You might also like

- Accounting - First Year Course, Interactive Student EditionDocument984 pagesAccounting - First Year Course, Interactive Student Editionfukfdg dhjk100% (1)

- A Brief History of PortugalDocument8 pagesA Brief History of PortugalPinto da Cruz100% (1)

- Government Service Insurance System v. CADocument1 pageGovernment Service Insurance System v. CAMan2x SalomonNo ratings yet

- Androa Asenua V UgandaDocument30 pagesAndroa Asenua V UgandaAloro Abdul Hakim BonaparteNo ratings yet

- JURISPRUDENCEDocument16 pagesJURISPRUDENCEKrizel Manangit ConcepcionNo ratings yet

- 2018-2019 Sbi StatementDocument9 pages2018-2019 Sbi StatementPower MuruganNo ratings yet

- Account - Statement - PDF - 1200011199762 - 29 April 2019 PDFDocument2 pagesAccount - Statement - PDF - 1200011199762 - 29 April 2019 PDFIqbalMuhamad100% (2)

- Account Statement PDFDocument3 pagesAccount Statement PDFSagar VlogsNo ratings yet

- C FSPPs RK Y4 e ARq RIDocument7 pagesC FSPPs RK Y4 e ARq RIMD RafiqNo ratings yet

- Circular On FlexiesDocument26 pagesCircular On FlexiesRaghu RamNo ratings yet

- Amrita International V Principal CommissionerDocument54 pagesAmrita International V Principal Commissionerபூவை ஜெ ரூபன்சார்லஸ்No ratings yet

- W.p.no.6913 of 2019 Dated 11.03.2020 JudgementDocument100 pagesW.p.no.6913 of 2019 Dated 11.03.2020 JudgementSiddharth TMNo ratings yet

- The Honourable MR - Justice M.S.Ramesh: W.P. (MD) No.11718 of 2022Document5 pagesThe Honourable MR - Justice M.S.Ramesh: W.P. (MD) No.11718 of 2022Senthilvel PandianNo ratings yet

- Mfa156 19 12 04 2023Document5 pagesMfa156 19 12 04 2023Bharath AdvocateNo ratings yet

- 6045 2020 33 1501 24390 Judgement 16-Oct-2020Document53 pages6045 2020 33 1501 24390 Judgement 16-Oct-2020PdpNo ratings yet

- W.P.Nos.32418 & 32420 of 2023Document6 pagesW.P.Nos.32418 & 32420 of 2023durai kathirNo ratings yet

- CaritasDocument185 pagesCaritasSatyam PathakNo ratings yet

- Director Disqualification Judgment PDFDocument614 pagesDirector Disqualification Judgment PDFlakshmimenon39No ratings yet

- Jawaban QuizDocument2 pagesJawaban QuizWahidiyah Indah LestariNo ratings yet

- Input Tax Credit Cannot Be Denied To Purchaser Merely Because Seller Didnt Record Transaction in GSTR-2A Form - Kerala High CourtDocument9 pagesInput Tax Credit Cannot Be Denied To Purchaser Merely Because Seller Didnt Record Transaction in GSTR-2A Form - Kerala High CourtdeepakasopaNo ratings yet

- Transaction Details: PrintDocument2 pagesTransaction Details: PrintRavindra GuptaNo ratings yet

- India SirimathyDocument23 pagesIndia SirimathyCamila CampilloNo ratings yet

- 'CL 2021 22 (1) 3Document24 pages'CL 2021 22 (1) 3aakash jainNo ratings yet

- State of UP V Sudhir Kumar Singh - Right To Be HeardDocument53 pagesState of UP V Sudhir Kumar Singh - Right To Be HeardShovit BetalNo ratings yet

- Claim Form CA Prashant KumarDocument6 pagesClaim Form CA Prashant Kumarjoshinachiket.jlcNo ratings yet

- WP8592 2023 Case IntordDocument4 pagesWP8592 2023 Case IntordK.P. SarmaNo ratings yet

- Jayant-Etc.-Vs-State-of-Madhya-Pradesh-Supreme-Court Ipc379 and 414Document43 pagesJayant-Etc.-Vs-State-of-Madhya-Pradesh-Supreme-Court Ipc379 and 414Biju SebastianNo ratings yet

- Kapaga Selvi Direction 20.11.2023Document8 pagesKapaga Selvi Direction 20.11.2023shahithNo ratings yet

- DownloadedDocument16 pagesDownloadedK RamakrishnanNo ratings yet

- Judgement Jayavilas Tobacco Case Appeal 2093 (2018) PDFDocument48 pagesJudgement Jayavilas Tobacco Case Appeal 2093 (2018) PDFAthiban VijayNo ratings yet

