You might also like

- CH04 ProblemDocument2 pagesCH04 ProblemTuyền Võ ThanhNo ratings yet

- Keys in Manacc Seatwork - BUDGETINGDocument2 pagesKeys in Manacc Seatwork - BUDGETINGRoselie Barbin50% (2)

- Full Report Case 4Document13 pagesFull Report Case 4Ina Noina100% (4)

- Assignment #1 OH Variance With SolutionDocument14 pagesAssignment #1 OH Variance With SolutionJeannet LagcoNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- ACCT1003 - Worksheet - 8 - Summer 2016Document5 pagesACCT1003 - Worksheet - 8 - Summer 2016sandrae brownNo ratings yet

- c5 Solutions BudgetingDocument13 pagesc5 Solutions BudgetingChinnam Lalitha100% (1)

- Quarantine Company, A Manufacturer of Small Tools, Provided The Following Information For The Year Ended December 31, 2019Document9 pagesQuarantine Company, A Manufacturer of Small Tools, Provided The Following Information For The Year Ended December 31, 2019Ann louNo ratings yet

- Cash Budget . Feb 2020: Q 1 Calgon ProductsDocument11 pagesCash Budget . Feb 2020: Q 1 Calgon Products신두No ratings yet

- Activity Based Costing and Activity Based Management - ProblemDocument3 pagesActivity Based Costing and Activity Based Management - Problemkiara kiesh FosterNo ratings yet

- Cost Sheet Project ReportDocument50 pagesCost Sheet Project ReportAnkit Raj50% (10)

- Budget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Document7 pagesBudget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Suraj KumarNo ratings yet

- Cash BudgetingDocument5 pagesCash BudgetingAnissa GeddesNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Cash Budget Problems and SolutionsDocument6 pagesCash Budget Problems and Solutionstamberahul1256No ratings yet

- Cash Management QuestionsDocument5 pagesCash Management QuestionsManasi Jamsandekar100% (1)

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Questions On Cash Budget-2Document7 pagesQuestions On Cash Budget-2Mpolokeng HlabanaNo ratings yet

- Cash Management: ProblemsDocument4 pagesCash Management: ProblemsPoojitha ReddyNo ratings yet

- Exercises Budgeting ACCT2105 3s2010Document7 pagesExercises Budgeting ACCT2105 3s2010Hanh Bui0% (1)

- Cash Budget Sums Mcom Sem 4Document14 pagesCash Budget Sums Mcom Sem 4Prachi BhosaleNo ratings yet

- M5 Management of Cash Pract. ProbDocument5 pagesM5 Management of Cash Pract. ProbAmruta PeriNo ratings yet

- Cash ManagementDocument16 pagesCash ManagementdhruvNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Cash BudgetDocument4 pagesCash BudgetSANDEEP SINGH0% (1)

- Cash BudgetDocument2 pagesCash BudgetAbdulkarim Hamisi KufakunogaNo ratings yet

- Budgeting - 1Document3 pagesBudgeting - 1Muhammad MansoorNo ratings yet

- Cash Management NumericalsDocument5 pagesCash Management NumericalsAnjali Jain100% (1)

- Asignación 4 LSFPDocument6 pagesAsignación 4 LSFPElia SantanaNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Preparation of Cash BudgetDocument3 pagesPreparation of Cash BudgetFaye RoceroNo ratings yet

- Cash Budget Test 3Document2 pagesCash Budget Test 3Prince TshepoNo ratings yet

- Case Analysis (1 30)Document3 pagesCase Analysis (1 30)manishadaaNo ratings yet

- Cash Budget: Aizel Joy A. Tampos 12-ABM A February 5, 2017Document3 pagesCash Budget: Aizel Joy A. Tampos 12-ABM A February 5, 2017AJNo ratings yet

- VM Salgaocar Institute of International Hospitality EducationDocument1 pageVM Salgaocar Institute of International Hospitality Educationbimbee 13No ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Cash Budget (Problem-1)Document1 pageCash Budget (Problem-1)Hakimzada Sharafat Ali HakimNo ratings yet

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

- 17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8Document6 pages17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8putu cherline21No ratings yet

