You might also like

- Cost and Management Accounting Mid Term Exam: July, 2020 Time Allowed: 3 Hours & 15 MinutesDocument10 pagesCost and Management Accounting Mid Term Exam: July, 2020 Time Allowed: 3 Hours & 15 MinutesmaryNo ratings yet

- Working Capital QuestionsDocument10 pagesWorking Capital QuestionsVaishnavi VenkatesanNo ratings yet

- CHAPTER 13 Solved Problems PDFDocument8 pagesCHAPTER 13 Solved Problems PDF7100507100% (2)

- Arms Length PrincipleDocument18 pagesArms Length PrincipleMARY IRUNGUNo ratings yet

- Case Study - Fashion Forward Vs Dream DesignDocument6 pagesCase Study - Fashion Forward Vs Dream DesignmynalawalNo ratings yet

- Working cap-SEM IIIDocument9 pagesWorking cap-SEM IIIBhushan BhorkadeNo ratings yet

- Management Accounting: Final ExaminationsDocument4 pagesManagement Accounting: Final ExaminationsAbdulAzeemNo ratings yet

- Working Capital Management - NumericalsDocument9 pagesWorking Capital Management - NumericalsAnjali JainNo ratings yet

- Problems From Unit - 5Document8 pagesProblems From Unit - 5jeganrajraj0% (1)

- Working Capital Requirement QuestionsDocument2 pagesWorking Capital Requirement QuestionsVIRAL DOSHI100% (1)

- Assessment and Computation of Working Capital Requirements Numerical QuestionsDocument6 pagesAssessment and Computation of Working Capital Requirements Numerical QuestionsNazreena MukherjeeNo ratings yet

- Test 7 Budgeting TestDocument1 pageTest 7 Budgeting TestHaseeb AhmadNo ratings yet

- Sir Saud Tariq: 13 Important Revision Questions On Each TopicDocument29 pagesSir Saud Tariq: 13 Important Revision Questions On Each TopicShehrozST100% (1)

- Corporate Finance I176 Xid-3384732 1Document8 pagesCorporate Finance I176 Xid-3384732 1kashualNo ratings yet

- Problems On Working CapitalDocument2 pagesProblems On Working CapitalDeepakNo ratings yet

- Problems 1: Marginal Costing TechniqueDocument2 pagesProblems 1: Marginal Costing TechniqueRajesh GuptaNo ratings yet

- Business Budgets and Budgetary Control: Sma - AbsDocument4 pagesBusiness Budgets and Budgetary Control: Sma - AbsSai SumanNo ratings yet

- Unit 1 WCM (Practical Problem)Document3 pagesUnit 1 WCM (Practical Problem)niranjan balaramNo ratings yet

- Problems in WC EstimationDocument3 pagesProblems in WC EstimationaparnahawaldarNo ratings yet

- Working Capital NumericalsDocument3 pagesWorking Capital NumericalsShriya SajeevNo ratings yet

- Assignment ProblemsDocument5 pagesAssignment ProblemsRamesh SigdelNo ratings yet

- Past Paper December 2020Document8 pagesPast Paper December 2020Jean Damascene HakizimanaNo ratings yet

- Determine The Working Required To Finance A Level of Activity of 1,80,000/-Units of OutputDocument2 pagesDetermine The Working Required To Finance A Level of Activity of 1,80,000/-Units of OutputAkash KumarNo ratings yet

- ECON F315 - FIN F315 - Compre QP PDFDocument3 pagesECON F315 - FIN F315 - Compre QP PDFPrabhjeet Kalsi100% (1)

- FM 4Document4 pagesFM 4Elizabeth RayNo ratings yet

- GIFT - CAF 8 Master Questions With Solutions & Marks - Caf 8 Sir Saud Tariq ST AcademyDocument36 pagesGIFT - CAF 8 Master Questions With Solutions & Marks - Caf 8 Sir Saud Tariq ST AcademyShehrozSTNo ratings yet

- Working CapitalDocument2 pagesWorking Capitalk.hgjNo ratings yet

- BComDocument3 pagesBComChristy jamesNo ratings yet

- IV SEM - BA & BBA - Basics of Financial Management - 2021-22Document3 pagesIV SEM - BA & BBA - Basics of Financial Management - 2021-22Aria MazeNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementAnkit ThakkarNo ratings yet

- C.FM QDocument7 pagesC.FM QcawinnersofficialNo ratings yet

- Income Statement Numerical QuestionsDocument2 pagesIncome Statement Numerical QuestionsKBA AMIR100% (2)

