You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- SSRN-id3861152 Pablo FernandezDocument17 pagesSSRN-id3861152 Pablo FernandezAngus SadpetNo ratings yet

- 2023 Market Risk Premium and Risk Free RateDocument16 pages2023 Market Risk Premium and Risk Free RateDanu Appraisal100% (2)

- SSRN Id4407839Document16 pagesSSRN Id4407839Nina RatnaNo ratings yet

- Risk-free rate & MRP 2020Document15 pagesRisk-free rate & MRP 2020050610220838No ratings yet

- Market Risk Premium and Risk-Free Rate Used For 69 Countries in 2019. A Survey (2019) - Pablo Fernandez, Mar Martinez, Isabel Fernández AcínDocument15 pagesMarket Risk Premium and Risk-Free Rate Used For 69 Countries in 2019. A Survey (2019) - Pablo Fernandez, Mar Martinez, Isabel Fernández AcínSimon BerruttiNo ratings yet

- 92 - Fernandez Market Risk Premium Used in 71 Countries 2016Document16 pages92 - Fernandez Market Risk Premium Used in 71 Countries 2016Angus SadpetNo ratings yet

- SiemensDocument9 pagesSiemensCam SNo ratings yet

- Country Risk Damodaran-AnalysisDocument42 pagesCountry Risk Damodaran-AnalysisSantiago GómezNo ratings yet

- Riesgo PaisDocument174 pagesRiesgo PaisDennis NinataypeNo ratings yet

- PC_Strategy_Mutual_Fund_Tracker_–_Mar_24_20240412140115Document7 pagesPC_Strategy_Mutual_Fund_Tracker_–_Mar_24_20240412140115Mohammed Israr ShaikhNo ratings yet

- Financial Strategy Analysis and BenchmarkingDocument36 pagesFinancial Strategy Analysis and BenchmarkingDaniel AjanthanNo ratings yet

- Auto Post COVID-19 - 052920 - tcm9-249607Document10 pagesAuto Post COVID-19 - 052920 - tcm9-249607Bidyut Bhusan PandaNo ratings yet

- Aid4trade17 Chap7 eDocument24 pagesAid4trade17 Chap7 eSisilia MarsheilaNo ratings yet

- LDM Updates and Reminders Submission RatesDocument12 pagesLDM Updates and Reminders Submission RatesChristine Joy E. Sanchez-CasteloNo ratings yet

- Ucl Edi Data Report 2018-22finalDocument28 pagesUcl Edi Data Report 2018-22finalkeshavaNo ratings yet

- BusinessPlanExportDocument158 pagesBusinessPlanExportPaola LoloNo ratings yet

- TEAM PILLAR: MOBILE APP FOR CNSC CAFETERIA DATA GATHERINGDocument29 pagesTEAM PILLAR: MOBILE APP FOR CNSC CAFETERIA DATA GATHERINGKhate BautistaNo ratings yet

- IFAC Beyond G20 Sustainability Reporting AssuranceDocument43 pagesIFAC Beyond G20 Sustainability Reporting AssuranceReza MuliaNo ratings yet

- The Rise of Customer Data Platforms in 2021Document28 pagesThe Rise of Customer Data Platforms in 2021Common UserNo ratings yet

- Pitch Madison 2022 PDFDocument67 pagesPitch Madison 2022 PDFpoorva narangNo ratings yet

- LPA Business Climate Survey 2021 FinalDocument23 pagesLPA Business Climate Survey 2021 FinalmohamedNo ratings yet

- Application (30 Points) :: and Monitoring Schedule For The Next Year Based On The Results From The Outside ReviewDocument7 pagesApplication (30 Points) :: and Monitoring Schedule For The Next Year Based On The Results From The Outside Reviewijaz afzalNo ratings yet

- GROUP 1 - Final Presentation: Financial Metrics in Business and Services A.Y. 2021-2022Document24 pagesGROUP 1 - Final Presentation: Financial Metrics in Business and Services A.Y. 2021-2022Alberto FrancesconiNo ratings yet

- BCG India Economic Monitor Jan 2021Document33 pagesBCG India Economic Monitor Jan 2021akashNo ratings yet

- (Template) DOH CSM ReportDocument8 pages(Template) DOH CSM Reportbpdh.nursingserviceNo ratings yet

- GCA Altium Digital - Media & Internet Monitor Q3 2020Document26 pagesGCA Altium Digital - Media & Internet Monitor Q3 2020John SmithNo ratings yet

- Ctryprem July 20Document171 pagesCtryprem July 20Chulbul PandeyNo ratings yet

- R9 News Release Ghanaians Bemoan Economic Conditions Afrobarometer v2 18july22Document3 pagesR9 News Release Ghanaians Bemoan Economic Conditions Afrobarometer v2 18july22Fuaad DodooNo ratings yet

