You might also like

- A Hierarchy of Turing Degrees: A Transfinite Hierarchy of Lowness Notions in the Computably Enumerable Degrees, Unifying Classes, and Natural Definability (AMS-206)From EverandA Hierarchy of Turing Degrees: A Transfinite Hierarchy of Lowness Notions in the Computably Enumerable Degrees, Unifying Classes, and Natural Definability (AMS-206)No ratings yet

- Test I Accounts MSDocument10 pagesTest I Accounts MSDhrisha GadaNo ratings yet

- Accruals Q1 AnswerDocument2 pagesAccruals Q1 AnswerRiyu RimmyNo ratings yet

- Mark Scheme PrinciplesDocument23 pagesMark Scheme PrinciplesV-academy MathsNo ratings yet

- MEI 202311 eDocument22 pagesMEI 202311 eChathura WickramaNo ratings yet

- Cambridge Assessment International Education: Accounting 0452/22 October/November 2017Document12 pagesCambridge Assessment International Education: Accounting 0452/22 October/November 2017pyaaraasingh716No ratings yet

- 7110 w13 Ms 22Document10 pages7110 w13 Ms 22Muhammad UmairNo ratings yet

- Business Book o LevelDocument7 pagesBusiness Book o LevelaviiishiiNo ratings yet

- 7110 w15 Ms 22 PDFDocument9 pages7110 w15 Ms 22 PDFRachel RAMSAMYNo ratings yet

- 1700378027.9185524 - Bdcom 2023-2024 Q1Document13 pages1700378027.9185524 - Bdcom 2023-2024 Q1Anwar Hossain ReponNo ratings yet

- Cambridge International Examinations: Principles of Accounts 7110/21 May/June 2017Document9 pagesCambridge International Examinations: Principles of Accounts 7110/21 May/June 2017Taha AhmedNo ratings yet

- Cambridge Assessment International Education: Principles of Accounts 7110/22 October/November 2017Document13 pagesCambridge Assessment International Education: Principles of Accounts 7110/22 October/November 2017Makanaka MutandariNo ratings yet

- Ase20093 01 Results Mark Scheme 220826 June 2022 SeriesDocument17 pagesAse20093 01 Results Mark Scheme 220826 June 2022 SeriesTheint ThiriNo ratings yet

- n560 - Financial Accounting n5 Memo June 2019 - AdallDocument9 pagesn560 - Financial Accounting n5 Memo June 2019 - AdallemgnNo ratings yet

- Accruals Q2 AnswerDocument1 pageAccruals Q2 AnswerRiyu RimmyNo ratings yet

- Dashboard FormatDocument2 pagesDashboard FormatahamedmubeenNo ratings yet

- MOCK Test SOLUTIONDocument5 pagesMOCK Test SOLUTIONNcebakazi DawedeNo ratings yet

- 03 0452 12 MS Final ScorisDocument10 pages03 0452 12 MS Final ScorisFarman FaheemNo ratings yet

- 7110 w15 Ms 21 PDFDocument11 pages7110 w15 Ms 21 PDFRachel RAMSAMYNo ratings yet

- Mark Scheme (Results) June 2015: International GCSE Accounting (4AC0)Document14 pagesMark Scheme (Results) June 2015: International GCSE Accounting (4AC0)Syeda Malika AnjumNo ratings yet

- NABARDDocument1 pageNABARDNitin PatelNo ratings yet

- 2018-GR-10-TEST-1-MEMODocument3 pages2018-GR-10-TEST-1-MEMOSuraj SukhuNo ratings yet

- Cambridge International Examinations Cambridge International General Certificate of Secondary EducationDocument11 pagesCambridge International Examinations Cambridge International General Certificate of Secondary EducationMandrich AppadooNo ratings yet

- Suggested Solutions June 2006Document11 pagesSuggested Solutions June 2006kalowekamoNo ratings yet

- 0452 s03 Ms 2Document6 pages0452 s03 Ms 2lie chingNo ratings yet

- Cambridge O Level: Accounting 7707/23 October/November 2020Document14 pagesCambridge O Level: Accounting 7707/23 October/November 2020ImanNo ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2011 Question Paper For The Guidance of TeachersDocument6 pages9706 Accounting: MARK SCHEME For The October/November 2011 Question Paper For The Guidance of TeachersProto Proffesor TshumaNo ratings yet

