You might also like

- Assignment Money Cash Flow Inc Group 21,23,27,30Document3 pagesAssignment Money Cash Flow Inc Group 21,23,27,30Karan Vashee100% (3)

- Question 1 & 2Document8 pagesQuestion 1 & 2Joel SamuelNo ratings yet

- It AuditDocument73 pagesIt AuditRudi Kurniawan100% (1)

- Provident Fund Full DetailsDocument5 pagesProvident Fund Full DetailsGaurav VijayNo ratings yet

- Surah Nas Tafsir Al-Mizan - An Exegesis of The Holy Quran by The Late Allamah Muhammad Hussain TabatabaiDocument6 pagesSurah Nas Tafsir Al-Mizan - An Exegesis of The Holy Quran by The Late Allamah Muhammad Hussain TabatabaiSyed Xishaan MosavieNo ratings yet

- 4 - Step Case Studies of Shyam Edlabadkar Sir 1-50 PDFDocument102 pages4 - Step Case Studies of Shyam Edlabadkar Sir 1-50 PDFavidmasterNo ratings yet

- Self EfficayDocument6 pagesSelf EfficayAmandeep Singh MankuNo ratings yet

- Employee TurnoverDocument20 pagesEmployee Turnoversneha fabeyNo ratings yet

- Crosstabs OutputDocument11 pagesCrosstabs OutputsaherrashidkamalNo ratings yet

- Limpieza de DatosDocument18 pagesLimpieza de DatosMarisol CantareroNo ratings yet

- ML Assignment 01Document1 pageML Assignment 01duawajih02No ratings yet

- KatuwalDocument20 pagesKatuwalignacioNo ratings yet

- MODULE 5 Discrete DistributionDocument16 pagesMODULE 5 Discrete DistributionMariel CadayonaNo ratings yet

- OR MerckDocument10 pagesOR MerckSaumya SahaNo ratings yet

- Project - Management (Bangio TT)Document19 pagesProject - Management (Bangio TT)Mitali BiswasNo ratings yet

- Finance For ManagersDocument17 pagesFinance For ManagersIkramNo ratings yet

- Certificate of Completion: This Is To Certify That Has Completed The Course/examDocument3 pagesCertificate of Completion: This Is To Certify That Has Completed The Course/examShowkatul IslamNo ratings yet

- Multi Reglog 2Document6 pagesMulti Reglog 2niasakiNo ratings yet

- Dispersion and Alpha Conversion: Counterpoint Global InsightsDocument17 pagesDispersion and Alpha Conversion: Counterpoint Global Insightsvalueinvestor123No ratings yet

- Presentation 2Document27 pagesPresentation 2Henok AsemahugnNo ratings yet

- CMPEDA Project: Lending Club Loan Data PredictionDocument7 pagesCMPEDA Project: Lending Club Loan Data PredictionFacundo RoncagliaNo ratings yet

- Oneway: NotesDocument16 pagesOneway: NotesM RofiqNo ratings yet

- Assignment 1Document4 pagesAssignment 1katelyntitus9No ratings yet

- 6 Figure Trading Plan Excel SheetDocument10 pages6 Figure Trading Plan Excel Sheetadesiyan promiseNo ratings yet

- CHPT 6 - Incentive and Compensation System Maf651Document96 pagesCHPT 6 - Incentive and Compensation System Maf651Angel Pria David LunchaNo ratings yet

- Labor Session2 Final-1Document80 pagesLabor Session2 Final-1Brian ObieroNo ratings yet

- Risk Profile: UTILIDAD ESPERADA (2.5) 2900 27.3312Document3 pagesRisk Profile: UTILIDAD ESPERADA (2.5) 2900 27.3312César VallejoNo ratings yet

- Percentage Conversion Worksheet PDFDocument2 pagesPercentage Conversion Worksheet PDFJamie LeeNo ratings yet

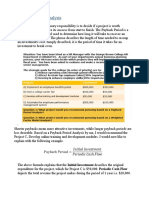

- Payback Period AnalysisDocument2 pagesPayback Period AnalysisMr. MaverickNo ratings yet

