You might also like

- The Production Process: The Behavior of Profit-Maximizing FirmsDocument24 pagesThe Production Process: The Behavior of Profit-Maximizing Firmsshan732No ratings yet

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Intro Econ Chap 4 KANENUSDocument42 pagesIntro Econ Chap 4 KANENUSReshid JewarNo ratings yet

- ME Session 8Document29 pagesME Session 8vaibhav khandelwalNo ratings yet

- Production ProcessDocument26 pagesProduction Process宓語嫣No ratings yet

- Producer_Theory (1)Document62 pagesProducer_Theory (1)Vriddhi ParekhNo ratings yet

- Theory of Firm-ProductionDocument18 pagesTheory of Firm-ProductionHARSHALI KATKARNo ratings yet

- CH 13 The Costs of ProductionDocument33 pagesCH 13 The Costs of ProductionSakibNo ratings yet

- Managerial Economics: PGDM-HR: 2019 - 21 Term 1 (July - September, 2019)Document27 pagesManagerial Economics: PGDM-HR: 2019 - 21 Term 1 (July - September, 2019)Daksh AnejaNo ratings yet

- Cost and Revenue Analysis Chapter 2 Unit 4Document51 pagesCost and Revenue Analysis Chapter 2 Unit 4desiredmalehereNo ratings yet

- Chapter 4 Theory of FirmDocument11 pagesChapter 4 Theory of Firmchuojx-jb23No ratings yet

- Managerial Economics Key ConceptsDocument33 pagesManagerial Economics Key Conceptschandel08No ratings yet

- Unit 7 - Cost and ProductionDocument25 pagesUnit 7 - Cost and ProductionRax-Nguajandja KapuireNo ratings yet

- Section 6 - BMIK 2023 - FinalDocument43 pagesSection 6 - BMIK 2023 - Final10622006No ratings yet

- Chapter 6 Production: Read Pindyck and Rubinfeld (2013), Chapter 6Document39 pagesChapter 6 Production: Read Pindyck and Rubinfeld (2013), Chapter 6Shay TNo ratings yet

- Snob Effect: - Negative Network Externality in Which A Consumer Wishes To Own An Exclusive or Unique GoodDocument24 pagesSnob Effect: - Negative Network Externality in Which A Consumer Wishes To Own An Exclusive or Unique GoodSanyam JainNo ratings yet

- 1.1 Theoretical Foundation of SUT and I-ODocument31 pages1.1 Theoretical Foundation of SUT and I-OHaidee Fay IgnacioNo ratings yet

- Topic 6 - Costs of ProductionDocument28 pagesTopic 6 - Costs of ProductionJonathan NicoNo ratings yet

- Costs of Production. PptDocument42 pagesCosts of Production. PptSc RayaNo ratings yet

- Production and Cost in Short RunDocument22 pagesProduction and Cost in Short RunFaraz SiddiquiNo ratings yet

- Chapter 6 - Production Key Concepts and Topics: Input Prices and Level of OutputDocument14 pagesChapter 6 - Production Key Concepts and Topics: Input Prices and Level of OutputKevni MikhailNo ratings yet

- Unit II - Part II - Costs of ProductionDocument40 pagesUnit II - Part II - Costs of ProductionSam Ebenezer .SNo ratings yet

- MICROECONOMICS ch06Document70 pagesMICROECONOMICS ch06Alena Francine EballoNo ratings yet

- Basic Production and Cost TheoryDocument52 pagesBasic Production and Cost TheoryPrincess Tamayo AlicawayNo ratings yet

- Production and Costs 2023Document62 pagesProduction and Costs 2023precious04ditauNo ratings yet

- Theory of Firm and Firms in Competitive Market-1Document45 pagesTheory of Firm and Firms in Competitive Market-1Lance Gabriel AsuncionNo ratings yet

- Lec-7 (Theory of Production)Document42 pagesLec-7 (Theory of Production)Wasiq BhuiyanNo ratings yet

- Colander ch09 Production&CostsIDocument71 pagesColander ch09 Production&CostsIJenil BetitoNo ratings yet

- CH 6 Production and CostDocument26 pagesCH 6 Production and Costshaheduzaman ShahedNo ratings yet

