You might also like

- Module 3 Calculus (Derivatives of Functions)Document16 pagesModule 3 Calculus (Derivatives of Functions)Michael AliagaNo ratings yet

- ILMP Grade 1 Unit 1 Lesson 1 Period 1Document2 pagesILMP Grade 1 Unit 1 Lesson 1 Period 1xuxunguyen100% (4)

- Planning and Configuring Message TransportDocument33 pagesPlanning and Configuring Message TransportSheriff deenNo ratings yet

- RF 265 266 Ab Samsung Refri PDFDocument107 pagesRF 265 266 Ab Samsung Refri PDFaderlochNo ratings yet

- Lecture 7Document13 pagesLecture 7Aliza FatymaNo ratings yet

- BenchTree BrochureDocument28 pagesBenchTree BrochureMichael martinez100% (1)

- DC Power Source EPU05A-03 - HuaweiDocument11 pagesDC Power Source EPU05A-03 - HuaweiKozics Tibi0% (1)

- Brush Dax Generadores Dax - 2 - PoleDocument4 pagesBrush Dax Generadores Dax - 2 - PoleHernan GirautNo ratings yet

- ISO IEC 17025 Sample Forms PDFDocument5 pagesISO IEC 17025 Sample Forms PDFsumaira100% (1)

- P2 Chp7 DifferentiationDocument45 pagesP2 Chp7 DifferentiationMahmoud HeshamNo ratings yet

- Lesson 8 Integration by Parts & Algebraic SubstitutionDocument19 pagesLesson 8 Integration by Parts & Algebraic SubstitutionMarvin James JaoNo ratings yet

- Seminar 7 Differential EquationsDocument23 pagesSeminar 7 Differential EquationsDaniele NaddeoNo ratings yet

- Lecture 04Document38 pagesLecture 04bensonwong427No ratings yet

- Seminar 4 OptimisationDocument25 pagesSeminar 4 OptimisationDaniele NaddeoNo ratings yet

- Lesson 1Document33 pagesLesson 1Matt GeoligaoNo ratings yet

- Chapter 5+6Document31 pagesChapter 5+6digiy40095No ratings yet

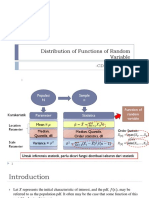

- Pertemuan1-Distribution of Functions of Random Variable-CDFDocument14 pagesPertemuan1-Distribution of Functions of Random Variable-CDFnauNo ratings yet

- Continuous Probability Distribution: Business Statistics Prepared By: Ikram-E-KhudaDocument31 pagesContinuous Probability Distribution: Business Statistics Prepared By: Ikram-E-KhudaAsharNo ratings yet

- 4.taylor ExpansionDocument15 pages4.taylor Expansion刘伟轩No ratings yet

- Functions 1.1 Functions As Mathematical ModelsDocument13 pagesFunctions 1.1 Functions As Mathematical Modelsarajara16No ratings yet

- Concepts On Rational FunctionDocument39 pagesConcepts On Rational FunctionZapanta, Andreine Ashley - LOVENo ratings yet

- Differentiation of Differential Coefficient: Let y Be A Function of X I.E. y F (X), LetDocument5 pagesDifferentiation of Differential Coefficient: Let y Be A Function of X I.E. y F (X), LetMeghaNo ratings yet

- Lesson 7 Transformation by Trigonometric FormulasDocument14 pagesLesson 7 Transformation by Trigonometric FormulasMarvin James JaoNo ratings yet

- Activity: "Everything in Moderation."Document14 pagesActivity: "Everything in Moderation."MAEZEL ASHLEY FREDELUCESNo ratings yet

- CHP 4 ActivitiesDocument7 pagesCHP 4 ActivitiesBennyNo ratings yet

- Week 3. K-Nearest Neighbours (KNN) : Dr. Shuo WangDocument18 pagesWeek 3. K-Nearest Neighbours (KNN) : Dr. Shuo WangMahmoud SolimanNo ratings yet

- Lecture 5Document6 pagesLecture 5Debayan BiswasNo ratings yet

- FAI 4 Mathematical Concepts IIDocument39 pagesFAI 4 Mathematical Concepts IIzhipengyang0110No ratings yet

- Linear Algebra, Numerical and Complex AnalysisDocument55 pagesLinear Algebra, Numerical and Complex AnalysisFayizNo ratings yet

- MATH 20063wk5Document18 pagesMATH 20063wk5Reyziel BarganNo ratings yet

- Lec10 11 12 13 14Document31 pagesLec10 11 12 13 14nishatur.rahman01No ratings yet

