You might also like

- ACC 221 - Second ExaminationDocument4 pagesACC 221 - Second ExaminationCharlesNo ratings yet

- Mendoza - Unit 1 - Statement of Changes in EquityDocument10 pagesMendoza - Unit 1 - Statement of Changes in EquityAim RubiaNo ratings yet

- MCQ On Holding CompanyDocument4 pagesMCQ On Holding Companytushar100% (3)

- Equity method accounting for investments in associatesDocument2 pagesEquity method accounting for investments in associatesAlora Eu100% (1)

- Shareholder'S Equity Multiple Choice QuestionsDocument7 pagesShareholder'S Equity Multiple Choice QuestionsRachel Rivera50% (2)

- Pas33 1Document9 pagesPas33 1d.pagkatoytoyNo ratings yet

- AFAR Theories Reviewer For CPALEDocument25 pagesAFAR Theories Reviewer For CPALEColeen CunananNo ratings yet

- Mock Cpa Board Exams - Rfjpia r-12 - W.ansDocument17 pagesMock Cpa Board Exams - Rfjpia r-12 - W.anssamson jobNo ratings yet

- Midterm or Pre Final Exam in Bus Com Trimex Pup CampusesDocument8 pagesMidterm or Pre Final Exam in Bus Com Trimex Pup CampusesmahilomferNo ratings yet

- SHAREHOLDERSDocument6 pagesSHAREHOLDERSJoana MarieNo ratings yet

- Mock Cpa Board Exams Rfjpia R 12 WDocument17 pagesMock Cpa Board Exams Rfjpia R 12 Wlongix100% (2)

- 2-1 Accounting ReviewerDocument15 pages2-1 Accounting ReviewerJulienne S. RabagoNo ratings yet

- Afar ToaDocument19 pagesAfar ToaRicamae Mendiola100% (1)

- Advanced Accounting 4th Edition Jeter Test BankDocument20 pagesAdvanced Accounting 4th Edition Jeter Test Bankbryanharrismpqrsfbokn100% (15)

- COLLEGE ACCOUNTANCY EXAMDocument8 pagesCOLLEGE ACCOUNTANCY EXAMerica insiongNo ratings yet

- Shareholders' Equity MCQDocument7 pagesShareholders' Equity MCQmae tuazon0% (1)

- A. Business CombinationDocument30 pagesA. Business CombinationJason SheeshNo ratings yet

- Accounts of Holding Companies PDFDocument6 pagesAccounts of Holding Companies PDFAnshu GauravNo ratings yet

- Cedrick SayoDocument6 pagesCedrick SayoMary Grace FloridoNo ratings yet

- Advance AccountingDocument18 pagesAdvance AccountingMarvin AquinoNo ratings yet

- QUIZ 03A ConsolidationDocument5 pagesQUIZ 03A ConsolidationCorpuz Rudica Ken33% (6)

- Operation Arising From Its Effective PortionDocument14 pagesOperation Arising From Its Effective PortionShey INFTNo ratings yet

- Consolidation-Method (Ta)Document7 pagesConsolidation-Method (Ta)Tram NgocNo ratings yet

- Chapter 04 Consolidation ofDocument64 pagesChapter 04 Consolidation ofBetty Santiago100% (1)

- All Subjects - CCDocument11 pagesAll Subjects - CCMJ YaconNo ratings yet

- Integrated Accounting Course 15 SummaryDocument11 pagesIntegrated Accounting Course 15 SummaryMaurienne Mojica0% (1)

- Chap 1 BuscomDocument6 pagesChap 1 BuscomNathalie GetinoNo ratings yet

- Business Combination TheoriesDocument2 pagesBusiness Combination TheoriesSchool Files100% (1)

- TFAR2304 - Investment in Equity SecuritiesDocument3 pagesTFAR2304 - Investment in Equity SecuritiesBea GarciaNo ratings yet

- ECO 444 Investments Test Bank-No AnswersDocument17 pagesECO 444 Investments Test Bank-No AnswersAllan Genesis Romblon100% (1)

