You might also like

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- How To Check Client or Fullz Credit Score@BaddestupdateDocument7 pagesHow To Check Client or Fullz Credit Score@Baddestupdatecolton gallahar100% (2)

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- Mortgage FundamentalsDocument14 pagesMortgage FundamentalsMadhuPreethi Nachegari100% (1)

- Business Analyst Finance Domain Interview QuestionsDocument9 pagesBusiness Analyst Finance Domain Interview QuestionsVish KinsNo ratings yet

- TransactionSummary PDFDocument2 pagesTransactionSummary PDFWenjie65No ratings yet

- All You Need To Know About Private LendingDocument7 pagesAll You Need To Know About Private LendingJulio CardenasNo ratings yet

- 101 Mortgage Broker Secrets To Get The Best MortgageDocument22 pages101 Mortgage Broker Secrets To Get The Best Mortgageweb3752100% (1)

- Mortgage MarketsDocument5 pagesMortgage MarketsCliezel Ugdamen100% (1)

- Mortgage System in USDocument63 pagesMortgage System in USAnkit SinghNo ratings yet

- Mortgage Loan DefinitionDocument65 pagesMortgage Loan DefinitionAnonymous iyQmvDnHnCNo ratings yet

- Mortgage-Backed Securities vs. Treasury Bonds: An Introduction to Mortgage REITs: Financial Freedom, #78From EverandMortgage-Backed Securities vs. Treasury Bonds: An Introduction to Mortgage REITs: Financial Freedom, #78No ratings yet

- Residential Mortgage Loans: Chapter SummaryDocument19 pagesResidential Mortgage Loans: Chapter SummarypinkcowyayNo ratings yet

- Bank Account Closing LetterDocument13 pagesBank Account Closing LetterSantosh ShresthaNo ratings yet

- Personal Loan ProjectDocument7 pagesPersonal Loan ProjectSudhakar GuntukaNo ratings yet

- MORTGAGEDocument9 pagesMORTGAGEbibin100% (1)

- Mortgage BasicsDocument18 pagesMortgage BasicsJie RongNo ratings yet

- Question Set Fabozzi, Chapter 12Document14 pagesQuestion Set Fabozzi, Chapter 12Hoang HaNo ratings yet

- Cartradeexchange Solutions Private LimitedDocument2 pagesCartradeexchange Solutions Private LimitedAJEET KUMARNo ratings yet

- (Module 4) ProblemsDocument6 pages(Module 4) ProblemsYanie Dela Cruz100% (1)

- What Is MRTADocument9 pagesWhat Is MRTASugashini KrishnanNo ratings yet

- MLTT Sales Idea For Takaful Life Planner - V4Document16 pagesMLTT Sales Idea For Takaful Life Planner - V4Nazarul FazreenNo ratings yet

- Online Term PlanDocument9 pagesOnline Term PlanPradeep PatilNo ratings yet

- Online Term Plans (ML-30!06!2011)Document8 pagesOnline Term Plans (ML-30!06!2011)Amit UpalekarNo ratings yet

- Literature Review On Life Insurance PDFDocument6 pagesLiterature Review On Life Insurance PDFaflskeqjr100% (1)

- Summer Class 2022Document5 pagesSummer Class 2022ERMA MAE GABATONo ratings yet

- BA Finance Domain - TutorialsDocument31 pagesBA Finance Domain - TutorialsRajesh MekalaNo ratings yet

- How Do Risk and Term Structure Affect Interest Rates?Document8 pagesHow Do Risk and Term Structure Affect Interest Rates?Aisha Bint TilaNo ratings yet

- Insider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1From EverandInsider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1No ratings yet

- Literature Review: D. Ramkumar (2003)Document7 pagesLiterature Review: D. Ramkumar (2003)ManthanNo ratings yet

- Life InsuranceDocument11 pagesLife InsuranceTuttu RajenDranNo ratings yet

- Housing Loan March 2014Document2 pagesHousing Loan March 2014Deborah JenningsNo ratings yet

