You might also like

- The Profit Zone (Review and Analysis of Slywotzky and Morrison's Book)From EverandThe Profit Zone (Review and Analysis of Slywotzky and Morrison's Book)No ratings yet

- Competitive Strategy - 10 - Merger & AcquisitionsDocument23 pagesCompetitive Strategy - 10 - Merger & AcquisitionsChiara SalaNo ratings yet

- Business Opportunity Thinking: Building a Sustainable, Diversified BusinessFrom EverandBusiness Opportunity Thinking: Building a Sustainable, Diversified BusinessNo ratings yet

- Lecture 9 - Corporate Strategy NotesDocument2 pagesLecture 9 - Corporate Strategy NotesArmenayNo ratings yet

- Types of Market IntegrationDocument4 pagesTypes of Market IntegrationDollente EddieNo ratings yet

- The Six Types of Successful AcquisitionsDocument6 pagesThe Six Types of Successful Acquisitionsx_artNo ratings yet

- 3.1.2 Business GrowthDocument8 pages3.1.2 Business GrowthAnuvrat ShankerNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful Acquisitionsbubb_rubbNo ratings yet

- Marketing 18Document13 pagesMarketing 18api-3728497No ratings yet

- Flashback Notes, Unit-2, XII ClassDocument24 pagesFlashback Notes, Unit-2, XII Classpraveenathelete007No ratings yet

- Instruction For Nantucket NectarsDocument4 pagesInstruction For Nantucket NectarsTanaporn Suwanchaiyong100% (1)

- Bain Brief Clearing The Roadblocks To Better b2b Pricing PDFDocument12 pagesBain Brief Clearing The Roadblocks To Better b2b Pricing PDFRishabh VijayNo ratings yet

- ASS1 COSTofQUALITY AMISTADDocument4 pagesASS1 COSTofQUALITY AMISTADchristian rey dibdibNo ratings yet

- Competitive Advantage, Firm Performance, and Business ModelsDocument29 pagesCompetitive Advantage, Firm Performance, and Business ModelsMuningrumNo ratings yet

- DrinkCo Insight To Action: The Three Facets of An Effective Go-To-Market StrategyDocument1 pageDrinkCo Insight To Action: The Three Facets of An Effective Go-To-Market StrategyWilson Perumal & CompanyNo ratings yet

- Case AnalysisDocument6 pagesCase AnalysisEina GuptaNo ratings yet

- Focus Generic Strategy. Cost Focus Involves Focusing On A Segment or Number of Segments ofDocument4 pagesFocus Generic Strategy. Cost Focus Involves Focusing On A Segment or Number of Segments ofSidad KurdistaniNo ratings yet

- Instruction For Nantucket NectarsDocument4 pagesInstruction For Nantucket NectarsTanaporn SuwanchaiyongNo ratings yet

- StrategiesDocument20 pagesStrategiesKashif TradingNo ratings yet

- Application of IO Framework revisedDocument3 pagesApplication of IO Framework revisedDev ShahNo ratings yet

- Market Integration: Types, Advantages, and DisadvantagesDocument10 pagesMarket Integration: Types, Advantages, and DisadvantagesWynnie RondonNo ratings yet

- PPT - C02 - Company and Marketing StrategyDocument68 pagesPPT - C02 - Company and Marketing StrategyYasmina AlyNo ratings yet

- Group5 - Assignment 2Document3 pagesGroup5 - Assignment 2NiteshNo ratings yet

- Stratma 1.1Document4 pagesStratma 1.1Patrick AlvinNo ratings yet

- Growth: StrategiesDocument28 pagesGrowth: StrategiesJelna CeladaNo ratings yet

- Strategy & Policy Lecture Week 8 - CanvasDocument39 pagesStrategy & Policy Lecture Week 8 - CanvasPo Wai LeungNo ratings yet

- Chapter 3CDocument16 pagesChapter 3CFerdinand GeliNo ratings yet

- Graph AnalysisDocument1 pageGraph AnalysisRoaa WaleedNo ratings yet

- Internal and External GrowthDocument22 pagesInternal and External GrowthArif Akmal BahromNo ratings yet

- Part Three: Business Marketing ProgrammingDocument26 pagesPart Three: Business Marketing ProgrammingCandra GirinataNo ratings yet

- Hershey's strategic analysis and planning matrixDocument4 pagesHershey's strategic analysis and planning matrixPatrik Oliver PantiaNo ratings yet

