You might also like

- Investment Pricing Methods: A Guide for Accounting and Financial ProfessionalsFrom EverandInvestment Pricing Methods: A Guide for Accounting and Financial ProfessionalsNo ratings yet

- 8 EFM Class 7 NPVDocument63 pages8 EFM Class 7 NPVSiu EricNo ratings yet

- Investment Decisions: (Capital Budgeting Techniques)Document69 pagesInvestment Decisions: (Capital Budgeting Techniques)Dharmesh GoyalNo ratings yet

- Financial Management Unit 3 DR Ashok KumarDocument65 pagesFinancial Management Unit 3 DR Ashok Kumarsk tanNo ratings yet

- Week 10 - 11 - Investment Appraisal TechniquesDocument15 pagesWeek 10 - 11 - Investment Appraisal TechniquesJoshua NemiNo ratings yet

- Session 11 Short Term FinancingDocument22 pagesSession 11 Short Term FinancingSakshi VermaNo ratings yet

- FIN 200 The Basics of Capital Budgeting Topic 3 2021Document6 pagesFIN 200 The Basics of Capital Budgeting Topic 3 2021RonaldNo ratings yet

- Capital BudgetingDocument26 pagesCapital BudgetingGowryshankar SumatharanNo ratings yet

- Corp Fin Session 15-16-17 Capital Budgeting TechniquesDocument55 pagesCorp Fin Session 15-16-17 Capital Budgeting TechniquesMona SethNo ratings yet

- Capital Budgeting DetailDocument64 pagesCapital Budgeting DetailDEV BHADANANo ratings yet

- ECO280 Chapter5Document86 pagesECO280 Chapter5Orkun AkyolNo ratings yet

- Chap05 FMDocument42 pagesChap05 FMDil RRNo ratings yet

- Chapter-8 Cap Bud ReportDocument7 pagesChapter-8 Cap Bud ReportGrazielle DiazNo ratings yet

- CH 10Document76 pagesCH 10Nguyen Ngoc Minh Chau (K15 HL)No ratings yet

- Capital BudgetingDocument14 pagesCapital BudgetingRianne NavidadNo ratings yet

- Cem-803: Economic Decision Analysis in ConstructionDocument52 pagesCem-803: Economic Decision Analysis in Constructionaneeqa sikanderNo ratings yet

- Capital Budgeting and Long-Term FinanceDocument28 pagesCapital Budgeting and Long-Term FinanceJamshidNo ratings yet

- Capital Investment DecisionspptDocument24 pagesCapital Investment DecisionspptDeepika PantNo ratings yet

- Chapter 12Document2 pagesChapter 12Mikasa MikasaNo ratings yet

- CH 10Document74 pagesCH 10Chi NguyễnNo ratings yet

- Chapter 6 - Capital Investment Decisions and Other Corporate PoliciesDocument11 pagesChapter 6 - Capital Investment Decisions and Other Corporate Policiesthuypham.31221027049No ratings yet

- Lecture 9 Invest AppDocument14 pagesLecture 9 Invest AppTshidiso KgosiemangNo ratings yet

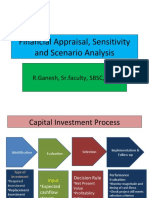

- Financial Appraisal, Sensitivity and Scenario Analysis: R.Ganesh, SR - Faculty, SBSC, HydDocument25 pagesFinancial Appraisal, Sensitivity and Scenario Analysis: R.Ganesh, SR - Faculty, SBSC, HydHinaAbbasNo ratings yet

- SBEQ 4452 Economic Feasibility StudyDocument20 pagesSBEQ 4452 Economic Feasibility StudySHARIFAH NOR SUBAIHAH BT SYED MOHAMMAD SABRI B18BE0065No ratings yet

- Chapter 9Document14 pagesChapter 9hadassahhadidNo ratings yet

- MGFB10 CapitalBudgetingRules Chapter7 NotesDocument58 pagesMGFB10 CapitalBudgetingRules Chapter7 NotesnigaroNo ratings yet

- Unit 3 Capital BudgetingDocument34 pagesUnit 3 Capital BudgetingRishikesh MundekarNo ratings yet

- Profitability AnalysisDocument13 pagesProfitability AnalysisAndrelyn NavaltaNo ratings yet

- Capital Budgeting - Theory & PracticeDocument41 pagesCapital Budgeting - Theory & PracticevikrammendaNo ratings yet

- Capital BudgetingDocument30 pagesCapital BudgetingAbdullah ZakariyyaNo ratings yet