- Evaluate Your Life Insurance Needs: P V Subramanyam, Financial TrainerDocument5 pagesEvaluate Your Life Insurance Needs: P V Subramanyam, Financial TrainerAjit AgnihotriNo ratings yet

- Thesis Statement For Life InsuranceDocument8 pagesThesis Statement For Life Insurancednnsgccc100% (2)

- A Reprint From Tierra Grande Magazine © 2014. Real Estate Center. All Rights ReservedDocument6 pagesA Reprint From Tierra Grande Magazine © 2014. Real Estate Center. All Rights Reservedapi-251198534No ratings yet

- Life Insurance in India - 4Document7 pagesLife Insurance in India - 4Himansu S MNo ratings yet

- Financial Markets and Institutions Madura 11th Edition Solutions ManualDocument38 pagesFinancial Markets and Institutions Madura 11th Edition Solutions ManualAngelaKellerafcr100% (20)

- IMoney Home Buying GuideDocument24 pagesIMoney Home Buying GuideshaharilannuarNo ratings yet

- Insurance-2 Dyuti RainaDocument10 pagesInsurance-2 Dyuti Rainavinay sharmaNo ratings yet

- Financial Markets and Institutions Abridged Edition 11th Edition Jeff Madura Solutions Manual 1Document36 pagesFinancial Markets and Institutions Abridged Edition 11th Edition Jeff Madura Solutions Manual 1jeffreylucasctdfzmqayg100% (23)

- RCMF - Loan Against InsuranceDocument8 pagesRCMF - Loan Against InsuranceAnuj KumarNo ratings yet

- Adjustable-Rate Mortgages: The Federal Reserve BoardDocument45 pagesAdjustable-Rate Mortgages: The Federal Reserve BoardJorgeNo ratings yet

- 8 Musharakah Muanaqisah - MeeraDocument30 pages8 Musharakah Muanaqisah - MeeraZul Qur'ainNo ratings yet

- TIME StampedDocument21 pagesTIME StampedMuzamel AbdellaNo ratings yet

- Reporting ScriptDocument5 pagesReporting ScriptKelly CardejonNo ratings yet

- Chapter 10 - The Mortgage MarketDocument12 pagesChapter 10 - The Mortgage MarketMerge MergeNo ratings yet

- Capstone Report - Ensure - Io - Final DraftDocument13 pagesCapstone Report - Ensure - Io - Final DraftRamapriyaNo ratings yet

- Mortgage and Amortization (Math of Investment)Document2 pagesMortgage and Amortization (Math of Investment)RCNo ratings yet

- Reasons To Sell Life Insurance.: PortfolioDocument2 pagesReasons To Sell Life Insurance.: PortfolioWin VitNo ratings yet

- HE OLE OF Ortgage Backed Securities: Words Count: 2939Document10 pagesHE OLE OF Ortgage Backed Securities: Words Count: 2939Abhinay KuraNo ratings yet

- Chapter - 3 Home LoanDocument65 pagesChapter - 3 Home LoanmotherfuckermonsterNo ratings yet

- CHAPTER 13 Debt Management in Retirement Planning PDFDocument35 pagesCHAPTER 13 Debt Management in Retirement Planning PDFMaisarah YaziddNo ratings yet

- Mortgage Financing ThesisDocument6 pagesMortgage Financing Thesisbethhalloverlandpark100% (2)

- Prem Financing AlternativeDocument2 pagesPrem Financing AlternativeBill BlackNo ratings yet

- Life Insurance ProjectDocument11 pagesLife Insurance ProjectDarshana MathurNo ratings yet

- Advantages of Junk Bonds: Financial Products No CommentsDocument5 pagesAdvantages of Junk Bonds: Financial Products No CommentsRajesh KumarNo ratings yet

- Mortgage Markets and Derivatives - AnswerDocument3 pagesMortgage Markets and Derivatives - AnswerSarang SNo ratings yet

- Concept of ClaimsDocument23 pagesConcept of ClaimsbapparoyNo ratings yet

- Interest Rate Cap Structure Definition, Uses, and ExamplesDocument2 pagesInterest Rate Cap Structure Definition, Uses, and ExamplesACC200 MNo ratings yet

