You might also like

- 2 Chapter 2 Treasury Management Cash Transfer MethodsDocument17 pages2 Chapter 2 Treasury Management Cash Transfer MethodsErica LargozaNo ratings yet

- Manual of Permitted Operations (MOPO)Document7 pagesManual of Permitted Operations (MOPO)Aniekan Akpaidiok100% (2)

- Remittance Application Form MAR2022 E - Form PDFDocument2 pagesRemittance Application Form MAR2022 E - Form PDFAlldyNo ratings yet

- Course Agenda: Understanding Money LaunderingDocument56 pagesCourse Agenda: Understanding Money LaunderinglarissarovaneNo ratings yet

- Receivables ManagementDocument37 pagesReceivables Managementchanky_kool8782% (11)

- BLO Unit 1-1Document24 pagesBLO Unit 1-1Mohammad MAAZNo ratings yet

- Direct Deposit Election FormDocument2 pagesDirect Deposit Election FormAsha Leigh100% (1)

- KYC Onboarding Work FlowDocument15 pagesKYC Onboarding Work FlowVijay Challa0% (1)

- Basics of Credit Analysis: Alexandru CebotariDocument24 pagesBasics of Credit Analysis: Alexandru CebotariStephaney KippleNo ratings yet

- Accounts Payable: A Guide to Running an Efficient DepartmentFrom EverandAccounts Payable: A Guide to Running an Efficient DepartmentNo ratings yet

- Check-Out Procedures: B.Sc. (HHA) / 2 Year/ Checkout ProceduresDocument10 pagesCheck-Out Procedures: B.Sc. (HHA) / 2 Year/ Checkout ProceduresAryan BishtNo ratings yet

- Working at Height PolicyDocument7 pagesWorking at Height PolicyAniekan AkpaidiokNo ratings yet

- FIBK BankReconciliatiaonReport FS FinalDocument10 pagesFIBK BankReconciliatiaonReport FS FinalAMIT SAWANTNo ratings yet

- Presentation On Credit Appraisal in Banking SectorDocument31 pagesPresentation On Credit Appraisal in Banking Sectorchintan05ecNo ratings yet

- Expected Credit Losses Simplified A BDO India Publication 2017 PDFDocument22 pagesExpected Credit Losses Simplified A BDO India Publication 2017 PDFAnonymous CSvZH6No ratings yet

- Blueprint of Banking SectorDocument33 pagesBlueprint of Banking SectormayankNo ratings yet

- Fair Lending Compliance: Intelligence and Implications for Credit Risk ManagementFrom EverandFair Lending Compliance: Intelligence and Implications for Credit Risk ManagementNo ratings yet

- Nil-Comm Law Rev-4c-Sbca-Case DigestsDocument104 pagesNil-Comm Law Rev-4c-Sbca-Case DigestsFaithy Darna100% (1)

- Damages - Case DigestDocument14 pagesDamages - Case Digestandrew estimoNo ratings yet

- ManualAndElectronicBankreconciliation V3-542vtqDocument92 pagesManualAndElectronicBankreconciliation V3-542vtqAmbati Sivaprasad ReddyNo ratings yet

- Payment GatewayTestingDocument8 pagesPayment GatewayTestingkumar314100% (1)

- Market Strategy of HDFC and Icici BankDocument66 pagesMarket Strategy of HDFC and Icici BankKamal Bamba100% (2)

- Part 7 Debtors ManagementDocument7 pagesPart 7 Debtors ManagementShivaniNo ratings yet

- Improve Cure Rate in Credit Card CollectionsDocument40 pagesImprove Cure Rate in Credit Card CollectionsbiswazoomNo ratings yet

- Unit 5Document35 pagesUnit 5Pratheek PutturNo ratings yet

- 1615456490-10 Credit Evaluation AnalysisDocument29 pages1615456490-10 Credit Evaluation AnalysisAshishku DashNo ratings yet

- 004 - Red Flags-Bank AudtsDocument41 pages004 - Red Flags-Bank Audtschandra sekharNo ratings yet

- Sample Project - 1Document108 pagesSample Project - 1MADHURAM SHARMANo ratings yet

- Final Report - Payments ProcessDocument32 pagesFinal Report - Payments Processmrshami7754No ratings yet

- Q2 Week 2 RECONitemsPRINTDocument19 pagesQ2 Week 2 RECONitemsPRINTxfq6tfqgtwNo ratings yet

