You might also like

- Tanahu Hydropower PDFDocument23 pagesTanahu Hydropower PDFpitamberNo ratings yet

- 3Document45 pages3Alex liaoNo ratings yet

- Behavioural FinanceDocument14 pagesBehavioural FinanceRadhakrishna MishraNo ratings yet

- Business Model Canvas: Key Partners Key Activities Value Propositions Customer Relationships Customer SegmentsDocument1 pageBusiness Model Canvas: Key Partners Key Activities Value Propositions Customer Relationships Customer SegmentsShukri FaezNo ratings yet

- Cost of CapitalDocument37 pagesCost of Capitalrajthakre81No ratings yet

- MBS Corporate Finance 2023 Slide Set 3Document104 pagesMBS Corporate Finance 2023 Slide Set 3PGNo ratings yet

- Free Book On Basic Financial ModellingDocument100 pagesFree Book On Basic Financial ModellingCareer and TechnologyNo ratings yet

- TESLA - Business ModelDocument21 pagesTESLA - Business ModelShiva Kumar 91100% (6)

- Tax Planning With Refrence To Employee's RemunerationDocument34 pagesTax Planning With Refrence To Employee's RemunerationRishabh Jain83% (6)

- Waterfront Development PrinciplesDocument72 pagesWaterfront Development PrinciplesNicholas Socrates100% (2)

- Cash Budgeting SolutionsDocument5 pagesCash Budgeting Solutionshussain200055100% (1)

- Chap 9 - 12 SolutionsDocument51 pagesChap 9 - 12 SolutionsSasank Tippavarjula81% (16)

- Capital GainsDocument11 pagesCapital GainsDIYA HALDER 21212020No ratings yet

- Capital Gains - An Overview: Ca Ameet PatelDocument51 pagesCapital Gains - An Overview: Ca Ameet PatelPrasun TiwariNo ratings yet

- Capital GainsDocument5 pagesCapital Gains203 129 PremNo ratings yet

- Gbs 520:financial and Management Accounting: Bryson MumbaDocument46 pagesGbs 520:financial and Management Accounting: Bryson MumbaSANDFORD MALULUNo ratings yet

- Principles of Corporate ValuationDocument14 pagesPrinciples of Corporate ValuationSubhrodeep DasNo ratings yet

- 10k Analysis Kendra MarutaniDocument13 pages10k Analysis Kendra Marutaniapi-700375052No ratings yet

- Capital Gains - IndexationDocument22 pagesCapital Gains - IndexationTomy MathewNo ratings yet

- Cost SheetDocument3 pagesCost SheetBig thinkNo ratings yet

- Pln-Cmams - MERGER AND ACQUISITION PART 2Document31 pagesPln-Cmams - MERGER AND ACQUISITION PART 2dwi suhartantoNo ratings yet

- Company Fundamentals - Income StatementDocument28 pagesCompany Fundamentals - Income StatementThắm TrầnNo ratings yet

- Financial Study of ACCDocument65 pagesFinancial Study of ACCAmitabh TiwariNo ratings yet

- Treasury Management: Capital Structure and Company ValuationDocument47 pagesTreasury Management: Capital Structure and Company ValuationSyed Saad ManzoorNo ratings yet

- Corporate Financial Reporting: Session 6 and 7: PGP 2018 20 Preparing and Understanding Income StatementDocument52 pagesCorporate Financial Reporting: Session 6 and 7: PGP 2018 20 Preparing and Understanding Income StatementArty DrillNo ratings yet

- Heritage Foods CaseDocument14 pagesHeritage Foods CasePriya DurejaNo ratings yet

- Tax Law Project On: Capital Gain and Capital AssetsDocument15 pagesTax Law Project On: Capital Gain and Capital AssetsAazamNo ratings yet

- 02 CVP HandoutDocument23 pages02 CVP HandoutRishika RathiNo ratings yet

- Chapter IIIDocument54 pagesChapter IIINesri YayaNo ratings yet

- 0.2 Investment Appraisal Part 2Document28 pages0.2 Investment Appraisal Part 2সৈকত হাবীবNo ratings yet

