You might also like

- Marketing Plan - Grab Philippines v1Document63 pagesMarketing Plan - Grab Philippines v1Panaguiton Marix83% (6)

- Project Report On Ginger and Garlic PasteDocument8 pagesProject Report On Ginger and Garlic PasteEIRI Board of Consultants and PublishersNo ratings yet

- The Progressive Era WorksheetDocument3 pagesThe Progressive Era Worksheetapi-298884028No ratings yet

- Market-Report-31 01 19Document3 pagesMarket-Report-31 01 19VinayNo ratings yet

- PEANUT MARKETING NEWS - May 13, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - May 13, 2020 - Tyron Spearman, EditorBrittany EtheridgeNo ratings yet

- PEANUT MARKETING NEWS - May 11, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - May 11, 2020 - Tyron Spearman, EditorBrittany EtheridgeNo ratings yet

- PEANUT MARKETING NEWS - November 13, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - November 13, 2020 - Tyron Spearman, EditorMorgan IngramNo ratings yet

- Shelled MKT Price: Market Loan Weekly PricesDocument1 pageShelled MKT Price: Market Loan Weekly PricesMorgan IngramNo ratings yet

- 09 135 20Document1 page09 135 20Morgan IngramNo ratings yet

- 30 Sfu 07 24 19Document8 pages30 Sfu 07 24 19nwberryfoundationNo ratings yet

- Shelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.4ct/lbDocument1 pageShelled MKT Price Weekly Prices: Same As Last Week 7-08-2021 (2020 Crop) 3,318,000 Tons, Up 8.2 % DOWN - $0.4ct/lbBrittany EtheridgeNo ratings yet

- Market Loan Weekly Prices: Shelled MKT PriceDocument1 pageMarket Loan Weekly Prices: Shelled MKT PriceMorgan IngramNo ratings yet

- Shelled MKT Price: Market Loan Weekly PricesDocument1 pageShelled MKT Price: Market Loan Weekly PricesMorgan IngramNo ratings yet

- Automated Day BookDocument13 pagesAutomated Day BookSamsul AlamNo ratings yet

- Basti Malook CC Ledger 18-19Document1 pageBasti Malook CC Ledger 18-19Zaki NiaziNo ratings yet

- Intraday Volatility Futures - Last Week: Corn/Maize MATIF (EUR/TON) Milling Wheat MATIF (EUR/TON)Document2 pagesIntraday Volatility Futures - Last Week: Corn/Maize MATIF (EUR/TON) Milling Wheat MATIF (EUR/TON)Luis Manuel Dias NunesNo ratings yet

- Argentine Dry Bean Harvest Trade Mission Report 2019Document33 pagesArgentine Dry Bean Harvest Trade Mission Report 2019Hariadi LaksamanaNo ratings yet

- PEANUT MARKETING NEWS - November 30, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - November 30, 2020 - Tyron Spearman, EditorMorgan IngramNo ratings yet

- CFRI T2 12 2019 ExaDocument66 pagesCFRI T2 12 2019 ExafernandocfreitasNo ratings yet

- Shelled MKT Price Market Loan Weekly Prices: F Om USDA Each Tuesday at 3 PM, Average Prices (USDA)Document1 pageShelled MKT Price Market Loan Weekly Prices: F Om USDA Each Tuesday at 3 PM, Average Prices (USDA)Brittany EtheridgeNo ratings yet

- PEANUT MARKETING NEWS - April 16, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - April 16, 2020 - Tyron Spearman, EditorBrittany EtheridgeNo ratings yet

- Lap - Pelayanan KefarmasianDocument9 pagesLap - Pelayanan KefarmasianviviNo ratings yet

- PEANUT MARKETING NEWS - April 2, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - April 2, 2020 - Tyron Spearman, EditorBrittany EtheridgeNo ratings yet

- 4 40 20 PDFDocument1 page4 40 20 PDFBrittany EtheridgeNo ratings yet

- Exercise 07Document7 pagesExercise 07Samaí PachecoNo ratings yet

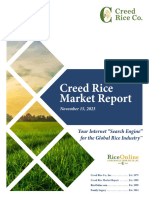

- Creed Rice Market Report, November 15, 2023Document13 pagesCreed Rice Market Report, November 15, 2023asociacion de caficultores de la amazonia peruanaNo ratings yet

- Hyak Graphs P06 WCDocument70 pagesHyak Graphs P06 WCJennifer BaxterNo ratings yet

- 4 51 20 PDFDocument1 page4 51 20 PDFBrittany EtheridgeNo ratings yet

- Feedgrains July 28Document2 pagesFeedgrains July 28Abbas AL-AghaNo ratings yet

- Vietnam Coffee USDA - Nov.2020Document6 pagesVietnam Coffee USDA - Nov.2020rGb111No ratings yet

- National Apple Processing Report: 2016 CropDocument5 pagesNational Apple Processing Report: 2016 CropmealysrNo ratings yet