- Working CapitalDocument12 pagesWorking CapitalYasin Misvari T MNo ratings yet

- WCM EstimationDocument3 pagesWCM Estimationtanya.p23No ratings yet

- Raw Material (5 Kgs @Rs.8) Rs.40 Direct Labour (2 Hours @Rs.5) 10 Variable Manufacturing Overheads 10 Fixed Manufacturing Overheads 20 Total 80Document1 pageRaw Material (5 Kgs @Rs.8) Rs.40 Direct Labour (2 Hours @Rs.5) 10 Variable Manufacturing Overheads 10 Fixed Manufacturing Overheads 20 Total 80arpit guptaNo ratings yet

- Working Capital QuizDocument3 pagesWorking Capital QuizHarshit GoyalNo ratings yet

- Corporate Finance - I748 - Xid-3956405 - 1Document2 pagesCorporate Finance - I748 - Xid-3956405 - 1kashualNo ratings yet

- WCM QuestionsDocument13 pagesWCM QuestionsALEEM MANSOORNo ratings yet

- BF U4 (WC) - 1 PDFDocument14 pagesBF U4 (WC) - 1 PDFjrkukrejatrw253No ratings yet

- Working Capital - PracticalDocument6 pagesWorking Capital - PracticalPiyush MalviyaNo ratings yet

- FM Revision Q BankDocument10 pagesFM Revision Q BankOmkar VaigankarNo ratings yet

- Part 1 - FM & ECO - 27145216 PDFDocument3 pagesPart 1 - FM & ECO - 27145216 PDFMaharajan GomuNo ratings yet

- Working Capital ManagementDocument16 pagesWorking Capital ManagementdhruvNo ratings yet

- Working Capital Sums 16Document21 pagesWorking Capital Sums 16Lakhan Sharma100% (1)

- QuestionsDocument2 pagesQuestionsSHREY ffNo ratings yet

- Budget Numerical PDFDocument5 pagesBudget Numerical PDFDilip BhusalNo ratings yet

- 1.0 Short-Term BudgetingDocument4 pages1.0 Short-Term BudgetingChristian Clyde Zacal ChingNo ratings yet

- Bcom (Em) Sem 5 - FM I - Examples of Estimating WC - Acc - 2324Document8 pagesBcom (Em) Sem 5 - FM I - Examples of Estimating WC - Acc - 2324Harsh RanaNo ratings yet

- Mock Exam MG T Acct 2019Document3 pagesMock Exam MG T Acct 2019Lê Việt HoàngNo ratings yet

- Mock Exam MGT Acct 2020Document3 pagesMock Exam MGT Acct 2020Lê Thu TràNo ratings yet

- Cost Sheet - Pages 16Document16 pagesCost Sheet - Pages 16omikron omNo ratings yet

- Working Capital AssignmentDocument3 pagesWorking Capital Assignmentrahulmehta1578No ratings yet

- FR (Old) MTP Compiler Past 8Document122 pagesFR (Old) MTP Compiler Past 8Pooja GuptaNo ratings yet

- FinMan Chapter 16 and 17 ProblemsDocument3 pagesFinMan Chapter 16 and 17 ProblemsJufel Ramirez100% (1)

- Final Examination (Summer-2020) : Shahzad ButtDocument4 pagesFinal Examination (Summer-2020) : Shahzad Buttali balochNo ratings yet

- For Fixation of Selling PriceDocument2 pagesFor Fixation of Selling PriceTejashree NirgudeNo ratings yet

- 06 - Working Capital Management ProblemsDocument4 pages06 - Working Capital Management ProblemsMerr Fe PainaganNo ratings yet

- Management Accounting Problem Unit 3Document17 pagesManagement Accounting Problem Unit 3princeNo ratings yet

- Working CapitalDocument9 pagesWorking CapitalLakshya AgrawalNo ratings yet

- ARM - CMA Mock March 2024 With SolutionDocument17 pagesARM - CMA Mock March 2024 With SolutionTooba MaqboolNo ratings yet

- 2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyFrom Everand2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyNo ratings yet

- Capital Expenditure DecisionsDocument2 pagesCapital Expenditure DecisionsSundarNo ratings yet

- Accounting Ratios For FSADocument4 pagesAccounting Ratios For FSASundarNo ratings yet

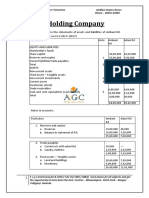

- Holding CompanyDocument3 pagesHolding CompanySundarNo ratings yet

- Aswina Mango From Malda Adv Booking OpenDocument3 pagesAswina Mango From Malda Adv Booking OpenSundarNo ratings yet

- LeverageDocument2 pagesLeverageSundarNo ratings yet

- Cost of CapitalDocument2 pagesCost of CapitalSundarNo ratings yet

- Qmin Kolkata Taj Bengal 2Document21 pagesQmin Kolkata Taj Bengal 2SundarNo ratings yet

- Financial Management SuggestionsDocument7 pagesFinancial Management SuggestionsSundarNo ratings yet