- Statista Ecommerce PerúDocument81 pagesStatista Ecommerce PerúJose VeraNo ratings yet

- Road Safety in Romania - Traffic Accidents, Crash, Fatalities & Injury Statistics - GRSFDocument4 pagesRoad Safety in Romania - Traffic Accidents, Crash, Fatalities & Injury Statistics - GRSFFabio BrazilNo ratings yet

- Global Wireless Matrix 2Q04 Sept 04Document140 pagesGlobal Wireless Matrix 2Q04 Sept 04ly_tran1No ratings yet

- Road Safety in Brazil - Traffic Accidents, Crash, Fatalities & Injury Statistics - GRSFDocument4 pagesRoad Safety in Brazil - Traffic Accidents, Crash, Fatalities & Injury Statistics - GRSFFabio BrazilNo ratings yet

- Healthcare and Life Science Industry: Quarterly UpdateDocument12 pagesHealthcare and Life Science Industry: Quarterly UpdateMicaela Agostina Del SantoNo ratings yet

- India's $14B beauty industryDocument71 pagesIndia's $14B beauty industryharyroyNo ratings yet

- 2020 Engagement Survey Results AnalysisDocument45 pages2020 Engagement Survey Results AnalysisKaruna GeddamNo ratings yet

- Iqvia Industry ReportDocument32 pagesIqvia Industry ReportAtharva ThiteNo ratings yet

- SPL Report - 2022Document34 pagesSPL Report - 2022Siew Ming SooNo ratings yet

- DQ ScorecardDocument6 pagesDQ ScorecardChaitu BachuNo ratings yet

- 2021 Sales Kick Off Conference Template - RetailDocument22 pages2021 Sales Kick Off Conference Template - Retailjenni.ebhodagheNo ratings yet

- Latin American country hotel investment trends 2016-2019Document5 pagesLatin American country hotel investment trends 2016-2019Carlos MoránNo ratings yet

- Bharti Airtel DCFDocument27 pagesBharti Airtel DCFHemant bhanawatNo ratings yet

- Session 5 SlidesDocument24 pagesSession 5 SlidesloujaynNo ratings yet

- Could E-Commerce Disintermediate Supermarkets?: Winning Strategies For CPG CompaniesDocument41 pagesCould E-Commerce Disintermediate Supermarkets?: Winning Strategies For CPG CompanieskrrajanNo ratings yet

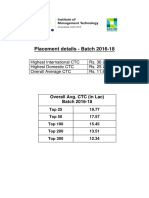

- Placement Report 2016 18 BatchDocument5 pagesPlacement Report 2016 18 BatchKollol DebNo ratings yet

- CAS Investment Partners April 2022 Letter To InvestorsDocument25 pagesCAS Investment Partners April 2022 Letter To InvestorsZerohedgeNo ratings yet

- Statistics For Management and Economics, 9th Edition Keller ISM PDFDocument869 pagesStatistics For Management and Economics, 9th Edition Keller ISM PDFHumaira70% (10)

- H123 Report Card AnalysisSub-Title Key Operating Metrics and Financial RatiosDocument30 pagesH123 Report Card AnalysisSub-Title Key Operating Metrics and Financial RatiosNikhilKapoor29No ratings yet

- IIM Kozhikode: Globalizing Indian ThoughtDocument8 pagesIIM Kozhikode: Globalizing Indian ThoughtRaunak GuptaNo ratings yet

- MBA ASDM Assignment Data Analysis & Decision MakingDocument7 pagesMBA ASDM Assignment Data Analysis & Decision Makinghusain albaqaliNo ratings yet

- Study - Id59062 - Cosmetics Industry in IndiaDocument71 pagesStudy - Id59062 - Cosmetics Industry in IndiaHarshit GuptaNo ratings yet

- Business Survey ReportDocument27 pagesBusiness Survey ReportKuri KetemaNo ratings yet

- Supply Chain Management Course OutlineDocument10 pagesSupply Chain Management Course OutlineAbhijit PaikarayNo ratings yet

- Caso 1Document28 pagesCaso 1Daniel CalderónNo ratings yet

- WING Investor Presentation IR Website 2018 WingstopDocument37 pagesWING Investor Presentation IR Website 2018 WingstopAla BasterNo ratings yet

- Global Mid-Year Forecast: JUNE 2021Document20 pagesGlobal Mid-Year Forecast: JUNE 2021Daiany Costa100% (1)

- 2022 Uace Statement of Release of ResultsDocument10 pages2022 Uace Statement of Release of ResultsOjiki StephenNo ratings yet

- Bonds The Loyalty Report 2023 Executive SummaryDocument17 pagesBonds The Loyalty Report 2023 Executive SummarydencisoNo ratings yet

- Monthly Financial Statements Summary Excel TemplateDocument8 pagesMonthly Financial Statements Summary Excel TemplateBalakrishna GopinathNo ratings yet

