You might also like

- GX Pathways To Decarbonization AutomotiveDocument8 pagesGX Pathways To Decarbonization Automotivekunalsukhija21No ratings yet

- Automotive Workshop On BiW-Structures PDFDocument41 pagesAutomotive Workshop On BiW-Structures PDFArvind KatyayanNo ratings yet

- Ms. Pamela Tikku (ICAT)Document30 pagesMs. Pamela Tikku (ICAT)NagaVenkateshGNo ratings yet

- Engine Technology Pathways For Heavy-Duty Vehicles in India: Working Paper 2016-6Document10 pagesEngine Technology Pathways For Heavy-Duty Vehicles in India: Working Paper 2016-6Santosh TrimbakeNo ratings yet

- METI ZEV Trend in JapanDocument24 pagesMETI ZEV Trend in JapanKennex TsaiNo ratings yet

- E-GAP - Session V - Vikram Widge - FinalDocument9 pagesE-GAP - Session V - Vikram Widge - FinalAmi KarNo ratings yet

- AT 17701 - Engine& Vehicle Management System: Session 38Document32 pagesAT 17701 - Engine& Vehicle Management System: Session 38pavanraneNo ratings yet

- ADL - Future of Fuel Cell VehiclesDocument4 pagesADL - Future of Fuel Cell VehiclesVõ Trọng ĐứcNo ratings yet

- Multi-Stage Vehicles: Formidable Challenge For Body Builders and OemsDocument10 pagesMulti-Stage Vehicles: Formidable Challenge For Body Builders and OemsYOURAJ TALWEKARNo ratings yet

- Hybrid Motorcycle Global MarketingDocument18 pagesHybrid Motorcycle Global Marketinglawren48No ratings yet

- Guidelines For A Sustainable Aviation Fuel Blending Mandate in EuropeDocument42 pagesGuidelines For A Sustainable Aviation Fuel Blending Mandate in EuropeDarryl Farhan WidyawanNo ratings yet

- 63760d18963d6a3c5708a7a4 - CC Token Whitepaper 17nov2022Document19 pages63760d18963d6a3c5708a7a4 - CC Token Whitepaper 17nov2022NayazNo ratings yet

- Letter of OfferDocument36 pagesLetter of OfferSamirHashimNo ratings yet

- Small Engines: Global Motorcycle Trends E-Mobility Trends Emissions Legislation Upgrades Motorcycle MarketDocument8 pagesSmall Engines: Global Motorcycle Trends E-Mobility Trends Emissions Legislation Upgrades Motorcycle MarketJahmia CoralieNo ratings yet

- Full Year 2021 Results: FEBRUARY 23, 2022Document58 pagesFull Year 2021 Results: FEBRUARY 23, 2022Jean Carlo Portales ChavezNo ratings yet

- OswalDocument13 pagesOswalPRIYANKA KNo ratings yet

- Stellantis FY 22 Results PresentationDocument60 pagesStellantis FY 22 Results Presentationpablo sanchez caballeroNo ratings yet

- Ccfa 2019 en Web v2Document102 pagesCcfa 2019 en Web v2ZULAIKHA BINTI MOHD ZULFIQRINo ratings yet

- Using Renewables For TrucksDocument30 pagesUsing Renewables For TrucksamolrNo ratings yet

- Euro 7 Emission StandardsDocument8 pagesEuro 7 Emission StandardsAYUSH RAINo ratings yet

- 2013 24 0150 - FinalDocument12 pages2013 24 0150 - FinalFranklin BoadaNo ratings yet

- Bahrain - Kuwait HFC Outlook VisualizationDocument32 pagesBahrain - Kuwait HFC Outlook VisualizationElias GomezNo ratings yet

- BASF CFO Commerzbank ODDO-BHF Corporate ConferenceDocument66 pagesBASF CFO Commerzbank ODDO-BHF Corporate ConferenceTorres LondonNo ratings yet

- The CDMDocument20 pagesThe CDMapi-3700769No ratings yet

- Dinodia 2018Document9 pagesDinodia 2018yourspajjuNo ratings yet

- Exhibit 4Document5 pagesExhibit 4MJNo ratings yet

- Enabling Commercial Vehicles To Move CleanerDocument3 pagesEnabling Commercial Vehicles To Move CleanerMASOUDNo ratings yet

- {20276E88-0000-C727-900D-BD75066C71D7}Document929 pages{20276E88-0000-C727-900D-BD75066C71D7}rashokprNo ratings yet

- Automotive Carbon Neutral Fuel Global Status and PotentialDocument22 pagesAutomotive Carbon Neutral Fuel Global Status and PotentialMohamad BachtiarNo ratings yet

- BMS Application and Inverter System Functional Safety Concepts For xEVsDocument35 pagesBMS Application and Inverter System Functional Safety Concepts For xEVsProvocateur SamaraNo ratings yet

- Oliver Wyman Australia NZ Case Competition Group Submission PDFDocument16 pagesOliver Wyman Australia NZ Case Competition Group Submission PDFMiku HatsuneNo ratings yet