- PLC and BCG Matrix Analysis for ITC LtdDocument41 pagesPLC and BCG Matrix Analysis for ITC Ltdrajs27No ratings yet

- Introduction To Marketing: University of Chicago Marketing ManagementDocument22 pagesIntroduction To Marketing: University of Chicago Marketing ManagementtikallaNo ratings yet

- Marcouse Chapter1 pt1Document2 pagesMarcouse Chapter1 pt1vad01No ratings yet

- 669368-Ubv2916u - Deem DilemmaDocument9 pages669368-Ubv2916u - Deem Dilemmarsnagpal2006No ratings yet

- Case Study ExampleDocument6 pagesCase Study ExampleNurhafizah RamliNo ratings yet

- Business as levelDocument24 pagesBusiness as levelxxsara 06No ratings yet

- Module II PBMDocument14 pagesModule II PBMRajesh Kumar NayakNo ratings yet

- BCG Concept of Competitive Analysis & Corporate StrategyDocument27 pagesBCG Concept of Competitive Analysis & Corporate StrategySandeep Guha Niyogi100% (1)

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful AcquisitionsConsulter TutorNo ratings yet

- Daily Wear: Business Management and StrategyDocument7 pagesDaily Wear: Business Management and StrategyMuhammad ArslanNo ratings yet

- Sustainable Fashion Company Product Market FitDocument6 pagesSustainable Fashion Company Product Market FitSaransh Thahrani100% (1)

- Sales Objectives and PlanningDocument31 pagesSales Objectives and PlanningAmit PaulNo ratings yet

- Topic 2 - Strategic Marketing Analysis and BudgetingDocument5 pagesTopic 2 - Strategic Marketing Analysis and BudgetingJoseph VillartaNo ratings yet

- Formulating Marketing Communication Plan: (Managing The Sales Force and Sales Administration)Document36 pagesFormulating Marketing Communication Plan: (Managing The Sales Force and Sales Administration)Jyoti Arvind PathakNo ratings yet

- Handbook of Business Strategy: Understanding Brand's Value: Advancing Brand Equity Tracking To Brand Equity ManagementDocument6 pagesHandbook of Business Strategy: Understanding Brand's Value: Advancing Brand Equity Tracking To Brand Equity ManagementbspirashanthNo ratings yet

- Strategic Management - Open Book Test-Question 07Document4 pagesStrategic Management - Open Book Test-Question 07pavithraNo ratings yet

- Case Study: Group No. 9Document11 pagesCase Study: Group No. 9BhushanbmNo ratings yet

- Learn Value - Berry GlobalDocument28 pagesLearn Value - Berry Globalivan.bliminse1402No ratings yet

- Attachment 1638013912-1Document45 pagesAttachment 1638013912-1Manzar HussainNo ratings yet

- Capsim Strategy LearningsDocument20 pagesCapsim Strategy LearningsAakash SinghalNo ratings yet

- Lesson 2 Managing ProductDocument14 pagesLesson 2 Managing ProductCOCONUTNo ratings yet

- Case Study - Nilgai Foods: Positioning Packaged Coconut Water in India (Cocofly)Document6 pagesCase Study - Nilgai Foods: Positioning Packaged Coconut Water in India (Cocofly)prathmesh kulkarniNo ratings yet

- Building Long Term Brand Equity Through Sales Promotion PlanDocument12 pagesBuilding Long Term Brand Equity Through Sales Promotion PlanSumedh BhagwatNo ratings yet

- PESTEL Analysis Reveals Costco's Strategic AdvantagesDocument10 pagesPESTEL Analysis Reveals Costco's Strategic AdvantagesSri VastavNo ratings yet

- Business Plan - Marketplace Simulation.Document11 pagesBusiness Plan - Marketplace Simulation.ARCHIT GUPTA PGP 2020 Batch100% (1)

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful Acquisitionsbubb_rubbNo ratings yet

- SWOT - Peer Group Analysis - ShopifyDocument5 pagesSWOT - Peer Group Analysis - Shopifyharshilthakkar208No ratings yet

- OP Investor Deck - 2019 9.25.19 VFDocument14 pagesOP Investor Deck - 2019 9.25.19 VFkeimokNo ratings yet

- Lesson 3Document14 pagesLesson 3Patricia RodriguesNo ratings yet

- CVP Analysis: Case: Aussie Pies (A)Document35 pagesCVP Analysis: Case: Aussie Pies (A)jk kumarNo ratings yet

