You might also like

- US Rice Supply and Use Tables 2013-2020Document12 pagesUS Rice Supply and Use Tables 2013-2020Akash NeupaneNo ratings yet

- Rice Outlook Monthly Tables November 2021Document13 pagesRice Outlook Monthly Tables November 2021jun njkNo ratings yet

- SAMAR Quickstat - January 2023Document4 pagesSAMAR Quickstat - January 2023Raymark LagrimasNo ratings yet

- Municipal Agriculture and Fisheries ProfileDocument10 pagesMunicipal Agriculture and Fisheries ProfilejaneNo ratings yet

- Maize January 2022Document4 pagesMaize January 2022nandarulsNo ratings yet

- Main - Merchandise - Annual - NewDocument1 pageMain - Merchandise - Annual - Newayten.ahmedNo ratings yet

- Agriculture Statistical Information - FinalDocument14 pagesAgriculture Statistical Information - FinalRoshma PandeyNo ratings yet

- Cash - Cost - EBITDA 2017-2022 FVDocument7 pagesCash - Cost - EBITDA 2017-2022 FVJulian Brescia2No ratings yet

- CS Consolidated Crop Year Wise 2021 22 2Document118 pagesCS Consolidated Crop Year Wise 2021 22 2siva suryaNo ratings yet

- Short Term Outlook Statistical Annex - enDocument21 pagesShort Term Outlook Statistical Annex - enMateja NovakNo ratings yet

- Pakistan exports and imports by commodity 2000-2005Document3 pagesPakistan exports and imports by commodity 2000-2005MuhammadOmairNo ratings yet

- ExportDocument2 pagesExportshyam agarwallaNo ratings yet

- Nepal Economic Survey 2009-10 - TablesDocument209 pagesNepal Economic Survey 2009-10 - TablesChandan SapkotaNo ratings yet

- Biogas Yields TableDocument3 pagesBiogas Yields Tablesilenite13No ratings yet

- Part A.1 Tariffs and Imports: Summary and Duty Ranges: Viet NamDocument1 pagePart A.1 Tariffs and Imports: Summary and Duty Ranges: Viet NamPrabhuNo ratings yet

- Employment by IndustryDocument21 pagesEmployment by IndustrysrimkbNo ratings yet

- India Paddy-May-2022Document5 pagesIndia Paddy-May-2022SRINIVASAN TNo ratings yet

- 2018 19Document178 pages2018 19charith resoNo ratings yet

- Area Production CropsDocument1 pageArea Production CropsZahid IhsanNo ratings yet

- Maize Outlook-October 2023Document4 pagesMaize Outlook-October 2023SRINIVASAN TNo ratings yet

- Dairy Forecasts: 2018 2019 IV Annual I II III IVDocument5 pagesDairy Forecasts: 2018 2019 IV Annual I II III IVAkash NeupaneNo ratings yet

- 10 Years Factories DataDocument36 pages10 Years Factories Datagetachew yetenaNo ratings yet

- Statistical AppendixDocument6 pagesStatistical AppendixVenus PlanetNo ratings yet

- India's Cotton Textiles Export Update for FY 2021-22Document8 pagesIndia's Cotton Textiles Export Update for FY 2021-22ashish mishraNo ratings yet

- Data of EconomatricsDocument2 pagesData of EconomatricsArmaan JunaidNo ratings yet

- T - 124interDocument2 pagesT - 124interYuvaraj StalinNo ratings yet

- Presentation - MEE - Spray Dryer - Drum De-Contamination - Dahej - July 2021Document28 pagesPresentation - MEE - Spray Dryer - Drum De-Contamination - Dahej - July 2021sai muraliNo ratings yet

- Tables: Table 1 Annual Growth Rate of Meat Production in India: 1975-2000Document6 pagesTables: Table 1 Annual Growth Rate of Meat Production in India: 1975-2000Sanket Kumar DeshmukhNo ratings yet

- Key Economic Indicators: DemographyDocument2 pagesKey Economic Indicators: Demographyshifan_amNo ratings yet

- Cereals ImportsDocument18 pagesCereals ImportsAlex's PrestigeNo ratings yet

- 2009-08-10 - Trade Policy Review - Report by The Secretariat On Guyana Rev1 PART1 (WTTPRS218R1-01)Document11 pages2009-08-10 - Trade Policy Review - Report by The Secretariat On Guyana Rev1 PART1 (WTTPRS218R1-01)Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Tariffs RussiaDocument1 pageTariffs Russiarubencito1No ratings yet

- I. Economic Environment (1) O: The Dominican Republic WT/TPR/S/207/Rev.1Document15 pagesI. Economic Environment (1) O: The Dominican Republic WT/TPR/S/207/Rev.1Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- IV. Trade Policies by Sector (1) A, F F (I) Agriculture: Nigeria WT/TPR/S/247Document32 pagesIV. Trade Policies by Sector (1) A, F F (I) Agriculture: Nigeria WT/TPR/S/247gghNo ratings yet