- Maa Kali Farms & FeedsDocument11 pagesMaa Kali Farms & FeedsK SANMUKHA PATRANo ratings yet

- W.P.No.33528 of 2023Document6 pagesW.P.No.33528 of 2023durai kathirNo ratings yet

- WP - 22739 - 2022 - Interim 1Document4 pagesWP - 22739 - 2022 - Interim 1Abhijeet TalwarNo ratings yet

- Can Suspend EmployeeDocument34 pagesCan Suspend EmployeeSree Vidya SaravananNo ratings yet

- The Hon'Ble Mr. Justice K.Ravichandrabaabu: W.P.No.26187 of 2019Document10 pagesThe Hon'Ble Mr. Justice K.Ravichandrabaabu: W.P.No.26187 of 2019ACCTLVO 35No ratings yet

- G.O.Ms - No.: (By Order and in The Name of The Governor of Andhra Pradesh)Document1 pageG.O.Ms - No.: (By Order and in The Name of The Governor of Andhra Pradesh)Balu Mahendra SusarlaNo ratings yet

- DownloadedDocument26 pagesDownloadedMohanNo ratings yet

- Ys%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaDocument32 pagesYs%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaSanaka LogesNo ratings yet

- Matrukrupa SODDocument12 pagesMatrukrupa SODK SANMUKHA PATRANo ratings yet

- Esi JudgementDocument90 pagesEsi JudgementJayaguru CNo ratings yet

- V3 - Manoj Gaur HC Writ - Track ChangesDocument17 pagesV3 - Manoj Gaur HC Writ - Track ChangesAshutosh Kumar SinghNo ratings yet

- Form NDocument13 pagesForm Nsangeetha satheeshNo ratings yet

- BHC - Section 8 (4) - R.R Realtors Vs The State of Maharashtra & Ors. - 31 July 2023Document25 pagesBHC - Section 8 (4) - R.R Realtors Vs The State of Maharashtra & Ors. - 31 July 2023ashishs8577No ratings yet

- SafariDocument1 pageSafariKoteswara RaoNo ratings yet

- Shantharam Prabhu Vs Mr.K. Dayanand Rai On 8 September, 2021Document32 pagesShantharam Prabhu Vs Mr.K. Dayanand Rai On 8 September, 2021Kantaraj TavaneNo ratings yet

- Circular JT Registrar 2-3-21Document4 pagesCircular JT Registrar 2-3-21Vital ToolsNo ratings yet

- Group Insurnace SoftwareDocument23 pagesGroup Insurnace SoftwareA2 Section CollectorateNo ratings yet

- Display PDFDocument4 pagesDisplay PDFjithin prasannanNo ratings yet

- FinalLayoutLetter KeesaraDocument4 pagesFinalLayoutLetter Keesarafr4ffmywynNo ratings yet

- Yashodhara Shroff Vs Union of India On 12 June 2019Document406 pagesYashodhara Shroff Vs Union of India On 12 June 2019Abhilash GaurNo ratings yet

- WP 939Document4 pagesWP 939panruti industrial company pvt ltdNo ratings yet

- Maa Durga Agency-OCCDocument11 pagesMaa Durga Agency-OCCK SANMUKHA PATRANo ratings yet

- 2017 SCC OnLine Mad 4480 Obitor Dicta and Ratio DecedendiDocument31 pages2017 SCC OnLine Mad 4480 Obitor Dicta and Ratio DecedendikmdharanNo ratings yet

- Judgment ChidambaramDocument24 pagesJudgment ChidambaramThe Indian JuristNo ratings yet

- April 19 March 20 PDFDocument86 pagesApril 19 March 20 PDFMalik MuzafferNo ratings yet

- MFA 4402 - 2014 - Ravish Benni - 02-11-2023Document2 pagesMFA 4402 - 2014 - Ravish Benni - 02-11-2023ramkittiNo ratings yet

- Shri Narayani Nidhi LTD F55265870 20230203Document2 pagesShri Narayani Nidhi LTD F55265870 20230203prabakaran365No ratings yet

- Registrar Office Corr.Document5 pagesRegistrar Office Corr.Dilip ThoratNo ratings yet

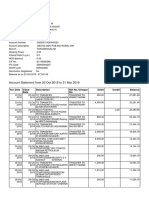

- Account Statement 14 Jun 2023-19 Jun 2023Document4 pagesAccount Statement 14 Jun 2023-19 Jun 2023propvisor real estateNo ratings yet

- DownloadedDocument4 pagesDownloadedVetri VendanNo ratings yet

- City Union MurughanDocument5 pagesCity Union MurughanloginidsenthilNo ratings yet