- Continuous Random VariablesDocument2 pagesContinuous Random Variableshernandezmaverick123No ratings yet

- Complex Functions & Mappings: 8023010-4: Advanced Engineering MathematicsDocument20 pagesComplex Functions & Mappings: 8023010-4: Advanced Engineering MathematicsHatem QUNo ratings yet

- 2022 - Mas 102 Cat 2Document1 page2022 - Mas 102 Cat 2william joabNo ratings yet

- EEP312 Chapter 5 Numerical DifferentiationDocument26 pagesEEP312 Chapter 5 Numerical DifferentiationLemonade TVNo ratings yet

- Tier 3 Practice TestDocument5 pagesTier 3 Practice TestMarcos RengifoNo ratings yet

- Inverse of A FunctionDocument14 pagesInverse of A FunctionSamantha Jasmine LimNo ratings yet

- Ceit DEDocument69 pagesCeit DEClint MosenabreNo ratings yet

- Prepared By: Mary Grace E. Butac: Lesson PlanDocument5 pagesPrepared By: Mary Grace E. Butac: Lesson PlanNornie MicsNo ratings yet

- Lekcija 5 - VjerovatnocaDocument60 pagesLekcija 5 - VjerovatnocaАнђела МијановићNo ratings yet

- 2 Discrete Random Variable Probability Distributions 2Document28 pages2 Discrete Random Variable Probability Distributions 2William TsuiNo ratings yet

- ISYE 6669 Homework 15 Fall 2021 PDFDocument3 pagesISYE 6669 Homework 15 Fall 2021 PDFEhxan HaqNo ratings yet

- Bacal 7Document23 pagesBacal 7MAEZEL ASHLEY FREDELUCESNo ratings yet

- Discrete Random Variables: IntegralDocument7 pagesDiscrete Random Variables: IntegralKanchana RandallNo ratings yet

- Seminar 2Document21 pagesSeminar 2hiyaxem683No ratings yet

- Cart and Pendulum ReformulationDocument3 pagesCart and Pendulum ReformulationEmanuel Morales RergisNo ratings yet

- Limit (Lec # 6)Document42 pagesLimit (Lec # 6)Hamid RajpootNo ratings yet

- Statistics: Assignment 3Document8 pagesStatistics: Assignment 3Houcem Bn SalemNo ratings yet

- Partial Differentiation and Its ApplicationsDocument26 pagesPartial Differentiation and Its ApplicationsMidhun MNo ratings yet

- Lec # 10 (LAGRANGES INTERPOLATION) PDFDocument20 pagesLec # 10 (LAGRANGES INTERPOLATION) PDFJunaid KaleemNo ratings yet

- CALCULUS 2 - Module1Document13 pagesCALCULUS 2 - Module1Zeiin ShionNo ratings yet

- M9 - Q1 W3 - Equations Transformable To Quadratic Equations PDFDocument32 pagesM9 - Q1 W3 - Equations Transformable To Quadratic Equations PDFmark hernandezNo ratings yet

- P2 Chp8 IntegrationDocument35 pagesP2 Chp8 IntegrationMahmoud HeshamNo ratings yet

- Ch-4 - Introduction To CalculusDocument51 pagesCh-4 - Introduction To Calculus5hbsb7mc68No ratings yet

- Lesson 1 - FunctionsDocument35 pagesLesson 1 - FunctionsMegane LeeNo ratings yet

- Lesson 1 - FunctionsDocument35 pagesLesson 1 - FunctionsQyndel Zach BiadoNo ratings yet

- Econ 131 Problem Set 1Document3 pagesEcon 131 Problem Set 1Tricia KiethNo ratings yet

- 10.1 Introduction To Complex NumbersDocument44 pages10.1 Introduction To Complex NumbersasfafafNo ratings yet

- Lecture 3Document5 pagesLecture 3Debayan BiswasNo ratings yet

- Rectangular MethodDocument13 pagesRectangular MethodAsder RedNo ratings yet

- G10 Math Q2 Module-1Document24 pagesG10 Math Q2 Module-1L. RikaNo ratings yet

- Tangent Line and Derivative Theorems of DifferentiationDocument24 pagesTangent Line and Derivative Theorems of Differentiationmabaylan.jebbrio214No ratings yet

- Lecture 2Document5 pagesLecture 2Debayan BiswasNo ratings yet

- Self Learning Module Basic Calculus q3 Week5Document24 pagesSelf Learning Module Basic Calculus q3 Week5Kayrell AquinoNo ratings yet

