Professional Documents

Culture Documents

Taxation

Uploaded by

Fiona MiralpesOriginal Description:

Original Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Taxation

Uploaded by

Fiona MiralpesCopyright:

Available Formats

lOMoARcPSD|30374161

Taxation- General Principles, Tax Remedies, Taxability of

Individuals and Corporations- Notes and Quiz

BS Accountancy (New Era University)

Scan to open on Studocu

Studocu is not sponsored or endorsed by any college or university

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

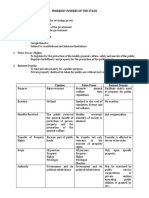

Inherent Powers of the State

- Power existing as natural or basic part of every sovereign state, without being

conferred or granted by the people or the Constitution

DISTINCTIONS AMONG THE THREE (3) INHERENT POWERS OF THE STATE

TAXATION POLICE POWER EMINENT DOMAIN

Power to enforce Power to make and Power to take private

NATURE

contributions to raise implement laws for the property for public use

gov't funds general welfare with just compensation

May be granted to

AUTHORITY

Government only Government only public service/utility

companies

PURPOSE For the support of the Promotion of general The taking of private

government through regulation property for public use

Community or a class On an individual as the

Community or a class of owner of personal

of individuals

PERSONS individuals property

Applies to all

AFFECTED Applies to all persons,

persons, property and

property and excises that

excises that may be Only particular property

may be subject thereto

subject thereto is comprehended

Property is Property is noxious or

TYPE OF Property is wholesome

wholesome and is intended for a noxious

PROPERTY devoted to public use purpose and as such

and is devoted to public

use or purpose

or purpose taken and destroyed

Contribution becomes No transfer or title. There

EFFECT part of public fund

There is a transfer of

may just be a restraint on

title or property

injurious use of property

RIGHTS

AFFECTED Property right Property right and liberty Property right

Plenary, Broader in application. Merely a power to take

SCOPE

comprehensive General power to make private. property for

supreme and implement law. public use

No direct and immediate

in form of protection benefit but only such as

BENEFITS Market value of property

and benefits received may arise from the

RECEIVED taken

from government maintenance of a healthy

economic standard of

society

AMOUNT Sufficient to cover cost of

No imposition. The

the license and the

OF No limit owner is paid equivalent

necessary expenses of

IMPOSITION to the fair value of his

police surveillance and

property.

regulation

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

PURPOSES OF TAXATION

1. Primary Purpose (also called Revenue or Fiscal Purpose)

- To raise revenues/funds to defray the necessary expenses of the

government

2. Secondary Purpose:

a. Regulatory Purpose

- employed as a devise for regulation or control (to implement the

police power of the State for the promotion of the general welfare)

by means of which certain effects or conditions envisioned by the

government may be achieved.

b. Compensatory Purposes

- Reduction of Social Inequality

- Economic Growth

- Protect local industries against unfair competition ³

protectionism

Nature and Characteristics of Taxation

1. Inherent Power - may be exercised although not expressly granted by the

constitution

2. Essentially a legislative function - only the legislative can impose taxes

3. Subject to inherent and constitutional limitations- not an absolute power

4. For public purpose

5. The strongest of all the inherent powers of the State.

6. Subject to treaty or comity

7. Generally payable in money

8. Territorial in scope

Absence of inherent

Power to tax is comprehensive, plenary, supreme &

and constitutional ³

unlimited

limitations

ÿ

<The power to tax includes the power to destroy=

-Justice Marshall

Taxes Defined

- enforced proportional contributions from persons and property, levied by

the State by virtue of its sovereignty for the support of the government and

for all its public needs.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

ESSENTIAL CHARACTERISTICS OF TAX

a. forced charge, imposition or contribution

b. pecuniary burden payable in money, not in kind!

c. imposed for public purposes

d. imposed pursuant to a legislative authority

e. levied within the territorial and legal jurisdiction of a state

f. assessed in accordance with reasonable rule of apportionment ³ ability to

pay theory

Theory and Basis of Taxation

1. Necessity Theory

- <existence of government is a necessity=.

- power based upon necessity

- The government cannot continue to perform of serving and protecting its

people without means to pay its expenses. For this reason, the state has

the right to compel all its citizens and property within its limits to contribute

2. Lifeblood Doctrine

- Taxes are the lifeblood of the government without which it can neither

exist nor endure. Upon taxation depends the State's ability to serve the

people for whose benefits taxes are collected

MANIFESTATION OF THE LIFEBLOOD DOCTRINE/THEORY:

o No Estoppel against the Government

o Collection of taxes cannot be enjoined (stopped) by injunction

o Taxes could not be the subject of compensation or set-off

o A valid tax may result in the destruction of the taxpayer's property

o Right to select objects (subjects) of taxation

3. The Benefits-Protection Theory

- reciprocal duties of "protection and support" between the State and its

inhabitants.

- State ³ collects taxes from the subjects of taxation in order that it may

be able to perform the functions of government.

- Citizens ³ pay taxes in order to be secured in the enjoyment of the

benefits of organized society.

- This theory spawned the Doctrine of Symbiotic Relationship which

means, taxes are what we pay for a civilized society

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

Similarities among the 3 Inherent Powers

1. Inherent in the State

2. Exist independently of the constitution although the conditions for their

exercise may be prescribed by the constitution.

3. Constitutes the 3 methods by which the State interfere with private

rights and property

4. Legislative in nature and character.

5. Presuppose an equivalent compensation received, directly or indirectly, by

the persons affected.

require or imply / forced charge

Scope of the Taxing Power of the Legislative

³ power of taxation is the most absolute of all powers of

According to the government

the Supreme ÿ

Court has the broadest scope of all the powers of the

government

ÿ

in the absence of limitations, it is considered as

comprehensive, unlimited, plenary and supreme

- Comprehensive- nearly all elements/

complete

- Plenary- absolute

- Supreme -superior to all others

The matters within the competence of the legislature include the determination of

the following:

1. Subject or object (person, property and excises/privileges) to be taxed

2. Purpose of the tax as long as it is a public purpose

3. Amount or rate of the tax

4. Kind of tax

5. Apportionment of the tax (i.e., whether the tax shall be general or limited

to a particular locality or partly general and partly local)

6. Situs of taxation

7. Manner or method of collection

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

Stages/Aspects of Taxation

1. Levying or Imposition

- involves the passage of tax laws or ordinances (in case of LGU)

through the legislature

2. Assessment and Collection

- involves the act of administration and implementation of tax laws by the

executive through its administrative agencies such as the BIR and the

Bureau of Customs.

• Assessment

- determination by the executive branch (i.e., BIR, BOC, LGU) of

the correct amount of the tax

• Collection of the tax levied, which is essentially administrative in

character.

Principles of Sound Tax System (3)

A sound tax system should satisfy all the principles of taxation, such as:

• the ability to generate sufficient revenues

• fulfill the socio-economic objectives

• should not hamper the productive system of the economy

ELEMENTS OF SOUND TAX SYSTEM

1. Fiscal Adequacy

- The sources of government revenue must be sufficient to meet

government expenditures and other public needs

2. Theoretical Justice

- must be based on the taxpayer's ability to pay

- taxation must be progressive conformably with the constitutional

mandate that congress shall evolve a progressive system of taxation.

