You might also like

- Stephane Reverre - The Complete Arbitrage Deskbook PDFDocument527 pagesStephane Reverre - The Complete Arbitrage Deskbook PDFlucacastagna83% (6)

- Chapter 3 SolutionsDocument16 pagesChapter 3 SolutionsEdmond ZNo ratings yet

- Toyota Maintanence Schedule PDFDocument10 pagesToyota Maintanence Schedule PDFcod22050% (2)

- CLEP Principles of Macroeconomics Practice TestDocument15 pagesCLEP Principles of Macroeconomics Practice Testsundevil2010usa4605No ratings yet

- Bonds 2 Questions UweDocument1 pageBonds 2 Questions UweAshok ShresthaNo ratings yet

- SQI and Drops Improvement of Silchar City Airtel ASSAM BY Muddasar NPI AssamDocument9 pagesSQI and Drops Improvement of Silchar City Airtel ASSAM BY Muddasar NPI AssamgauravmakhlogaNo ratings yet

- MCA Trend Assistant 32171300a-EnDocument5 pagesMCA Trend Assistant 32171300a-EnFábio LeiteNo ratings yet

- Base Metals Q2 2010 - OutlookDocument14 pagesBase Metals Q2 2010 - Outlookkoderi100% (1)

- HA MonoEstación Andamarca TempMaxMensual 1hidroañoDocument6 pagesHA MonoEstación Andamarca TempMaxMensual 1hidroañoHeidy E. MendozaNo ratings yet

- The Stock Market in MarchDocument2 pagesThe Stock Market in MarchJohn Paul GroomNo ratings yet

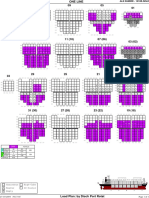

- Als Sumire 1018e Load Scan Plan (Colour)Document1 pageAls Sumire 1018e Load Scan Plan (Colour)Anonymous WnxskULNo ratings yet

- Where Are We in The Global Crisis?Document14 pagesWhere Are We in The Global Crisis?charudhall164217No ratings yet

- The Oil Market Through The Lens of The Latest Oil Price CycleDocument22 pagesThe Oil Market Through The Lens of The Latest Oil Price CycleAnkit BirharuaNo ratings yet

- VR16 URG-I CQB GBB Parts ListDocument1 pageVR16 URG-I CQB GBB Parts Listthrow away100% (1)

- Oklahoma Budget Overview: Trends and Outlook, August 2010Document45 pagesOklahoma Budget Overview: Trends and Outlook, August 2010dblattokNo ratings yet

- MGFB10Midterm W2014 SolutionOnlyV1 PDFDocument7 pagesMGFB10Midterm W2014 SolutionOnlyV1 PDFSarah KNo ratings yet

- 08 TLResultDocument2 pages08 TLResultUmair AhmedNo ratings yet

- 08 TLResultDocument2 pages08 TLResultUmair AhmedNo ratings yet

- Oati 30 enDocument48 pagesOati 30 enerereredssdfsfdsfNo ratings yet

- Introduction To The Fifth Power Plan: Figure 1-1 - Daily Average Firm Prices at Mid ColumbiaDocument11 pagesIntroduction To The Fifth Power Plan: Figure 1-1 - Daily Average Firm Prices at Mid Columbiawildan irfansyahNo ratings yet

- TheArgentineEconomy IAE - Marzo 2011Document43 pagesTheArgentineEconomy IAE - Marzo 2011norbertoNo ratings yet

- Previous Pageblock Return To Previous Menu Next PageblockDocument4 pagesPrevious Pageblock Return To Previous Menu Next PageblockRobin JacketNo ratings yet

- Cable NIDocument1 pageCable NIGaber3No ratings yet

- Political Economy in Shambles Some Additions To The Marxist-Leninist Crisis TheoryDocument52 pagesPolitical Economy in Shambles Some Additions To The Marxist-Leninist Crisis TheorypweispfenningNo ratings yet

- HA MonoEstación Andamarca PrecipMensual EnerDic 1Document6 pagesHA MonoEstación Andamarca PrecipMensual EnerDic 1Heidy E. MendozaNo ratings yet

- The Stock Market in MayDocument2 pagesThe Stock Market in MayJohn Paul GroomNo ratings yet

- Forex PDFDocument76 pagesForex PDFjeet bagdaiNo ratings yet

- Trading Journal Template 34Document2 pagesTrading Journal Template 34Dery AnggaraNo ratings yet

- Optimal Group, Inc.: Company BackgroundDocument10 pagesOptimal Group, Inc.: Company BackgroundMeester KewpieNo ratings yet

- FX Money MGT (Performance) v2Document1 pageFX Money MGT (Performance) v2Alex WongNo ratings yet