- Accrev1 FINAL EXAM 19 20 NO ANSWERSDocument15 pagesAccrev1 FINAL EXAM 19 20 NO ANSWERSGray JavierNo ratings yet

- MILYONARYO TESTBANK AFAR-THEORIESDocument21 pagesMILYONARYO TESTBANK AFAR-THEORIESVanessa Anne Acuña DavisNo ratings yet

- Chapter 9 KDocument38 pagesChapter 9 KPauline DacirNo ratings yet

- Integrated Topic 1 (Far-004a)Document4 pagesIntegrated Topic 1 (Far-004a)lyndon delfinNo ratings yet

- Full Solution Manual Advance Accounting 5th Edition by Debra Jeter SLW1016Document18 pagesFull Solution Manual Advance Accounting 5th Edition by Debra Jeter SLW1016Sm Help75% (4)

- 15 - Investments - TheoryDocument8 pages15 - Investments - TheoryROMAR A. PIGANo ratings yet

- Act 6J03 - Comp2 - 1stsem05-06Document12 pagesAct 6J03 - Comp2 - 1stsem05-06ROMAR A. PIGANo ratings yet

- Chapter 2 3 4 15 16Document99 pagesChapter 2 3 4 15 16HayjackNo ratings yet

- ACC 113 - Week 3-1Document4 pagesACC 113 - Week 3-1Mylene HeragaNo ratings yet

- Test Bank For Advanced Accounting 5th Edition Jeter, ChaneyDocument17 pagesTest Bank For Advanced Accounting 5th Edition Jeter, ChaneyEych Mendoza100% (2)

- Afar ToaDocument22 pagesAfar ToaVanessa Anne Acuña DavisNo ratings yet

- Junior Philippine Accounting Midterms ReviewDocument5 pagesJunior Philippine Accounting Midterms ReviewezraelydanNo ratings yet

- Test Bank Advanced Accounting 5th Edition Jeter PDFDocument17 pagesTest Bank Advanced Accounting 5th Edition Jeter PDFSyra SorianoNo ratings yet

- Accounting For Business Combinations: Multiple ChoiceDocument19 pagesAccounting For Business Combinations: Multiple Choicehassan nassereddineNo ratings yet

- CH 01Document14 pagesCH 01Ryan Victor MoralesNo ratings yet

- ULS Final Quiz 1 BSA3 CY2023Document2 pagesULS Final Quiz 1 BSA3 CY2023eliescario00No ratings yet

- Afar Quick NotesDocument35 pagesAfar Quick NotesMichelle AlvarezNo ratings yet

- SIM ACC 226ACCE 411 Week 4 To 5 COPY 1Document31 pagesSIM ACC 226ACCE 411 Week 4 To 5 COPY 1Mireya Yue100% (1)

- Chapter 1: Partnership: Part 1: Theory of AccountsDocument10 pagesChapter 1: Partnership: Part 1: Theory of AccountsKeay Parado0% (1)

- Intercompany Plant Asset TransactionsDocument11 pagesIntercompany Plant Asset TransactionsRo-Anne LozadaNo ratings yet

- 1st Midterm Quiz QuestionnaireDocument11 pages1st Midterm Quiz QuestionnaireAthena Fatmah AmpuanNo ratings yet

- Quiz - Pensions & SHE MCQsDocument8 pagesQuiz - Pensions & SHE MCQsErine ContranoNo ratings yet

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Summary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingFrom EverandSummary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingNo ratings yet

- Acctg 321 A and B - Quiz - PPE - CSDocument5 pagesAcctg 321 A and B - Quiz - PPE - CSGet BurnNo ratings yet

- Acctg 321 A and B - Quiz - PPE - CSDocument5 pagesAcctg 321 A and B - Quiz - PPE - CSGet BurnNo ratings yet

- Jesus As A Healer RS Script 1Document4 pagesJesus As A Healer RS Script 1Get BurnNo ratings yet

