You might also like

- XtxtnbregDocument13 pagesXtxtnbregalicorpanaoNo ratings yet

- Stata xtprobit guideDocument20 pagesStata xtprobit guidejc224No ratings yet

- XtxtmlogitDocument31 pagesXtxtmlogitAmoussouNo ratings yet

- RbetaregDocument10 pagesRbetaregBaron BulayaNo ratings yet

- Panel Data Regression with GLSDocument11 pagesPanel Data Regression with GLSNha LeNo ratings yet

- XtxtpcseDocument11 pagesXtxtpcsemuniya altezaNo ratings yet

- RfrontierDocument15 pagesRfrontierzainurihanifNo ratings yet

- RivregressDocument16 pagesRivregresskainaNo ratings yet

- Varlist: Robust - Robust Variance EstimatesDocument24 pagesVarlist: Robust - Robust Variance EstimatesAsep KusnaliNo ratings yet

- Robust - Robust Variance EstimatesDocument25 pagesRobust - Robust Variance Estimatessarbaz0003No ratings yet

- Time Series AnalysisDocument6 pagesTime Series AnalysisLibertyNo ratings yet

- CausaldidregressDocument35 pagesCausaldidregresseflitadataNo ratings yet

- Hausman - Hausman Specification TestDocument10 pagesHausman - Hausman Specification TestSaiganesh RameshNo ratings yet

- Xtregar - Fixed-And Random-Effects Linear Models With An AR (1) DisturbanceDocument15 pagesXtregar - Fixed-And Random-Effects Linear Models With An AR (1) DisturbanceDiego Armando Pérez ReséndizNo ratings yet

- Ayuda Comandos Stata MetaDocument42 pagesAyuda Comandos Stata Metaread03541No ratings yet

- Logit MultinomialDocument16 pagesLogit MultinomialBruno BaiaNo ratings yet

- PSF Models in StataDocument14 pagesPSF Models in StataalkrasNo ratings yet

- Suest - Seemingly Unrelated Estimation: 20 Estimation and Postestimation CommandsDocument19 pagesSuest - Seemingly Unrelated Estimation: 20 Estimation and Postestimation Commandseko abiNo ratings yet

- Stata Help Hausman Test PDFDocument9 pagesStata Help Hausman Test PDFHabib AhmadNo ratings yet

- Seemingly Unrelated Estimation with suestDocument19 pagesSeemingly Unrelated Estimation with suesteko abiNo ratings yet

- TsvarDocument12 pagesTsvartayson1212No ratings yet

- Poisson Regression in StataDocument10 pagesPoisson Regression in StataUNLV234No ratings yet

- RbiprobitDocument8 pagesRbiprobitDaniel Redel SaavedraNo ratings yet

- Clustsig RDocument7 pagesClustsig RSeverodvinsk MasterskayaNo ratings yet

- Genetic Algorithms and The Variance of Fitness: Ex EmsDocument14 pagesGenetic Algorithms and The Variance of Fitness: Ex EmspriyankaNo ratings yet

- Dynamic Panel Data Estimation and Modeling in StataDocument11 pagesDynamic Panel Data Estimation and Modeling in StataUttam GolderNo ratings yet

- Bivariate Probit RegressionDocument7 pagesBivariate Probit RegressionnovanikarineNo ratings yet

- Useful Stata Commands - 2012 PDFDocument2 pagesUseful Stata Commands - 2012 PDFroberthtaipevNo ratings yet

- Depvarlist If In: Vec - Vector Error-Correction ModelsDocument24 pagesDepvarlist If In: Vec - Vector Error-Correction ModelsAdalberto CalsinNo ratings yet

- RmprobitDocument8 pagesRmprobitlompoNo ratings yet

- Varlist If in Weight Options: Pca - Principal Component AnalysisDocument17 pagesVarlist If in Weight Options: Pca - Principal Component AnalysisclmarinNo ratings yet

- 17 UnionFindDocument53 pages17 UnionFindMuhammad BaqirNo ratings yet

- Week 5 - EViews Practice NoteDocument16 pagesWeek 5 - EViews Practice NoteChip choiNo ratings yet

- SVAR Model Specification and OptionsDocument19 pagesSVAR Model Specification and OptionsOğuzhan ÖzçelebiNo ratings yet

- Maximize Stata's ML EstimatorsDocument7 pagesMaximize Stata's ML EstimatorsMariia SungatullinaNo ratings yet