3. Administrative Feasibility

- Tax laws must be capable of convenient, just and effective

administration free from confusion and uncertainty

- should have the merits of simplicity, flexibility and diversity.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

LIMITATIONS ON THE TAXING POWER

A. Inherent Limitations- inherent limitations proceed from the very nature of

the taxing power itself. The taxing power has very distinct and positive

limitations some of which inhere in its very nature and exist whether

declared or not declared in the written constitution.

1. Public purpose

Proceeds from tax must be used for:

a. Support of the government.

b. Some of the recognized objects of government.

c. To promote the welfare of the community (not individuals)

2. Situs of taxation or territoriality

The taxing power is limited to person and property within and subject to its

jurisdiction

PLACE OF TAXATION

a. The state where the subject be taxed has a situs may rightfully levy

& collect tax

b. The situs is necessarily in the State which has jurisdiction or which

exercises dominion over the subject in question

FACTORS TO CONSIDER IN DETERMINING SITUS OF TAXATION

a. Subject matter (person, property, activity)

b. Nature of tax

c. Citizenship

d. Residence of the taxpayer

APPLICATION SITUS TAXATION SUBJECT MATTER

SUBJECT MATTER SITUS

Persons Residence the taxpayer

Real Property Location

Tangible Personal Property Location

Intangible Personal Property Domicile of the owner

Residence, citizenship, source of

Income

income

Business Place business

Gratuitous Transfer of Residence or citizenship of the

Property transferor or location of property

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

EXC.

TAXABLE ON

Income taxation on RC & ³

Income within and outside PH

DC

Transfer Taxation on ³ Transfer of property located w/in &

Resident/Citizen

outside PH

(RC, NRC, RA)

3. International comity treaty

A State cannot tax another based on the principle of Sovereign Equality

among States (i.e., tax law passed imposing taxes on foreign

ambassadors not a valid law)

4. Non-delegability of the Taxing power (Enactment Tax Laws)

- The taxing power is purely legislative; hence power cannot be

delegated either to the executive or judicial departments.

- The limitation arises the doctrine of separation of powers among three

branches the government.

EXCEPTIONS TO THE RULE AGAINST DELEGATION:

a. Delegation to the President, subject to some limitations and

restrictions, to fix within specified limits, tariff rates and tonnage or

wharfage duties and other duties and imposts.

b. Delegation to local governments the power to create its own

sources of revenues and to levy taxes, subject to such limitations as

provided by law.

c. Delegation to administrative agencies certain aspects of the

taxing process that are not legislative such as:

▪ the power to fix value of property for purposes of taxation

pursuant to fixed rules

▪ the power to assess and collect taxes

5. Tax Exemptions of the government

a. Agencies performing governmental functions are tax-exempt

unless expressly taxed.

b. Agencies performing proprietary functions are subject to tax

unless expressly exempted

c. GOCCS performing proprietary functions are subject to tax,

however, the following are granted exemptions:

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

▪ Government Service Insurance System (GSIS)

▪ Social Security System (SSS)

▪ Philippine Health Insurance Corporation (PHIC)

▪ Local Water Districts (RA 10026)

NOTE: Philippine Charity Sweepstakes Office (PCSO) is tax-exempt prior to Jan.

1, 2018 (effectivity of TRAIN Law).

B. Constitutional Limitations on the Taxing Power

1. Observance of due process of law

2. Equal protection of law

3. Uniformity in taxation

4. Progressive scheme of taxation

5. Non-imprisonment for non-payment of poll tax

6. Non-impairment of the obligations of contracts

7. Free-worship clause

8. Exemption of charitable institutions, churches, parsonages, or convents

appurtenant thereto, mosques, and non-profit cemeteries, and all lands,

buildings and improvements actually, directly and exclusively used for

religious, charitable or educational purposes.

9. Exemption from taxes of the revenues and assets of non-profit, non-

stock educational institutions including grants, endowments, donations

or contributions for educational purposes

10. Non-appropriation of public funds or property for the benefit of any

church, sect or system of religion, etc.

11. No money shall be paid out of the Treasury 'except in pursuance of

an appropriation made by law,

12. Concurrence of a majority of ALL MEMBERS OF CONGRESS for

the passage of a law granting tax exemption

13. Non-diversification of tax collections

14. The President shall have the power to veto any particular item(s) in

an appropriation, revenue or tariff, but the veto shall not affect the

item(s) to which no objection has been made.

15. Non-impairment of the jurisdiction of the Supreme Court to review

tax cases

16. Appropriations, revenue or tariff bills shall originate exclusively in the

House of Representatives but the Senate may propose or concur with

amendments.

17. Each local government unit shall exercise the power to create its

own sources of revenue and shall have a just share in the national

taxes.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

NATIONAL TAXES vs. LOCAL TAXES

NATIONAL LOCAL

AUTHORITY Inherent Power Delegated Power

Legislative in nature

Legislative in nature through

through enactment of tax

NATURE enactment of local ordinances by

laws by the Congress and

the local legislative branch

the Senate.

1. Levying = Congress 1. Levying = Legislative branch

PROCESS 2. Assessment/ Collection of the LGU

= BIR & BOC 2. Assessment/Collection

= Treasurer

National Internal Revenue Taxes under the administration of the BIR:

a. Income Tax

b. Estate and donor's tax

c. Value-added tax

d. Other percentage taxes

e. Excise taxes

f. Documentary stamp taxes

DOUBLE TAXATION

KINDS OF DOUBLE TAXATION

a. Direct Duplicate Taxation

- objectionable and prohibited because it violates the constitutional

provision on uniformity and equality. It means:

▪ Taxing twice;

▪ By the same taxing authority;

▪ Within the same jurisdiction or taxing district;

▪ For the same purpose;

▪ In the same year or taxing period; and

▪ Same kind or character of tax

b. Indirect Duplicate Taxation

- not legally objectionable.

- extends to all cases in which there is a burden of two or more pecuniary

imposition but imposed by different taxing authorities

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

SOURCES OF TAX LAWS

a. Constitution

b. Tax Treaties and Conventions with Foreign Countries

c. The "Tax Code" [RA No. 8424- National Internal Revenue Code, as

amended (le, RA 10963-TRAIN Law; RA 11534-CREATE Law), Tariff and

Customs Code, and portion of the Local Government Code]

d. Statutes and laws like RA 1125 (an Act Creating the Court of Tax Appeals)

and RA 7716 (E-VAT Law)

e. Presidential Decrees and Executive Orders

f. Court Decisions

g. Revenue Issuances promulgated by the Department of Finance such as

Revenue Regulations (RR) Revenue Memorandum Circulars (RMCS),

Revenue Memorandum Orders (RMOS), BIR Revenue Rulings and those

of the Bureau of Customs like Customs Memorandum Orders

h. Local Tax Ordinances

ORDER OF PRIORITY:

1 Constitution

2 Tax treaties

3 Tax Laws/statues and judicial decisions

4 Revenue issuances (revenue regulations, revenue memorandum circulars,

revenue memorandum orders, revenue rulings, etc.)

NATURE OF TAX LAWS

• civil and not penal in nature, although there are penalties provided for

their violation.

• The purpose of tax laws imposing penalties for delinquencies is to compel

the timely payment of taxes or to punish evasion or neglect of duty in

respect thereof.

CONSTRUCTION OR INTERPRETATION OF TAX LAWS IN CASE OF DOUBT

OR AMBIGUITY

a. Tax statutes are construed strictly against the government and

liberally in favor of the taxpayer. Taxes, being burdens, are not to

be presumed beyond what the statute expressly and clearly

FAVOR

declares.