- ORM-2 Assignment 1Document2 pagesORM-2 Assignment 1Komal ModiNo ratings yet

- Calculating Payback Period, IRR, and NPV for Equipment Purchase DecisionsDocument4 pagesCalculating Payback Period, IRR, and NPV for Equipment Purchase DecisionsSamintangNo ratings yet

- Cost & Management Accounting - MGT402 Quiz 1Document63 pagesCost & Management Accounting - MGT402 Quiz 1Ayesha NaureenNo ratings yet

- ZICA T6 - ManagementDocument91 pagesZICA T6 - ManagementMongu Rice100% (7)

- Enron Case Study 09-12-2013Document32 pagesEnron Case Study 09-12-2013Giridharan Arsenal100% (2)

- FM 2Document14 pagesFM 2Castor DamasoNo ratings yet

- CIR Disallows Depreciation Beyond Acquisition CostDocument3 pagesCIR Disallows Depreciation Beyond Acquisition Costluigi vidaNo ratings yet

- Chapter 18 - Financial Management Learning GoalsDocument25 pagesChapter 18 - Financial Management Learning GoalsRille LuNo ratings yet

- Uy Tong vs. CA prohibits automatic property appropriationDocument2 pagesUy Tong vs. CA prohibits automatic property appropriationFai Meile100% (1)

- FIE433 - International Equity FinancingDocument20 pagesFIE433 - International Equity FinancingAsyrafi ArifinNo ratings yet

- DMI Finance - R-26032019Document8 pagesDMI Finance - R-26032019Varun PathakNo ratings yet

- WhatsApp Chat With SPACE MUSICDocument114 pagesWhatsApp Chat With SPACE MUSIC10k subscribers without any Videos ChallengeNo ratings yet

- Guide to Internal Control SystemsDocument8 pagesGuide to Internal Control Systemssarvjeet_kaushal0% (1)

- Partnership in Business LawDocument5 pagesPartnership in Business LawJimmy LevisNo ratings yet

- JS20 SBR Me2 - QDocument9 pagesJS20 SBR Me2 - QNik Hanisah Zuraidi AfandiNo ratings yet

- Opposition To QLS Motion For Summary JudgementDocument9 pagesOpposition To QLS Motion For Summary JudgementLee PerryNo ratings yet

- Himanshu Lohia: Curriculum VitaeDocument4 pagesHimanshu Lohia: Curriculum Vitaehimanshulohia85No ratings yet

- AgribusinessDocument234 pagesAgribusinessPurna DhanukNo ratings yet

- Types of PPP PPP Advantages and Disadvantages Criteria To Evaluate Projects For PPPDocument31 pagesTypes of PPP PPP Advantages and Disadvantages Criteria To Evaluate Projects For PPPswatiNo ratings yet

- TPIPL Final ReportDocument48 pagesTPIPL Final ReportNgoc Nguyen HongNo ratings yet

- Lloyds Steel Industries LTDDocument20 pagesLloyds Steel Industries LTDRohit JohnNo ratings yet

- Duration Gap Analysis Session 6Document33 pagesDuration Gap Analysis Session 6Tharindu PereraNo ratings yet

- Finance Formula SheetDocument4 pagesFinance Formula Sheetdjlyfe100% (1)

- Acct 101 FinalDocument9 pagesAcct 101 FinalAndrea NingNo ratings yet

- Basis of ChargeDocument21 pagesBasis of Chargemonirba48No ratings yet

- Background DraftDocument3 pagesBackground DraftKatrina Faith Salonga BeoNo ratings yet

- CHECK - P2 Quiz 1 GradedDocument3 pagesCHECK - P2 Quiz 1 GradedARNEL CALUBAGNo ratings yet

- Solar PV Financial Modeling Impacts v1.2Document16 pagesSolar PV Financial Modeling Impacts v1.2Andre S100% (1)

- Sample Sale DeedDocument8 pagesSample Sale Deedpradip_kumar100% (1)

- General Summary Tender: Lampiran EDocument42 pagesGeneral Summary Tender: Lampiran EIntan Farhana Mohd RoslanNo ratings yet

- Clarity Inquiry #9ehb78p6wbDocument17 pagesClarity Inquiry #9ehb78p6wbPatricia CarvajalNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- Streetsmart Financial Basics for Nonprofit Managers: 4th EditionFrom EverandStreetsmart Financial Basics for Nonprofit Managers: 4th EditionRating: 3.5 out of 5 stars3.5/5 (3)

- Other People's Money: The Real Business of FinanceFrom EverandOther People's Money: The Real Business of FinanceRating: 4 out of 5 stars4/5 (34)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- The Leadership Capital Index: Realizing the Market Value of LeadershipFrom EverandThe Leadership Capital Index: Realizing the Market Value of LeadershipRating: 5 out of 5 stars5/5 (2)

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet