You might also like

- Consignment Account PDFDocument13 pagesConsignment Account PDFAyush KumarNo ratings yet

- ACC Topic 5.1 Statement of Comprehensive Income Financial Position (Notes)Document16 pagesACC Topic 5.1 Statement of Comprehensive Income Financial Position (Notes)Romzy RahmatNo ratings yet

- Consignment Account NotesDocument12 pagesConsignment Account NotesPonnan AdiyenNo ratings yet

- Advanced Financial AccountingDocument102 pagesAdvanced Financial AccountingYash WanthNo ratings yet

- Receivable Financing - NotesDocument3 pagesReceivable Financing - NotesTEOPE, EMERLIZA DE CASTRONo ratings yet

- PDAFDocument2 pagesPDAFMaeNo ratings yet

- Balance Sheet NotesDocument4 pagesBalance Sheet NotesAudrey RolandNo ratings yet

- Cost Accounting CycleDocument8 pagesCost Accounting CycleRosiel Mae CadungogNo ratings yet

- CorpLiq Draft (Recovered)Document9 pagesCorpLiq Draft (Recovered)Via Samantha de AustriaNo ratings yet

- ABM Fundamentals of ABM 1 Module 12 Accounting Cycle of A Merchandising BusinessDocument16 pagesABM Fundamentals of ABM 1 Module 12 Accounting Cycle of A Merchandising BusinessMariel Santos67% (3)

- Financial Accounting 2Document89 pagesFinancial Accounting 2Colince johnson0% (1)

- Total Cash Receipt From Issuance of BondsDocument11 pagesTotal Cash Receipt From Issuance of Bondskrisha milloNo ratings yet

- EC 1 - Acctg Cycle Part 2 ConceptsDocument3 pagesEC 1 - Acctg Cycle Part 2 ConceptsChelay EscarezNo ratings yet

- Receivable Financing: Pledge, Assignment, and FactoringDocument30 pagesReceivable Financing: Pledge, Assignment, and FactoringJoy UyNo ratings yet

- 3 Consignment AccountsDocument12 pages3 Consignment Accountsking brothersNo ratings yet

- HO - Consignment Arrangements StudentsDocument2 pagesHO - Consignment Arrangements Studentspatburner1108No ratings yet

- Fabm1 Module 12Document13 pagesFabm1 Module 12Mika GerminoNo ratings yet

- Control ACCOUNTDocument2 pagesControl ACCOUNTMujahid AmanNo ratings yet

- Receivable FinancingDocument34 pagesReceivable FinancingmaryzeenNo ratings yet

- Business Finance: Session 3: Financial StatementsDocument45 pagesBusiness Finance: Session 3: Financial StatementsXia AlliaNo ratings yet

- Quarterly Statement of Cash FlowDocument3 pagesQuarterly Statement of Cash FlowDILG San FabianNo ratings yet

- BFW1001 Foundations of Finance: Valuation FundamentalsDocument11 pagesBFW1001 Foundations of Finance: Valuation FundamentalsLeo TranNo ratings yet

- 2k15-Fin. Reporting Analysis-3Document30 pages2k15-Fin. Reporting Analysis-3flamerydersNo ratings yet

- Accounts ReceivableDocument8 pagesAccounts ReceivableFireworks PHNo ratings yet

- Cash Flow Statement: 1 Cash Flows From Operating ActivitiesDocument5 pagesCash Flow Statement: 1 Cash Flows From Operating ActivitiesPRABAL BHATNo ratings yet

- FDP Form 9 - Statement of Cash FlowsDocument1 pageFDP Form 9 - Statement of Cash FlowsNoel Jr BuenafeNo ratings yet

- CHAPTER 1 - JOINT VENTURE CidosDocument10 pagesCHAPTER 1 - JOINT VENTURE CidosNoriani Binti SambriNo ratings yet

- Financial Accounting and Reporting - Trade and Other Receivables (Recognition, Measurement, Estimation and Valuation)Document6 pagesFinancial Accounting and Reporting - Trade and Other Receivables (Recognition, Measurement, Estimation and Valuation)LuisitoNo ratings yet

- Corporation - Retained Earnings and DividendsDocument4 pagesCorporation - Retained Earnings and DividendsJay Mayca TyNo ratings yet

- Explanations On StatementsDocument3 pagesExplanations On StatementsSimphiwe NandoNo ratings yet

- Discounting of NRDocument9 pagesDiscounting of NRArt EezyNo ratings yet

- Preparation of Financial Statements-Sole TradersDocument5 pagesPreparation of Financial Statements-Sole TradersHeavens Mupedzisa100% (1)