{

b. Provisions granting tax exemptions are construed strictly against

the taxpayer claiming tax exemption and liberally in favor of the

government.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

APPLICATION OF TAX LAWS

- prospective in operation because the nature and amount of the tax

could not be foreseen and understood by the taxpayer at the time the

transactions which the law seeks to tax was completed.

EXCEPTION:

While it is not favored, a statute may nevertheless operate

retroactively provided it is expressly declared or is clearly the legislative

intent. But a tax law should not be given retroactive application when

it would be harsh and oppressive.

CLASSIFICATION OF TAXES

A. According to Subject Matter:

▪ Personal, Poll or Capitation Tax

- tax of a fixed amount imposed upon individual, whether citizens or

not, residing within a specified territory without regard to their

property or the occupation in which he may be engaged (e.g. basic

community tax)

▪ Property Tax

- tax imposed on property, whether real or personal, in proportion

either to its value, or in accordance with some other reasonable

method of apportionment (e.g. real estate tax)

▪ Excise Tax

- Residual definition

- tax on the exercise of certain rights and privileges (e.g. income tax,

estate tax, donor's tax, VAT)

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

B. According to Who Bears the Burden

DIRECT TAX INDIRECT TAX

e.g. income tax, estate tax, donor's e.g. VAT and OPT

tax

Imposed on the person obliged to Payment is demanded from a

pay the same and this burden person who is allowed to transfer

cannot be shifted or passed on the burden of taxation to another

to another

Taxpayer who pays the tax is Paid by a person who is not

directly liable directly liable who may therefore

shift or pass the tax to another

person or entity

Demanded from the very person demanded in the first instance from

who, as intended, should pay the one person with the expectation

tax that he can shift the burden to

someone else, not as a tax but as

part of the purchase price

C. According to Determination of Amount

▪ Specific Tax

- fixed amount based on volume, weight or quantity of goods as

measured by tools, instruments or standards. (e.g. excise tax on

cigars and liquors)

▪ Ad Valorem Tax

- based on the value of the property subject to tax (e.g. VAT, income

tax, donor's tax and estate tax)

- Excise tax based on selling price or other specified value of goods

D. According to Purpose

▪ Fiscal/General/Revenue Tax

- levied without a specific or pre-determined purpose, (e.g.

income tax, donor's tax and estate tax)

▪ Regulatory/Special/Sumptuary Tax

- those intended to achieve some social or economic goals. (e.g.

tariff and certain duties on imports)

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

E. According to Jurisdiction/Scope or Authority

▪ National Tax-imposed by the National Government

▪ Local Tax-imposed by municipal corporations (e.g. real estate tax)

F. According to Graduation or Rate

▪ Proportional/Flat Rate Tax

- unitary or single rate, (e.g. VAT, OPT)

▪ Progressive/Graduated Tax

- as the tax base grows the tax rate increases. (e.g. income tax on

individuals, estates, trusts, estate tax, donor's tax)

▪ Regressive Tax

- the tax rate increases as the tax base decreases.

TAX DISTINGUISHED FROM OTHER CHARGES AND FEES

TAX VS. TOLL

TAX TOLL

▪ it is a demand of sovereignty ▪ it is a demand of proprietorship

▪ it is one's support for the ▪ it is a compensation for the use of

government somebody else's property

▪ it is imposed only by the ▪ it may be imposed by the

government government or private individuals

▪ it is based on governmental needs ▪ it is determined by the cost of

property or improvement thereon

TAX VS. PENALTY

TAX PENALTY

▪ it is imposed to raise revenue ▪ it is imposed to regulate conduct

▪ it is imposed only by the through punishment and

government suppression of injurious act

▪ it arises from law ▪ may be imposed by the

▪ generally, payable in money government or by private

individuals

▪ it may arise from law or contract

▪ may be paid in money or in kind

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

TAX VS. ASSESSMENT

TAX SPECIAL ASSESSMENT

▪ levied on business, interests, ▪ levied on land

transactions, rights, persons, ▪ cannot be made the personal

properties or privileges liability of the person assessed,

▪ may be made a personal liability of because it is the land that answers

the person assessed for the liability

▪ based on necessity with no hope of ▪ based wholly on benefits received

direct or immediate benefit to the ▪ it is exceptional in application for

taxpayer the recovery of cost and/or

▪ is of general application maintenance of improvement

TAX VS. LICENSE FEE

TAX LICENSE FEE

▪ tax is levied in the exercise of the ▪ license fee emanates from the

taxing power police power of the state

▪ purpose of it is to generate revenue ▪ the purpose of it is regulatory

▪ generally, amount is unlimited ▪ limited to the necessary expenses

▪ non-payment does not make the of regulation and control

business illegal ▪ imposed on the exercise of a right

or privileges

▪ non-payment makes the business

illegal.

TAX VS. DEBT TAX

TAX DEBT

▪ based on law ▪ based on contract

▪ not assignable ▪ assignable

▪ payable in money ▪ payable in kind or in money

▪ not subject to set off ▪ subject to set-off

▪ non-payment may result to ▪ No imprisonment (except when

imprisonment. debt arises from crime)

▪ bears interest only if delinquent ▪ interest depend upon the

stipulation of the parties

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

TAX VS. CUSTOMS DUTIES

TAX CUSTOM DUTIES

▪ imposed on person, property, rights ▪ Imposed on imported or exported

or transaction goods

▪ it comprehends more than the term ▪ it is also a tax

custom duties

❖ SUBSIDY

▪ Refers to a pecuniary aid directly granted by the government to an

individual or private commercial enterprise deemed beneficial to the public.

▪ NOT A TAX although tax may have to be imposed to pay it.

❖ REVENUE

▪ Refers to all the funds or income derived by the government, whether from

tax or any other source.

▪ Amount collected

❖ INTERNAL REVENUE

▪ taxes imposed by the legislature other than duties on imports and exports.

❖ TARIFF

May be used in one of three (3) senses:

1 A book of rates drawn usually in alphabetical order containing the names

of several kinds of merchandise with the corresponding duties to be paid

for the same, or

2 The duties payable on goods imported or exported; or

3 The system or principle of imposing duties on the importation (or

exportation) of goods.

*The term tariff and customs duties are used interchangeably in the Tariff and

Customs Code

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

SYSTEMS OF "INCOME" TAXATION

a. Global System

- All items of gross income, deductions are reported in one income tax

return and the applicable tax rate is applied on the tax base.

b. Schedular System

- Different types of income are subject to different sets of graduated or

flat income tax rates.

OTHER DOCTRINES/RULES IN TAXATION

❖ Equitable Recoupment

- Claim for refund which is prevented by prescription may be allowed to

be used as payment for unsettled tax liabilities if both taxes arise from

the same transaction in which overpayment is made and underpayment

is due.

❖ Set-off taxes

- taxes are not subject to set-off or legal compensation because the

government and the taxpayer are not mutual creditors and debtors of

each other.

❖ Taxpayer Suit

- This provides that a taxpayer suit can only be allowed if the act involves

a direct and illegal disbursement of public funds derived from taxation

Exemptions from Taxation

- grant of immunity, express or implied

CLASSIFICATION OF EXEMPTION

a. Express or affirmative

- these are express provisions in the Constitution, statues, treaties,

ordinances, franchises or contracts

b. Implied or exemption by omission

- this occurs when a tax is levied on certain classes of persons,

properties or transactions without mentioning other classes. Those not

mentioned are deemed exempted by omission

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

INTERPRETATION OF EXEMPTION GRANT

- strictly construed against the person or entity claiming exemption.