- 613 WRITING TASK 1 Complex SentenceDocument9 pages613 WRITING TASK 1 Complex SentenceNhiNo ratings yet

- Could We See $2 Gas in Europe in 2020?: October 2019Document6 pagesCould We See $2 Gas in Europe in 2020?: October 2019IkhsanSolikhuddinNo ratings yet

- PEANUT MARKETING NEWS - September 23, 2020 - Tyron Spearman, EditorDocument1 pagePEANUT MARKETING NEWS - September 23, 2020 - Tyron Spearman, EditorMorgan IngramNo ratings yet

- Gilt Week Ahead 20230306Document4 pagesGilt Week Ahead 20230306asdf23No ratings yet

- Weekly Recap Jan 15Document1 pageWeekly Recap Jan 15Daviduta IonutNo ratings yet

- Major 20 and 20 Crops 20 Bulletin 202022Document38 pagesMajor 20 and 20 Crops 20 Bulletin 202022KC De CastroNo ratings yet

- Current Account Statement - 26022019Document4 pagesCurrent Account Statement - 26022019Adriana MicuNo ratings yet

- Sadaf JulyDocument2 pagesSadaf JulyMilo MileNo ratings yet

- Grain and Feed Annual - Hanoi - Vietnam - VM2023-0019Document24 pagesGrain and Feed Annual - Hanoi - Vietnam - VM2023-0019Chin YeeNo ratings yet

- Sadat JulyDocument2 pagesSadat JulyMilo MileNo ratings yet

- Practice Exercises 5 7 Arithmetic Operations W InstructionsDocument10 pagesPractice Exercises 5 7 Arithmetic Operations W InstructionsKurt BongolNo ratings yet

- Apexindo Pratama Duta TBK Apex: Company History Dividend AnnouncementDocument3 pagesApexindo Pratama Duta TBK Apex: Company History Dividend AnnouncementJandri Zhen TomasoaNo ratings yet

- Fallow Not Planted Not Planted: Chilly: 2316 Plants Capsicum: 654 Plants Cabbage: 2076 Plants Brinjal: 1678 PlantsDocument7 pagesFallow Not Planted Not Planted: Chilly: 2316 Plants Capsicum: 654 Plants Cabbage: 2076 Plants Brinjal: 1678 Plantsarg3112No ratings yet

- Cable - 1978MOSCOW31709 - D UKRAINE 1978 AGRICULTURAL RESULTS AND PLANS SUPPLEMENTDocument1 pageCable - 1978MOSCOW31709 - D UKRAINE 1978 AGRICULTURAL RESULTS AND PLANS SUPPLEMENTAntonette CabioNo ratings yet

- Nota Galon IT T2019Document11 pagesNota Galon IT T2019WaisNo ratings yet

- Shelled MKT Price Market Loan Weekly Prices: Same As Last WeekDocument1 pageShelled MKT Price Market Loan Weekly Prices: Same As Last WeekBrittany EtheridgeNo ratings yet

- The Cash BookDocument4 pagesThe Cash BookIsabella Navarro PaezNo ratings yet

- 05-55-19 PMNDocument1 page05-55-19 PMNBrittany EtheridgeNo ratings yet

- Major20and20Crops20Bulletin20July-September 2022Document40 pagesMajor20and20Crops20Bulletin20July-September 2022KC De CastroNo ratings yet

- Shelled MKT Price Weekly Prices: Same As Last Week 4-23-2021 (2020 Crop) 3,107,188 3,067,168 Tons DOWN $0.4 CT/LBDocument1 pageShelled MKT Price Weekly Prices: Same As Last Week 4-23-2021 (2020 Crop) 3,107,188 3,067,168 Tons DOWN $0.4 CT/LBMorgan IngramNo ratings yet

- Coffee StatisticsDocument8 pagesCoffee StatisticsMohammed Saber Ibrahim Ramadan ITL World KSANo ratings yet

- Major Non-Food and Industrial Crops Quarterly Bulletin For The First Quarter of 2021 - 0Document36 pagesMajor Non-Food and Industrial Crops Quarterly Bulletin For The First Quarter of 2021 - 0Dead LeafNo ratings yet

- Tugas 1 (IDX)Document42 pagesTugas 1 (IDX)Sintya AgustinaNo ratings yet

- EXPENSES (DAY1) - FEBRUARY 18, 2019: 02/18/19 San Roque Supermaket RetailDocument5 pagesEXPENSES (DAY1) - FEBRUARY 18, 2019: 02/18/19 San Roque Supermaket RetailLouiegie Thomas San JuanNo ratings yet

- WALMART Visit Us at Management - UmakantDocument54 pagesWALMART Visit Us at Management - Umakantwelcome2jungleNo ratings yet

- GaCC Rapportage 2008Document4 pagesGaCC Rapportage 2008Stichting Oud in Afrika (Old in Africa Foundation)No ratings yet