- CDM Clean Development Mechanism PresentationDocument26 pagesCDM Clean Development Mechanism PresentationSam KurianNo ratings yet

- Roland Berger Study Extract Powertrain Component Outlook 2030Document17 pagesRoland Berger Study Extract Powertrain Component Outlook 2030Manu TecNo ratings yet

- WWH Obd Final Rev1 2Document101 pagesWWH Obd Final Rev1 2PECABANo ratings yet

- Future Trends in Automotive Industry and Challenges: Confidential CDocument20 pagesFuture Trends in Automotive Industry and Challenges: Confidential CSreejith S NairNo ratings yet

- Roland Berger Disruption Off Highway IndustryDocument12 pagesRoland Berger Disruption Off Highway IndustrySiraj ShaikhNo ratings yet

- 1-1 - Presentation of CBAM Taiwan April 23Document29 pages1-1 - Presentation of CBAM Taiwan April 23陳鼎元No ratings yet

- Al Alamein Teaser v5Document15 pagesAl Alamein Teaser v5E BNo ratings yet

- How Hydrogen Combustion Engines Can Contribute To Zero EmissionsDocument7 pagesHow Hydrogen Combustion Engines Can Contribute To Zero EmissionsMiguel SantosNo ratings yet

- xEV Inverter Solution With An Inductive Position Sensor Application Model and Software PDFDocument46 pagesxEV Inverter Solution With An Inductive Position Sensor Application Model and Software PDFkrishrohanNo ratings yet

- FAO On Carbon MarketDocument7 pagesFAO On Carbon MarketSayaka TsugaiNo ratings yet

- Evolution of The CDM: Toward 2012 and BeyondDocument13 pagesEvolution of The CDM: Toward 2012 and BeyondSaurav GuptaNo ratings yet

- 210803 - Auto Market TrendDocument25 pages210803 - Auto Market Trendshivaguru venkatramanNo ratings yet

- Roland Berger Li Ion Batteries Bubble Bursts 20121019Document16 pagesRoland Berger Li Ion Batteries Bubble Bursts 20121019ashoho1No ratings yet

- Costamp Group positioned as European leader in die casting marketDocument17 pagesCostamp Group positioned as European leader in die casting marketFARANo ratings yet

- © Oecd/Iea - Oecd/Nea 2015Document21 pages© Oecd/Iea - Oecd/Nea 2015Febrian AdiputraNo ratings yet

- Financial Evaluation of PV Solar ProjectsDocument76 pagesFinancial Evaluation of PV Solar Projectsalex_feryando42No ratings yet

- Powertrain 2020Document42 pagesPowertrain 2020sadananda_pvcNo ratings yet

- Automotive Engineering 2025: Five Key ChallengesDocument12 pagesAutomotive Engineering 2025: Five Key ChallengesNissam SidheeqNo ratings yet

- KPIT Technologies - GSDocument49 pagesKPIT Technologies - GSchetankvora0% (1)

- Roel HoendersDocument17 pagesRoel Hoendersxmaxrider1 bbmjNo ratings yet

- MEPC 76 Webinar Presentation FINALDocument31 pagesMEPC 76 Webinar Presentation FINALeconmechNo ratings yet

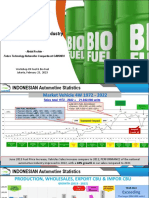

- Indonesia's Automotive Industry Focusing on Low Carbon Emissions and Sustainable FuelsDocument13 pagesIndonesia's Automotive Industry Focusing on Low Carbon Emissions and Sustainable FuelsMohamad BachtiarNo ratings yet

- LTATF TATASTEEL PresentationDocument8 pagesLTATF TATASTEEL PresentationKiranNo ratings yet

- 欧美发动机技术发展路线Document32 pages欧美发动机技术发展路线blueseatxNo ratings yet

- WindDocument12 pagesWindshashisastryNo ratings yet

- DNV GL Complete-Alt-Fuels Guidance Paper 2018-04 WebDocument44 pagesDNV GL Complete-Alt-Fuels Guidance Paper 2018-04 WebGeorge KanellakisNo ratings yet

- The Korea Emissions Trading Scheme: Challenges and Emerging OpportunitiesFrom EverandThe Korea Emissions Trading Scheme: Challenges and Emerging OpportunitiesNo ratings yet

- Reaching Zero with Renewables: Biojet FuelsFrom EverandReaching Zero with Renewables: Biojet FuelsNo ratings yet

- Carbon Offsetting in International Aviation in Asia and the Pacific: Challenges and OpportunitiesFrom EverandCarbon Offsetting in International Aviation in Asia and the Pacific: Challenges and OpportunitiesNo ratings yet

- GGH1502 Assignment1&2 001 2021 3 BDocument28 pagesGGH1502 Assignment1&2 001 2021 3 BDanielle Toni Dee NdlovuNo ratings yet

- ISPE Good Practice Guide and Compressed AirDocument5 pagesISPE Good Practice Guide and Compressed Airqac gmpNo ratings yet