- AA-Risk IdentificationDocument2 pagesAA-Risk IdentificationRafsan JazzNo ratings yet

- Solution - 4.1b - PROCESS - RISK - CONTROL - MATRIX - Window BDocument4 pagesSolution - 4.1b - PROCESS - RISK - CONTROL - MATRIX - Window BrickmortyNo ratings yet

- Bank ReconciliationDocument22 pagesBank ReconciliationstanleymasemulaNo ratings yet

- RisksDocument7 pagesRisksJaden EuNo ratings yet

- Chapter 9Document33 pagesChapter 9Faris IkhwanNo ratings yet

- Receivables Management: "Any Fool Can Lend Money, But It TakesDocument37 pagesReceivables Management: "Any Fool Can Lend Money, But It Takesjai262418No ratings yet

- Response - Revenue AssuranceDocument4 pagesResponse - Revenue AssuranceBhagwatiprasad MathurNo ratings yet

- Group 2 - Cash TransferDocument34 pagesGroup 2 - Cash TransferCiocon JewelynNo ratings yet

- Chapter 5 by in PDF Book Basics of Credit Analysis: Alexandru CebotariDocument24 pagesChapter 5 by in PDF Book Basics of Credit Analysis: Alexandru CebotariAbdul QadirNo ratings yet

- Credit MonitoringDocument166 pagesCredit Monitoringjananidhanasekaran26No ratings yet

- Pr3 Gp3Document33 pagesPr3 Gp3Kwang Yi JuinNo ratings yet

- Inherent Risk: Planning Materiality LevelDocument1 pageInherent Risk: Planning Materiality LevelKid & Baby Gallery TCLNo ratings yet

- Risk ManagementDocument15 pagesRisk Managementvaibhav surekaNo ratings yet

- Enhancing The Credibility of Msmes - Performance & Credit Rating SchemeDocument32 pagesEnhancing The Credibility of Msmes - Performance & Credit Rating SchemeSatya PrakashNo ratings yet

- Multiple Choice - Chapter10 To Chapter20Document22 pagesMultiple Choice - Chapter10 To Chapter20Aditya Agung SatrioNo ratings yet

- 3-5 CMDocument6 pages3-5 CMKate Cyrene PerezNo ratings yet

- AAA Assignment 1 FinalDocument7 pagesAAA Assignment 1 FinaljasonnumahnalkelNo ratings yet

- BUSINESS OFFICE AND HEAD OFFICE RISK RATING For UBA AFRICA - OCT2011Document18 pagesBUSINESS OFFICE AND HEAD OFFICE RISK RATING For UBA AFRICA - OCT2011Michel Bryan SemwoNo ratings yet

- BNI-IFRS9 Day2Document59 pagesBNI-IFRS9 Day2Adrian Eka PutraNo ratings yet

- Potomac Accounting Test - AnswersDocument5 pagesPotomac Accounting Test - AnswersJason PutotNo ratings yet

- TRADE CREDIT AND RISK SYSTEM - ICI - 170718 Rev01Document32 pagesTRADE CREDIT AND RISK SYSTEM - ICI - 170718 Rev01Balaji SowmyanarayananNo ratings yet

- Concept Map (Garcia, Plata, Villamin) PDFDocument6 pagesConcept Map (Garcia, Plata, Villamin) PDFMinji OhNo ratings yet

- SA 320 - User of FS ConsiderationDocument6 pagesSA 320 - User of FS ConsiderationHindutav aryaNo ratings yet

- Investing and Financing Decisions and The Balance SheetDocument35 pagesInvesting and Financing Decisions and The Balance Sheetfmj6687No ratings yet

- Risk Based Audit Approach For Branch Banking Team-CBHDocument15 pagesRisk Based Audit Approach For Branch Banking Team-CBHtusharholey90No ratings yet

- Cash Transfer Methods: Berito, Quennie Bernal, Jessamie Cacho, CarminaDocument26 pagesCash Transfer Methods: Berito, Quennie Bernal, Jessamie Cacho, CarminaJewelyn CioconNo ratings yet

- Cash Transfer Methods: Berito, Quennie Bernal, Jessamie Cacho, CarminaDocument26 pagesCash Transfer Methods: Berito, Quennie Bernal, Jessamie Cacho, CarminaJewelyn CioconNo ratings yet