- Comparison of Non-Intrusive Polynomial Chaos and Stochastic Collocation MethodsDocument20 pagesComparison of Non-Intrusive Polynomial Chaos and Stochastic Collocation MethodsAlfredo Gonzalez SoteloNo ratings yet

- Conjugate PriorDocument7 pagesConjugate Priorbambey0% (1)

- RnpregresskernelDocument24 pagesRnpregresskernelDaniel Redel SaavedraNo ratings yet

- BayesbayesxtregDocument4 pagesBayesbayesxtregBelaynehYitayewNo ratings yet

- Eregress Predict - Predict After Eregress and XteregressDocument6 pagesEregress Predict - Predict After Eregress and XteregressBienvenu KakpoNo ratings yet

- Unit Root and Cointegration TestsDocument9 pagesUnit Root and Cointegration TestsFernando Perez SavadorNo ratings yet

- Conjugate Prior - WikipediaDocument6 pagesConjugate Prior - WikipediaAyanNo ratings yet

- ANOVA Cheat SheetDocument6 pagesANOVA Cheat Sheetvisualfn financeNo ratings yet

- Robust Control With Structured Perturbations: L.H. S.PDocument6 pagesRobust Control With Structured Perturbations: L.H. S.PkevincanNo ratings yet

- Tss SpaceDocument24 pagesTss SpaceJENNY MINAYANo ratings yet

- Ancient language reconstruction using probabilistic modelsDocument30 pagesAncient language reconstruction using probabilistic modelsANo ratings yet

- Which Test When: 1 Exploratory TestsDocument5 pagesWhich Test When: 1 Exploratory TestsAnonymous HIhW9DBNo ratings yet

- A Glossary of StatisticsDocument20 pagesA Glossary of StatisticskapilNo ratings yet

- Alignments & Phylogenetic Trees: Introduction to Sequence AlignmentDocument18 pagesAlignments & Phylogenetic Trees: Introduction to Sequence AlignmentSevs LorillaNo ratings yet

- Help for metafunnel plots meta-analysis biasDocument2 pagesHelp for metafunnel plots meta-analysis biasPedroNo ratings yet

- Comandos STATADocument10 pagesComandos STATAMiguel Hernandes JuniorNo ratings yet

- GLM, GAMs & GLLMs - An Overview of Theory For Applications in Fisheries Research, VENABLES, 2004Document19 pagesGLM, GAMs & GLLMs - An Overview of Theory For Applications in Fisheries Research, VENABLES, 2004Igor MonteiroNo ratings yet

- Estimating Dynamic Common Correlated Effects Models in StataDocument41 pagesEstimating Dynamic Common Correlated Effects Models in StataSAWADOGONo ratings yet

- 1-Way ANOVA Tests: The SettingDocument7 pages1-Way ANOVA Tests: The SettingKhushbuNo ratings yet

- Varlist If in Weight: Correlate - Correlations (Covariances) of Variables or CoefficientsDocument8 pagesVarlist If in Weight: Correlate - Correlations (Covariances) of Variables or CoefficientsRiazboniNo ratings yet

- Multinomial Logistic Regression Models: Newsom Psy 525/625 Categorical Data Analysis, Spring 2021 1Document5 pagesMultinomial Logistic Regression Models: Newsom Psy 525/625 Categorical Data Analysis, Spring 2021 1Deo TuremeNo ratings yet

- Generalized Linear ModelDocument9 pagesGeneralized Linear Modelharrison9No ratings yet

- Glossary SPSS StatisticsDocument6 pagesGlossary SPSS StatisticsDina ArjuNo ratings yet

- Backpropagation: Fundamentals and Applications for Preparing Data for Training in Deep LearningFrom EverandBackpropagation: Fundamentals and Applications for Preparing Data for Training in Deep LearningNo ratings yet

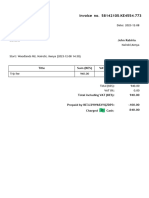

- Ride Invoice From Bolt 6Document1 pageRide Invoice From Bolt 6jminyosoNo ratings yet

- STATA GraphicsDocument35 pagesSTATA GraphicsjminyosoNo ratings yet

- STATA Data SummariesDocument15 pagesSTATA Data SummariesjminyosoNo ratings yet

- Session1 Output ManagementDocument13 pagesSession1 Output ManagementjminyosoNo ratings yet

- Exam 1 690C 2020 SOLUTIONS StataDocument6 pagesExam 1 690C 2020 SOLUTIONS StatajminyosoNo ratings yet