- Chapter 6Document16 pagesChapter 6Renese LeeNo ratings yet

- Capital Budgeting - EvaluationDocument47 pagesCapital Budgeting - Evaluationpranav1931129No ratings yet

- Working Capital ManagementDocument8 pagesWorking Capital ManagementMariell PenaroyoNo ratings yet

- Chapter 5-Project AppraisalDocument49 pagesChapter 5-Project AppraisalAklilu GirmaNo ratings yet

- Working Capital ManagementDocument54 pagesWorking Capital ManagementTanishqa JoganiNo ratings yet

- UNIT 4 - Capital BudgetingDocument38 pagesUNIT 4 - Capital BudgetingKrishnan SrinivasanNo ratings yet

- Techniques of Capital BudgetingDocument21 pagesTechniques of Capital BudgetingShilpa RajuNo ratings yet

- Chapter - 08 (ИЈИЇ Ёрµе)Document16 pagesChapter - 08 (ИЈИЇ Ёрµе)yw37491382No ratings yet

- Chapter 6 - Capital Budgeting PDFDocument34 pagesChapter 6 - Capital Budgeting PDFSyamala 29No ratings yet

- Capital BudgetingDocument27 pagesCapital BudgetingDilu - SNo ratings yet

- Net Present Value and Other Investment Criteria: Mcgraw-Hill/IrwinDocument32 pagesNet Present Value and Other Investment Criteria: Mcgraw-Hill/IrwinraditNo ratings yet

- Techniques of Capital BudgetingDocument21 pagesTechniques of Capital BudgetingbansalparthNo ratings yet

- L 5 Capital Investment DecisionsDocument23 pagesL 5 Capital Investment DecisionsMist FactorNo ratings yet

- 7 Dividends and Dividend PolicyDocument25 pages7 Dividends and Dividend PolicyAiman OmerNo ratings yet

- Advanced Investment AppraisalDocument64 pagesAdvanced Investment AppraisalAayaz Turi100% (2)

- Capital - Budgeting Decision RulesDocument21 pagesCapital - Budgeting Decision RulesEmirNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document34 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Garima BansalNo ratings yet

- Capital Budgeting Analysis: CA. Sonali Jagath PrasadDocument63 pagesCapital Budgeting Analysis: CA. Sonali Jagath PrasadSonali JagathNo ratings yet

- Asis 5 (CH 9) - PertanyaanDocument4 pagesAsis 5 (CH 9) - PertanyaanAndre JonathanNo ratings yet

- Finance AppraisalDocument50 pagesFinance AppraisalSubhenduKumarPandaNo ratings yet

- Capital Budgeting Techniques PDFDocument21 pagesCapital Budgeting Techniques PDFAvinav SrivastavaNo ratings yet

- Capital Budgeting - Week Three - Updated - June 2022Document57 pagesCapital Budgeting - Week Three - Updated - June 2022Emmmanuel ArthurNo ratings yet

- Capital Budgeting: Dr. Md. Anwar Ullah, FCMA Southeast UniversityDocument37 pagesCapital Budgeting: Dr. Md. Anwar Ullah, FCMA Southeast Universityasif rahanNo ratings yet

- Capital BudgetingDocument9 pagesCapital BudgetingSEKEETHA DE NOBREGANo ratings yet

- Course: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit CollectionDocument27 pagesCourse: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit Collectionsalsabilla rpNo ratings yet

- ch10 - The Basics of Capital BudgetingDocument14 pagesch10 - The Basics of Capital Budgetinganower.hosen61No ratings yet

- 9 Capital Budgeting KirimDocument51 pages9 Capital Budgeting KirimMas SamiNo ratings yet

- Lecture 10 - Capital Investment Decisions - JJDocument28 pagesLecture 10 - Capital Investment Decisions - JJTariq KhanNo ratings yet

- Capital BudgetingDocument59 pagesCapital BudgetingSaharsh SaraogiNo ratings yet

- Topic 2 Lecture 4 Net Present Value and Other Investment RulesDocument40 pagesTopic 2 Lecture 4 Net Present Value and Other Investment RulesSyaimma Syed AliNo ratings yet

- Chapter 2 Time Value of Money Edited (Student)Document20 pagesChapter 2 Time Value of Money Edited (Student)Nguyễn Thái Minh ThưNo ratings yet

- Chapter 6 Practical Aspects of Investment Appraisal (Student)Document10 pagesChapter 6 Practical Aspects of Investment Appraisal (Student)Nguyễn Thái Minh ThưNo ratings yet

- Task2 Agree Disagree-GDocument40 pagesTask2 Agree Disagree-GNguyễn Thái Minh ThưNo ratings yet

