You might also like

- Testing Commissioning of LCS and IlluminationDocument36 pagesTesting Commissioning of LCS and IlluminationAnandu AshokanNo ratings yet

- Dupa New Construction of Perimeter Fence at Jbdaph 1-09-2023Document21 pagesDupa New Construction of Perimeter Fence at Jbdaph 1-09-2023Kaizen MinnaNo ratings yet

- Ratio Used To Gauge Asset Management Efficiency and Liquidity Name Formula SignificanceDocument9 pagesRatio Used To Gauge Asset Management Efficiency and Liquidity Name Formula SignificanceAko Si JheszaNo ratings yet

- Capsim Capstone - Best Strategy - Free Excel File - COMPETITION 5.0Document75 pagesCapsim Capstone - Best Strategy - Free Excel File - COMPETITION 5.0Somil GuptaNo ratings yet

- Jsa Cutting PileDocument6 pagesJsa Cutting Pilehilmi hilmiNo ratings yet

- JUST IN TIME AND BACKFLUSH COSTING With Illustrative ProblemDocument7 pagesJUST IN TIME AND BACKFLUSH COSTING With Illustrative Problemenzo0% (1)

- 02 - ISO DIS 22398 - Guia para Ejercicios y TesteoDocument54 pages02 - ISO DIS 22398 - Guia para Ejercicios y TesteoNelson Eduardo Arturo AristizabalNo ratings yet

- TPM - Alternative - Roadmap Implementation Guide Line V1Document39 pagesTPM - Alternative - Roadmap Implementation Guide Line V1Dinh Thi TruongNo ratings yet

- Ind As On Assets of The Financial Statements: Unit 1: Indian Accounting Standard 2: InventoriesDocument37 pagesInd As On Assets of The Financial Statements: Unit 1: Indian Accounting Standard 2: Inventorieswacky chitchatNo ratings yet

- Valuation of Inventory Methods and Their ImpactDocument4 pagesValuation of Inventory Methods and Their ImpactTeresa ManNo ratings yet

- Onlineaccounting - LK: Definition of InventoryDocument3 pagesOnlineaccounting - LK: Definition of InventoryayeshaNo ratings yet

- Chapter 3 - IND AS 2 InventoriesDocument18 pagesChapter 3 - IND AS 2 InventoriesAmbati Madhava ReddyNo ratings yet

- Ias 2 - InventoriesDocument2 pagesIas 2 - Inventoriesangelinamaye99No ratings yet

- Ind As 2 Inventories 74892bos60524-Cp6-U1Document42 pagesInd As 2 Inventories 74892bos60524-Cp6-U1kedar bhideNo ratings yet

- Ind As On Assets of The Financial Statements: Unit 1: Indian Accounting Standard 2: InventoriesDocument38 pagesInd As On Assets of The Financial Statements: Unit 1: Indian Accounting Standard 2: InventoriesSri KanthNo ratings yet

- Objective: Scope Inventories Net Realisable ValueDocument14 pagesObjective: Scope Inventories Net Realisable ValueZohair HumayunNo ratings yet

- UFAS2Document4 pagesUFAS2Romylen De GuzmanNo ratings yet

- Cfas Lesson 3 Pas 2 (Activity)Document3 pagesCfas Lesson 3 Pas 2 (Activity)Michelle CabezoNo ratings yet

- Scope: Allocation of Fixed Production OverheadsDocument8 pagesScope: Allocation of Fixed Production OverheadsjayveeNo ratings yet

- Accounts Chapter 4Document13 pagesAccounts Chapter 4lalitshreya1No ratings yet

- Acc 203 RevDocument6 pagesAcc 203 RevHazel DimaanoNo ratings yet

- Chapter 5 InventoriesDocument12 pagesChapter 5 InventoriesMelvin OngNo ratings yet

- A2 Sample Chapter Inventory Valuation PDFDocument19 pagesA2 Sample Chapter Inventory Valuation PDFRafa BentolilaNo ratings yet

- LKAS 2 / IAS 2 - InventoriesDocument29 pagesLKAS 2 / IAS 2 - InventoriesShihan Haniff100% (9)

- InventoriesDocument3 pagesInventoriesNikki RañolaNo ratings yet

- This Study Resource Was: Lecture NotesDocument3 pagesThis Study Resource Was: Lecture NotesWymple Kate Alexis FaisanNo ratings yet

- L1 - ABFA1163 FA II (Student)Document8 pagesL1 - ABFA1163 FA II (Student)Xue YikNo ratings yet

- Valuing Inventory: Key Aspects of AS 2Document32 pagesValuing Inventory: Key Aspects of AS 2arvindNo ratings yet

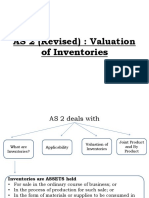

- AS 2 (Revised) : Valuation of InventoriesDocument13 pagesAS 2 (Revised) : Valuation of InventoriesAkshay PatilNo ratings yet

- 67171bos54090 cp4Document28 pages67171bos54090 cp4NISHANT SOINNo ratings yet

- Module 1 - Management AccountingDocument153 pagesModule 1 - Management AccountingNina KasimNo ratings yet