- Chapter9ppt PDFDocument32 pagesChapter9ppt PDFNasir IqbalNo ratings yet

- Concise explanations of probability concepts and formulasDocument481 pagesConcise explanations of probability concepts and formulasTara McTara83% (6)

- The Overuse of Mathematics in EconomicsDocument16 pagesThe Overuse of Mathematics in EconomicsShahbazAliMemonNo ratings yet

- R.hofer M-Point Invariants of Real GeometriesDocument6 pagesR.hofer M-Point Invariants of Real GeometriesEder Raul Huaccachi HuamaniNo ratings yet

- Data Structures Tutorial with SolutionsDocument5 pagesData Structures Tutorial with SolutionsSunitha BabuNo ratings yet

- June 2014 (R) MA - C3 EdexcelDocument9 pagesJune 2014 (R) MA - C3 EdexcelAmeenIbrahimNo ratings yet

- Computation CDocument8 pagesComputation CVeeno DarveenaNo ratings yet

- Exploring Negative Space: Log Cross Ratio 2iDocument11 pagesExploring Negative Space: Log Cross Ratio 2iSylvia Cheung100% (2)

- A NGLEDocument8 pagesA NGLEYashita JainNo ratings yet

- Solving Coupled System of Nonlinear PDE's Using The Natural Decomposition MethodDocument21 pagesSolving Coupled System of Nonlinear PDE's Using The Natural Decomposition MethodPrabal AcharyaNo ratings yet

- Chapter 3 Exponential and Logarithmic FunctionsDocument17 pagesChapter 3 Exponential and Logarithmic Functionsapi-3704862100% (4)

- S Announcement 35889Document4 pagesS Announcement 35889Xean MmtNo ratings yet

- 65 - C - 3 MathematicsDocument23 pages65 - C - 3 Mathematicsshadowanonymous069No ratings yet

- Research Paper Mathematics EducationDocument6 pagesResearch Paper Mathematics Educationfkqdnlbkf100% (1)

- Taylor Series Method, Euler's Method and Modified Euler's MethodDocument8 pagesTaylor Series Method, Euler's Method and Modified Euler's MethodSourav PaulNo ratings yet

- Algorithm W Step by Step: Martin Grabm UllerDocument7 pagesAlgorithm W Step by Step: Martin Grabm Uller简文章No ratings yet

- MidtermDocument1 pageMidtermNOV DAVANNNo ratings yet

- TOC and Compiler Design exam questionsDocument3 pagesTOC and Compiler Design exam questionsandrew0% (1)

- January 2017 QPDocument20 pagesJanuary 2017 QPbasilabdellatiefNo ratings yet

- Feedback control enables coexistence in two-species chemostat modelsDocument23 pagesFeedback control enables coexistence in two-species chemostat modelsCatalin TudoriuNo ratings yet

- 3RD TERM - Basic CalculusDocument8 pages3RD TERM - Basic CalculusAaliyah Reign SanchezNo ratings yet

- Topic 4 (Money) - Y4 09Document16 pagesTopic 4 (Money) - Y4 09Noorizan Mohd Esa0% (1)

- Math Polygons 1Document1 pageMath Polygons 1api-293358997No ratings yet

- Trading Systems and MethodsDocument5 pagesTrading Systems and Methodssanjay patidarNo ratings yet

- Relative-Motion Analysis of Two Particles Using Translating AxesDocument18 pagesRelative-Motion Analysis of Two Particles Using Translating AxesAtef NazNo ratings yet

- Part3Module2 PDFDocument15 pagesPart3Module2 PDFKAUSTAV BASAKNo ratings yet

- IAS PREVIOUS YEARS QUESTIONS ON ORDINARY DIFFERENTIAL EQUATIONS (2017-1983Document9 pagesIAS PREVIOUS YEARS QUESTIONS ON ORDINARY DIFFERENTIAL EQUATIONS (2017-1983Anonymous gViEc4100% (1)

- Quartic Equations - by Robert L. Ward, For The Math Forum Simplifying The EquationDocument4 pagesQuartic Equations - by Robert L. Ward, For The Math Forum Simplifying The EquationVijay AnandNo ratings yet

- Sampling TheoremDocument92 pagesSampling TheoremRahul SharmaNo ratings yet

- Wolfram - Alpha Activity - Topic, Real Numbers - Intermediate Algebra Activity 1Document3 pagesWolfram - Alpha Activity - Topic, Real Numbers - Intermediate Algebra Activity 1Pearson Math Stats100% (2)