- BppuDocument2 pagesBppuni made safitriNo ratings yet

- 3 M Mastery ProblemDocument4 pages3 M Mastery ProblemAdam Hobbs100% (1)

- Service Tax Registration No. credit card statement summaryDocument4 pagesService Tax Registration No. credit card statement summarySamNo ratings yet

- Cambridge International Examinations: Accounting 0452/22 March 2017Document13 pagesCambridge International Examinations: Accounting 0452/22 March 2017Mike ChindaNo ratings yet

- Mark Scheme: Accounting 5121Document12 pagesMark Scheme: Accounting 5121SaadArshadNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDocument5 pages9706 Accounting: MARK SCHEME For The May/June 2014 SeriesMateeh-ur -rehmanNo ratings yet

- Swiss Cottage 2023 Prelim P1 AnswersDocument5 pagesSwiss Cottage 2023 Prelim P1 Answersvikalp.singh.sengarNo ratings yet

- June Grade 10 Marking Guideline PDFDocument7 pagesJune Grade 10 Marking Guideline PDFBasetsana MakuaNo ratings yet

- 4AC0 01 MSC 20150305 PDFDocument14 pages4AC0 01 MSC 20150305 PDFSabsNo ratings yet

- 0452 w10 2 1 Ms PDFDocument9 pages0452 w10 2 1 Ms PDFbipin jainNo ratings yet

- Procurement Tracking SheetDocument12 pagesProcurement Tracking SheetMohannad Abo SulbNo ratings yet

- 4ac1-02-rms-20220825Document10 pages4ac1-02-rms-20220825attackdfg2002No ratings yet

- TABLE-0 Executive SummaryDocument1 pageTABLE-0 Executive SummaryShrey SaxenaNo ratings yet

- Cambridge O Level: Accounting 7707/22 May/June 2020Document12 pagesCambridge O Level: Accounting 7707/22 May/June 2020rAJBS;DFNo ratings yet

- Diamer Basha Dam Project Preliminary Works Contracts: General Manager/Project Director Chief Executive OfficerDocument2 pagesDiamer Basha Dam Project Preliminary Works Contracts: General Manager/Project Director Chief Executive OfficerNauman LiaqatNo ratings yet

- 0452 m17 Ms 22Document13 pages0452 m17 Ms 22Mohammed MaGdyNo ratings yet

- Ruiz, Eric Gerard D.: Problem IDocument9 pagesRuiz, Eric Gerard D.: Problem IMyAccntNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperDocument8 pages9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperShona MaheshwariNo ratings yet

- Ap 3 Merge 3-1234Document4 pagesAp 3 Merge 3-1234api-295670758No ratings yet

- Quiz 4 - Problem 1Document2 pagesQuiz 4 - Problem 1KyleRhayneDiazCaliwagNo ratings yet

- ACFrOgDV - 7kt04AxDyGcNL79lC HfjgmZ6EO0SqXVcl2uZ5cAPbhNyMY4 LmmxCpo4Xo2Uo5GezhPw4E543REYaq9k2iN JkFqjIIYkAU9U4nEi16BAkFxkRK2pbvbEDocument5 pagesACFrOgDV - 7kt04AxDyGcNL79lC HfjgmZ6EO0SqXVcl2uZ5cAPbhNyMY4 LmmxCpo4Xo2Uo5GezhPw4E543REYaq9k2iN JkFqjIIYkAU9U4nEi16BAkFxkRK2pbvbEwlv hugoNo ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2011 Question Paper For The Guidance of TeachersDocument5 pages9706 Accounting: MARK SCHEME For The October/November 2011 Question Paper For The Guidance of Teacherspridegwatidzo2No ratings yet

- Jockey Club Ti-I College F.4 Business, Accounting and Financial Studies Second Term Examination (2020-2021)Document5 pagesJockey Club Ti-I College F.4 Business, Accounting and Financial Studies Second Term Examination (2020-2021)ouo So方No ratings yet

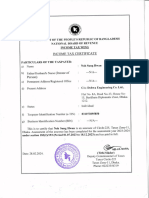

- Tax Certificate of Noh Sung Hwan - 20240310 - 0001Document2 pagesTax Certificate of Noh Sung Hwan - 20240310 - 0001Md RasalNo ratings yet