- Auditing Theory 2nd Sem PrelimsDocument6 pagesAuditing Theory 2nd Sem PrelimsAccounting MaterialsNo ratings yet

- 2020 - Audcap1 - 2.3 RCCM - BunagDocument1 page2020 - Audcap1 - 2.3 RCCM - BunagSherilyn BunagNo ratings yet

- Working Capital Management: Details in Fixed Income)Document1 pageWorking Capital Management: Details in Fixed Income)Ngân HàNo ratings yet

- COSO Framework and Internal ControlDocument15 pagesCOSO Framework and Internal Controlchiara uyNo ratings yet

- Final Cash Audit ProgramDocument3 pagesFinal Cash Audit ProgramMarie May Sese Magtibay100% (1)

- Audit Homework 4.25 4.26 4.29Document4 pagesAudit Homework 4.25 4.26 4.29Hieu NguyenNo ratings yet

- Managing Cash: Merits & Demerits of Holding CashDocument4 pagesManaging Cash: Merits & Demerits of Holding Cashverty asdNo ratings yet

- Evaluating Your International Supplier Payment Cost & EfficiencyDocument12 pagesEvaluating Your International Supplier Payment Cost & EfficiencyFranki HaberNo ratings yet

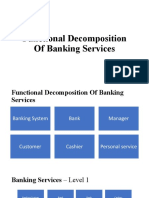

- Functional Decomposition of Banking Services 12Document4 pagesFunctional Decomposition of Banking Services 12MUSYOKA KITUKUNo ratings yet

- AUDIT QDocument2 pagesAUDIT QkamaiiiNo ratings yet

- DecompositionDocument4 pagesDecompositionMUSYOKA KITUKUNo ratings yet

- Week 7 PowerpointDocument33 pagesWeek 7 PowerpointAnka MaNo ratings yet

- Ratios - FormulasDocument14 pagesRatios - FormulasNivedita AgarwalNo ratings yet

- Credit Rating in India - JBIMSDocument8 pagesCredit Rating in India - JBIMSSidhi AgarwalNo ratings yet

- Executive's Guide to Fair Value: Profiting from the New Valuation RulesFrom EverandExecutive's Guide to Fair Value: Profiting from the New Valuation RulesNo ratings yet

- JSA For CT OperationsDocument39 pagesJSA For CT OperationsAniekan Akpaidiok0% (1)

- Jsa-Function Test Equipment.Document1 pageJsa-Function Test Equipment.Aniekan AkpaidiokNo ratings yet

- Module 100 - Introduction To QHSES ManagementDocument89 pagesModule 100 - Introduction To QHSES ManagementAniekan AkpaidiokNo ratings yet

- JSA-pumping Lines Rig Up.Document3 pagesJSA-pumping Lines Rig Up.Aniekan AkpaidiokNo ratings yet

- Jsa-Spot Equipment On Boat or Barge.Document1 pageJsa-Spot Equipment On Boat or Barge.Aniekan AkpaidiokNo ratings yet

- JSAS For Pumping Main Treatment.Document2 pagesJSAS For Pumping Main Treatment.Aniekan AkpaidiokNo ratings yet

- Safety ProgramDocument9 pagesSafety ProgramNick LatumboNo ratings yet

- Scope of QMS - Netcore - 2021Document4 pagesScope of QMS - Netcore - 2021Aniekan AkpaidiokNo ratings yet

- Assignment Template (1) - Module 104Document1 pageAssignment Template (1) - Module 104Aniekan AkpaidiokNo ratings yet

- Daily HSE Activities Report Aug-Wk9 (7th To 13th-19)Document1 pageDaily HSE Activities Report Aug-Wk9 (7th To 13th-19)Aniekan AkpaidiokNo ratings yet

- Module 101-AssignmentDocument2 pagesModule 101-AssignmentAniekan AkpaidiokNo ratings yet

- Working at Height ProcedureDocument11 pagesWorking at Height ProcedureAniekan AkpaidiokNo ratings yet

- Assignment TemplateDocument2 pagesAssignment TemplateAniekan AkpaidiokNo ratings yet

- Daily HSE Activities Report Aug-Wk10 (14th To 20th-19)Document1 pageDaily HSE Activities Report Aug-Wk10 (14th To 20th-19)Aniekan AkpaidiokNo ratings yet

- Daily HSE Activities Report AugSept-Wk12 (28th To 3rd-19)Document1 pageDaily HSE Activities Report AugSept-Wk12 (28th To 3rd-19)Aniekan AkpaidiokNo ratings yet