- One must Justify such claim by clear and positive grant.

ESCAPE FROM TAXATION

1. Evasion or Dodging

- taxpayer uses unlawful means to evade or lessen the payment tax

2. Avoidance or tax minimization

- reduction or totally escaping payment of tax through legally permissible

means of tax

3. Shifting

- Transfer of burden of tax to another without violating the law.

• Impact is the point at which tax is originally imposed.

• Incidence is the point at which the tax burden finally rests or settles

down.

THREE (3) KINDS SHIFTING

a. Forward shifting

- Follows the normal flow of distribution

- imposed on producers but passed on to consumers

b. Backward Shifting

- Common with non-essential commodities where buyers have

considerable market power and commodities with numerous

substitute products

- Tax burden is shifted back to the agents of production through

purchase transaction

c. Onward shifting

- Occurs in the distribution channel that exhibits forward or backward

shifting

4. Capitalization

- the seller is willing to lower the price of the commodity provided the

taxes will be shouldered by the buyer

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Gener al Pr inciples of Taxation

TAXATION REVIEW

5. Transformation

- the manufacturer absorbs the additional taxes imposed by the

government without passing it to the buyers for fear of lost of his/its

market. Instead, he/it increases quantity of production, thereby turning

their units of production at lower cost resulting to the transformation of

the tax into gain through the medium of production.

6. Exemption

- immunity, privilege or freedom from payment of a charge or burden to

which others are obliged to pay.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

When PAN is not required:

1 When the finding for any deficiency tax is the result of mathematical error

in the computation of the tax as appearing on the face of the return;

2 When a discrepancy has been determined between the tax withheld and

the amount remitted by the withholding agent;

3 When a taxpayer who opted to claim a refund or tax credit of excess

creditable withholding tax for a taxable period was determined to have

carried over and automatically applied the same amount claimed against

the estimated tax liabilities for the taxable quarter or quarters of the

succeeding taxable year;

4 When the excise tax due on excisable articles has not been paid; or

5 When the articles locally purchased or imported by an exempt person,

such as, but not limited to, vehicles, capital equipment, machineries and

spare parts, has been sold, traded or transferred to non-exempt persons.

(Section 228, NIRC).

Under RR No. 30-02, the following can be compromised:

1 Delinquent accounts;

2 Cased under administrative protest after issuance of the FAN to the

taxpayer which are still pending in the Regional Offices, Revenue District,

Legal Service, Large Taxpayer Services (LTS), Collection Service,

Enforcement Service and other offices in the National Office;

3 Civil tax cases being disputed before the courts;

4 Collection cases filed in courts

5 Criminal violations, other than those already filed in court or those involving

criminal tax fraud.

What cannot be compromised:

1. Withholding tax cases, unless the applicant-taxpayer invokes provisions of

law that cast doubt on the taxpayer's obligation to withhold;

2. Criminal tax fraud cases confirmed by the CIR;

3. Criminal violations already filed in court;

4. Delinquent accounts with duly approved schedule of installment payments;

5. Cases where final reports of reinvestigation or reconsideration have been

issued resulting to reduction in the original assessment and the taxpayer is

agreeable to such decision by signing the required agreement form;

6. Cases which become final and executory after final judgement of a court,

where compromise is requested on the ground of doubtful validity of the

assessment; and

7. Cases which become final and executory after final judgement of a court,

where compromise is requested on the ground of doubtful validity of the

assessment.

• 25% in case of failure to:

• File the return and pay tax on time

• File the return with the proper internal revenue officer

• Pay the deficiency tax within the time prescribed

• Pay the full or part of the amount of tax shown on any return required to be

filed

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

Suspension of the running of prescriptive period:

1. For the period during with the CIR is prohibited from making the

assessment or beginning distraint or levy or a proceeding in court and for

sixty (60) days thereafter;

2. When the taxpayer requests for reinvestigation which is granted by the

Commissioner;

3. When the taxpayer cannot be located in the address given by him in the

return filed upon which a tax is being assessed or collected; UNLESS the

taxpayer informs the Commissioner of any change in address

4. When the warrant of distraint or levy is duly served upon the taxpayer, his

authorized representative, or a member of his household with sufficient

discretion, and no property could be located; and

5. When the taxpayer is out of the Philippines. (Section 223, NIRC)

6. When there is a valid waiver.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

REMEDIES OF TAXPAYER (before payment)

TAXATION REVIEW NOTES

ASSESSMENT PROCESS

LOA Audit

120 days

Notice of Discrepancy

(NOD)

Discussion of Discrepancy

Taxpayer to present and explain his side on the discrepancies

Minimum of 5 days and maximum of 30 days from receipt of NOD

Preliminary Assessment

Notice (PAN)

reply within 15 days

If no reply from taxpayer or reply to PAN was found to be without merit

Final Assessment Formal Letter of

Notice (FAN) Demand (FLD)

reply within 30 days

Note whether

Request for Reinvestigation Request for Reconsideration

Submit within 30 days

without need of additional evidence

Submit new documents

within 60 days from filing request

180 days

180 days

Final Decision on Disputed Assessment (FDDA)

either by

direct denial Indirect Denial

CIR fails to act on protest within 180 days from date of

submission

30 days

30 days

Appeal to Appeal to CTA Await final decision of CIR

Court of Tax Appeals From the lapse of 180 day and appeal such to CTA

(CTA) period after receipt of decision

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

TAX REMEDIES

On the part of government - actions provided to enforce tax collection

On the part of taxpayers - avail to seek relief from undue burden, to counter

those allegations

A. ASSESSMENT PROCESS

1 Tax Audit or ● Letter of Authority (LOA)

Investigation official document that empowers a Revenue

Officer to examine and scrutinize a taxpayer’s

books in order to determine the correct internal

revenue tax liabilities

● No LOA = Null/ void assessment or

examination

● 10 days to provide necessary documents for

audit

● >10 days Letter of informal Conference

Cases not covered by LOA

1. Civil or criminal tax fraud

2. Policy cases under audit by special teams in the

National Office

Effects of issuance of LOA

● Tax return or declaration filed may be modified,

changed or modified within 3 years from the

date of filing

● Amendments are not allowed when LOA or

investigation of such has been served

LOA vs. LN (Letter Notice)

LN is not an authority to conduct an audit or

examination of the taxpayer leading up to the

issuance of assessment.