- Whole Brain Learning System Outcome-Based Education: Senior High School Grade Basic CalculusDocument32 pagesWhole Brain Learning System Outcome-Based Education: Senior High School Grade Basic CalculusKayrell AquinoNo ratings yet

- 2.2 Quadratic Equations Graphs Quadratic FunctionsDocument52 pages2.2 Quadratic Equations Graphs Quadratic FunctionsMbocaBentoNo ratings yet

- Module in Teaching and Learning 1 CHAPTER 1 1Document28 pagesModule in Teaching and Learning 1 CHAPTER 1 1Michel Jay Arguelles EspulgarNo ratings yet

- Used To Exercises Grammar Drills Grammar Guides - 73036Document2 pagesUsed To Exercises Grammar Drills Grammar Guides - 73036Gisela AlvesNo ratings yet

- Coriolis ForceDocument3 pagesCoriolis ForceDipanjan ChaudhuriNo ratings yet

- As Built Quotation ComputationDocument4 pagesAs Built Quotation ComputationIcedTea 71oNo ratings yet

- Mono RailsDocument23 pagesMono RailsRanjith KumarNo ratings yet

- Unit 9B Acceleration Diagrams: Anaiy818 8lngi0 and Oompwnd Link# in Planar MotionDocument13 pagesUnit 9B Acceleration Diagrams: Anaiy818 8lngi0 and Oompwnd Link# in Planar MotionSubramanian ChidambaramNo ratings yet

- Ada Lovelace Lesson PlanDocument3 pagesAda Lovelace Lesson PlanTony AppsNo ratings yet

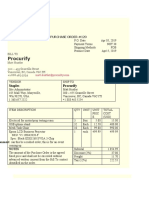

- 6400 - File - LATIHAN SOAL FORM TEKS PURCHASE ORDER X IPA IPSDocument3 pages6400 - File - LATIHAN SOAL FORM TEKS PURCHASE ORDER X IPA IPSKayla SimphonyNo ratings yet

- Federal Urdu University of Arts, Science and Technology, IslamabadDocument4 pagesFederal Urdu University of Arts, Science and Technology, IslamabadQasim Jahangir WaraichNo ratings yet

- First Law of Thermodynamics 1580126216698243765e2ed008943f7Document3 pagesFirst Law of Thermodynamics 1580126216698243765e2ed008943f7Atul YadavNo ratings yet

- Tech Roaster Oct DBMS 2017Document15 pagesTech Roaster Oct DBMS 2017pankaj aggarwalNo ratings yet

- Elizabeth Johnson Resume 2022Document1 pageElizabeth Johnson Resume 2022api-558219272No ratings yet

- Wire Rope Splice Details "BB"Document1 pageWire Rope Splice Details "BB"JUAN RULFONo ratings yet

- Contator - D Catalogo 2009 en PDFDocument56 pagesContator - D Catalogo 2009 en PDFJailson RibeiroNo ratings yet

- BullwhipDocument40 pagesBullwhipAngsuman BhanjdeoNo ratings yet

- Tanuj Kumar Majumdar (Optical) Roll-03Document24 pagesTanuj Kumar Majumdar (Optical) Roll-03Tanuj MajumdarNo ratings yet

- VinodhDocument4 pagesVinodhapi-511841129No ratings yet

- Simatic Net: Installation InstructionsDocument35 pagesSimatic Net: Installation InstructionssanjayswtNo ratings yet

- Ramesh 5yr Experience...Document5 pagesRamesh 5yr Experience...Ramesh PandaNo ratings yet

- Troy Bruchwalski: Union Affiliation: (412) 527 - 7602 Height: 6'2'' Weight: 185 LbsDocument2 pagesTroy Bruchwalski: Union Affiliation: (412) 527 - 7602 Height: 6'2'' Weight: 185 Lbsapi-280100346No ratings yet

- 8 Kable Mono I Bipolarne Mono and Bipolar CablesDocument4 pages8 Kable Mono I Bipolarne Mono and Bipolar CablesAbu QisronNo ratings yet

- The Dissociation & The Surprise of Haruhi SuzumiyaDocument583 pagesThe Dissociation & The Surprise of Haruhi SuzumiyaMuphridNo ratings yet

- Letter of Transmittal: Subject: Submission of Internship Report On Financial Performance of SonaliDocument11 pagesLetter of Transmittal: Subject: Submission of Internship Report On Financial Performance of SonalijehanNo ratings yet