- FM Theory 2Document14 pagesFM Theory 2SundarNo ratings yet

- Last Time Tips by CA Ankit PatwariDocument41 pagesLast Time Tips by CA Ankit PatwariSundarNo ratings yet

- Fr&Fsa TheoryDocument30 pagesFr&Fsa TheorySundarNo ratings yet

- Sonimad Sawmill Inc Ssi Purchases Logs From Independent Timber ContractorsDocument2 pagesSonimad Sawmill Inc Ssi Purchases Logs From Independent Timber ContractorsAmit PandeyNo ratings yet

- Case Study 2. R.E. Construction: It's Now or NeverDocument2 pagesCase Study 2. R.E. Construction: It's Now or NeverClarence PascualNo ratings yet

- 1.44 22-10-2020 Revision of Fee To ArbitratorsDocument2 pages1.44 22-10-2020 Revision of Fee To ArbitratorsGuramrit Pal Singh BalNo ratings yet

- 00 CD VolumDocument331 pages00 CD Volumecocadec0% (1)

- Digital India: How Far Did Demonetization HelpDocument39 pagesDigital India: How Far Did Demonetization HelpSherin SunnyNo ratings yet

- Transaction Cycles and Accounting ApplicationsDocument35 pagesTransaction Cycles and Accounting ApplicationsSelamawit Taddesse100% (1)

- Curiculum Vitae: ExperienceDocument12 pagesCuriculum Vitae: ExperienceDesi Hendaryanie WiramiharjaNo ratings yet

- Service Agreement For Annual Physical ExamDocument9 pagesService Agreement For Annual Physical ExamJher BerNo ratings yet

- The Prince2 Foundation Examination: Sample Paper 1Document16 pagesThe Prince2 Foundation Examination: Sample Paper 1scorpionitinNo ratings yet

- Analisis Keberlanjutan Aksesibilitas Angkutan Umum Di Kota SukabumiDocument19 pagesAnalisis Keberlanjutan Aksesibilitas Angkutan Umum Di Kota Sukabumisahidan thoybahNo ratings yet

- JD For Marketing Manager - ICICI BankDocument1 pageJD For Marketing Manager - ICICI BankPrachi AroraNo ratings yet

- CompReg 14MARCH2020Document1,620 pagesCompReg 14MARCH2020GorrillaNo ratings yet

- Module # 2 Pricing StrategiesDocument13 pagesModule # 2 Pricing StrategiesgraceNo ratings yet

- Test Bank For International Financial Management 13th EditionDocument36 pagesTest Bank For International Financial Management 13th Editionancientypyemia1pxotk100% (48)

- Soal P 12 Tryout 1 AfterDocument13 pagesSoal P 12 Tryout 1 AfterintanNo ratings yet

- Terms and Conditions Current Account/Current Account-I or Savings Account/Savings Account-I (CASA/CASA-i) Double Cash Bonus Campaign 2.0Document12 pagesTerms and Conditions Current Account/Current Account-I or Savings Account/Savings Account-I (CASA/CASA-i) Double Cash Bonus Campaign 2.0mohd addinNo ratings yet

- RCBC Vs Royal Cargo DigestDocument2 pagesRCBC Vs Royal Cargo DigestJeremae Ann CeriacoNo ratings yet

- 2021 - MDS - Hillrom - Distributor Business Plan 2021 v1Document18 pages2021 - MDS - Hillrom - Distributor Business Plan 2021 v1Paweł GoławskiNo ratings yet

- After Effect of Corona Virus in Garments Industry PDFDocument9 pagesAfter Effect of Corona Virus in Garments Industry PDF360 degree TextileNo ratings yet

- Qaqr 3Document3 pagesQaqr 3Kadek Yuki AndikaNo ratings yet

- Unemployment AssignmentDocument3 pagesUnemployment AssignmentJaspreet SinghNo ratings yet

- Weekly Business Update - Business Development - 032519-032919Document26 pagesWeekly Business Update - Business Development - 032519-032919Nate TrinityNo ratings yet

- The Health and Growth Potential of The Steel Manufacturing Industries in SADocument94 pagesThe Health and Growth Potential of The Steel Manufacturing Industries in SAShumani PharamelaNo ratings yet

- Topic 3Document28 pagesTopic 3Learner's LicenseNo ratings yet

- Federal Budget FY2022-23 - 110622Document15 pagesFederal Budget FY2022-23 - 110622hatn1234No ratings yet

- 3 DLP Officers BOBDocument22 pages3 DLP Officers BOBopparasharNo ratings yet

- Allied BankDocument3 pagesAllied BankHamzaNo ratings yet

- Bukalapak Com TBK Bilingual Q1 2023 FinalDocument175 pagesBukalapak Com TBK Bilingual Q1 2023 FinalTappp - Elevate your networkingNo ratings yet