- HEINEKEN NV (Beverages) : Earnings & Estimates Market DataDocument3 pagesHEINEKEN NV (Beverages) : Earnings & Estimates Market DataDrag MadielNo ratings yet

- The Trendpointers Report: Advance Signals For Economic Expectations and ConsumptionDocument19 pagesThe Trendpointers Report: Advance Signals For Economic Expectations and ConsumptionmarcycapronNo ratings yet

- Master-2008-09-Rrp Calculation SheetDocument52 pagesMaster-2008-09-Rrp Calculation Sheetstructuredes.1No ratings yet

- World Bank Commodity Price Data (The Pink Sheet)Document166 pagesWorld Bank Commodity Price Data (The Pink Sheet)Vincent LauNo ratings yet

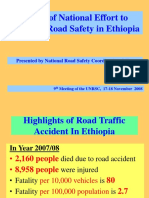

- Status of National Effort To Enhance Road Safety in EthiopiaDocument19 pagesStatus of National Effort To Enhance Road Safety in EthiopiaPulkitSainiDbspNo ratings yet

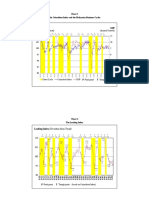

- Chart 3 The Coincident Index and The Malaysian Business CyclesDocument8 pagesChart 3 The Coincident Index and The Malaysian Business Cyclessmazadamha sulaimanNo ratings yet

- Bulk Denstiy CalculationDocument65 pagesBulk Denstiy CalculationFrank VargasNo ratings yet

- High Probability Trading Slide - Kathy Lien (Part 1)Document57 pagesHigh Probability Trading Slide - Kathy Lien (Part 1)IsabelNogales100% (2)

- GraphsDocument3 pagesGraphsJohn Paul GroomNo ratings yet

- HMW 3 - AnswersDocument5 pagesHMW 3 - Answersbrahim.safa2018No ratings yet

- 7 16 10TheWrongDebateDocument3 pages7 16 10TheWrongDebaterichardck30No ratings yet

- Empirical Results: 1.1 Data OverviewDocument11 pagesEmpirical Results: 1.1 Data Overviewapi-444401653No ratings yet

- The Non-Deliverable Forward (NDF) Market For The Indian RupeeDocument9 pagesThe Non-Deliverable Forward (NDF) Market For The Indian RupeeandrewpereiraNo ratings yet

- Lmo Io 390 A1a6Document407 pagesLmo Io 390 A1a6Daniel MkandawireNo ratings yet

- Governors Third Quarter Media Brief 2008Document16 pagesGovernors Third Quarter Media Brief 2008Chola MukangaNo ratings yet

- Forex Good PDFDocument80 pagesForex Good PDFsudheeraryaNo ratings yet

- Defiance Cap - The Week That Just Passed Mar 19, 2010Document6 pagesDefiance Cap - The Week That Just Passed Mar 19, 2010WallstreetableNo ratings yet

- Pirates of The ComexDocument10 pagesPirates of The Comexgaoup100% (1)

- Hex 3Document123 pagesHex 3CatastrioNo ratings yet

- Car ShowroomDocument20 pagesCar ShowroomDanish ShakeelNo ratings yet

- ACFrOgAaY3q8hxmvSYm2VdzJeC0r D-KNsXYeGg81Mss12NUcOa9 TC4RZ3hmcYBqG1uY6Hc1Aw4Fd Kwa2bnYfc0oc1nAoGZu4PuPA4in3 ZI EpMq7zImn5jyx9uE VgnCHiXlnlVKV9qeIE3ADocument51 pagesACFrOgAaY3q8hxmvSYm2VdzJeC0r D-KNsXYeGg81Mss12NUcOa9 TC4RZ3hmcYBqG1uY6Hc1Aw4Fd Kwa2bnYfc0oc1nAoGZu4PuPA4in3 ZI EpMq7zImn5jyx9uE VgnCHiXlnlVKV9qeIE3Asergiu petreaNo ratings yet

- Self Unit Commitment To Centralized Unit CommitmentDocument28 pagesSelf Unit Commitment To Centralized Unit CommitmenteinerNo ratings yet

- Mortgage Risk On The RiseDocument2 pagesMortgage Risk On The RiseCreditTraderNo ratings yet

- 19336888, Chan Ken WaiDocument68 pages19336888, Chan Ken WaiFarhana MizaNo ratings yet

- The Week That Just Passed March 12, 2010Document4 pagesThe Week That Just Passed March 12, 2010WallstreetableNo ratings yet

- Darren Weekly Report 47Document6 pagesDarren Weekly Report 47DarrenNo ratings yet

- The Power of The Royalty Business Model: Gold vs. Gold Miners vs. Franco NevadaDocument7 pagesThe Power of The Royalty Business Model: Gold vs. Gold Miners vs. Franco NevadaTodd SullivanNo ratings yet