- Book 1Document8 pagesBook 1dhrivsitlani29No ratings yet

- Accountancy ProjectDocument27 pagesAccountancy ProjectLINCY ELDHONo ratings yet

- AFA - Earnings Drivers EtcDocument24 pagesAFA - Earnings Drivers EtcHYUN JUNG KIMNo ratings yet

- BYOBB Business Plan Financial ProjectionsDocument11 pagesBYOBB Business Plan Financial ProjectionsSourabh SinghNo ratings yet

- Capital Gains Index Numbers.Document2 pagesCapital Gains Index Numbers.cosmic roverNo ratings yet

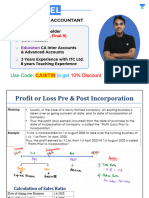

- Profit Prior To IncorporationDocument11 pagesProfit Prior To IncorporationVasu JainNo ratings yet

- Captial Gain PresentationDocument18 pagesCaptial Gain Presentationvrmahajan59No ratings yet

- Unit III Capital Budgeting Decision CriteriaDocument55 pagesUnit III Capital Budgeting Decision CriteriaVivek ValiantNo ratings yet

- Methods of Calculating Depreciation ExerciseDocument17 pagesMethods of Calculating Depreciation ExerciseASMARA HABIBNo ratings yet

- FMCF - Unit 2Document20 pagesFMCF - Unit 2Deepak VermaNo ratings yet

- Chapter 3 - Understanding The Income StatementDocument68 pagesChapter 3 - Understanding The Income StatementNguyễn Yến NhiNo ratings yet

- Session8-Depreciation, Tax and Cash FlowDocument11 pagesSession8-Depreciation, Tax and Cash FlowVismay WadiwalaNo ratings yet

- Capital StructureDocument19 pagesCapital StructureRatul HasanNo ratings yet

- Be AnalysisDocument32 pagesBe AnalysisMuskan GoyalNo ratings yet

- Profit Prior To IncorporationDocument12 pagesProfit Prior To Incorporationhk7012004No ratings yet

- MIS - Resource Allocation - Tanaporn S. - Id 6519013 - Smart MBA Sec8Document7 pagesMIS - Resource Allocation - Tanaporn S. - Id 6519013 - Smart MBA Sec8ธนพร สกุลอนันท์No ratings yet

- Lec6 - Plant Assets DepreciationDocument58 pagesLec6 - Plant Assets DepreciationDylan Rabin Pereira100% (1)

- Investment Spending: Session 06Document15 pagesInvestment Spending: Session 06Raj PatelNo ratings yet

- Capsule Corporation Excel-2Document449 pagesCapsule Corporation Excel-2Nicola ZucchettiNo ratings yet

- Lecture 1 Manufacturing Project Appraisal, Selection & FeasibilityDocument41 pagesLecture 1 Manufacturing Project Appraisal, Selection & FeasibilityMuhammadNo ratings yet

- Improvement: Aggregate FollowingDocument18 pagesImprovement: Aggregate FollowingGauravNo ratings yet

- 5UEFM Revised 01Document45 pages5UEFM Revised 01Olivia KhinNo ratings yet

- DEVELOPMENT APPRAISAL Rev 02Document25 pagesDEVELOPMENT APPRAISAL Rev 02sarcozy922No ratings yet

- Accounting Topic 3 SlidesDocument96 pagesAccounting Topic 3 Slidesddosanjh939No ratings yet

- CF EstimationDocument11 pagesCF Estimationsazzad_ßĨdNo ratings yet

- International Capital BudgetingDocument43 pagesInternational Capital BudgetingRammohanreddy RajidiNo ratings yet

- Topic 2 Part B Lecture SlidesDocument11 pagesTopic 2 Part B Lecture SlidesLinh Le Thi ThuyNo ratings yet

- Basic Finance - Day1Document72 pagesBasic Finance - Day1Raj BharathNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document34 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Garima BansalNo ratings yet

