You might also like

- Class 11 Accounts Project DPSDocument10 pagesClass 11 Accounts Project DPSComplicated Alpaca100% (1)

- MTP-1 (Solutions (QR Code) )Document13 pagesMTP-1 (Solutions (QR Code) )ajay.007.sngNo ratings yet

- Ishita Sharaf - Accounts ProjectDocument6 pagesIshita Sharaf - Accounts ProjectPragya SharafNo ratings yet

- Homework 27-02-2023 (Journal)Document3 pagesHomework 27-02-2023 (Journal)Akshayaa PrakashNo ratings yet

- TS Grewal Solution For Class 11 Accountancy Chapter 5 - JournalDocument47 pagesTS Grewal Solution For Class 11 Accountancy Chapter 5 - JournalRUSHIL GUPTANo ratings yet

- Journal Entry Answers 30 Aug 22Document2 pagesJournal Entry Answers 30 Aug 22WarrioropNo ratings yet

- Ledger and Trial BalanceDocument24 pagesLedger and Trial BalanceMd.Amir hossain khan100% (1)

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Account... DR: Date Partucular LF Amount (DR) Amount (CR)Document4 pagesAccount... DR: Date Partucular LF Amount (DR) Amount (CR)Natasha KapoorNo ratings yet

- Cbse cl12 Ead Accountancy Answers To Sample Paper 6Document15 pagesCbse cl12 Ead Accountancy Answers To Sample Paper 6amaankhan828768No ratings yet

- Account ProjectDocument31 pagesAccount ProjectAayush ShNo ratings yet

- Pass The Journal Entries For The Following Transactions On The Dissolution of The Firm of P and Q After Various Assets - AccountancyDocument3 pagesPass The Journal Entries For The Following Transactions On The Dissolution of The Firm of P and Q After Various Assets - Accountancydhanya1995No ratings yet

- Fa2 Assignment - Ic201248Document7 pagesFa2 Assignment - Ic201248Lavisha GoyalNo ratings yet

- RKG Class 11 Accounts Mock 1 SolDocument14 pagesRKG Class 11 Accounts Mock 1 SolSangket MukherjeeNo ratings yet

- DK Goel Solutions Class 11 Accountancy Chapter 9 - Books of Original Entry - JournalDocument69 pagesDK Goel Solutions Class 11 Accountancy Chapter 9 - Books of Original Entry - JournalVanyaNo ratings yet

- Acting For Debs AnsDocument3 pagesActing For Debs AnsbalonNo ratings yet

- Journal - Ledger in Class WorksheetDocument9 pagesJournal - Ledger in Class WorksheetAnurag KapoorNo ratings yet

- Accounts Class 12Document167 pagesAccounts Class 12Utkarsh Navandar100% (1)

- Problem - No.1 Amalgamation in The Nature of Purchase - Net Asset Method Without Statutory Reserve)Document6 pagesProblem - No.1 Amalgamation in The Nature of Purchase - Net Asset Method Without Statutory Reserve)Siva SankariNo ratings yet

- Accounts ProjectDocument4 pagesAccounts ProjectSonu VargheseNo ratings yet

- CA FDN - Paper 1 - 100M - 26.11. AnswerDocument21 pagesCA FDN - Paper 1 - 100M - 26.11. Answerdhanalakm79No ratings yet

- Ts Grewal Solutions Class 12 Accountancy Volume 2 Chapter 9Document6 pagesTs Grewal Solutions Class 12 Accountancy Volume 2 Chapter 9samuraisurya58No ratings yet

- Adobe Scan 20 Aug 2021Document17 pagesAdobe Scan 20 Aug 2021Rishit GoelNo ratings yet

- COGS CasesDocument24 pagesCOGS CasesPrabhat KharelNo ratings yet

- Class 11 Accounts SP 2 Answer KeyDocument18 pagesClass 11 Accounts SP 2 Answer KeyUdyamGNo ratings yet

- AccountsDocument13 pagesAccountspalash khannaNo ratings yet

- Acting For Debs AnsDocument3 pagesActing For Debs AnsbalonNo ratings yet

- Accounts 1Document3 pagesAccounts 1Akhil JainNo ratings yet

- Chapter 4 To Chapter 5Document24 pagesChapter 4 To Chapter 5XENA LOPEZNo ratings yet

- Cash Book (Bank Column) : Answer Key of BRS, Boe Inventory Q1. in The Books of GDocument5 pagesCash Book (Bank Column) : Answer Key of BRS, Boe Inventory Q1. in The Books of GPRAKHAR MUNDRANo ratings yet

- Ledger Book Question SolutionDocument78 pagesLedger Book Question SolutionAKSHAY KUMAR GUPTANo ratings yet