- Pengaruh Kepemimpinan, Budaya Organisasi Dan Motivasi Terhadap Kepuasan Kerja Pegawai Pada Satuan Kerja Perangkat Daerah Pemerintah Kabupaten MarosDocument6 pagesPengaruh Kepemimpinan, Budaya Organisasi Dan Motivasi Terhadap Kepuasan Kerja Pegawai Pada Satuan Kerja Perangkat Daerah Pemerintah Kabupaten MarosPutra Muhammaad Al FatihNo ratings yet

- Building A Compensation Plan Part 3: Implementing The Total Rewards PlanDocument17 pagesBuilding A Compensation Plan Part 3: Implementing The Total Rewards PlanIva NedeljkovicNo ratings yet

- Math Percent 2Document2 pagesMath Percent 2Kevin LiNo ratings yet

- Demand Forecasting by Alcance Lou Gene ManuelDocument21 pagesDemand Forecasting by Alcance Lou Gene ManuelIvy Joy JamiliNo ratings yet

- 73 75Document4 pages73 75Rifa AlfiandiNo ratings yet

- Using Data to Make Effective DecisionsDocument60 pagesUsing Data to Make Effective DecisionsSAVALI HELSHAMNo ratings yet

- IET 104 - Industrial Management Seminars Fall 2020 - Assessment 5Document5 pagesIET 104 - Industrial Management Seminars Fall 2020 - Assessment 5Shehab AshrafNo ratings yet

- Unit 13 Design of Perfomance Linked Reward System: ObjectivesDocument15 pagesUnit 13 Design of Perfomance Linked Reward System: ObjectivesRaveena SharmaNo ratings yet

- Designing Performance-Linked Reward SystemsDocument27 pagesDesigning Performance-Linked Reward Systemsपशुपति नाथNo ratings yet

- Regression BasicsDocument19 pagesRegression BasicssanjayshahdevNo ratings yet

- Sol 2.1 Custom Config changes HDR multiplier and AEDocument7 pagesSol 2.1 Custom Config changes HDR multiplier and AEDolby MovieNo ratings yet

- Business ModelDocument15 pagesBusiness ModelKrutagna KadiaNo ratings yet

- CS507 Assignment No. 02 Covers Lectures 8-15Document4 pagesCS507 Assignment No. 02 Covers Lectures 8-15UmairAfzalNo ratings yet

- SsreportccDocument5 pagesSsreportccapi-459396591No ratings yet

- Banking SectorDocument14 pagesBanking SectorMAYERANo ratings yet

- Scoring: Table 1. Item Numbers For Each SubscaleDocument2 pagesScoring: Table 1. Item Numbers For Each SubscaleBellNo ratings yet

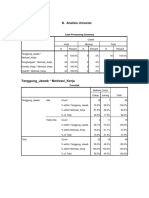

- Tanggung - Jawab Motivasi - Kerja: B. Analisis UnivariatDocument5 pagesTanggung - Jawab Motivasi - Kerja: B. Analisis UnivariatAbdi PalualaNo ratings yet

- 1.2 Research Problem: "What Are The Factors Which Help To Motivate The Employees?Document10 pages1.2 Research Problem: "What Are The Factors Which Help To Motivate The Employees?syedsiddiqNo ratings yet

- BMS Ni AziDocument5 pagesBMS Ni AziSymphony of HeartsNo ratings yet

- Altman's Z-ScoreDocument15 pagesAltman's Z-ScoreVipul BhagatNo ratings yet

- Add PPT For Financial Statement AnalysisDocument27 pagesAdd PPT For Financial Statement AnalysisBCC 27 AccountNo ratings yet

- Job Evaluation: Cherlyn Ann M. Nablo, RPM HR Officer-In-Charge Ace Baypointe HospitalDocument27 pagesJob Evaluation: Cherlyn Ann M. Nablo, RPM HR Officer-In-Charge Ace Baypointe Hospitalluzille anne alerta100% (1)

- Sun Pharmaceutical IndustriesDocument2 pagesSun Pharmaceutical Industriessharmasumeet1987No ratings yet

- MTP Oct. 2018 FM and Eco AnswerDocument16 pagesMTP Oct. 2018 FM and Eco AnswerAisha MalhotraNo ratings yet

- CFRA_Vol_2_2014_15Document4 pagesCFRA_Vol_2_2014_15tNo ratings yet

- Impact of Employee Participation On Job SatisfactionDocument22 pagesImpact of Employee Participation On Job Satisfactionkomal khalid100% (1)