- Cfas Pas 1-16Document8 pagesCfas Pas 1-16Sagad KeithNo ratings yet

- Chapter 4 - Inventories - 27 PagesDocument27 pagesChapter 4 - Inventories - 27 PagesSamartha UmbareNo ratings yet

- Fundamentals of AccountingDocument6 pagesFundamentals of AccountingMJ Dela PenaNo ratings yet

- Inventories: Learning OutcomesDocument28 pagesInventories: Learning OutcomesCA Kranthi KiranNo ratings yet

- Other Cost Incurred in Bringing The Inventories To Their Present Location andDocument3 pagesOther Cost Incurred in Bringing The Inventories To Their Present Location andMarianne SironNo ratings yet

- Cost Accounting (BCOM)Document3 pagesCost Accounting (BCOM)WebkuttanNo ratings yet

- 74695bos60485 Inter p1 cp5 U1Document20 pages74695bos60485 Inter p1 cp5 U1Just KiddingNo ratings yet

- Charts On As by Rohan Sir Vsmart AcademyDocument15 pagesCharts On As by Rohan Sir Vsmart AcademyNarend SinghNo ratings yet

- Paso 3 Gestión contable de inventarios y activos fijos Contabilidad FinancieraDocument4 pagesPaso 3 Gestión contable de inventarios y activos fijos Contabilidad FinancieraAstridNo ratings yet

- MODULE 3 InventoriesDocument6 pagesMODULE 3 InventoriesJean Geibrielle RomeroNo ratings yet

- Ias2 SNDocument7 pagesIas2 SNEmaan QaiserNo ratings yet

- Pas 2 InventoriesDocument10 pagesPas 2 InventoriesAnne100% (1)

- 4.1 Audit of Inventories and Cost of SalesDocument2 pages4.1 Audit of Inventories and Cost of SalesNavsNo ratings yet

- 08 Ias 2Document3 pages08 Ias 2Irtiza AbbasNo ratings yet

- 13.3 As 2 Valuation of Inventories Revision Notes by Nitin Goel Sir PDFDocument6 pages13.3 As 2 Valuation of Inventories Revision Notes by Nitin Goel Sir PDFSrinishaNo ratings yet

- As - 2: Valuation of InventoriesDocument18 pagesAs - 2: Valuation of InventoriesrajuNo ratings yet

- IAS 2 - InventoriesDocument17 pagesIAS 2 - InventoriesraopraniNo ratings yet

- Aldi-A German Retailing Icon: FINAL CASE ANALYSIS - Sales & Operation PlanningDocument6 pagesAldi-A German Retailing Icon: FINAL CASE ANALYSIS - Sales & Operation PlanningSARGAM JAINNo ratings yet

- Comparison 7.5 ĐiểmDocument23 pagesComparison 7.5 Điểmtuân okNo ratings yet

- Reporting of Long-Lived Assets/PPE/Fixed AssetsDocument6 pagesReporting of Long-Lived Assets/PPE/Fixed AssetsAnishaSapraNo ratings yet

- Charts On AS by Rohan Sir VSMART ACADEMY PDFDocument36 pagesCharts On AS by Rohan Sir VSMART ACADEMY PDFAejaz Mohamed86% (7)

- Module 05 - Inventories, Agricultural Assets and ImpairmentDocument21 pagesModule 05 - Inventories, Agricultural Assets and Impairmentpaula manaloNo ratings yet

- Ias 2 SummaryDocument5 pagesIas 2 Summaryp.dashaelaineNo ratings yet

- AS2 Valuation of Inventories GuideDocument12 pagesAS2 Valuation of Inventories GuideJohanNo ratings yet

- Pas 2 InventoriesDocument12 pagesPas 2 InventoriesLETIGIO, RHEANA ROSE M.No ratings yet

- Inventories Accounting StandardDocument25 pagesInventories Accounting StandardvijaykumartaxNo ratings yet

- ACC 203 Module 4 PAS 2 Inventories PAS 41 Biological AssetsDocument15 pagesACC 203 Module 4 PAS 2 Inventories PAS 41 Biological AssetsKirsty SicamNo ratings yet

- G Ias 2Document19 pagesG Ias 2Daniel MNo ratings yet

- AF210 - Topic 5 - Lecture - MWDocument10 pagesAF210 - Topic 5 - Lecture - MWStanley RobertNo ratings yet

- Inventory ValuationDocument16 pagesInventory ValuationKillari PadmasriNo ratings yet

- C16-MFRS 102 InventoriesDocument2 pagesC16-MFRS 102 InventoriesNur ain Natasha ShaharudinNo ratings yet

- As 2Document7 pagesAs 2sanjay sNo ratings yet

- Section 13Document26 pagesSection 13Abata BageyuNo ratings yet

- PAS 2 Inventories - Cost Formulas, Write-Downs & ReversalsDocument13 pagesPAS 2 Inventories - Cost Formulas, Write-Downs & ReversalsJohn Arsen AsuncionNo ratings yet