- PR May21Document1 pagePR May21Khandaker Amir EntezamNo ratings yet

- Business Studies: Exports and ImportsDocument3 pagesBusiness Studies: Exports and ImportsDimple VaishnavNo ratings yet

- An Introduction To Pakistan's Sugar Industry: TH TH THDocument12 pagesAn Introduction To Pakistan's Sugar Industry: TH TH THSennen DesouzaNo ratings yet

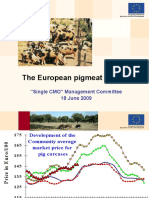

- Development of the European pigmeat sectorDocument20 pagesDevelopment of the European pigmeat sectorMadalina RobescuNo ratings yet

- Part A.1 Tariffs and Imports: Summary and Duty Ranges: CanadaDocument1 pagePart A.1 Tariffs and Imports: Summary and Duty Ranges: CanadaCr CryptoNo ratings yet

- InDocument19 pagesInGauravmarwah2009No ratings yet

- Hari Senin Milku Strawberry Tanggal 24/05/2022 Shift S3 Run Hour 8 Bagian Keterangan DT (Menit) ProsesDocument4 pagesHari Senin Milku Strawberry Tanggal 24/05/2022 Shift S3 Run Hour 8 Bagian Keterangan DT (Menit) ProsesRomli HoiriyahNo ratings yet

- Growth Rate and Composition of Real GDPDocument27 pagesGrowth Rate and Composition of Real GDPpallavi jhanjiNo ratings yet

- FINAL CLAFA 2 2023 Sharing 20 AprilDocument91 pagesFINAL CLAFA 2 2023 Sharing 20 AprilKennedy MabehlaNo ratings yet

- GDP 2007 08Document3 pagesGDP 2007 08api-3709098No ratings yet

- US trade data tablesDocument22 pagesUS trade data tablesvivek foj2No ratings yet

- Select Economic IndicatorsDocument2 pagesSelect Economic IndicatorsArun ChandraNo ratings yet

- Gradual Increase in Rice Production Area and Reduction of Post-Harvest LossesDocument4 pagesGradual Increase in Rice Production Area and Reduction of Post-Harvest LossesDodong MelencionNo ratings yet

- CMO October 2022 ForecastsDocument1 pageCMO October 2022 ForecastsAnthony FloresNo ratings yet

- Vjetari Statistikor I Bujqesise 2021Document154 pagesVjetari Statistikor I Bujqesise 2021Amla RusiNo ratings yet

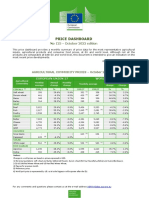

- Commodity Price Dashboard 2022 11 enDocument9 pagesCommodity Price Dashboard 2022 11 enoscarNo ratings yet

- Agriculture: Table 2.1: Historical Growth Performance Agriculture Growth Years PercentDocument44 pagesAgriculture: Table 2.1: Historical Growth Performance Agriculture Growth Years Percentsecretive_boyNo ratings yet

- Indian Food CompotionDocument14 pagesIndian Food CompotionLavan GaddamNo ratings yet

- Maize June 2020Document3 pagesMaize June 2020Rajveer ChauhanNo ratings yet

- Part A.1 Tariffs and Imports: Summary and Duty Ranges: ThailandDocument1 pagePart A.1 Tariffs and Imports: Summary and Duty Ranges: ThailandAlddin AlPatchNo ratings yet

- (Note) Details Are in Table 11.2-3.Document39 pages(Note) Details Are in Table 11.2-3.Josh MukandaNo ratings yet

- Five Year Oilseeds and Commercial Crops Ending 2021 22Document22 pagesFive Year Oilseeds and Commercial Crops Ending 2021 22siva suryaNo ratings yet

- Danish Pig Farming Statistics and Trends Over the Last DecadeDocument1 pageDanish Pig Farming Statistics and Trends Over the Last Decaderujiu huNo ratings yet

- ANRML - JULY - Month Review-2023 - Read-Only ELECTRICAL UPDATED 1st AugDocument16 pagesANRML - JULY - Month Review-2023 - Read-Only ELECTRICAL UPDATED 1st Augsabir aliNo ratings yet

- Biscuit, Cookie and Cracker Manufacturing Manuals: Manual 2: Biscuit DoughsFrom EverandBiscuit, Cookie and Cracker Manufacturing Manuals: Manual 2: Biscuit DoughsNo ratings yet

- Municipal Solid Waste Recycling in Western Europe to 1996From EverandMunicipal Solid Waste Recycling in Western Europe to 1996Rating: 3.5 out of 5 stars3.5/5 (3)