After LN, the RO should secure a LOA before

proceeding to further assessment

2 Notice of • NOD is given to a taxpayer is found to be liable

Discrepancy for deficiency tax in the course of investigation by

(NOD) the RO

• Aims to fully afford the taxpayer with fair

opportunity to present and explain his side on the

discrepancies found

• 5 days from the receipt of NOD

EXTENSION: not exceeding 30 days from receipt

of NOD

FAILURE OF TAXPAYER TO RECONCILE WILL

RESULT IN THE ISSUANCE OF DEFFICIENCY TAX

ASSESSMENT THROUGH PAN

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

3 Prelim Issued by the Regional Assessment Division,

Assessment Commissioner

Notice (PAN) • shall be in writing, otherwise void

Not required when

● Deficiency tax is the result of mathematical error

in computation

● Discrepancies between tax withheld and actual

amount has been determined by withholding

agent

● Excise tax due has not been paid

● When an article purchased by an exempt person

has been sold, traded or transferred to non-

exempt persons

The taxpayer has 15 days to contest upon receipt of

PAN

4 Final Letter of Issued when

Demand (FLD)/ ● Failed to respond to the PAN

Final ● The reply found to be w/o merit (di convincing)

Assessment

Notice (FAN) PRESCRIPTIVE PERIOD

3 years from:

a. Actual filing of return;

Return filed is NOT

or

fraudulent

b. Deadline for filing

Whichever is LATER

1. Return filed is

fraudulent 10 years from discovery

2. NO return was filed

Remedies of the taxpayer

● Protest to CIR within 30 days from the date of

receipt of FAN

○ Request for reconsideration- without need

for additional evidence

○ Request for reinvestigation - present

additional evidences within 60 days from

the date of protest

5 Final Decision DENIAL OF PROTEST

on a Disputed 1. Direct denial

Assessment 2. Indirect denial - CIR fails to act on the protest

(FDDA) within 180 days from the date of submission

Remedies of the taxpayer

1. Direct denial - file an appeal with Court of Tax

Appeal (CTA) within 30 days from the receipt

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

2. Indirect denial

a. File an appeal with CTA within 30 days

from the lapse of 180-day period

b. Await the final decision CIR and appeal

such to CTA within 30 days from the

receipt of such decision

6 Denial of Appeal Remedies of the taxpayer

by CTA Division 1. File a motion for reconsideration within 15 days

from the receipt

If denied, file an appeal with CTA en banc

within 15 days from the receipt

7 Denial of Appeal Remedies of the taxpayer

by CTA En banc 1. File a motion for reconsideration within 15days

from the receipt

a. If denied, file an appeal with Supreme Court

within 15 days from the receipt

8 Denial of Appeal Remedies of the taxpayer

by SC Division 1. File a motion for reconsideration within 15days

from the receipt

a. If denied, file an appeal with SC en banc

within 15 days from the receipt

9 Denial of Appeal Remedies of the taxpayer

by SC En banc 1. File a motion for reconsideration within 15days

from the receipt

a. If denied, the taxpayer has no more remedy

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

B. COLLECTION Allowed when the assessment is final, executory

and demandable

Exceptions as to period of Limitation of

Assessment and Collection of Tax

• (a) False & fraudulent return with intent to

evade tax or of failure to file a return- tax may

be assessed or filed without assessment, at

any time within 10 years after the discovery

provided that the fact of fraud shall be

judicially taken cognizance of in the civil or

criminal action for the collection thereof.

• Internal revenue tax as prescribed in (a) may

be collected within 5 years following the

assessment

Methods

1 Distraint- seizure of personal property,

tangible or intangible

a. Actual Distraint- personal property is

physically seized by BIR

Garnishment- distraint of bank

accounts

b. Constructive Distraint- person in

possession of personal property is

made to sign a receipt that he will

preserve the property and will not

dispose of without the express

authority of BIR

WHO CAN COMMENCE DISTRAINT

PROCEEDINGS?

Amount > 1M – CIR

Amount 1M – Revenue District

Officer

2. Levy- seizure of real properties & interest in

or rights to such property

3. Judicial Proceedings

a. Filing of civil case for collection

b. File a criminal case (Tax Evasion)

- 5 years from commission or

discovery, whichever is later

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

C. COMPROMIS Grounds

E 1. Reasonable doubt as to the validity of the claim

against the taxpayer exists

2. Final position of the taxpayer demonstrates a

clear inability to pay the assessed tax

All criminal violations may be compromised, except:

1. Those already filed in court

2. Those involving fraud

Minimum Amounts

1. Financial incapacity- minimum of 10% of the

basic assessed tax

2. Other cases- minimum of 40% of the basic

assessed tax

Instances when approval of the Board is Required

1. Basic tax > 1million

2. Settlement offered is less than the minimum

rates

D. ABATEMENT Grounds

OR 1. Tax appears to be unjustly or excessively

CANCELATIO assessed

N OF TAX 2. Administration and collection costs do not justify

LIABILITY the collection of the amount due

E. SUSPENSION Under the following situations:

OF THE 1. Taxpayer’s reinvestigation request was granted

RUNNING OF 2. Taxpayer cannot be located in the address

STATUTE OF given in the return

LIMITATIONS 3. No property of the taxpayer can be located

4. Taxpayer is out of the country

Suspension shall be for the duration of the situation

plus 60 days thereafter

F. CIVIL 1. SURCHARGE-

PENALTIES 25% in any of the following cases:

a. Failure to file any return and pay the tax due

on time

b. Filing a return with an internal revenue officer

other than those with whom the return is

required to be filed

c. Failure to pay deficiency tax within time

prescribed in the Notice of Assessment

d. Failure to pay the amount of tax due for which

no return is required to be filed

50% in any of the following cases:

a. Willful neglect to file return on time

b. Taxpayer files only after prior notice in writing

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Tax Remedies

TAXATION REVIEW NOTES

from the BIR

Simple neglect (25% surcharge)- files return

after deadline without notice from BIR

Evidence for false or fraudulent return

1. Substantial overstatement (>30%) of

deductions

2. Substantial under declaration (<30%) of

taxable assets, receipts & income

2. INTEREST (12% per annum)

- An increment on any unpaid amount of tax,

assessed from the date prescribed for payment

until the amount is fully paid

Kinds

1. Deficiency Interest- imposed on deficiency tax

due

-Assessed & collected from prescribed payment

date until (whichever comes first):

a. Full payment

b. Issuance of notice and demand by the

Commissioner

2. Delinquency Interest- interest imposed on the

failure of taxpayer to pay:

a. The amount tax due on any return required

to be filed

b. The amount tax due for which no return is

required

c. Deficiency tax, or any surcharge or interest

Double imposition of Interest

- In no case shall deficiency and delinquency

interest be imposed simultaneously

G. REFUND OF Requisites:

TAXES 1. Tax was erroneously or illegally collected by

BIR

2. Taxpayer should file a written claim for refund

with CIR within 2 years from the date of

payment

3. Claim with CIR= denied

File petition for refund with CTA

a. Within 30 days from receipt of denial;

AND

b. Within 2 years from the date of

payment of tax or penalty

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

INDIVIDUALS

1 Those who are citizens of the Philippines at the time

of the adoption of the Constitution

2 Those whose fathers or mothers are citizens of the

RESIDENT Philippines

CITIZEN (RC) 3 Those born before January 17, 1973 of Filipino

mothers, who elect Philippine Citizenship upon

reaching the age of majority; and

4 Those who are naturalized in accordance with law

1 Who establishes to the satisfaction of the

Commissioner the fact of his physical presence

abroad with definite intention to reside therein

2 Works and derives income from abroad and

whose employment thereat requires him to be

physically present abroad most of the time (must

be outside PH for not less than 183 days) during

NON-RESIDENT the taxable year.