- Test Unit 7Document6 pagesTest Unit 7quynhNo ratings yet

- ELC590 Persuassive Speech Course OutlineDocument4 pagesELC590 Persuassive Speech Course OutlineAdam ShamsuNo ratings yet

- Prevention and Management of Environment Health IssuesDocument14 pagesPrevention and Management of Environment Health IssuesJoy GundayNo ratings yet

- Marine - Diesel Fuel Lube Oil - Main Engine - Supply Vessel - Far Solitaire - CCMA7037UKDocument1 pageMarine - Diesel Fuel Lube Oil - Main Engine - Supply Vessel - Far Solitaire - CCMA7037UKFlota PacualesNo ratings yet

- Lesson 2 - Environmental Problems, Their Causes and SustainabilityDocument43 pagesLesson 2 - Environmental Problems, Their Causes and SustainabilityBlessie Ysavyll SaballeNo ratings yet

- Republic Act 9275: An Act Providing For A Comprehensive Water Quality Management and For Other PurposesDocument21 pagesRepublic Act 9275: An Act Providing For A Comprehensive Water Quality Management and For Other PurposesHercules OlañoNo ratings yet

- FILMTEC™ SW30-4040 Membranes: FeaturesDocument2 pagesFILMTEC™ SW30-4040 Membranes: FeaturesAlejandro AliNo ratings yet

- Petronas Technical Standards: Drainage & Sewer Systems For Onshore FacilitiesDocument52 pagesPetronas Technical Standards: Drainage & Sewer Systems For Onshore FacilitiesvinothNo ratings yet

- Renewable Energy Resources: Textile ProcessingDocument17 pagesRenewable Energy Resources: Textile ProcessingrohithNo ratings yet

- Dec 21 2022 - EPA - Response - Sewage Crisis Culebra - Contact Milton Diaz Email Address - Gmail - RE - AAA EMERGENCY CulebraDocument19 pagesDec 21 2022 - EPA - Response - Sewage Crisis Culebra - Contact Milton Diaz Email Address - Gmail - RE - AAA EMERGENCY CulebraCORALationsNo ratings yet

- Ground Floor Supply Layout: Potable Hot & Cold General PlumbingDocument1 pageGround Floor Supply Layout: Potable Hot & Cold General PlumbingDanny ArimaNo ratings yet

- Report - Bogi Manish Kumar - PTS-05Document63 pagesReport - Bogi Manish Kumar - PTS-05Sai Prasad GoudNo ratings yet

- Mobile Vendors j22Document20 pagesMobile Vendors j22belgacemmariembNo ratings yet

- Facilitating Linkage of Heterogeneous Regional, National and Sub-National Climate Policies Through A Future International AgreementDocument63 pagesFacilitating Linkage of Heterogeneous Regional, National and Sub-National Climate Policies Through A Future International AgreementhaileyuNo ratings yet

- Biodiversity and Species ExtinctionDocument14 pagesBiodiversity and Species ExtinctionJunriel Arig BonachitaNo ratings yet

- Fuel System: EmissionsDocument8 pagesFuel System: EmissionsMohammed BasionyNo ratings yet

- Lesson 3 Drainage SystemDocument45 pagesLesson 3 Drainage SystemkimchhoungNo ratings yet

- Mark Anderson MTU Tier 2 EmissionsDocument24 pagesMark Anderson MTU Tier 2 Emissionscristian picadoNo ratings yet

- Chemical Agent Resistant Coating (CARC) : MilsprayDocument6 pagesChemical Agent Resistant Coating (CARC) : Milspraybitconcepts9781No ratings yet

- CV - Environmental - Top - EEM - BrochureDocument8 pagesCV - Environmental - Top - EEM - BrochureLandryNo ratings yet

- Chapter 10 Environmental SustainabilityDocument43 pagesChapter 10 Environmental Sustainabilityintan syaheeraNo ratings yet

- GGGI 2020 Going Green - Electric Bus Fleet Feasibility StudyDocument109 pagesGGGI 2020 Going Green - Electric Bus Fleet Feasibility StudyAmul ShresthaNo ratings yet

- Pollution Under Control Certificate: Form 59Document1 pagePollution Under Control Certificate: Form 59Subhash PaulNo ratings yet

- TSD - GHG Mitigation Measures For Combustion TurbinesDocument30 pagesTSD - GHG Mitigation Measures For Combustion TurbinesMuhammad Redzwan Bin IsmailNo ratings yet

- Legends: Nickel Smelter Plant - PT Macika Mineral IndustriDocument1 pageLegends: Nickel Smelter Plant - PT Macika Mineral IndustriAditya RahmanNo ratings yet

- Emmanuel’s Resort water usage and pollution preventionDocument4 pagesEmmanuel’s Resort water usage and pollution preventionBryan LluismaNo ratings yet

- Motivation For Recycling Solid Waste and Exploration of Regulatory Framework: A Case Study of NamibiaDocument9 pagesMotivation For Recycling Solid Waste and Exploration of Regulatory Framework: A Case Study of NamibiaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Economic Benefits of Cleaning Up The ChesapeakeDocument56 pagesEconomic Benefits of Cleaning Up The Chesapeakewamu885No ratings yet