- Serial No Memo-Number Memo Date Document Number DCC Serial No Document Rev NoDocument3 pagesSerial No Memo-Number Memo Date Document Number DCC Serial No Document Rev Nojilani2No ratings yet

- The Winter Market Gardener: A Successful Grower's Handbook for Year-Round HarvestsFrom EverandThe Winter Market Gardener: A Successful Grower's Handbook for Year-Round HarvestsRating: 5 out of 5 stars5/5 (1)

- Japan's Big Bang: The Deregulation and Revitalization of the Japanese EconomyFrom EverandJapan's Big Bang: The Deregulation and Revitalization of the Japanese EconomyNo ratings yet

- Open-Economy Politics: The Political Economy of the World Coffee TradeFrom EverandOpen-Economy Politics: The Political Economy of the World Coffee TradeRating: 2.5 out of 5 stars2.5/5 (1)

- Partnership Proposal 1,5 MilyarDocument31 pagesPartnership Proposal 1,5 MilyarPrasetyoWaskitoNo ratings yet

- PolicySchedule 1101815120220607 154054Document2 pagesPolicySchedule 1101815120220607 154054Suhi SuhelNo ratings yet

- Disequilibrium in Balance of PaymentDocument6 pagesDisequilibrium in Balance of PaymentIshant MishraNo ratings yet

- Bangladesh Army University of Science and Technology Bachelor of Business Administration (BBA)Document4 pagesBangladesh Army University of Science and Technology Bachelor of Business Administration (BBA)Shahadat Hossain SourovNo ratings yet

- IAS 16 PPE Lecture Slides (Updated)Document39 pagesIAS 16 PPE Lecture Slides (Updated)Ndila mangalisoNo ratings yet

- Public Administration Objective Questions Part 1Document24 pagesPublic Administration Objective Questions Part 1M AbbasNo ratings yet

- Chapter 1. Hoshin Kanri Basics. Nested Experiments, Xmatrix and Chartering Teams PDFDocument20 pagesChapter 1. Hoshin Kanri Basics. Nested Experiments, Xmatrix and Chartering Teams PDFAntoniojuarezjuarezNo ratings yet

- Eb183013 Final ReportDocument54 pagesEb183013 Final ReportAbrar Alam ChowdhuryNo ratings yet

- Rentomojo ProjectDocument7 pagesRentomojo ProjectShweta SinhaNo ratings yet

- Pas 16 Property, Plant, and Equipment: PART 1: Nature and Initial Measurement of PPE Nature and DefinitionDocument8 pagesPas 16 Property, Plant, and Equipment: PART 1: Nature and Initial Measurement of PPE Nature and DefinitionBrian Daniel BayotNo ratings yet

- Application of ManagementDocument2 pagesApplication of ManagementM Chandraman ECE KIOTNo ratings yet

- Worksheet 5Document14 pagesWorksheet 5HiraiNo ratings yet

- Certificate of Abandonment Business NameDocument1 pageCertificate of Abandonment Business NameGryswolfNo ratings yet

- Landbank Customer Information Sheet CorporationDocument6 pagesLandbank Customer Information Sheet CorporationMayNo ratings yet

- The Champion Legal Ads: 03-30-23Document49 pagesThe Champion Legal Ads: 03-30-23Donna S. SeayNo ratings yet

- The Influence of Perceived Entrepreneurship Education On InnovationDocument7 pagesThe Influence of Perceived Entrepreneurship Education On InnovationArafatNo ratings yet

- Far 340: Financial Analysis Statement Petronas Gas BerhadDocument26 pagesFar 340: Financial Analysis Statement Petronas Gas BerhadaishahNo ratings yet

- Unileiver Polka MergerDocument1 pageUnileiver Polka MergerMuhammad_Khan_5185No ratings yet

- Saad Statement BobDocument3 pagesSaad Statement BobAmisha SinghNo ratings yet

- Establishing Man Machine RatioDocument5 pagesEstablishing Man Machine RatioMadeleine Jennifer AyosoNo ratings yet

- Sustainability 12 10691 v2Document30 pagesSustainability 12 10691 v2knwongabNo ratings yet

- SAP PP Training Tutorial - Learn SAP Production Planning ModuleDocument3 pagesSAP PP Training Tutorial - Learn SAP Production Planning ModuleShrouk GamalNo ratings yet

- Secret Recipe Case Study MalaysiaDocument2 pagesSecret Recipe Case Study MalaysiaPradeepRathiNo ratings yet

- Critical Evaluation of DELLDocument9 pagesCritical Evaluation of DELLAneelaMalikNo ratings yet

- SDG GOAL 9: Industry, Innovation and Infrastructure: Mec600 - Engineer in SocietyDocument9 pagesSDG GOAL 9: Industry, Innovation and Infrastructure: Mec600 - Engineer in SocietydasdasdNo ratings yet

- Lifelines of EconomyDocument8 pagesLifelines of EconomytanishqNo ratings yet

- Name and Address of The ApplicantDocument2 pagesName and Address of The ApplicantAbbas AliNo ratings yet