CITIZEN (NRC) 3 One who leaves the Philippines to reside abroad as

an immigrant, or for employment on a

permanent basis

4 Citizen previously considered as NRC who arrives to

reside permanently in Phil: NRC for the taxable

year which he arrives with respect to income derived

from sources abroad UNTIL the date of his arrival in

the country

1 OFW, physically present abroad as a consequence

OVERSEAS of employment

CONTRACT

WORKER 2 Salaries & wages= paid by employer abroad and

(OCW) is not borne by anyone in the Phil

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

3 Duly registered as such with POEA with a valid

Overseas Employment Certificate (OEC)

4 Seaman who receives compensation for services

rendered abroad as a member of the complement

vessel engaged exclusively in international trade

Requirements:

a. Duly registered as such with POEA with a valid

OEC

b. With a valid Seafarer’s Identification Record

Book (SIRB) or Seaman’s Book issued by

Maritime Industry Authority (MARINA)

NOT A CITIZEN; alien with acquired residence in the PH

retains status as resident until he abandons the same and

actually departs from PH

1 An alien actually present in the Philippines who is

RESIDENT not a mere transient or sojourner

ALIEN (RA)

2 Has a definite purpose that requires an extended

stay;

PH= temporary home

3 Has no definite intention as to his stay

NONRESIDENT NON-RES & NON-CIT

ALIEN ENGAED 1 Alien engaged in trade or business in PH

IN TRADE OR 2 Alien who come to PH for an aggregate period of

BUSINESS more than 180 days

(NRA)

NONRESIDENT

ALIEN NOT

ENGAED IN Residual definition

TRADE OR

BUSINESS

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

SITUS OF TAXABLE INCOME OF INDIVIDUALS

NATIONALITY/RESIDENCE INCOME WITHIN INCOME WITHOUT

Resident citizen ✓ ✓

Resident Alien ✓

NRC ✓

NRA ✓

TAXABILITY OF DIVIDENDS

RECEIVED BY KIND OF TAX

DC Not taxable

DIVIDENDS RFC No taxable

DECLARED BY NRFC 25%; tax sparing credit

DOMESTIC CORP Resident or Citizen 10% FWT

NRA ETB 20% FWT

NRA NETB 25% FWT

DC Ordinary income tax

DIVIDENDS Foreign Corporation Not taxable

DECLARED BY

FOREIGN CORP Resident Citizen Ordinary income tax

NRC, NRA, RA Not taxable

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

CORPORATIONS

DEFINITION

- Artificial being created by operation of law, having the right of succession

and the powers, attributes and properties expressly authorized by law or

incidental to its existence

- Corporation shall include:

a. One Person corporation (OPC)

- corporation w/ a single stockholder provided that only a NATURAL

person, trust or an estate may form OPC

b. Partnerships, no matter how created or organized;

c. Joint stock companies

- Group of individuals, acting jointly, establish and operate

business enterprise under an artificial name, with an invested

capital divided into transferrable shares, an elected BOD and

other corporate characteristics, but operating without formal

government authority

d. Joint accounts (cuentas en participacion)

- Constituted when one interests himself in the business of another

by contributing capital and sharing P/L in proportion agreed

upon.

- Not subject to any formality; orally or in writing

- All organizations with substantially salient features of a

corporation to be taxable as a corporation

e. Associations; or

f. Insurance companies

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

- Corporation does NOT include:

a. General Professional Partnerships (GPP)

b. Joint venture or consortium formed for the purpose of:

1. Construction projects, or

2. Engaging in coal, petroleum geothermal and other energy operations

pursuant to an operating or consortium agreement under a service

contract with the government

ELABORATION ON JOINT VENTURE OR CONSORTIUM (2)

- A commercial undertaking by 2 or more persons, differing from a

partnership in that it relates to the disposition of a single lot of goods or the

completion of a single project

- GR: Taxable as corporation

Exc. Joint ventures described in 2(a) and (b)

Additional requirements for tax exemption:

1. JV/C formed for undertaking construction projects

a. Should involve joining or pooling of resources by licensed local

contracts; licensed as general contractor by the PCAB of DTI

b. Local contractors are engaged in construction business

c. JV must likewise be duly licensed as such by PCAB of DTI

JV involving FOREIGN CONTRACTORS

a. The member foreign contractor is covered by a special license as

contractor by PCAB of DTI

b. Construction project is certified by the tendering agency (government

office) that the project is a foreign financed/ internationally-funded

project and that international bidding is allowed under Bilateral

Agreement entered into by the PH gov’t and the foreign/ international

financing institution pursuant to RA 4566 (Contractor’s License Law)

2. Engaging in petroleum, coal, geothermal and other energy operations

pursuant to an operating or consortium agreement under a service contract

with the gov’t

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

CLASSIFICATION OF CORPORATE TAXPAYERS

1. Domestic Corporation (DC)

- Organized in the Philippines or under its law

2. Resident Foreign Corporation (RFC)

- Created or organized in a foreign country or under the laws of a foreign

country and engaged in business in the Philippines

3. Non-resident Foreign Corporation (NRFC)

- Created or organized in a foreign country or under the laws of a foreign

country and is not engaged in business in the Philippines

EXEMPT CORPORATIONS

1 Labor, agricultural or horticultural organization not organized principally for

profit;

2 Mutual savings bank not having a capital stock represented by shares, and

cooperative bank without capital stock organized and operated for mutual

purposes and without profit;

3 A beneficiary society, order or association, operating for the exclusive

benefit of the members such as a fraternal organization operating under the

lodge system, or a mutual aid association or a nonstock corporation

organized by employees providing for the payment of life, sickness accident,

or other benefits exclusively to the members of such society, order, or

association, or nonstock corporation or their dependents;

4 Cemetery company owned and operated exclusively for the benefit of its

members;

5 Nonstock corporation or association organized and operated exclusively for

religious, charitable, scientific, athletic, or cultural purposes, or for the

rehabilitation of veterans, no part of its net income or asset shall belong to

or inure to the benefit of any member, organizer, officer or any specific

person;

6 Business league, chamber of commerce, or board of trade, not organized

for profit and no part of the net income of which inures to the benefit of any

private stockholder or individual;

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

7 Civic league or organization not organized for profit but operated exclusively

for the promotion of social welfare;

8 A non-stock and nonprofit educational institution;

9 Government educational institution;

10 Farmers' or other mutual typhoon or fire insurance company, mutual ditch

or irrigation company, mutual or cooperative telephone company, or like

organization of a purely local character, the income of which consists solely

of assessments, dues, and fees collected from members for the sole

purpose of meeting its expenses; and

11 Farmers', fruit growers', or like association organized and operated as a

sales agent for the purpose of marketing the products of its members and

turning back to them the proceeds of sales, less the necessary selling

expenses on the basis of the quantity of produce finished by them

GOVERNMENT-OWNED OR CONTROLLED CORPORATIONS

All corporations, agencies or instrumentalities owned or controlled by the

Government shall be taxable like <ordinary corporations=.