- Daily HSE Activities Report Aug-Wk8 (1st To 6th-19)Document1 pageDaily HSE Activities Report Aug-Wk8 (1st To 6th-19)Aniekan AkpaidiokNo ratings yet

- Stop Work Policy-Rev01Document1 pageStop Work Policy-Rev01Aniekan AkpaidiokNo ratings yet

- MANAGEMENT OF CHANGE PROCEDURE NetcoreDocument12 pagesMANAGEMENT OF CHANGE PROCEDURE NetcoreAniekan AkpaidiokNo ratings yet

- Risk Assessment For Cementing and Pumping OperationsDocument8 pagesRisk Assessment For Cementing and Pumping OperationsAniekan AkpaidiokNo ratings yet

- Security Policy Statement-Rev01Document1 pageSecurity Policy Statement-Rev01Aniekan AkpaidiokNo ratings yet

- Ethics Policy-Rev01Document1 pageEthics Policy-Rev01Aniekan AkpaidiokNo ratings yet

- Drop Object Prevention Policy and Procedure: NISNL-QHSE-DROPS-0421Document10 pagesDrop Object Prevention Policy and Procedure: NISNL-QHSE-DROPS-0421Aniekan AkpaidiokNo ratings yet

- Fmbo Question Bank and McqsDocument19 pagesFmbo Question Bank and McqspraveenNo ratings yet

- Seamen'S Provident Fund Organization, Mumbai: Annexure - 1Document9 pagesSeamen'S Provident Fund Organization, Mumbai: Annexure - 1Anindya DeyNo ratings yet

- Ghee TestingDocument51 pagesGhee Testing114912No ratings yet

- New Technological Innovations in The Banking SectorDocument5 pagesNew Technological Innovations in The Banking SectorlapogkNo ratings yet

- Moral Character Determination Application InstructionsDocument11 pagesMoral Character Determination Application InstructionsAdam CohenNo ratings yet

- TLC Online Learning Packs Brochure 2020Document20 pagesTLC Online Learning Packs Brochure 2020trongnvtNo ratings yet

- New Product Development and Product Management in Banks: Banking Term PaperDocument12 pagesNew Product Development and Product Management in Banks: Banking Term PaperdesaiurjaNo ratings yet

- Inr1904000000246 PDFDocument2 pagesInr1904000000246 PDFSiddhartha kumar singhNo ratings yet

- Account Statement For Account:22112413000022: Branch DetailsDocument4 pagesAccount Statement For Account:22112413000022: Branch Detailsvishwak properties mangal avenueNo ratings yet

- A Study On Customer S Perception TowardsDocument8 pagesA Study On Customer S Perception TowardsPrabhu SahuNo ratings yet

- Micr Cheque Personalisation Encoder: Make FZA-2155 A Great Addition To Your Cheque Clearing ProcessesDocument2 pagesMicr Cheque Personalisation Encoder: Make FZA-2155 A Great Addition To Your Cheque Clearing ProcessesÖmer ElmasriNo ratings yet

- Leisure Guide Fall 2010 English WEB1Document60 pagesLeisure Guide Fall 2010 English WEB1Tyler SamsonNo ratings yet

- ReviewerDocument67 pagesReviewerKyungsoo DohNo ratings yet

- Personal Health Insurance Application FormDocument9 pagesPersonal Health Insurance Application Formjob.cndNo ratings yet

- A Study Analysis On Working Capital Managment at Pole Star Cargo Pvt. Ltd.Document69 pagesA Study Analysis On Working Capital Managment at Pole Star Cargo Pvt. Ltd.AJAY ABIPLNo ratings yet

- CHEQUEmaster ClassDocument10 pagesCHEQUEmaster ClassMohanarajNo ratings yet

- M F8 Ot Ui VIOOs GRXMDocument6 pagesM F8 Ot Ui VIOOs GRXMSupreet ManturNo ratings yet

- Notes NHFS Up To Cir. 25 2015 EMI CorrectedDocument34 pagesNotes NHFS Up To Cir. 25 2015 EMI CorrectedAnoop PS Sasidharan100% (1)

- Thanh Toan QteDocument11 pagesThanh Toan Qtethanh trucNo ratings yet

- Form 1300tDocument21 pagesForm 1300tdotnet4100% (1)