- Chapter 13Document12 pagesChapter 13palash khannaNo ratings yet

- FMA 4 Journal Ledger Trial Balance Incomplete Complete As HomeWork 1611996675443Document5 pagesFMA 4 Journal Ledger Trial Balance Incomplete Complete As HomeWork 1611996675443viveo23No ratings yet

- Class Test: JournalDocument5 pagesClass Test: JournalHafsa ANo ratings yet

- Journal TransactionsDocument3 pagesJournal TransactionsFaye Garlitos100% (1)

- Accounting Mcqs 1Document20 pagesAccounting Mcqs 1Pramod Gowda BNo ratings yet

- Bhaskar AssignmentDocument2 pagesBhaskar Assignment2009silmshady6709No ratings yet

- Class Work Journal EntryDocument16 pagesClass Work Journal EntryRishabh ChawlaNo ratings yet

- TS Grewal Solutions Class 12 Accountancy Volume 1 Chapter 7 - Dissolution of Partnership FirmDocument17 pagesTS Grewal Solutions Class 12 Accountancy Volume 1 Chapter 7 - Dissolution of Partnership FirmMayank Garange100% (1)

- Journal Entry in The Books of M/s Enthusiastic Enterprise LTDDocument2 pagesJournal Entry in The Books of M/s Enthusiastic Enterprise LTDAnuj GohainNo ratings yet

- Journal of Afzal, Kolkata: Date Particulars Debit CreditDocument9 pagesJournal of Afzal, Kolkata: Date Particulars Debit CreditUjjwal AgrawalNo ratings yet

- Corporate Accounting NotesDocument78 pagesCorporate Accounting NotesdivyanshuNo ratings yet

- ProblemsDocument12 pagesProblemsShereen FathimaNo ratings yet

- Anser Key of Rectification of ErrorsDocument3 pagesAnser Key of Rectification of ErrorsmenekyakiaNo ratings yet

- Class 11 Accountancy Chapter-3 Revision NotesDocument11 pagesClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanNo ratings yet

- Journal Problems For AssignmentDocument2 pagesJournal Problems For AssignmentMD. Arif HossainNo ratings yet

- JournalDocument2 pagesJournalAnkur AryaNo ratings yet

- Xii Accountancy Question Bank 1Document46 pagesXii Accountancy Question Bank 1KavoNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- AccountsDocument43 pagesAccountsgogunikhilNo ratings yet

- Business Combination Answers (Manav)Document58 pagesBusiness Combination Answers (Manav)Harshit ChauhanNo ratings yet

- Issue of ShareDocument3 pagesIssue of ShareSayeed AnwarNo ratings yet

- Aec12 - Journal EntriesDocument3 pagesAec12 - Journal EntriesAlyanna Grace OhimanNo ratings yet

- Board Paper-2022-XIDocument8 pagesBoard Paper-2022-XIRn GuptaNo ratings yet

- Marasigan WorksheetDocument15 pagesMarasigan WorksheetLyca MaeNo ratings yet

- 5 Basic AccountingDocument31 pages5 Basic Accounting2205611No ratings yet

- Kendriya Vidyalaya Sangathan, Lucknow Region TERM-II 2021-22 Marking Scheme Class - XI Subject - AccountancyDocument4 pagesKendriya Vidyalaya Sangathan, Lucknow Region TERM-II 2021-22 Marking Scheme Class - XI Subject - AccountancyThe Web RendezvousNo ratings yet

- BBA 2+2 Class Problems and SolutionsDocument75 pagesBBA 2+2 Class Problems and SolutionsBharath.S 16-17-G8No ratings yet

- Credit Derivatives Pricing Models: Models, Pricing and ImplementationFrom EverandCredit Derivatives Pricing Models: Models, Pricing and ImplementationRating: 2 out of 5 stars2/5 (1)

- A Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsFrom EverandA Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsNo ratings yet

- Unit 1 Course MaterialDocument14 pagesUnit 1 Course MaterialPraveen kumarNo ratings yet

- 141 150Document10 pages141 150Praveen kumarNo ratings yet

- CAE1 Time Table - (Except First Year and Final Year Students) - Even Sem 2021-22Document21 pagesCAE1 Time Table - (Except First Year and Final Year Students) - Even Sem 2021-22Praveen kumarNo ratings yet

- SCSX4301-OPERATING SYSTEM-LabmanualDocument22 pagesSCSX4301-OPERATING SYSTEM-LabmanualPraveen kumarNo ratings yet

- 1618479829673notification - CMPs 15 - 04 - 2021Document3 pages1618479829673notification - CMPs 15 - 04 - 2021Praveen kumarNo ratings yet

- ORPHANS. Only My Sister and I Are Staying in Our Home, Nobody Even Visiting UsDocument2 pagesORPHANS. Only My Sister and I Are Staying in Our Home, Nobody Even Visiting UsPraveen kumarNo ratings yet