- Financial Statements New Format 1Document9 pagesFinancial Statements New Format 1alyanna paladaNo ratings yet

- Working Capital Statement Proforma PDFDocument2 pagesWorking Capital Statement Proforma PDFSheldon FcbNo ratings yet

- Chapter 3 Accrued Liabilities and Deferred Revenue - ContinuationDocument29 pagesChapter 3 Accrued Liabilities and Deferred Revenue - ContinuationJouhara San JuanNo ratings yet

- Business FinanceDocument6 pagesBusiness FinanceHassan AbdullahNo ratings yet

- Preparation of Financial Statements-PartnershipsDocument7 pagesPreparation of Financial Statements-PartnershipsHeavens MupedzisaNo ratings yet

- CH 06 Unit 03Document31 pagesCH 06 Unit 03ASIFNo ratings yet

- Receivable Financing CH14 by LailaneDocument30 pagesReceivable Financing CH14 by LailaneEunice BernalNo ratings yet

- 2 Cash Flows and Cash BudgetDocument17 pages2 Cash Flows and Cash Budgetangelika dijamcoNo ratings yet

- Diya 1Document4 pagesDiya 1Vipul I PanchasarNo ratings yet

- ConsignmentDocument5 pagesConsignmentMANKARAN SINGH BHATIA 21-22No ratings yet

- Accounting For Project by AA59Document2 pagesAccounting For Project by AA59Alzahraa TradingNo ratings yet

- CH05 - Corp Liquidation & ReorganizationDocument26 pagesCH05 - Corp Liquidation & ReorganizationTrixie Pearl TompongNo ratings yet

- Receivable Financing Pledge Assignment ADocument34 pagesReceivable Financing Pledge Assignment AJoy UyNo ratings yet

- Proforma Journal Entries - Merchandising TransactionsDocument4 pagesProforma Journal Entries - Merchandising TransactionsJames Christian AvesNo ratings yet

- Control AccountDocument3 pagesControl AccountKady AnnNo ratings yet

- Chapter 24 - Teachers Manual - Aa Part 2 PDFDocument13 pagesChapter 24 - Teachers Manual - Aa Part 2 PDFSheed ChiuNo ratings yet

- 2 Closing Process For Services Businessp2Document16 pages2 Closing Process For Services Businessp2smofias12006No ratings yet

- Additional Notes-Statement of Cash FlowDocument13 pagesAdditional Notes-Statement of Cash FlowdaminbalqisNo ratings yet

- QSCF 6Document2 pagesQSCF 6ricohizon99No ratings yet

- Insurance Claim AccountDocument26 pagesInsurance Claim AccountAdiNo ratings yet

- Receivable FinancingDocument6 pagesReceivable FinancingErla PilapilNo ratings yet

- Operating Cycle of Merchandising BusinessDocument4 pagesOperating Cycle of Merchandising BusinessTrina Joy Homerez100% (1)

- Partnership LiquidationDocument4 pagesPartnership LiquidationMelanie RuizNo ratings yet

- Accounting For Inventory, Control Accounts and A Bank ReconciliationDocument13 pagesAccounting For Inventory, Control Accounts and A Bank ReconciliationMonicah NyamburaNo ratings yet

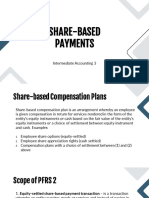

- Share Based PaymentsDocument36 pagesShare Based PaymentsChristine Dawn LascoNo ratings yet

- Accounts For Clubs and SocietiesDocument4 pagesAccounts For Clubs and SocietiesSimba Muhonde100% (2)

- Drawing Financial Statements and ProjectionsDocument36 pagesDrawing Financial Statements and ProjectionsAaron MushunjeNo ratings yet

- Credit Derivatives Pricing Models: Models, Pricing and ImplementationFrom EverandCredit Derivatives Pricing Models: Models, Pricing and ImplementationRating: 2 out of 5 stars2/5 (1)

- Investment Manager Private Equity in New York NY Resume Anthony BuffaDocument2 pagesInvestment Manager Private Equity in New York NY Resume Anthony BuffaAnthonyBuffaNo ratings yet

- P1 - ReviewDocument14 pagesP1 - ReviewEvitaAyneMaliñanaTapit0% (2)