- 0452 Accounting: MARK SCHEME For The May/June 2013 SeriesDocument11 pages0452 Accounting: MARK SCHEME For The May/June 2013 SeriesIronMechKillerNo ratings yet

- Bsac 373 Audit Application 2 Prelim QuizDocument2 pagesBsac 373 Audit Application 2 Prelim QuizJ KimNo ratings yet

- Adobe Scan 26-Jul-2022Document1 pageAdobe Scan 26-Jul-2022shubham satamNo ratings yet

- Cambridge IGCSE™: Accounting 0452/23 October/November 2020Document14 pagesCambridge IGCSE™: Accounting 0452/23 October/November 2020ATTIQ UR REHMANNo ratings yet

- Cambridge International General Certificate of Secondary EducationDocument9 pagesCambridge International General Certificate of Secondary Educationcheah_chinNo ratings yet

- CashbookDocument2 pagesCashbookJoshua AssinNo ratings yet

- Principles of Accounting 2 Exam Marking KeyDocument6 pagesPrinciples of Accounting 2 Exam Marking KeyYus LindaNo ratings yet

- Completion of Reviera Hotel-Remaining Works (Ah-239) : Payment Status Ytd Summary (As of 21/02/2023)Document115 pagesCompletion of Reviera Hotel-Remaining Works (Ah-239) : Payment Status Ytd Summary (As of 21/02/2023)Imad HamidaNo ratings yet

- PowerPoint Presentation1Document1 pagePowerPoint Presentation1Dhrisha GadaNo ratings yet

- Paper 4Document17 pagesPaper 4Dhrisha GadaNo ratings yet

- PowerPoint Presentation3Document1 pagePowerPoint Presentation3Dhrisha GadaNo ratings yet

- Paper 2 Section 3 and 4 EconomicsDocument2 pagesPaper 2 Section 3 and 4 EconomicsDhrisha GadaNo ratings yet

- Cambridge IGCSE Mathematics Paper 2Document8 pagesCambridge IGCSE Mathematics Paper 2Vũ Hà VânNo ratings yet

- TEST SHEET Practical Mock 3.2Document5 pagesTEST SHEET Practical Mock 3.2Dhrisha GadaNo ratings yet

- Equations and Inequalities Paper 1Document2 pagesEquations and Inequalities Paper 1Dhrisha GadaNo ratings yet

- CombinepdfDocument64 pagesCombinepdfDhrisha GadaNo ratings yet

- WS3Document1 pageWS3Dhrisha GadaNo ratings yet

- MPsALES IN462 9D00Document1 pageMPsALES IN462 9D00Dhrisha GadaNo ratings yet

- 0417 m17 QP 31Document8 pages0417 m17 QP 31Popi MastroianniNo ratings yet

- Class 9 IGCSE Business Studies Syllabus 2022-23Document1 pageClass 9 IGCSE Business Studies Syllabus 2022-23Dhrisha GadaNo ratings yet

- Supa ScubaDocument2 pagesSupa ScubaDhrisha GadaNo ratings yet

- Storage Devices Chapter 3: Magnetic, Optical, Solid-State MediaDocument13 pagesStorage Devices Chapter 3: Magnetic, Optical, Solid-State MediaDhrisha GadaNo ratings yet

- Chap 1, 2, RevisionDocument3 pagesChap 1, 2, RevisionDhrisha Gada100% (1)

- Syllabus For Class9 AccountingDocument1 pageSyllabus For Class9 AccountingDhrisha GadaNo ratings yet

- Maths SyllabusDocument1 pageMaths SyllabusDhrisha GadaNo ratings yet

- N19evidence9f08 1Document4 pagesN19evidence9f08 1Dhrisha GadaNo ratings yet

- CL 9 ICT Syllabus T1 2022 23 - IGCSEDocument1 pageCL 9 ICT Syllabus T1 2022 23 - IGCSEDhrisha GadaNo ratings yet

- Economics Syllabus 22 23Document1 pageEconomics Syllabus 22 23Dhrisha GadaNo ratings yet

- N 19 Evidence 9 F08Document1 pageN 19 Evidence 9 F08Dhrisha GadaNo ratings yet

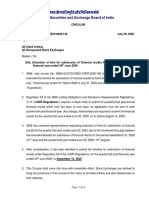

- Extension of Time For Submission of Financial Results For The Quarter - Half Year - Financial Year Ended 30th June 2020Document2 pagesExtension of Time For Submission of Financial Results For The Quarter - Half Year - Financial Year Ended 30th June 2020secretarial officerNo ratings yet