However, the following shall be exempt:

1. Government Service and Insurance System (GSIS)

2. Social Security System (SSS)

3. Home Development Mutual Fund (HDMF aka Pag-ibig)

4. Philippine Health Insurance Corporation (PHIC)

5. Local Water Districts (RA 10026)

NOTE:

• PCSO is taxable beginning Jan. 1, 2018 (TRAIN Law)

• HDMF or Pag-ibig is exempt only upon the effectivity of CREATE Law

(April 11, 2021)

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

INCOME TAXES ON CORPORATION

TAX

TYPE SOURCES APPLICABLE TAX

BASE

Ordinary Income:

− RCIT 20% for MSME; 25% for non-MSME

Passive Income: FWT

− Interest Income: 20%;15%

Net − Royalties: 20%

DC World

Income − Dividend: Exempt

Capital Gains on sale of

• shares of stock of DC sold directly to

buyer: 15%

• sale of real property in PH classified as

capital asset: 6%

Ordinary Income

- RCIT 25%

Passive Income: FWT

Net - Interest Income: 20%;15%

RFC PH - Royalties: 20%

Income

- Dividend: Exempt

Capital Gains on sale of shares of stock of DC

sold directly to buyer

- CGT 15%

Ordinary Income

- FWT 25%

Passive Income

Gross - FWT 25%

NRFC PH

Income - FCDU: Exempt:

Capital Gains on sale of shares of stock of DC

sold directly to buyer

- CGT 15%

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

Taxability of Individuals and Cor por ations

TAXATION REVIEW

DC with total assets 100M AND

net taxable income 5M (aka Micro

** Beg. July Small and Medium Enterprises), Reduced

1, 2020 excluding land on which the particular to 20%

business entity’s office, plant, and

equipment are situated

Type of Income Applicable Tax

DC & RFC: RCIT

Regular or ordinary income

NRFC: FWT

Passive income (Interest Income,

Royalty Income in PH, Dividend FWT

Income in PH)

Capital gains on • CGT applicable to all

• Sales of shares of stock of DC corporations (15%)

sold directly to a buyer

• Sale of real property in PH • CGT applicable only to DC

classified as capital asset (6%)

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

1. House Bill no. 123 was transmitted to the Senate and was passed accordingly.

The Bill was submitted to the President for his signature on August 1, 2021. On

September 5, 2021, the President stated on a media interview that he does not

intend to sign the bill into law that is why he is not yet acting on the bill. What is

the status of the House Bill no. 123?

a. The bill is automatically vetoed upon the lapse of 15 days

b. The bill is automatically lapsed into law after 30 days

c. The bill’s effectivity is suspended until the President signed the same.

d. The bill has become effective until the President vetoes it.

The correct answer is: The bill is automatically lapsed into law after 30 days

PRESIDENTIAL ACTION ON THE BILL

1. If the bill is approved the President, the same is assigned an RA number

and transmitted to the House where it originated

2. If the bill is vetoed, the same, together with a message citing the reason

for the veto, is transmitted to the House where the bill originated.

2. That courts cannot issue injunction against the government’s effort to collect

taxes is justified by

a. The lifeblood doctrine

b. Imprescriptibility of taxes

c. The ability to pay theory

d. The doctrine of estoppel

The correct answer is: The Lifeblood Doctrine

This <lifeblood doctrine= has been invoked to validate many of the Bureau of

Internal Revenue’s (BIR) action, including advanced collection of taxes, the no

injunction rule in taxation, taxes being a preferred credit, among others.

MANIFESTATION OF THE LIFEBLOOD DOCTRINE/THEORY:

• No Estoppel against the Government

• Collection of taxes cannot be enjoined (stopped) by injunction

• Taxes could not be the subject of compensation or set-off

• A valid tax may result in the destruction of the taxpayer's property

• Right to select objects (subjects) of taxation

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

3. The principal purpose of taxation is

a. To encourage the growth of home industries through the proper use of

tax exemptions and tax incentives

b. To implement the police power of the state

c. The reduce excessive inequalities of wealth

d. To raise revenues for governmental needs

The correct answer is: To raise revenues for governmental needs

PURPOSES OF TAXATION

1. Primary Purpose (also called Revenue or Fiscal Purpose)

- To raise revenues/funds to defray the necessary expenses of the

government

2. Secondary Purpose:

a. Regulatory Purpose

- employed as a devise for regulation or control (to implement the

police power of the State for the promotion of the general

welfare) by means of which certain effects or conditions

envisioned by the government may be achieved.

b. Compensatory Purposes

- Reduction of Social Inequality

- Economic Growth

- Protect local industries against unfair competition ³

protectionism

4. In this type of tax, non-payment is constitutionally exempted from imprisonment.

a. Income tax

b. Value-Added Tax

c. Poll tax

d. All of the above

The correct answer is: Poll Tax

Article III, Section 20 of the 1987 Constitution- No person shall be

imprisoned for debt or non-payment of a poll tax.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

5. The aspects of taxation are

a. Legislative in character

b. Executive in character

c. Shared by the legislative and executive departments

d. Judicial in character

The correct answer is: Legislative in character

The power to tax is purely legislative in character. It is up to Congress

which will determine the subjects or objects to be taxed, purpose, the amount of

the rate and the manner and means of its collection.

6. Taxation as distinguished from police power and power of eminent domain

a. Property is taken to promote the general welfare

b. May be exercised only by the government

c. Operates upon the whole citizenry

d. There is generally no limit as to the amount that may be imposed

The correct answer is: There is generally no limit as to the amount that may be

imposed.

With regards to the amount of imposition, taxation has no limit. In police power,

the amount is ssufficient to cover cost of the license and the necessary expenses

of police surveillance and regulation while in eminent domain, there is no

imposition- the owner is paid equivalent to the fair value of his property.

7. Which of the inherent powers may be exercised even by public service

corporations and public entities?

a. Power of taxation

b. Police power

c. Power of eminent domain

d. A and C

The correct answer is: Power of eminent domain

The authority for eminent domain may be granted to public service/ utility

companies.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

8. The power to acquire private property upon payment of just compensation for

public purpose.

a. Power of taxation

b. Police power

c. Power of eminent domain

d. Veto power

The correct answer is: Power of eminent domain

The purpose of eminent domain is to take private property for public use

wherein the owner is paid equivalent to the fair value of his property.

9. The power to regulate liberty and property to promote the general welfare.

a. Power of taxation

b. Police power

c. Power of eminent domain

d. Veto power

The correct answer is: Police power

10. The inherent powers of the government are primarily ________ in character.

a. Executive

b. Legislative

c. Judicial

d. Quasi-Judicial

The correct answer is: Legislative

Similarities among the 3 Inherent Powers

1. Inherent in the State

2. Exist independently of the constitution although the conditions for their

exercise may be prescribed by the constitution.

3. Constitutes the 3 methods by which the State interfere with private rights

and property

4. Legislative in nature and character.

5. Presuppose an equivalent compensation received, directly or indirectly,

by the persons affected.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

11. Which of the following inherent powers of the state is inferior to

constitutional right of non-impairment of obligations of contracts?

a. Power of taxation

b. Police power

c. Power of eminent domain

d. None of the above

The correct answer is: Power of taxation

As to relationship to the non-impairment of obligations clause of the

Constitution:

1. Police power – superior to the clause

2. Power of eminent domain – inferior to the clause

3. Taxation – inferior to the clause

12. Which of the following statements is correct?

a. Income tax is an indirect tax.

b. Our National Internal Revenue Laws are criminal in nature

c. The theory of taxation states that the power of taxation is supreme,

plenary, unlimited, and comprehensive.

d. Taxation is subject to inherent and constitutional limitations.

The correct answer is: Taxation is subject to inherent and constitutional

limitations.

Choice A is incorrect because income tax is a direct tax which is

imposed directly on the liable person & cannot be shifted to another. An

undirect tax is demanded from a person who is allowed to transfer the burden

of taxation to another.