- Decision Time Frames and CostsDocument68 pagesDecision Time Frames and CostsMadeeha ZuberiNo ratings yet

- CH 7-The Production Process: The Behaviour of Profit-Maximizing FirmsDocument33 pagesCH 7-The Production Process: The Behaviour of Profit-Maximizing FirmsgülraNo ratings yet

- ProductionDocument37 pagesProductionDavidNo ratings yet

- Producer Choice and Firm Production DecisionsDocument26 pagesProducer Choice and Firm Production DecisionsHari PrasathNo ratings yet

- Theory of Cost of Production6Document91 pagesTheory of Cost of Production6Bhathika GimhanNo ratings yet

- Chapter 3 - Production, costs, and organization of firmDocument89 pagesChapter 3 - Production, costs, and organization of firmHieu HoangNo ratings yet

- Production and Cost AnalysisDocument60 pagesProduction and Cost AnalysisKhushwant AryaNo ratings yet

- Cost of ProductionDocument27 pagesCost of Productionfaisal197No ratings yet

- The Demand For Labor: Mcgraw-Hill/IrwinDocument58 pagesThe Demand For Labor: Mcgraw-Hill/IrwinGunjan PruthiNo ratings yet

- Producer's BehaviourDocument46 pagesProducer's BehaviourSanjoli JainNo ratings yet

- Costs of Production: Short and Long Run Cost Curves ExplainedDocument24 pagesCosts of Production: Short and Long Run Cost Curves Explainedakshat guptaNo ratings yet

- Cost Analysis and Cost ManagementDocument75 pagesCost Analysis and Cost ManagementMinh Hạnhx CandyNo ratings yet

- Labour Market Government Intervention A2Document27 pagesLabour Market Government Intervention A2housnabaakil25No ratings yet

- Chapter Four: Theory of Production and CostDocument33 pagesChapter Four: Theory of Production and CostfaNo ratings yet

- Cost and Revenue Analysis in ProductionDocument36 pagesCost and Revenue Analysis in ProductionDuma DumaiNo ratings yet

- Cost Volume Profit AnalysisDocument25 pagesCost Volume Profit AnalysisAmit DeyNo ratings yet

- Managerial Economics (MBA 751) @CH 3Document23 pagesManagerial Economics (MBA 751) @CH 3DrGuled MohammedNo ratings yet

- ECO 610: Lecture 3: Production, Economic Costs, and Economic ProfitDocument35 pagesECO 610: Lecture 3: Production, Economic Costs, and Economic ProfitMelat TNo ratings yet

- Cost Analysis: Maximizing ProfitsDocument9 pagesCost Analysis: Maximizing ProfitsAnkit KagraNo ratings yet

- Managerial Economics (Chapter 6)Document39 pagesManagerial Economics (Chapter 6)api-370372490% (10)

- Production: Managerial EconomicsDocument9 pagesProduction: Managerial Economicsakki72000No ratings yet

- 8 Costs Production 2022Document40 pages8 Costs Production 2022Pletea GeorgeNo ratings yet

- Chapter 6 - Part I Costs of ProductionDocument41 pagesChapter 6 - Part I Costs of ProductionHamdiNo ratings yet

- Labor Economy Chap005Document44 pagesLabor Economy Chap005yaseminNo ratings yet

- Chapter 8 - Production and Cost in The Short-RunDocument48 pagesChapter 8 - Production and Cost in The Short-RunEron Rafael NogueraNo ratings yet

- The Costs of Production: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversityDocument28 pagesThe Costs of Production: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversityHabiba AliNo ratings yet

- Week 11 - English Muhammad Rizky RamadhanDocument44 pagesWeek 11 - English Muhammad Rizky RamadhanMuhammad Rizky RamadhanNo ratings yet

- Analysis of Cost and RevenueDocument28 pagesAnalysis of Cost and RevenueSaurav SubediNo ratings yet

- Module 2 PDFDocument61 pagesModule 2 PDFAa AaNo ratings yet

- Production and Cost - Cotd.Document17 pagesProduction and Cost - Cotd.Emon ChowdhuryNo ratings yet