- Girija Plot No 11Document1 pageGirija Plot No 11Selva GaneshNo ratings yet

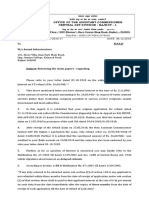

- Office of The Assistant Commissioner Central GST Division: Rajkot - IDocument2 pagesOffice of The Assistant Commissioner Central GST Division: Rajkot - INitish MittalNo ratings yet

- Klkiulm QDQ PK 4 SXDocument8 pagesKlkiulm QDQ PK 4 SXkarthickNo ratings yet

- Bureaucrats Disputed Bjp Government Ratification of Andrews Ganj Land ScamFrom EverandBureaucrats Disputed Bjp Government Ratification of Andrews Ganj Land ScamNo ratings yet

- Main Grant Guidelines: African Women's Development FundDocument3 pagesMain Grant Guidelines: African Women's Development FundItélioMuchisseNo ratings yet

- National Service Training Program 1 - CWTS 3 Units Prerequisite: NoneDocument3 pagesNational Service Training Program 1 - CWTS 3 Units Prerequisite: NoneJamesluis PartosaNo ratings yet

- IYCN Agents of Change - 2009 ReportDocument27 pagesIYCN Agents of Change - 2009 ReportChaitanya KumarNo ratings yet

- Loctite SF 770: Product DescriptionDocument3 pagesLoctite SF 770: Product DescriptionNishant SenapatiNo ratings yet

- Media Trail Research PaperDocument7 pagesMedia Trail Research PaperShruti AgarwalNo ratings yet

- Rubric For Assessing Student Participation: Developing (70%-80%) Unacceptable ( 70%) Frequency of Participation in ClassDocument1 pageRubric For Assessing Student Participation: Developing (70%-80%) Unacceptable ( 70%) Frequency of Participation in ClassJXDZ. TVNo ratings yet

- Switzerland Became A Neutral Country in The World WarDocument3 pagesSwitzerland Became A Neutral Country in The World WarFauziNo ratings yet

- (Quiz 2-ANSWER) ULLC1003 - 202005Document6 pages(Quiz 2-ANSWER) ULLC1003 - 202005Jessie PcdNo ratings yet

- Form15h GH01389401 PDFDocument3 pagesForm15h GH01389401 PDFNamme KyarakhahaiNo ratings yet

- SDSDSDDocument2 pagesSDSDSDPascuala MallillinNo ratings yet

- The Turkish Embassy Letters 발제 최종Document6 pagesThe Turkish Embassy Letters 발제 최종지민No ratings yet

- Ar 414 Professional Practice 3Document14 pagesAr 414 Professional Practice 3JAMES LLOYD ANTHONY CONCHANo ratings yet

- 001 Application For Notarial CommissionDocument4 pages001 Application For Notarial CommissionSam LagoNo ratings yet

- The Mah Welfare Officers (D, Q and CoS) Rules, 1966Document14 pagesThe Mah Welfare Officers (D, Q and CoS) Rules, 1966Nanmathi Balachandran 10G 21No ratings yet

- CPEC and Regional IntegrationDocument10 pagesCPEC and Regional IntegrationM MustafaNo ratings yet

- Story Tenali TextDocument43 pagesStory Tenali Textmohammad karishmaNo ratings yet

- Basic GAD ConceptsDocument26 pagesBasic GAD ConceptsCarl Laura ClimacoNo ratings yet

- Christie, Isham N.D. 'A Marxist Critique of John Rawl's 'Theory of Justice'' (12 PP.)Document12 pagesChristie, Isham N.D. 'A Marxist Critique of John Rawl's 'Theory of Justice'' (12 PP.)voxpop88No ratings yet

- Fitri Andalus Handayani & Mohamad Ichsana Nur 1 Implementasi Good Governance Di IndonesiaDocument11 pagesFitri Andalus Handayani & Mohamad Ichsana Nur 1 Implementasi Good Governance Di IndonesiaMeizy AnggunNo ratings yet

- TCS Corporate Sustainability Report 2011-12-3Document104 pagesTCS Corporate Sustainability Report 2011-12-3Chinmai HemaniNo ratings yet

- ENMG698c Lecture3Document62 pagesENMG698c Lecture3Joli SmithNo ratings yet

- Logical Framework TemplateDocument7 pagesLogical Framework Templateسمر مرادNo ratings yet

- Gender Studies ReferencesDocument6 pagesGender Studies Referencesmariamunir83No ratings yet

- Civ No 39 of 2000 PDFDocument10 pagesCiv No 39 of 2000 PDFherman gervasNo ratings yet

- Socialism For-Future Mini-LuXDocument89 pagesSocialism For-Future Mini-LuXCelya PhamNo ratings yet