13. This is an inherent limitation on the power of taxation.

a. Rule on uniformity and equity in taxation

b. Due process of law and equal protection of the laws

c. Non-impairment of the jurisdiction of the Supreme Court in tax cases

d. Tax must be for public purpose

The correct answer is: Tax must be for public purpose.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

14. This is a constitutional limitation on the power of taxation.

a. Tax laws must be applied within the territorial jurisdiction of the state

b. Exemption of government agencies and instrumentalities from taxation

c. No appropriation of public money for religious purposes

d. Power to tax cannot be delegated to private persons or entities

inherent

The correct answer is: No appropriation of public money for religious purposes

Choice A refers to situs of taxation or territoriality, choice B refers to tax

exemption of the government, and choice D refers to the non-delegability of the

Taxing Power (enactment of tax laws) which are all inherent limitations of

taxation.

15. The sources of revenue should be sufficient to meet the demands of public

expenditures.

a. Equality or Theoretical Justice

b. Administrative Feasibility

c. Fiscal Adequacy

d. Life Blood Doctrine

The correct answer is: Fiscal Adequacy

Principles of a Sound Tax System

1. Fiscal Adequacy

− The sources of government revenue must be sufficient to meet

government expenditures and other public needs

2. Theoretical Justice

− must be based on the taxpayer's ability to pay

− taxation must be progressive conformably with the constitutional

mandate that congress shall evolve a progressive system of taxation.

3. Administrative Feasibility

− Tax laws must be capable of convenient, just and effective

administration free from confusion and uncertainty

− should have the merits of simplicity, flexibility and diversity.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

16. Which of the following is not an inherent limitation of taxation?

a. Territoriality

b. International Comity

c. For public purpose

d. Non-impairment of obligation and contract

The correct answer is: Non-impairment of obligation and contract

Inherent Limitations of Taxation

1. For public purpose

2. Situs of taxation/territoriality

1. International Comity or Treaty

2. 4. Non-delegability of the Taxing Power (Enactment of Tax Laws)

17. Which of the following is not a tax mechanism to minimize the impact of

double taxation?

a. Tax shifting

b. Tax levy

c. Tax capitalization

d. Tax transformation

The correct answer is: Tax Levy

Tax shifting

- Transfer of burden of tax to another without violating the law

Tax capitalization

- the seller is willing to lower the price of the commodity provided

the taxes will be shouldered by the buyer

Tax Transformation

- the manufacturer absorbs the additional taxes imposed by the

government without passing it to the buyers for fear of loss of

his/its market. Instead, he/it increases quantity of production,

thereby turning their units of production at lower cost resulting to

the transformation of the tax into gain through the medium of

production.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

18. The tax imposed should be proportionate to the taxpayer's ability to pay.

a. Equality or Theoretical Justice

b. Administrative Feasibility

c. Fiscal Adequacy

d. Life Blood Doctrine

The correct answer is: Equality or Theoretical Justice

Principles of a Sound Tax System

1. Fiscal Adequacy

− The sources of government revenue must be sufficient to meet

government expenditures and other public needs

2. Theoretical Justice

− must be based on the taxpayer's ability to pay

− taxation must be progressive conformably with the constitutional

mandate that congress shall evolve a progressive system of taxation.

3. Administrative Feasibility

− Tax laws must be capable of convenient, just and effective

administration free from confusion and uncertainty

− should have the merits of simplicity, flexibility and diversity.

19. Withholding is:

a. A method of reducing a taxpayer’s income.

b. A method by which the government collect taxes at the time of its

deadline.

c. A method by which the government collect taxes in advance.

d. A method of increasing a taxpayer’s income.

The correct answer is: A method by which the government collect taxes in

advance

Withholding Taxes is a corporate tax obligation paid by taxpayers

engaged in trade or business activities in the Philippines. Employers

withhold from the salary of their employees every month and each amount

withheld serves as an advanced payment for the employer's Income Taxes

during the business year.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

20. The tax laws must be capable of convenient, just and effective

administration.

a. Equality or Theoretical Justice

b. Administrative Feasibility

c. Fiscal Adequacy

d. None of the above

The correct answer is: Administrative Feasibility

Principles of a Sound Tax System

1. Fiscal Adequacy

− The sources of government revenue must be sufficient to meet

government expenditures and other public needs

2. Theoretical Justice

− must be based on the taxpayer's ability to pay

− taxation must be progressive conformably with the constitutional

mandate that congress shall evolve a progressive system of taxation.

3. Administrative Feasibility

− Tax laws must be capable of convenient, just and effective

administration free from confusion and uncertainty

− should have the merits of simplicity, flexibility and diversity.

21. When the law itself provides for non-payment of taxes; such tax escape is

known as:

a. Tax evasion

b. Tax holiday

c. Tax minimization

d. Tax avoidance

The correct answer is: Tax holiday

1. Evasion or Dodging

− taxpayer uses unlawful means to evade or lessen the payment tax

2. Avoidance or tax minimization

− reduction or totally escaping payment of tax through legally

permissible

− means of tax

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

22. The principles of a sound tax system exclude

a. Economic efficiency

b. Fiscal adequacy

c. Theoretical justice

d. Administrative feasibility

The correct answer is: Economic efficiency

Principles of a Sound Tax System

1. Fiscal Adequacy

− The sources of government revenue must be sufficient to meet

government expenditures and other public needs

2. Theoretical Justice

− must be based on the taxpayer’s ability to pay

− taxation must be progressive conformably with the constitutional

mandate that congress shall evolve a progressive system of taxation.

3. Administrative Feasibility

− Tax laws must be capable of convenient, just and effective

administration free from confusion and uncertainty

− should have the merits of simplicity, flexibility and diversity.

23. The Marshall Doctrine justifies:

a. The use of taxation as an implement of police power.

b. The imposition of taxes in progressive rates.

c. The bias of taxation for the protection of the less fortunate.

d. The power of the government to collect taxes even without the grant of

the Constitution.

The correct answer is: The use of taxation as an implement of police power

Because of the absence of inherent and constitutional limitations, the power to

tax is comprehensive, plenary, supreme & unlimited.

<The power to tax includes the power to destroy=

- Justice Marshall

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW

24. Substituted filing of income tax returns is a manifestation of which principle

of a sound tax system?

a. Equality

b. Theoretical justice

c. Fiscal adequacy

d. Administrative feasibility

The correct answer is: Administrative Feasibility

25. Statement 1 – The point on which a tax is originally imposed is impact of

taxation.

Statement 2 – Police power is superior to the non-impairment clause of the

constitution

Statement 3 – As a rule, taxes are subject to set-off or compensation

Statement 4 – As rule, provisions on the validity of tax exemptions are resolved

liberally in favor of the taxpayer

Statement 1 Statement 2 Statement 3 Statement 4

a. True False False False

b. True True False True

c. True True False False

d. False False False False

The correct answer is: Correct answer is choice C.

Statement 1 is true.

Statement 2 is true because police power is broader than taxation and eminent

domain because it involves a general power to make and implement laws and

as to relationship to the non-impairment of obligations clause of the Constitution,

police power is superior to the clause while power of eminent domain and

Taxation are inferior to the clause.

Statement 3 is false because based on the other doctrines/ rules in taxation,

taxes are not subject to set-off or legal compensation because the government

and the taxpayer are not mutual creditors and debtors of each other.

Statement 4 is false provisions granting tax exemptions are construed strictly

against the taxpayer claiming tax exemption and liberally in favor of the

government.

Downloaded by Lotivio Ma. Mica (lotiviomica@gmail.com)

lOMoARcPSD|30374161

TAXATION REVIEW