- Raffles Holdings Limited - Valuation of A DivestitureDocument37 pagesRaffles Holdings Limited - Valuation of A Divestiturejk kumarNo ratings yet

- Raffles Holdings Limited - Valuation of A Divestiture Teaching Note - NTU044-XLS-EnGDocument7 pagesRaffles Holdings Limited - Valuation of A Divestiture Teaching Note - NTU044-XLS-EnGjk kumarNo ratings yet

- The Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of GilletteDocument366 pagesThe Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of Gillettejk kumarNo ratings yet

- Case: The Boeing 7E7Document183 pagesCase: The Boeing 7E7jk kumarNo ratings yet

- ANNUAL REPORT 2017-18 HIGHLIGHTSDocument220 pagesANNUAL REPORT 2017-18 HIGHLIGHTSramsinntNo ratings yet

- White Hills Children's MuseumDocument23 pagesWhite Hills Children's Museumjk kumarNo ratings yet

- Boeing 7e7 Uv6426 Xls EngDocument82 pagesBoeing 7e7 Uv6426 Xls Engjk kumarNo ratings yet

- Estimation of Cost of Capital: Case: The Boeing 7E7Document125 pagesEstimation of Cost of Capital: Case: The Boeing 7E7jk kumarNo ratings yet

- 6 Polaroid Corporation 1996Document64 pages6 Polaroid Corporation 1996jk kumarNo ratings yet

- EVA Analysis: Case: Vyaderm PharmaceuticalsDocument56 pagesEVA Analysis: Case: Vyaderm Pharmaceuticalsjk kumarNo ratings yet

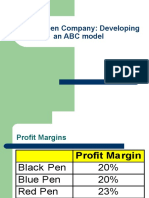

- Classic Pen Company: Developing An ABC ModelDocument22 pagesClassic Pen Company: Developing An ABC Modeljk kumarNo ratings yet

- Boeing 7e7 Uv6426 Xls EngDocument82 pagesBoeing 7e7 Uv6426 Xls Engjk kumarNo ratings yet

- ABC - Ashokleyland MDP 2017Document41 pagesABC - Ashokleyland MDP 2017jk kumarNo ratings yet

- Siemens Electric Motor Works (A) Process-Oriented CostingDocument12 pagesSiemens Electric Motor Works (A) Process-Oriented Costingjk kumar100% (1)

- Marriott - Spread SheetDocument13 pagesMarriott - Spread Sheetjk kumarNo ratings yet

- Project No 1 DCF 2 DCF 3 DCF 4 DCF 5 Initial Investment: Exhibit 1 Project Free Cash Flows (Dollars in Thousands)Document5 pagesProject No 1 DCF 2 DCF 3 DCF 4 DCF 5 Initial Investment: Exhibit 1 Project Free Cash Flows (Dollars in Thousands)jk kumarNo ratings yet

- Mercury Athletic Footwear - Valuing The OpportunityDocument55 pagesMercury Athletic Footwear - Valuing The OpportunityKunal Mehta100% (2)

- Case: The Boeing 7E7Document183 pagesCase: The Boeing 7E7jk kumarNo ratings yet

- 12 Marriott Corporation - The Cost of Capital (Abridged)Document9 pages12 Marriott Corporation - The Cost of Capital (Abridged)jk kumarNo ratings yet

- Boeing 7E7 - UV6426-XLS-ENGDocument85 pagesBoeing 7E7 - UV6426-XLS-ENGjk kumarNo ratings yet

- 3 Divisional Cost of CapitalDocument41 pages3 Divisional Cost of Capitaljk kumarNo ratings yet

- Value Investing - Used in Private Banking ProgrameDocument57 pagesValue Investing - Used in Private Banking Programejk kumarNo ratings yet

- Market Timing Case Study Evaluating Investment RiskDocument31 pagesMarket Timing Case Study Evaluating Investment Riskjk kumarNo ratings yet

- Terrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705Document6 pagesTerrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705jk kumarNo ratings yet

- Mercury Case ExhibitsDocument10 pagesMercury Case ExhibitsjujuNo ratings yet

- BEA Associates - Enhanced Equity Index FundDocument16 pagesBEA Associates - Enhanced Equity Index Fundjk kumarNo ratings yet

- Convertible Securities: Case: Mogen IncDocument93 pagesConvertible Securities: Case: Mogen Incjk kumarNo ratings yet

- European Option: Basic (No Dividend) ModelDocument8 pagesEuropean Option: Basic (No Dividend) Modeljk kumarNo ratings yet