- 22 Bài Mẫu Task 2 Từ Đề Thi Thật 2021 by NgocbachDocument98 pages22 Bài Mẫu Task 2 Từ Đề Thi Thật 2021 by NgocbachTai Pham TanNo ratings yet

- 1250kva DG SetDocument61 pages1250kva DG SetAnagha Deb100% (1)

- Boot Time Memory ManagementDocument22 pagesBoot Time Memory Managementblack jamNo ratings yet

- Advantage Dis OqpskDocument5 pagesAdvantage Dis OqpskHarun AminurasyidNo ratings yet

- Alternative Refrigerants Manny A PresentationDocument29 pagesAlternative Refrigerants Manny A PresentationEmmanuel Zr Dela CruzNo ratings yet

- Henry's Bench: Keyes Ky-040 Arduino Rotary Encoder User ManualDocument4 pagesHenry's Bench: Keyes Ky-040 Arduino Rotary Encoder User ManualIsrael ZavalaNo ratings yet

- 12 - Chepter 5Document11 pages12 - Chepter 5KhaireddineNo ratings yet

- Music and Yoga Are Complementary To Each OtherDocument9 pagesMusic and Yoga Are Complementary To Each OthersatishNo ratings yet

- LNMIIT Course Information Form: A. B. C. D. E. FDocument2 pagesLNMIIT Course Information Form: A. B. C. D. E. FAayush JainNo ratings yet

- A Priori and A Posteriori Knowledge: A Priori Knowledge Is Knowledge That Is Known Independently of Experience (That IsDocument7 pagesA Priori and A Posteriori Knowledge: A Priori Knowledge Is Knowledge That Is Known Independently of Experience (That Ispiyush_maheshwari22No ratings yet

- ART Threaded Fastener Design and AnalysisDocument40 pagesART Threaded Fastener Design and AnalysisAarón Escorza MistránNo ratings yet

- Advanced Calculus For Applications - Francis B Hilderand 1962Document657 pagesAdvanced Calculus For Applications - Francis B Hilderand 1962prabu201No ratings yet

- Classification by Depth Distribution of Phytoplankton and ZooplanktonDocument31 pagesClassification by Depth Distribution of Phytoplankton and ZooplanktonKeanu Denzel BolitoNo ratings yet

- MaekawaDocument2 pagesMaekawabhaskar_chintakindiNo ratings yet

- Calydracomfort PiDocument16 pagesCalydracomfort PiionNo ratings yet

- Factors Affecting Pakistani English Language LearnersDocument19 pagesFactors Affecting Pakistani English Language LearnersSaima Bint e KarimNo ratings yet

- Instability of Slender Concrete Deep BeamDocument12 pagesInstability of Slender Concrete Deep BeamFrederick TanNo ratings yet

- Papaer JournelDocument6 pagesPapaer JournelsonalisabirNo ratings yet

- BS en 13369-2018 - TC - (2020-11-30 - 09-45-34 Am)Document164 pagesBS en 13369-2018 - TC - (2020-11-30 - 09-45-34 Am)Mustafa Uzyardoğan100% (1)

- Screen 2014 Uricchio 119 27Document9 pagesScreen 2014 Uricchio 119 27NazishTazeemNo ratings yet

- Answerkey Precise ListeningDocument26 pagesAnswerkey Precise ListeningAn LeNo ratings yet

- PlayStation MagazineDocument116 pagesPlayStation MagazineFrank Costello67% (3)

- CCTV Proposal Quotation-1 Orine EdutechDocument5 pagesCCTV Proposal Quotation-1 Orine EdutechĄrpit Rāz100% (1)

- Research ProposalDocument2 pagesResearch Proposalsmh9662No ratings yet

- Teacher Thought For InterviewDocument37 pagesTeacher Thought For InterviewMahaprasad JenaNo ratings yet

- The Macquarie Australian Slang DictionarDocument7 pagesThe Macquarie Australian Slang DictionarnetshidoNo ratings yet

- Sociology Internal AssessmentDocument21 pagesSociology Internal AssessmentjavoughnNo ratings yet

- Zishan Engineers (PVT.) LTD.: TransmittalDocument8 pagesZishan Engineers (PVT.) LTD.: TransmittalJamal BakhtNo ratings yet

- HSC School Ranking 2012Document4 pagesHSC School Ranking 2012jHexst0% (1)

- Radar & Satellite Communication SystemDocument1 pageRadar & Satellite Communication SystemSyed Viquar AhmedNo ratings yet

- Syracuse University Dissertation FormatDocument4 pagesSyracuse University Dissertation FormatWritingContentNewYork100% (1)