- CG QBNKDocument5 pagesCG QBNKPraveen kumarNo ratings yet

- Consent LetterDocument1 pageConsent LetterPraveen kumarNo ratings yet

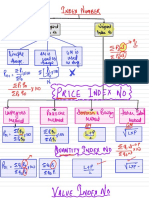

- Index NumberDocument8 pagesIndex NumberPraveen kumarNo ratings yet

- June 2001 North American Native Orchid JournalDocument79 pagesJune 2001 North American Native Orchid JournalNorth American Native Orchid JournalNo ratings yet

- (Re-) Mapping The Concept of DreamingDocument5 pages(Re-) Mapping The Concept of DreamingEduardo VLNo ratings yet

- Soliton WavesDocument42 pagesSoliton WavesAbdalmoedAlaiashyNo ratings yet

- Design of Composite Columns: The American Approach: Roberto T. LeonDocument18 pagesDesign of Composite Columns: The American Approach: Roberto T. LeonvardhangargNo ratings yet

- 2nd Quarter Exam Empowerment - TechnologiesDocument3 pages2nd Quarter Exam Empowerment - Technologieskathryn soriano100% (11)

- S7 Communication Between SIMATIC S7-1500 and SIMATIC S7-300: Step 7 V16 / Bsend / BRCVDocument45 pagesS7 Communication Between SIMATIC S7-1500 and SIMATIC S7-300: Step 7 V16 / Bsend / BRCV9226355166No ratings yet

- Books Published in Goa 2007Document24 pagesBooks Published in Goa 2007Frederick NoronhaNo ratings yet

- Endress HauserDocument28 pagesEndress Hausermanox007No ratings yet

- Mcqs On Virology by Misango Da Phd.Document101 pagesMcqs On Virology by Misango Da Phd.Musa yohana100% (2)

- Acc 103 Course OutlineDocument3 pagesAcc 103 Course OutlineAnitha KimamboNo ratings yet

- Sight GagDocument12 pagesSight Gagcecepo4733No ratings yet

- Letter MDocument5 pagesLetter Malshamsi studentNo ratings yet

- Noes Flex CubeDocument8 pagesNoes Flex CubeSeboeng MashilangoakoNo ratings yet

- Orbitrol Desarmado y ArmadoDocument9 pagesOrbitrol Desarmado y Armadojulio cesarNo ratings yet

- High Voltage - 2020 - Su - Electrical Tree Degradation in High Voltage Cable Insulation Progress and ChallengesDocument12 pagesHigh Voltage - 2020 - Su - Electrical Tree Degradation in High Voltage Cable Insulation Progress and ChallengesLuiz KowalskiNo ratings yet

- Ann Charlton - Steamy DecemberDocument203 pagesAnn Charlton - Steamy Decembershrutigarodia95% (22)

- Drufelcnc Ddcm6V5 (Ddream) Installation ManualDocument32 pagesDrufelcnc Ddcm6V5 (Ddream) Installation ManualgowataNo ratings yet

- Project Review and Administrative AspectsDocument22 pagesProject Review and Administrative Aspectsamit861595% (19)

- Kaizen ToolsDocument43 pagesKaizen Toolssandee1983No ratings yet

- LDR Project (Watermark)Document17 pagesLDR Project (Watermark)RakshitaNo ratings yet

- Analytical Model For Predicting Shear Strengths of Exterior Reinforced Concrete Beam-Column Joints For Seismic ResistanceDocument14 pagesAnalytical Model For Predicting Shear Strengths of Exterior Reinforced Concrete Beam-Column Joints For Seismic ResistanceAndres NaranjoNo ratings yet

- ASPIRO TechnologyDocument19 pagesASPIRO Technologysehyong0419No ratings yet

- Nadi Astrology PDFDocument3 pagesNadi Astrology PDFabhi16No ratings yet

- Rsync Cheat Sheet: by ViaDocument3 pagesRsync Cheat Sheet: by ViaAsep SeptiadiNo ratings yet

- R in Hydrology - EGUDocument25 pagesR in Hydrology - EGUJulio Montenegro GambiniNo ratings yet

- PHP SQL AnywhereDocument7 pagesPHP SQL Anywherecool03No ratings yet

- Disaster Readiness and Risk ReductionDocument239 pagesDisaster Readiness and Risk ReductionGemma Rose LaquioNo ratings yet

- Unit 4 Grammar Standard PDFDocument1 pageUnit 4 Grammar Standard PDFCarolina Mercado100% (2)

- VxRail 7.0.x Release NotesDocument39 pagesVxRail 7.0.x Release NotesphongnkNo ratings yet

- Comparative Analysis of Print Media and Digital MediaDocument32 pagesComparative Analysis of Print Media and Digital MediaDeval Jyoti ShahNo ratings yet