- Lecture 11Document26 pagesLecture 11Riaz Baloch Notezai100% (1)

- Budgeting - Planning: A325 Discussion - March 19, 2012Document8 pagesBudgeting - Planning: A325 Discussion - March 19, 2012alfaNo ratings yet

- Budgeting NumericalsDocument6 pagesBudgeting NumericalsAll in ONENo ratings yet

- Additional Information:: From The Following Information Prepare A Cash Budget For The Months of June and JulyDocument2 pagesAdditional Information:: From The Following Information Prepare A Cash Budget For The Months of June and JulyNsscollege RajakumariNo ratings yet

- Managerial Budget Master ProjectDocument2 pagesManagerial Budget Master Projectapi-340156713No ratings yet

- UNO MA2Test1-ProblemDocument1 pageUNO MA2Test1-ProblemJulliena BakersNo ratings yet

- FALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERDocument7 pagesFALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERAkankshaNo ratings yet

- Budgeting Pretest Teachers PDFDocument4 pagesBudgeting Pretest Teachers PDFKatzkie Montemayor GodinezNo ratings yet

- Two The 20%. The: Vinze and of As TinDocument4 pagesTwo The 20%. The: Vinze and of As TinPRAYAGRAJ MITRA MANDAL GROUPNo ratings yet

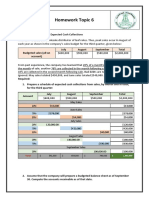

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Module 8 - In-Class Exercises - Budgeting-1Document2 pagesModule 8 - In-Class Exercises - Budgeting-1lengocanhkhNo ratings yet

- Foundations of Financial Management: Spreadsheet TemplatesDocument9 pagesFoundations of Financial Management: Spreadsheet Templatesalaa_h1100% (1)

- Example Question Financial ManagementDocument3 pagesExample Question Financial ManagementNadhirah NadriNo ratings yet

- Chapter Two Master Budget and Responsibility Accounting What Is Budget?Document12 pagesChapter Two Master Budget and Responsibility Accounting What Is Budget?kirosNo ratings yet

- Budgeting Tute 01Document2 pagesBudgeting Tute 01Maithri Vidana KariyakaranageNo ratings yet

- FMDocument10 pagesFMKei YeeNo ratings yet

- Copy - of - Tamplate - Proposal - AnggaranDocument10 pagesCopy - of - Tamplate - Proposal - AnggaranjosgarudaeagleNo ratings yet

- Example Cash BudgetDocument1 pageExample Cash BudgetPamela GalangNo ratings yet

- BudgetingDocument51 pagesBudgetingVignesh KivickyNo ratings yet

- Months Sales Material Wages Overheads: Estimated Sale and CostDocument1 pageMonths Sales Material Wages Overheads: Estimated Sale and CostGarimaNo ratings yet

- Modul Akuntansi Manajemen II 2019-2020-Converted-Converted - 209630662Document30 pagesModul Akuntansi Manajemen II 2019-2020-Converted-Converted - 209630662hendy DidoNo ratings yet

- LB53 Case MA Graviela Charleen 2502001574Document4 pagesLB53 Case MA Graviela Charleen 2502001574Natasha HerlianaNo ratings yet

- Chapter 8 Case QuestionsDocument2 pagesChapter 8 Case QuestionsMcCoy BroughNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- IGCSE-- EXTENDED TUTORING 2023-2024 -- LEDGERS --Document12 pagesIGCSE-- EXTENDED TUTORING 2023-2024 -- LEDGERS --MUSTHARI KHANNo ratings yet

- Lcci - Higher - 2022 - QPDocument20 pagesLcci - Higher - 2022 - QPMUSTHARI KHANNo ratings yet

- Retirement of Partner - A LevellDocument3 pagesRetirement of Partner - A LevellMUSTHARI KHANNo ratings yet

- Standard Costing - A LevelDocument3 pagesStandard Costing - A LevelMUSTHARI KHANNo ratings yet

- Abc 1Document2 pagesAbc 1MUSTHARI KHANNo ratings yet

- Activity Based Costing - A Level - No MSDocument3 pagesActivity Based Costing - A Level - No MSMUSTHARI KHANNo ratings yet