- CHAPTER 3 - Questions - EditedDocument9 pagesCHAPTER 3 - Questions - EditedEsraa TarekNo ratings yet

- 5 Adjusting Entries For Prepaid ExpenseDocument4 pages5 Adjusting Entries For Prepaid Expenseapi-299265916No ratings yet

- Public Private PartnershipsDocument14 pagesPublic Private PartnershipsCharu ModiNo ratings yet

- Strong Tie LTDDocument15 pagesStrong Tie LTDchitu1992100% (4)

- Indian Money Market Structure and ComponentsDocument9 pagesIndian Money Market Structure and ComponentsPrasun KumarNo ratings yet

- Basel III: Bank Regulation and StandardsDocument13 pagesBasel III: Bank Regulation and Standardskirtan patelNo ratings yet

- Revision Test Paper CAP III June 2020Document233 pagesRevision Test Paper CAP III June 2020Roshan PanditNo ratings yet

- Individual Research Activity 1 BusinessDocument7 pagesIndividual Research Activity 1 BusinesshariNo ratings yet

- ScriptDocument3 pagesScriptMOHD AZAMNo ratings yet

- Wire Transfer Procedure PDFDocument7 pagesWire Transfer Procedure PDFombonoNo ratings yet

- Konverter CSV - Batch UploaddDocument20 pagesKonverter CSV - Batch UploaddDevi Merry Sonia Sitepu50% (2)

- Types of Major Accounts and Financial Statements Chapter 4 ProblemsDocument6 pagesTypes of Major Accounts and Financial Statements Chapter 4 ProblemsAmie Jane MirandaNo ratings yet

- Accountancy NotesDocument23 pagesAccountancy NotesAlbana QemaliNo ratings yet

- Accounting For LeasesDocument9 pagesAccounting For LeasesNelson Musili100% (3)

- A0x8akqPTbqMfGpKj 26Zg BB Course1 Week4 Workbook-V2.02Document8 pagesA0x8akqPTbqMfGpKj 26Zg BB Course1 Week4 Workbook-V2.02Zihad HossainNo ratings yet

- Sampath Card Estatement 2020-10-28-4051226 PDFDocument1 pageSampath Card Estatement 2020-10-28-4051226 PDFBuddhika Gihan Wijerathne0% (1)

- Technical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEDocument30 pagesTechnical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEJayant Sharma100% (1)

- Chapter 5 - Health Insurance SchemesDocument0 pagesChapter 5 - Health Insurance SchemesJonathon CabreraNo ratings yet

- Consumers' Perceptions of Reliance Life Insurance Health PlansDocument105 pagesConsumers' Perceptions of Reliance Life Insurance Health Plans2014rajpointNo ratings yet

- CaseDocument4 pagesCaseRyza Mae BascoNo ratings yet

- Audit of CBS EnvironmentDocument28 pagesAudit of CBS EnvironmentPatricia UkemNo ratings yet

- Bank Reconciliation Statements: MBA ExecutiveDocument37 pagesBank Reconciliation Statements: MBA ExecutiveAreeb IqbalNo ratings yet

- Hilton SamplechapterDocument41 pagesHilton SamplechapterNinikKurniatyNo ratings yet

- 1 The Nature, Purpose and Scope of AuditingDocument12 pages1 The Nature, Purpose and Scope of Auditingyebegashet100% (1)

- Week 1 Assignment Fundamental Principles in TaxationDocument5 pagesWeek 1 Assignment Fundamental Principles in TaxationIan Paolo CaylanNo ratings yet

- Cash Management Models & TechniquesDocument3 pagesCash Management Models & Techniqueshae1234No ratings yet

- CMBS 101 Slides (All Sessions)Document41 pagesCMBS 101 Slides (All Sessions)Karan MalhotraNo ratings yet

- Capital Structure Test QuestionsDocument28 pagesCapital Structure Test QuestionsSardonna FongNo ratings yet

- ACCT5001 2022 S2 - Module 2 - Lecture Slides StudentDocument33 pagesACCT5001 2022 S2 - Module 2 - Lecture Slides Studentwuzhen102110No ratings yet