- SM - New YearDocument2 pagesSM - New YearJohn Paul GroomNo ratings yet

- Air MinumDocument4 pagesAir MinumNabila Maulidina WidyarahmahNo ratings yet

- Pack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersFrom EverandPack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersNo ratings yet

- Week 4.2 - Writing MinutesDocument7 pagesWeek 4.2 - Writing MinutesQuỳnh Linh NgôNo ratings yet

- Present Value FactorDocument1 pagePresent Value FactorQuỳnh Linh NgôNo ratings yet

- Present Value FactorDocument1 pagePresent Value FactorQuỳnh Linh NgôNo ratings yet

- Reading 2 Alaska Is Melting!Document2 pagesReading 2 Alaska Is Melting!Quỳnh Linh NgôNo ratings yet

- Effective Interest RatesDocument2 pagesEffective Interest RatesZaid Tariq AlabiryNo ratings yet

- Macroeconomic Aims and Policies and Trade 5 June 2012 (Students)Document21 pagesMacroeconomic Aims and Policies and Trade 5 June 2012 (Students)ragul96No ratings yet

- Chapter 7 - International Arbitrage and IRPDocument30 pagesChapter 7 - International Arbitrage and IRPPháp NguyễnNo ratings yet

- L3 Essay Institutional Investors QuestionsDocument7 pagesL3 Essay Institutional Investors QuestionsBero TapoleroNo ratings yet

- Blades Case StudyDocument3 pagesBlades Case StudyKhánh LoanNo ratings yet

- Ray Dalio - The CycleDocument20 pagesRay Dalio - The CyclePhương LộcNo ratings yet

- Greed IS Back: Business With PersonalityDocument36 pagesGreed IS Back: Business With PersonalityCity A.M.No ratings yet

- NYSERDA AnalysisDocument145 pagesNYSERDA AnalysisNick PopeNo ratings yet

- Term Paper - CB 604 - Section A - Financial Institutions and MarketsDocument22 pagesTerm Paper - CB 604 - Section A - Financial Institutions and MarketsISTIAK Mahmud MitulNo ratings yet

- Prelim Math InveDocument2 pagesPrelim Math InveARON PAUL SAN MIGUELNo ratings yet

- Time Value of Money: Abm5 - Business FinanceDocument34 pagesTime Value of Money: Abm5 - Business FinanceBarbie BleuNo ratings yet

- The Effect of Selected Macro-Economic Variables On The Performance of Smes in Kebbi StateDocument15 pagesThe Effect of Selected Macro-Economic Variables On The Performance of Smes in Kebbi StatesonyNo ratings yet

- Financial Management Theory and Practice 3rd Edition Brigham Solutions ManualDocument21 pagesFinancial Management Theory and Practice 3rd Edition Brigham Solutions ManualIanGaymkaf100% (57)

- GRADE 11 BUSINESS MATH (Gross and Net Earning)Document7 pagesGRADE 11 BUSINESS MATH (Gross and Net Earning)Jesmar SitaoNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelZayed BoodhooNo ratings yet

- Harshad Mehta Case StudyDocument12 pagesHarshad Mehta Case Studysimran agarwalNo ratings yet

- Chapter 2 - Determinants of Interest RatesDocument36 pagesChapter 2 - Determinants of Interest RatesMai Lan AnhNo ratings yet

- How To Get Collateral Free Business Loan Under CGTMSE SchemeDocument6 pagesHow To Get Collateral Free Business Loan Under CGTMSE Schemeshweta guptaNo ratings yet

- 99Document14 pages99gb_shaik03No ratings yet

- CFPB Discount Points Guidence PDFDocument3 pagesCFPB Discount Points Guidence PDFdzabranNo ratings yet

- FR ACCA Test FullDocument16 pagesFR ACCA Test Fullduducchi2308No ratings yet

- Test Bank With Answers Intermediate Accounting 12e by Kieso Chapter 14Document36 pagesTest Bank With Answers Intermediate Accounting 12e by Kieso Chapter 14Nicolas ErnestoNo ratings yet

- Lecture 6 - Interest Rates and Bond ValuationDocument56 pagesLecture 6 - Interest Rates and Bond Valuationabubaker janiNo ratings yet

- Chap 008Document6 pagesChap 008Haris JavedNo ratings yet

- R.P 32, 2018Document25 pagesR.P 32, 2018sajid bhattiNo ratings yet

- International Business The Challenges of Globalization 8th Edition Wild Solutions ManualDocument17 pagesInternational Business The Challenges of Globalization 8th Edition Wild Solutions Manualalanfideliaabxk100% (31)

- Ps Na Bago Sa ECONDocument10 pagesPs Na Bago Sa ECONJonelou CusipagNo ratings yet

- BP2BT, FLPP, SSB ComparisonsDocument12 pagesBP2BT, FLPP, SSB ComparisonsTawakkalNo ratings yet