- Assignment 2 Sample IIDocument1 pageAssignment 2 Sample IImechanical singhNo ratings yet

- CMA PGP23 ClassPPT Module3 PDFDocument106 pagesCMA PGP23 ClassPPT Module3 PDFSaransh Chauhan 23100% (1)

- Week5 Ch6 in Class Examples-PrintDocument8 pagesWeek5 Ch6 in Class Examples-PrintnasduioahwaNo ratings yet

- المحاضرة التاسعة والعاشرةDocument6 pagesالمحاضرة التاسعة والعاشرةAly SaadNo ratings yet

- FinUnderstandingacialn StatementsDocument77 pagesFinUnderstandingacialn StatementsrookeeNo ratings yet

- FINACC - Depreciation, Long-Lived Nonmonetary Assets and Their Amortization - 031318Document8 pagesFINACC - Depreciation, Long-Lived Nonmonetary Assets and Their Amortization - 031318ventus5thNo ratings yet

- Part III - Developing The Entrepreneurial PlanDocument24 pagesPart III - Developing The Entrepreneurial Plannivedita choudhuryNo ratings yet

- Equity ValuationDocument53 pagesEquity ValuationDevanshi ShahNo ratings yet

- Economic Review 2012 Vol. OneDocument326 pagesEconomic Review 2012 Vol. OneKent WhiteNo ratings yet

- SKF KogelaharDocument45 pagesSKF Kogelaharjupriadi sitompulNo ratings yet

- Locon UI Delegates MailingDocument14 pagesLocon UI Delegates MailingNurul ArumNo ratings yet

- Infosys ProfileDocument3 pagesInfosys ProfileshreemugNo ratings yet

- Face Mask, Gloves, PPE Kit Offer Price PDFDocument2 pagesFace Mask, Gloves, PPE Kit Offer Price PDFDipak GohilNo ratings yet

- A Report On Corporate Governance Issue of Dutch Bangla Bank LimitedDocument12 pagesA Report On Corporate Governance Issue of Dutch Bangla Bank LimitedVictor DasNo ratings yet

- Supression NetAppDocument6 pagesSupression NetAppsteve jonesNo ratings yet

- Fiscal Policy and Developments-FinalDocument108 pagesFiscal Policy and Developments-FinalShime HI RayaNo ratings yet

- Swellex SpartanDocument2 pagesSwellex SpartanJosue Mario RamirezNo ratings yet

- Professional Photographer Bank StatementDocument6 pagesProfessional Photographer Bank StatementDhiraj Kumar PradhanNo ratings yet

- Eprocurement System Government of IndiaDocument2 pagesEprocurement System Government of Indiasugirtha pradeepNo ratings yet

- Personal Computer Case Study SolutionDocument3 pagesPersonal Computer Case Study Solutionfaraz ahmad khanNo ratings yet

- AFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Document3 pagesAFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Judith CastroNo ratings yet

- Agreement Establishing The WtoDocument7 pagesAgreement Establishing The WtoShahadath FaroukNo ratings yet

- 1) Research MethodologyDocument4 pages1) Research MethodologyRaj SriniNo ratings yet

- Economics of A Small Premium WineryDocument5 pagesEconomics of A Small Premium WineryIshan RastogiNo ratings yet

- Secretary CertificateDocument2 pagesSecretary CertificateJhoanna TriaNo ratings yet

- Thambivilas Business Proposal PDFDocument94 pagesThambivilas Business Proposal PDFkangayanNo ratings yet

- Countries, Capital and CoutriesDocument8 pagesCountries, Capital and CoutriesJagannath JagguNo ratings yet

- Apna PPT VCDocument29 pagesApna PPT VCRahul MehtaNo ratings yet

- FASTag Application FormDocument4 pagesFASTag Application FormPurav PatelNo ratings yet

- GI Book 6e-170-172Document3 pagesGI Book 6e-170-172ANH PHAM QUYNHNo ratings yet