- Q1 - Chapter 1-AnswerkeyDocument3 pagesQ1 - Chapter 1-AnswerkeyGet BurnNo ratings yet

- Accountancy Department AuditDocument6 pagesAccountancy Department AuditGet BurnNo ratings yet

- Revised Corporation Code of The Philippines - HandoutsDocument33 pagesRevised Corporation Code of The Philippines - HandoutsGet BurnNo ratings yet

- Income TaxDocument5 pagesIncome TaxGet BurnNo ratings yet

- Auditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamDocument10 pagesAuditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamGet BurnNo ratings yet

- For 0308 AssignmentDocument1 pageFor 0308 AssignmentGet BurnNo ratings yet

- Foreign CorporationDocument7 pagesForeign CorporationGet BurnNo ratings yet

- Manufacturing OperationsDocument14 pagesManufacturing OperationsGet BurnNo ratings yet

- Law On Partnership - HandoutsDocument20 pagesLaw On Partnership - HandoutsGet BurnNo ratings yet

- Lease Problem SolvingDocument1 pageLease Problem SolvingGet BurnNo ratings yet

- WITHRAWAL OFA PARTNER-WPS OfficeDocument4 pagesWITHRAWAL OFA PARTNER-WPS OfficeGet BurnNo ratings yet

- Law 311 Midterm Activity 3Document4 pagesLaw 311 Midterm Activity 3Get BurnNo ratings yet

- Problem-Job Order CostingDocument3 pagesProblem-Job Order CostingGet BurnNo ratings yet

- DocxDocument67 pagesDocxGet BurnNo ratings yet

- ACCTG 211n ReceivablesDocument3 pagesACCTG 211n ReceivablesGet BurnNo ratings yet

- PDF Chapter 03 DLDocument37 pagesPDF Chapter 03 DLGet BurnNo ratings yet

- Chapter 3 Quiz 1 PDFDocument2 pagesChapter 3 Quiz 1 PDFAhmad SyaugiNo ratings yet

- 7 Classifications of Manufacturing CostsDocument1 page7 Classifications of Manufacturing CostsGet BurnNo ratings yet

- ACCTG 221 Final Exam Part 1Document6 pagesACCTG 221 Final Exam Part 1Get BurnNo ratings yet

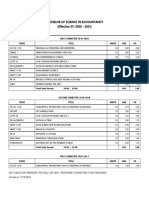

- Bachelor of Science in Accountancy (Effective SY: 2020 - 2021)Document4 pagesBachelor of Science in Accountancy (Effective SY: 2020 - 2021)Get BurnNo ratings yet

- Review 105 - Day 13 P1: Notes ReceivableDocument12 pagesReview 105 - Day 13 P1: Notes ReceivableGet BurnNo ratings yet

- Bernaldez - Donor's TaxDocument2 pagesBernaldez - Donor's TaxGet BurnNo ratings yet

- Accountancy Department transactions analysisDocument4 pagesAccountancy Department transactions analysisGet BurnNo ratings yet

- ACCTG. 221n MIDTERM EXAM SUMMER 2022 Part 2 MCQ PROBLEMDocument4 pagesACCTG. 221n MIDTERM EXAM SUMMER 2022 Part 2 MCQ PROBLEMGet BurnNo ratings yet

- 6:30 Standard CostingDocument1 page6:30 Standard CostingGet BurnNo ratings yet

- Audit of Inventories Problem 1: Requirement: Compute The Correct Amount of InventoryDocument4 pagesAudit of Inventories Problem 1: Requirement: Compute The Correct Amount of InventoryGet BurnNo ratings yet

- SMS Security Android AppDocument8 pagesSMS Security Android AppSuman SouravNo ratings yet

- How To Make Lampblack - AllDocument6 pagesHow To Make Lampblack - AllclaudjiuNo ratings yet

- Rapid Web Development With Python/Django: Julian HillDocument37 pagesRapid Web Development With Python/Django: Julian Hilljppn33No ratings yet