- Education Indian School of Business - : IPL FranchiseDocument1 pageEducation Indian School of Business - : IPL FranchiseAnyone SomeoneNo ratings yet

- CV PDFDocument1 pageCV PDFAnyone SomeoneNo ratings yet

- CV PDFDocument1 pageCV PDFAnyone SomeoneNo ratings yet

- CGPA 3.94, Top 1% GMAT, Consulting ProjectsDocument1 pageCGPA 3.94, Top 1% GMAT, Consulting ProjectsAnyone SomeoneNo ratings yet

- CV PDFDocument1 pageCV PDFAnyone SomeoneNo ratings yet

- Markstrat pointers marketing strategyDocument2 pagesMarkstrat pointers marketing strategyAnyone SomeoneNo ratings yet

- The Importance of Self-Esteem: - A Popular Management IdeaDocument4 pagesThe Importance of Self-Esteem: - A Popular Management IdeaAnyone SomeoneNo ratings yet

- Vodites - Mds and SemanticDocument5 pagesVodites - Mds and SemanticAnyone SomeoneNo ratings yet

- CV PDFDocument1 pageCV PDFAnyone SomeoneNo ratings yet

- Markstrat Pointers 1 Breakeven AnalysisDocument1 pageMarkstrat Pointers 1 Breakeven AnalysisAnyone SomeoneNo ratings yet

- Contact Information and Office HoursDocument4 pagesContact Information and Office HoursAnyone SomeoneNo ratings yet

- Markstrat Pointers 2 Market AnalysisDocument1 pageMarkstrat Pointers 2 Market AnalysisAnyone SomeoneNo ratings yet

- Practice QuestionsDocument4 pagesPractice QuestionsAnyone SomeoneNo ratings yet

- Leading Organizations Through PeopleDocument4 pagesLeading Organizations Through PeopleAnyone SomeoneNo ratings yet

- Management of OrganizationsDocument4 pagesManagement of OrganizationsAnyone SomeoneNo ratings yet

- Q. No. Question Stem Ans Key AnswerDocument1 pageQ. No. Question Stem Ans Key AnswerAnyone SomeoneNo ratings yet

- Apple Products TNCDocument80 pagesApple Products TNCabhijit khaladkarNo ratings yet

- Jeff Immelt, CEO, General ElectricDocument4 pagesJeff Immelt, CEO, General ElectricAnyone SomeoneNo ratings yet

- With The The: A-Lzots / I IB Government of India Niti New DatedDocument2 pagesWith The The: A-Lzots / I IB Government of India Niti New DatedAnyone SomeoneNo ratings yet

- Full Time MBA Class of 2016 Profile Book PDFDocument8 pagesFull Time MBA Class of 2016 Profile Book PDFAnyone SomeoneNo ratings yet

- JD Ba&bie&deDocument20 pagesJD Ba&bie&deAnyone SomeoneNo ratings yet

- AnnualFee PDFDocument1 pageAnnualFee PDFAnyone SomeoneNo ratings yet

- Apple TNC PDFDocument174 pagesApple TNC PDFAnyone SomeoneNo ratings yet

- Apple TNC PDFDocument174 pagesApple TNC PDFAnyone SomeoneNo ratings yet

- Session2 Demand v2Document61 pagesSession2 Demand v2Anyone SomeoneNo ratings yet

- Amex Discounted PDFDocument2 pagesAmex Discounted PDFAnyone SomeoneNo ratings yet

- Gmat Deadlines PDFDocument1 pageGmat Deadlines PDFAnyone SomeoneNo ratings yet

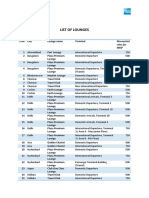

- Ahmedabad: City Terminal Lounge Name Discounted Access (In INR) Complimentary AccessDocument2 pagesAhmedabad: City Terminal Lounge Name Discounted Access (In INR) Complimentary AccessAnyone SomeoneNo ratings yet

- Session1 Practice Problems AkDocument2 pagesSession1 Practice Problems AkAnyone SomeoneNo ratings yet

- Consolidated Financial Statements of Prather Company and SubsidiaryDocument7 pagesConsolidated Financial Statements of Prather Company and SubsidiaryImelda100% (1)