- Management Accounting Model Answers Series 3 2012Document14 pagesManagement Accounting Model Answers Series 3 2012MUSTHARI KHANNo ratings yet

- Extra Questions - A LevelDocument8 pagesExtra Questions - A LevelMUSTHARI KHANNo ratings yet

- A2 Accounting - Topicwise Past Paper QuestionsDocument5 pagesA2 Accounting - Topicwise Past Paper QuestionsMUSTHARI KHANNo ratings yet

- Multiple Choice QuestionsDocument9 pagesMultiple Choice Questionskhankhan1No ratings yet

- Chapter 2 Sol 40-43Document6 pagesChapter 2 Sol 40-43Something ChicNo ratings yet

- Cost Accounting Mastery - 1Document4 pagesCost Accounting Mastery - 1Mark RevarezNo ratings yet

- CHAPTER 13 Intermediate Acctng 1Document66 pagesCHAPTER 13 Intermediate Acctng 1Tessang OnongenNo ratings yet

- CLASSIFICATION OF COSTS: Manufacturing: Subhash Sahu (Cs Executive Student of Jaipur Chapter)Document85 pagesCLASSIFICATION OF COSTS: Manufacturing: Subhash Sahu (Cs Executive Student of Jaipur Chapter)shubhamNo ratings yet

- GP AnalysisDocument25 pagesGP Analysismiles1280No ratings yet

- Chapter 2Document54 pagesChapter 2Léo AudibertNo ratings yet

- A Study On Working Capital Management in Strides Shasun Limited at CuddaloreDocument75 pagesA Study On Working Capital Management in Strides Shasun Limited at Cuddaloreashok kumar100% (3)

- BudgetingDocument37 pagesBudgetingMompoloki MontiNo ratings yet

- Cost AccountingDocument8 pagesCost Accountingtushar sundriyalNo ratings yet

- CSIR Research Grant 123Document46 pagesCSIR Research Grant 123Irshaan SyedNo ratings yet

- ST Mary UniversityDocument4 pagesST Mary UniversityRobbob JahloveNo ratings yet

- روعه Fidic Red Book 1999 Clauses Risks - CORBETT&CODocument414 pagesروعه Fidic Red Book 1999 Clauses Risks - CORBETT&COMØhãmmed ØwięsNo ratings yet

- Ref PPT For Rate AnalysisDocument22 pagesRef PPT For Rate AnalysisParth Shah75% (4)

- Allama Iqbal Open University, Islamabad: (Department of Commerce)Document5 pagesAllama Iqbal Open University, Islamabad: (Department of Commerce)ilyas muhammadNo ratings yet

- Biodegradable Plastic Bag Manufacturing Industry-800655 PDFDocument68 pagesBiodegradable Plastic Bag Manufacturing Industry-800655 PDFAryanNo ratings yet

- 5 Process CostingDocument23 pages5 Process CostingBəhmən OrucovNo ratings yet

- Quantity Survey EstimatesDocument24 pagesQuantity Survey EstimatesShahid KhanNo ratings yet

- Sales Variance & Operating StatementDocument12 pagesSales Variance & Operating StatementEjaz AhmadNo ratings yet

- Rakib 1stDocument3 pagesRakib 1stMD Hafizul Islam HafizNo ratings yet

- Responsibility Accounting: Chapter Study ObjectivesDocument7 pagesResponsibility Accounting: Chapter Study ObjectivesLive LoveNo ratings yet

- Standard Costing and Variance AnalysisDocument19 pagesStandard Costing and Variance Analysisbarakkat72No ratings yet

- Tutorial 1 Cost ClassificationDocument5 pagesTutorial 1 Cost ClassificationSyafiqNo ratings yet

- Classification of CostsDocument10 pagesClassification of CostsChristine Marie RamirezNo ratings yet

- Exercise 6-1 (Classification of Cost Drivers)Document18 pagesExercise 6-1 (Classification of Cost Drivers)Barrylou ManayanNo ratings yet

- Model Project Profile On Plastic Bottle (Pcbi)Document2 pagesModel Project Profile On Plastic Bottle (Pcbi)sivanagendrarao beharabhargavaNo ratings yet