- EL-10 Cereals-2Document12 pagesEL-10 Cereals-2HELENA SUSANTI PANGNo ratings yet

- Module 2 Lesson 3 in TleDocument18 pagesModule 2 Lesson 3 in TleZadd DadullaNo ratings yet

- Flour Mills - DatabaseDocument9 pagesFlour Mills - Databasesubragm0% (1)

- Project Report On Flour Mill Plant (Whole Wheat Flour & Chakki Atta)Document4 pagesProject Report On Flour Mill Plant (Whole Wheat Flour & Chakki Atta)EIRI Board of Consultants and PublishersNo ratings yet

- Buckwheat Flour - Adds Nutrients and Flavor To Baked GoodsDocument6 pagesBuckwheat Flour - Adds Nutrients and Flavor To Baked GoodsAnne MorenoNo ratings yet

- Malting Barley StoryDocument8 pagesMalting Barley StoryeduenglerNo ratings yet

- Coix Lacryma-Jobi Ma Yuen Coix Lacryma-Jobi StenocarpaDocument7 pagesCoix Lacryma-Jobi Ma Yuen Coix Lacryma-Jobi StenocarpaMuhamad Taufiq RahmanNo ratings yet

- Equipment ListDocument2 pagesEquipment Listالدال على الخير كفاعلهNo ratings yet

- CP-PANE DI SANT ABBONDIO EnglishDocument4 pagesCP-PANE DI SANT ABBONDIO Englishdani danNo ratings yet

- UntitledDocument216 pagesUntitledlovebhanwala1153No ratings yet

- A Grain of Wheat - Ngugi Wa Thiong'o PDFDocument277 pagesA Grain of Wheat - Ngugi Wa Thiong'o PDFMima2400082% (33)

- Brazilian Ports - Grains Line Up 07.11.2022Document10 pagesBrazilian Ports - Grains Line Up 07.11.2022Mumtaz AlaviNo ratings yet

- Reporting PGRFA-germplasm Accessions-2010-ICRISAT - 12!10!2010 Cer PathDocument637 pagesReporting PGRFA-germplasm Accessions-2010-ICRISAT - 12!10!2010 Cer PathSri LakshmiNo ratings yet

- Technological Properties of Spelt - Amaranth Composite FloursDocument4 pagesTechnological Properties of Spelt - Amaranth Composite FloursCovaci MihailNo ratings yet

- Mahajan Mini Flour Mill, UdhampurDocument24 pagesMahajan Mini Flour Mill, UdhampurMj PayalNo ratings yet

- Flour - The Integral Part of Balance Diet-Exploratory Study On Cereals ProductsDocument7 pagesFlour - The Integral Part of Balance Diet-Exploratory Study On Cereals Productsma hNo ratings yet

- Anson Mills Wholesale Products 2019Document5 pagesAnson Mills Wholesale Products 2019jikson26No ratings yet

- Little MilletDocument2 pagesLittle MilletRandolf DaitNo ratings yet

- Introduction to Cereals and GrassesDocument24 pagesIntroduction to Cereals and GrassesDenisa CretuNo ratings yet

- RICE, CROPS, ZONES, APDocument4 pagesRICE, CROPS, ZONES, APVishnu Reddy Vardhan PulimiNo ratings yet

- CH 2 Cereal GrainsDocument82 pagesCH 2 Cereal GrainsshahidNo ratings yet

- VikramDocument14 pagesVikramPrashant MishraNo ratings yet

- Meri Life Project ThakurmundaDocument4 pagesMeri Life Project ThakurmundaOmmsai co2011No ratings yet

- Cereal and Cereal ProductDocument6 pagesCereal and Cereal ProductSiti ArnieNo ratings yet

- Curated Organic, Natural Food Products and Agri-FoodPreneurship SupportDocument6 pagesCurated Organic, Natural Food Products and Agri-FoodPreneurship SupportAmudha priyaNo ratings yet

- စပါးစိုက်ပျိုးနည်းစနစ်များDocument33 pagesစပါးစိုက်ပျိုးနည်းစနစ်များaiktiplarNo ratings yet

- Ok VALOR DIGEST INTESTINAL PNDR NRC CARNE 2016Document12 pagesOk VALOR DIGEST INTESTINAL PNDR NRC CARNE 2016jss_bustamanteNo ratings yet

- Ukraine Import: Date Type - MD Customs EDRPOU - Hr8 Importer - NameDocument9 pagesUkraine Import: Date Type - MD Customs EDRPOU - Hr8 Importer - NameRanjit kumar reddyNo ratings yet

- 2018 Examination Pass ListDocument13 pages2018 Examination Pass Listwf4sr4rNo ratings yet

- Order Form Rev 2Document11 pagesOrder Form Rev 2migwanNo ratings yet