident Ltd. - Prerna NarwalVishvesh GargNo ratings yet