- Executive's Guide to Fair Value: Profiting from the New Valuation RulesFrom EverandExecutive's Guide to Fair Value: Profiting from the New Valuation RulesNo ratings yet

- Fair Value for Financial Reporting: Meeting the New FASB RequirementsFrom EverandFair Value for Financial Reporting: Meeting the New FASB RequirementsNo ratings yet

- Clarissa Borbon - UTS Module 2.5 WorksheetDocument4 pagesClarissa Borbon - UTS Module 2.5 WorksheetClarissa BorbonNo ratings yet

- Fin MarDocument3 pagesFin MarClarissa BorbonNo ratings yet

- Clarissa Borbon - UTS Module 2.4 WorksheetDocument5 pagesClarissa Borbon - UTS Module 2.4 WorksheetClarissa BorbonNo ratings yet

- Problem 1: ComputationsDocument6 pagesProblem 1: ComputationsClarissa BorbonNo ratings yet

- Borbon Bsa2bDocument1 pageBorbon Bsa2bClarissa BorbonNo ratings yet

- Problem 1: ComputationsDocument6 pagesProblem 1: ComputationsClarissa BorbonNo ratings yet

- Concise for Borbon Clarissa D. BSA-2B ConWorld Prof. Richard Nellas DocumentDocument3 pagesConcise for Borbon Clarissa D. BSA-2B ConWorld Prof. Richard Nellas DocumentClarissa BorbonNo ratings yet

- Borbon Bsa2bDocument1 pageBorbon Bsa2bClarissa BorbonNo ratings yet

- Borbon Bsa2bDocument1 pageBorbon Bsa2bClarissa BorbonNo ratings yet

- Touchpoint Mapping: An Essential Foundation For Improving Customer Experience and ValueDocument15 pagesTouchpoint Mapping: An Essential Foundation For Improving Customer Experience and ValuenidalitNo ratings yet

- Air Synapsis - Aeronautical Design Services Pre-qualification-LDocument74 pagesAir Synapsis - Aeronautical Design Services Pre-qualification-LsureeshNo ratings yet

- Introduction of Eureka ForbesDocument9 pagesIntroduction of Eureka ForbesOsbertAaronNoronha100% (1)

- ENT300 Module01 THEORIES CONCEPT OF ENTRDocument21 pagesENT300 Module01 THEORIES CONCEPT OF ENTRXandra Louise Estela TeNo ratings yet

- What Is Strategic ManagementDocument32 pagesWhat Is Strategic ManagementradhikaiyerNo ratings yet

- Teks Moderator Sempro SemhasDocument2 pagesTeks Moderator Sempro Semhasela saputriNo ratings yet

- Hospital Bed Capacity PlanningDocument34 pagesHospital Bed Capacity Planningvj4249No ratings yet

- Total Quality Management: Total Quality Management or TQM Is An Integrative Philosophy of Management ForDocument8 pagesTotal Quality Management: Total Quality Management or TQM Is An Integrative Philosophy of Management ForUpasana KanchanNo ratings yet

- Chapter 2Document10 pagesChapter 2Meloy ApiladoNo ratings yet

- Edocument 213Document41 pagesEdocument 213bobby.theiss375No ratings yet

- Unit 5 - TRANSFER PRICINGDocument28 pagesUnit 5 - TRANSFER PRICINGRachma DiniNo ratings yet

- (Assignment) Finc 331 Project 1Document6 pages(Assignment) Finc 331 Project 1Nashon ChachaNo ratings yet

- Department of Education: Annual Procurement PlanDocument1 pageDepartment of Education: Annual Procurement PlanOrlando ClaorNo ratings yet

- 8 The Master BudgetDocument20 pages8 The Master BudgetPatricia Mae AdarloNo ratings yet

- Engineering Project Management RolesDocument23 pagesEngineering Project Management RolesRana BasitNo ratings yet

- Focus On Excellence!: Gordon J. Stevenson October 2014Document89 pagesFocus On Excellence!: Gordon J. Stevenson October 2014jonny jonnoNo ratings yet

- Keep Them Flying - IBM WPDocument20 pagesKeep Them Flying - IBM WPRalph CarpenterNo ratings yet

- Design Build ProducibilityDocument31 pagesDesign Build ProducibilityMike Byers100% (1)

- Job Title: Senior Consultant - Tech Consulting - National - Data & Analytics - BangaloreDocument2 pagesJob Title: Senior Consultant - Tech Consulting - National - Data & Analytics - Bangalorekamal4u85No ratings yet

- 2021-22 - T1 Mock Test - Class XII - Business Studies - Set1Document14 pages2021-22 - T1 Mock Test - Class XII - Business Studies - Set1Sampada BassiNo ratings yet

- Principles of Management ProjectDocument23 pagesPrinciples of Management ProjectghsjgjNo ratings yet

- Fabm 1 Week 1: Introduction To Accounting: Nature of BusinessDocument7 pagesFabm 1 Week 1: Introduction To Accounting: Nature of BusinessTumamudtamud, JenaNo ratings yet

- Ica Question BankDocument22 pagesIca Question Bankicchapurtiutsavmandal1No ratings yet