- SBI Life Rinn Raksha FlierDocument2 pagesSBI Life Rinn Raksha FlierMonojit SahaNo ratings yet

- 1.6.2) Secondary DataDocument51 pages1.6.2) Secondary DataManjodh Singh BassiNo ratings yet

- Articulos Google Adsense Ingles 2018Document65 pagesArticulos Google Adsense Ingles 2018jairo perdomoNo ratings yet

- Ulip PolicyDocument92 pagesUlip Policybhajayram786No ratings yet

- Credit Card Assignment PDF WeeblyDocument2 pagesCredit Card Assignment PDF Weeblyapi-371069146No ratings yet

- 1 FAQs FinacleDocument17 pages1 FAQs FinacleVikramNo ratings yet

- Chapter 5 Problems The Time Value of MoneyDocument46 pagesChapter 5 Problems The Time Value of MoneyShahid KhanNo ratings yet

- Spark BillDocument3 pagesSpark BillStudy INo ratings yet

- TD Commission To To BPMDocument4 pagesTD Commission To To BPMSai GuruNo ratings yet

- Key Facts Statement PayDay LoanDocument2 pagesKey Facts Statement PayDay LoanSimon AdesolaNo ratings yet

- Annuity SolutionDocument15 pagesAnnuity Solution신동호No ratings yet

- GD - Assignment 2 LatestDocument29 pagesGD - Assignment 2 LatestNurFazalina AkbarNo ratings yet

- AcknowledgementDocument1 pageAcknowledgementaloka.rajNo ratings yet

- CIBIL Score 743: Abhisekha PatnaikDocument9 pagesCIBIL Score 743: Abhisekha PatnaikNilonee ShahNo ratings yet

- International Experiences On Credit Guarantees For Loans To Sme 20081123085412 1027 11Document31 pagesInternational Experiences On Credit Guarantees For Loans To Sme 20081123085412 1027 11Muhamad YusufNo ratings yet

- Visa Checklist For Uk Student VisaDocument15 pagesVisa Checklist For Uk Student VisaSathish SatiNo ratings yet

- OpTransactionHistoryUX302 02 2024Document56 pagesOpTransactionHistoryUX302 02 2024avijitghosh775No ratings yet

- Alexander Van Dyke Math 1050 Project 2 - Mortgage CostsDocument5 pagesAlexander Van Dyke Math 1050 Project 2 - Mortgage Costsapi-233311543No ratings yet

- H. Mgt.Document284 pagesH. Mgt.sahoogayatri719No ratings yet

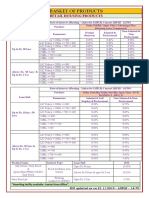

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaNo ratings yet

- BF Di Pa TaposDocument8 pagesBF Di Pa TaposKierstin Kyle RiegoNo ratings yet

- Microfinance Chapter 4Document27 pagesMicrofinance Chapter 4Salina BasnetNo ratings yet

- Transaction Confirmation Report en GB Be1dc9Document1 pageTransaction Confirmation Report en GB Be1dc9ruif45534No ratings yet

- Chapter 10 Lease AccountingDocument6 pagesChapter 10 Lease AccountingCasinas Kyana LouisseNo ratings yet

- Chapter 5 Mortgage Market P1Document13 pagesChapter 5 Mortgage Market P1Hang Huynh Thi ThuyNo ratings yet

- Report of Commerical Banknof EthiopiaDocument22 pagesReport of Commerical Banknof EthiopiaTariku RichNo ratings yet

- WSAFE396 - Organisation Profile and Job DescriptionDocument3 pagesWSAFE396 - Organisation Profile and Job DescriptionjasmyneNo ratings yet

- Current Month Retroactive Total in Base Currency (XAF) : United Nations Secretariat Secretariat Des Nations UniesDocument2 pagesCurrent Month Retroactive Total in Base Currency (XAF) : United Nations Secretariat Secretariat Des Nations UniesDhotNo ratings yet

- EpayslipDocument1 pageEpayslipconstantin radu lunguNo ratings yet