- Congo Whitepaper 9.2019Document12 pagesCongo Whitepaper 9.2019Gostino Lok100% (2)

- JPM Russian Securities - Ordinary Shares (GB - EN) (03!09!2014)Document4 pagesJPM Russian Securities - Ordinary Shares (GB - EN) (03!09!2014)Carl WellsNo ratings yet

- Summary SIA Ch.13 - Expenditure CycleDocument3 pagesSummary SIA Ch.13 - Expenditure CycleAthiyya Nabila AyuNo ratings yet

- BIS Loan Request for $200K Warehouse ExpansionDocument4 pagesBIS Loan Request for $200K Warehouse ExpansionOscar Arana50% (2)

- CV - Experienced Professional with Finance and Sales BackgroundDocument3 pagesCV - Experienced Professional with Finance and Sales BackgroundOvon NormanNo ratings yet

- Governance Letter To CompaniesDocument3 pagesGovernance Letter To CompaniesTBP_Think_TankNo ratings yet

- Job Insecurity and GlobalizationDocument5 pagesJob Insecurity and GlobalizationJayboy SARTORIONo ratings yet

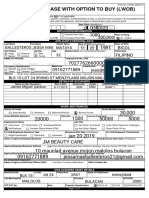

- Lwob - Application-Form Edited Edited EditedDocument2 pagesLwob - Application-Form Edited Edited Editedjessamaeballesteros21100% (1)

- AcreTrader Farmland Investing WhitepaperDocument13 pagesAcreTrader Farmland Investing Whitepaperbasa100% (1)

- Patagonia & Interface IncDocument13 pagesPatagonia & Interface InceshanNo ratings yet

- Global Marketplaces and Business CentersDocument36 pagesGlobal Marketplaces and Business Centersrabea018No ratings yet

- Business Plan HacheryDocument52 pagesBusiness Plan HacherypipestressNo ratings yet

- Case of Electric ToothbrushDocument5 pagesCase of Electric ToothbrushЮрий КориневскийNo ratings yet

- 2018 Coleman Tax Return PDFDocument46 pages2018 Coleman Tax Return PDFJonathan Brinton100% (1)

- Week 2 ProblemsDocument4 pagesWeek 2 Problemsbjh1234517% (6)

- Transfer ConfirmationDocument3 pagesTransfer Confirmationme NaderNo ratings yet

- YLB Yoga Business Plan Guide PDFDocument25 pagesYLB Yoga Business Plan Guide PDFbydiaNo ratings yet

- Blinc 360 and Ajna TechDocument14 pagesBlinc 360 and Ajna TechAlkame IncNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)PV VimalNo ratings yet

- Fiib - Om - Process and Capacity AnalysisDocument9 pagesFiib - Om - Process and Capacity AnalysisCherin SamNo ratings yet

- Jun Freolo Figueroa STDocument3 pagesJun Freolo Figueroa STwarlitopadernaNo ratings yet

- Corporate Finance 10th Edition Ross Test Bank 1Document70 pagesCorporate Finance 10th Edition Ross Test Bank 1james100% (38)

- What Is A Case StudyDocument20 pagesWhat Is A Case StudyPriyanka Ravi100% (2)

- Https:/pipipl In/brochure PDFDocument15 pagesHttps:/pipipl In/brochure PDFCreative IdeasNo ratings yet

- Entrepreneurial Ecosystem in LebanonDocument10 pagesEntrepreneurial Ecosystem in LebanonTarek TomehNo ratings yet

- 1008 Short-Form Course Outline (Fall2023)Document2 pages1008 Short-Form Course Outline (Fall2023)momilaNo ratings yet

- The Analysis of Indicators Aimed at The Sustainable Development of Alcohol Production Using The Python Programming Language (According To The Data of The Republic of Armenia)Document5 pagesThe Analysis of Indicators Aimed at The Sustainable Development of Alcohol Production Using The Python Programming Language (According To The Data of The Republic of Armenia)International Journal of Innovative Science and Research TechnologyNo ratings yet

- DFCDocument1 pageDFCJolina BanzonNo ratings yet

- JME Regional-ClassificationsDocument16 pagesJME Regional-ClassificationsADITYA GHASLENo ratings yet