- Bond ValuationDocument52 pagesBond Valuationjk kumarNo ratings yet

- Sanction StatusDocument76 pagesSanction StatusTYCS35 SIDDHESH PENDURKARNo ratings yet

- In May 2010 The Budgeted Sales Were 19Document4 pagesIn May 2010 The Budgeted Sales Were 19Bisag AsaNo ratings yet

- Merger & AcquisitionDocument24 pagesMerger & Acquisition9990255764No ratings yet

- Sap Product Costing Configuration DocumentDocument16 pagesSap Product Costing Configuration Documentguru_vkg75% (4)

- 20 BCD7263 Sam AltmanDocument32 pages20 BCD7263 Sam Altmananunay.20bcd7263No ratings yet

- CA Final Mock Test Paper 2 SolutionsDocument19 pagesCA Final Mock Test Paper 2 SolutionsdikshaNo ratings yet

- P2106069 - Manual Book DND 150 VolvoDocument597 pagesP2106069 - Manual Book DND 150 VolvoUsup ViankNo ratings yet

- Sustainable Supply Chain Management: A Review of Literature and Implications For Future ResearchDocument49 pagesSustainable Supply Chain Management: A Review of Literature and Implications For Future ResearchShashi BhushanNo ratings yet

- Accounting For Government and Not-For-Profit OrganizationsDocument7 pagesAccounting For Government and Not-For-Profit OrganizationsAngela QuililanNo ratings yet

- V - 62 Caroni, Trinidad, Tuesday 14th March, 2023-Price $1.00 N - 39Document17 pagesV - 62 Caroni, Trinidad, Tuesday 14th March, 2023-Price $1.00 N - 39ERSKINE LONEYNo ratings yet

- Asme B16-25 1997Document22 pagesAsme B16-25 1997susisaravananNo ratings yet

- Job Description: Polaris Power Engineering Silliman Avenue Extension Dumaguete CityDocument2 pagesJob Description: Polaris Power Engineering Silliman Avenue Extension Dumaguete CityWilliam Andrew Gutiera BulaqueñaNo ratings yet

- IFRS IntroductionDocument44 pagesIFRS Introductionpadm0% (1)

- Micro Perspective of Tourism & Hospitaity ManagementDocument9 pagesMicro Perspective of Tourism & Hospitaity ManagementRikki Vergara FloresNo ratings yet

- Wessal Karim's Rs. 91,000 Conveyor Project NPV AnalysisDocument5 pagesWessal Karim's Rs. 91,000 Conveyor Project NPV AnalysisHumair UddinNo ratings yet

- Coke's Product Life Cycle in 40 CharactersDocument10 pagesCoke's Product Life Cycle in 40 Charactersvishalsurwase2_3559060% (5)

- Basic Occupational Safety and Health IntroductionDocument35 pagesBasic Occupational Safety and Health IntroductionJoseph Nathan MarquezNo ratings yet

- Assignment?Document6 pagesAssignment?Fahad HassanNo ratings yet

- Payment advice from Coastal Gujarat Power to Centre Tap EngineeringDocument2 pagesPayment advice from Coastal Gujarat Power to Centre Tap EngineeringNanu PatelNo ratings yet

- FindsDocument8 pagesFindsdan4oNo ratings yet

- Call Centre Investment ProposalDocument3 pagesCall Centre Investment ProposalPredueElleNo ratings yet

- La La Land SongbookDocument74 pagesLa La Land SongbookNickNo ratings yet

- Space MatrixDocument22 pagesSpace MatrixEvi AfifahNo ratings yet

- PIP - One Time CleansingDocument5 pagesPIP - One Time Cleansingcpscmain.supplyNo ratings yet

- Restaurant Feasibility ReportDocument7 pagesRestaurant Feasibility ReportJoneric RamosNo ratings yet

- Valve Market Report ESADocument53 pagesValve Market Report ESAAshwin KumarNo ratings yet

- Personal Branding Persevering Towards Success Leza KlenkDocument13 pagesPersonal Branding Persevering Towards Success Leza KlenkPrabhuNo ratings yet

- Reviewer in Smaw NC IDocument2 pagesReviewer in Smaw NC IMaricar CarandangNo ratings yet

- 9 Strategic Parterning and CollaborativeDocument50 pages9 Strategic Parterning and CollaborativeSafdar PervaizNo ratings yet

- Saipem Sustainability 2018Document72 pagesSaipem Sustainability 2018dandiar1No ratings yet