- HW ExplanationDocument20 pagesHW ExplanationMysara MunneeNo ratings yet

- Univariat Uas WordDocument13 pagesUnivariat Uas WordElfida NabillahNo ratings yet

- 1 - Laporan Tahunan 2022 11Document1 page1 - Laporan Tahunan 2022 11Lowongan PekerjaanNo ratings yet

- Descriptive statistics and reliability of aggression and suicide scalesDocument5 pagesDescriptive statistics and reliability of aggression and suicide scalesFercho CastilloNo ratings yet

- Application Week2: Costs and BenefitsDocument6 pagesApplication Week2: Costs and BenefitsWilsonbvNo ratings yet

- Financial Literacy Affects The Financial ManagementDocument11 pagesFinancial Literacy Affects The Financial ManagementAin AdikoNo ratings yet

- PA Lab 4Document6 pagesPA Lab 4syedkashif047No ratings yet

- The Influence of Job Stress, Organizational Climate and Job Environment On Employee Turnover IntentionDocument8 pagesThe Influence of Job Stress, Organizational Climate and Job Environment On Employee Turnover IntentionIjbmm JournalNo ratings yet

- Sammy The Brave The Adventure To Find The Magic ChestDocument2 pagesSammy The Brave The Adventure To Find The Magic ChestAmandeep Singh MankuNo ratings yet

- Ethics E-LEARNING 25.03.19 PDFDocument5 pagesEthics E-LEARNING 25.03.19 PDFANITHA SNo ratings yet

- Job - DemographicDocument6 pagesJob - DemographicAmandeep Singh MankuNo ratings yet

- Gender Differences PDFDocument27 pagesGender Differences PDFAmandeep Singh MankuNo ratings yet

- Self DemographicDocument6 pagesSelf DemographicAmandeep Singh MankuNo ratings yet

- Job Involvement Predicted by Self-EfficacyDocument4 pagesJob Involvement Predicted by Self-EfficacyAmandeep Singh MankuNo ratings yet

- 11 Auditing EMDocument120 pages11 Auditing EMAmandeep Singh MankuNo ratings yet

- 30 Due Date Chart of All Satuatory PaymentDocument1 page30 Due Date Chart of All Satuatory PaymentAmandeep Singh MankuNo ratings yet

- Paper 11 NEW GST PDFDocument399 pagesPaper 11 NEW GST PDFsomaanvithaNo ratings yet

- Letter ADocument26 pagesLetter AAmandeep Singh MankuNo ratings yet

- (Walter Crane) Floral Fantasy PDFDocument58 pages(Walter Crane) Floral Fantasy PDFMarleneDietrichNo ratings yet

- Financial ServicesDocument12 pagesFinancial ServicesAmandeep Singh MankuNo ratings yet

- Salary SheetDocument229 pagesSalary SheetAmandeep Singh MankuNo ratings yet

- Receivable ManagementDocument4 pagesReceivable ManagementAmandeep Singh MankuNo ratings yet

- Everyday YesDocument97 pagesEveryday YesAmandeep Singh Manku100% (1)

- Company fixed asset registerDocument2 pagesCompany fixed asset registerAmandeep Singh Manku100% (1)

- Operation ResearchDocument26 pagesOperation ResearchAmandeep Singh MankuNo ratings yet

- Drilbits International Private Limited Balance Sheet As at 31St March, 2008Document39 pagesDrilbits International Private Limited Balance Sheet As at 31St March, 2008Sushrutt S. AlekarNo ratings yet

- 44 Depreciation ScheduleDocument6 pages44 Depreciation ScheduleAmandeep Singh MankuNo ratings yet

- Booklet EnglishDocument10 pagesBooklet Englishabhyuday97No ratings yet

- CAPM Model Explained: Risk and Return RelationshipDocument2 pagesCAPM Model Explained: Risk and Return RelationshipAmandeep Singh MankuNo ratings yet

- Essential English words for understanding and memorizationDocument23 pagesEssential English words for understanding and memorizationAmandeep Singh MankuNo ratings yet

- 1 Excel DictioneryDocument207 pages1 Excel Dictionerysomnathsingh_hydNo ratings yet

- LEttersDocument5 pagesLEttersAmandeep Singh MankuNo ratings yet

- Regular and Irregular VerbDocument4 pagesRegular and Irregular VerbAmandeep Singh MankuNo ratings yet