- 2 PMT PV NPV ImptDocument20 pages2 PMT PV NPV ImptBoby MondalNo ratings yet

- Sama Credit & Leasing SDN BHD v. Pegawai Pemegang Harta: S. 49 (1) andDocument3 pagesSama Credit & Leasing SDN BHD v. Pegawai Pemegang Harta: S. 49 (1) andShereenNo ratings yet

- United India Insurance - Wikipedia, The Free EncyclopediaDocument5 pagesUnited India Insurance - Wikipedia, The Free EncyclopediaSaurav Sundarka0% (1)

- Financial and Managerial Accounting The Basis For Business Decisions 18th Edition Williams Test Bank PDFDocument81 pagesFinancial and Managerial Accounting The Basis For Business Decisions 18th Edition Williams Test Bank PDFa257194639No ratings yet

- Auditing and AttestationDocument45 pagesAuditing and Attestationmira01No ratings yet

- Bangladesh Bank Cottage Industry GuidelineDocument1 pageBangladesh Bank Cottage Industry GuidelineTanayNo ratings yet

- Sweat EquityDocument17 pagesSweat EquitygeddadaarunNo ratings yet

- Registration of Mortgages, Charges, Etc.: Mortgage or Charge Means An Interest or Lien Created On The Property or AssetsDocument15 pagesRegistration of Mortgages, Charges, Etc.: Mortgage or Charge Means An Interest or Lien Created On The Property or AssetsAsad AliNo ratings yet

- EDHEC Valuation Manual PDFDocument40 pagesEDHEC Valuation Manual PDFradhika1992No ratings yet

- Bonds & Their Valuation: Charak RAYDocument43 pagesBonds & Their Valuation: Charak RAYCHARAK RAYNo ratings yet

- 5 6156785960404123873 PDFDocument1 page5 6156785960404123873 PDFellaNo ratings yet

- PRTC - Final Preboard - Taxation - 2017Document5 pagesPRTC - Final Preboard - Taxation - 2017Kenneth Bryan Tegerero Tegio50% (2)

- Tracking Error in Index FundDocument2 pagesTracking Error in Index FundSaprem KulkarniNo ratings yet

- Yes Bank CrisisDocument10 pagesYes Bank CrisisAyaan khan100% (1)

- L (.Il Julylg,: or For The in To ofDocument7 pagesL (.Il Julylg,: or For The in To ofCliff DaquioagNo ratings yet

- FAR.2920 - Generating Cash From Receivables.Document4 pagesFAR.2920 - Generating Cash From Receivables.Eyes Saw100% (1)

- 30 Esl Topics Word Bank WorkingDocument2 pages30 Esl Topics Word Bank WorkingMaka AbdushelishviliNo ratings yet

- Case Digest - Credit Transaction No. 9 13Document5 pagesCase Digest - Credit Transaction No. 9 13anon_746511540No ratings yet

- Gina L Eggleton 22965 NE Albertson RD Gaston, OR 97119: Company: Check No. Group: Loc. Dept: Check Date: HoursDocument4 pagesGina L Eggleton 22965 NE Albertson RD Gaston, OR 97119: Company: Check No. Group: Loc. Dept: Check Date: HoursGigi EggletonNo ratings yet

- Zydus Wellness Standalone Yearly Results Vanaspati & Oils Standalone Yearly Results of Zydus Wellness - BSE 531335, NSE ZYDUSWELLDocument2 pagesZydus Wellness Standalone Yearly Results Vanaspati & Oils Standalone Yearly Results of Zydus Wellness - BSE 531335, NSE ZYDUSWELLRozy SinghNo ratings yet

- Maximum Mark: 90: Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesMaximum Mark: 90: Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelShivamNo ratings yet

- BC - 402 - AuditingDocument2 pagesBC - 402 - AuditingQadir RafiqueNo ratings yet

- Final BLT203 SemIV Bcom Spring 2020Document4 pagesFinal BLT203 SemIV Bcom Spring 2020SunnyNo ratings yet

- General Banking Act PDFDocument69 pagesGeneral Banking Act PDFJerwin TiamsonNo ratings yet

- Cash Flow AsdprinciplesDocument16 pagesCash Flow AsdprinciplesAzrul KechikNo ratings yet

- Business Applications FOR BASE, RATE, PERCENTAGEDocument36 pagesBusiness Applications FOR BASE, RATE, PERCENTAGEVevianJavierCervantesNo ratings yet

- Agor Oil IndustryDocument17 pagesAgor Oil IndustryNirankar SinghNo ratings yet

- B127-Aragon-A No 4Document6 pagesB127-Aragon-A No 4Shaina AragonNo ratings yet