- PreceptronDocument17 pagesPreceptroneng_kmmNo ratings yet

- Asme A112.4.14-2004 PDFDocument14 pagesAsme A112.4.14-2004 PDFAmer AmeryNo ratings yet

- Muhammad Farrukh QAMAR - Assessment 2 Student Practical Demonstration of Tasks AURAMA006 V2Document19 pagesMuhammad Farrukh QAMAR - Assessment 2 Student Practical Demonstration of Tasks AURAMA006 V2Rana Muhammad Ashfaq Khan0% (1)

- 1 SMDocument9 pages1 SMhasanuddinnst1No ratings yet

- Outline of The Gospel of John: Book of Signs: Jesus Reveals His Glory To The World (Israel) (1:19-12:50)Document4 pagesOutline of The Gospel of John: Book of Signs: Jesus Reveals His Glory To The World (Israel) (1:19-12:50)Aamer JavedNo ratings yet

- Power Grid FailureDocument18 pagesPower Grid Failurechandra 798No ratings yet

- 7Document19 pages7Maria G. BernardinoNo ratings yet

- Employee Leave Management System: FUDMA Journal of Sciences July 2020Document7 pagesEmployee Leave Management System: FUDMA Journal of Sciences July 2020MOHAMMED ASHICKNo ratings yet

- Quotation SS20230308 100KVAR APFC PANEL VIDHYA WIRESDocument4 pagesQuotation SS20230308 100KVAR APFC PANEL VIDHYA WIRESsunil halvadiyaNo ratings yet

- Biotensegrity and Myofascial Chains A Global Approach To An Integrated Kinetic ChainDocument8 pagesBiotensegrity and Myofascial Chains A Global Approach To An Integrated Kinetic ChainMohamed ElMeligieNo ratings yet

- KR 280 R3080 F technical specificationsDocument1 pageKR 280 R3080 F technical specificationsDorobantu CatalinNo ratings yet

- LPC Licensure Process HandbookDocument14 pagesLPC Licensure Process HandbookMac PatelNo ratings yet

- AGN PresentationDocument119 pagesAGN PresentationNikki GarlejoNo ratings yet

- Introduction to Pidilite IndustriesDocument8 pagesIntroduction to Pidilite IndustriesAbhijit DharNo ratings yet

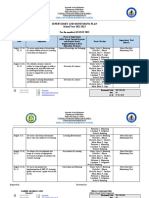

- Supervisory Plan 2022 2023Document4 pagesSupervisory Plan 2022 2023Jesieca Bulauan100% (12)

- First Aid KitDocument15 pagesFirst Aid Kitdex adecNo ratings yet

- EMAG W01 RodHeatingDocument16 pagesEMAG W01 RodHeatingMiguel Ángel ArizaNo ratings yet

- Earned Value Analysis 8 StepsDocument8 pagesEarned Value Analysis 8 StepsHira RazzaqNo ratings yet

- Choose the Right Low Boy Trailer ModelDocument42 pagesChoose the Right Low Boy Trailer ModelOdlnayer AllebramNo ratings yet

- SEO-Optimized Title for Document on English Exam QuestionsDocument4 pagesSEO-Optimized Title for Document on English Exam Questionsminh buiNo ratings yet

- Eco 121 Set 2 Fundamentals of EconomicsDocument3 pagesEco 121 Set 2 Fundamentals of EconomicsShadreck CharlesNo ratings yet

- Emd MPC 543Document25 pagesEmd MPC 543jaskaran singhNo ratings yet

- Novec1230 RoomIntegrityDocument2 pagesNovec1230 RoomIntegritynastyn-1No ratings yet

- Flat Slab NoteDocument4 pagesFlat Slab NotesasiNo ratings yet

- Probability Concepts and Random Variable - SMTA1402: Unit - IDocument105 pagesProbability Concepts and Random Variable - SMTA1402: Unit - IVigneshwar SNo ratings yet

- Arm Cortex InstructionsDocument14 pagesArm Cortex InstructionsHamsini ShreenivasNo ratings yet