- B) Price Elasticity of SupplyDocument3 pagesB) Price Elasticity of SupplyAmandeep Singh MankuNo ratings yet

- The Case For AntiGravity-bookletDocument48 pagesThe Case For AntiGravity-bookletJerry DoughertyNo ratings yet

- Grade 2 Reading RubricDocument3 pagesGrade 2 Reading Rubricanurag_kapila3901100% (3)

- Food of The Future TFK Lesson and ReflectionDocument2 pagesFood of The Future TFK Lesson and Reflectionapi-307027477No ratings yet

- Computational MHDDocument66 pagesComputational MHDverthex20992828No ratings yet

- CV - Mohammadan Adilla AdzanysDocument8 pagesCV - Mohammadan Adilla Adzanystonyoibenuaq100% (1)

- The Vehicle Steer by Wire Control System by Implementing PID ControllerDocument5 pagesThe Vehicle Steer by Wire Control System by Implementing PID ControllerdashNo ratings yet

- HQE2R Diagnostics & PrioritésDocument205 pagesHQE2R Diagnostics & PrioritéssusCitiesNo ratings yet

- Amadeus Cho: Hypercomputer HeroDocument3 pagesAmadeus Cho: Hypercomputer HeroEnrique Fernandez TorreblancaNo ratings yet

- Min Max HeapsDocument22 pagesMin Max HeapsyashikabirdiNo ratings yet

- SAP - SAPSCRIPT Made Easy - A Step-By-Step Guide To Form Design & Printout in R3Document298 pagesSAP - SAPSCRIPT Made Easy - A Step-By-Step Guide To Form Design & Printout in R3Alina Alex100% (3)

- Sand Dune Video Prediction Using CNNsDocument1 pageSand Dune Video Prediction Using CNNsJeffersson Ramos CamposNo ratings yet

- Liderança - PNL - Anthony Robbins - Coaching PDFDocument12 pagesLiderança - PNL - Anthony Robbins - Coaching PDFJefferson DalamuraNo ratings yet

- Full Download Introduction To Criminology 3rd Edition Walsh Test BankDocument35 pagesFull Download Introduction To Criminology 3rd Edition Walsh Test Bankrosannpittervip100% (36)

- Summary of English Material Grade 12 2019Document28 pagesSummary of English Material Grade 12 2019heelrayhan photographyNo ratings yet

- Add Field in COOIS 2 SAPDocument12 pagesAdd Field in COOIS 2 SAPaprian100% (1)

- Astm 3441Document6 pagesAstm 3441Todor Ivanov YankovNo ratings yet

- SAP PP ConfigurationDocument25 pagesSAP PP ConfigurationRanjan100% (2)

- Student Placement DetailsDocument125 pagesStudent Placement DetailsAbhishekNo ratings yet

- English for Elementary StudentsDocument32 pagesEnglish for Elementary StudentsFajar RiyantoNo ratings yet

- Maths in Focus Chapter 11Document52 pagesMaths in Focus Chapter 11eccentricftw450% (2)

- Adjacent Precast Concrete Box Beam BridgesDocument86 pagesAdjacent Precast Concrete Box Beam BridgesSudathipTangwongchai100% (1)

- Classical Reports in Sap ABAPDocument14 pagesClassical Reports in Sap ABAPSaswat Raysamant0% (1)

- Class 10 Final PDFDocument10 pagesClass 10 Final PDFBhuvansh GoyalNo ratings yet

- Finite Element Analysis of Pressure VesselDocument9 pagesFinite Element Analysis of Pressure VesselSenguttuvan RaajaahNo ratings yet

- Atlas 2010: Rare Breeds and Varieties of GreeceDocument129 pagesAtlas 2010: Rare Breeds and Varieties of GreeceΧΑΡΗΣΚΑΛΟΓΕΡΟΠΟΥΛΟΣNo ratings yet

- Test 4: Mic Ho Use Agency - RepairsDocument4 pagesTest 4: Mic Ho Use Agency - Repairsandi ariNo ratings yet

- Project Report: The Measurement of Brand Awareness and Brand PerceptionDocument49 pagesProject Report: The Measurement of Brand Awareness and Brand PerceptionDark InstinctNo ratings yet

- Ladies and GentlemenDocument4 pagesLadies and GentlemenMARY JOY ANGGABOYNo ratings yet