You might also like

- Investment Analysis - Polar Sports (A)Document9 pagesInvestment Analysis - Polar Sports (A)pratyush parmar100% (13)

- Porter's Five Forces: Understand competitive forces and stay ahead of the competitionFrom EverandPorter's Five Forces: Understand competitive forces and stay ahead of the competitionRating: 4 out of 5 stars4/5 (10)

- Price and Output Determination Under Imperfect CompetitionDocument19 pagesPrice and Output Determination Under Imperfect CompetitionAshish PareekNo ratings yet

- Monopolistic and Oligopoly: © 2006 Thomson/South-WesternDocument34 pagesMonopolistic and Oligopoly: © 2006 Thomson/South-WesternSurya PanwarNo ratings yet

- Session 8 - Monopoly - MonopolisticDocument24 pagesSession 8 - Monopoly - MonopolisticRamnik WaliaNo ratings yet

- Monopolistic CompetitionDocument38 pagesMonopolistic CompetitionGivemeanswersNo ratings yet

- Bcom Be MCQ III UnitDocument14 pagesBcom Be MCQ III UnitD.Vishnu Vardhan CommerceNo ratings yet

- Microeconomics PartDocument30 pagesMicroeconomics PartEmma QuennNo ratings yet

- Perfectly Competitive Market: Perfect CompetitionDocument8 pagesPerfectly Competitive Market: Perfect CompetitionLuna KimNo ratings yet

- MonopolisticDocument25 pagesMonopolisticDharshini RajkumarNo ratings yet

- Chapter 7.1 and 7.2 Group 1 ManEconDocument3 pagesChapter 7.1 and 7.2 Group 1 ManEconfrancheskaarcederaNo ratings yet

- Economics MarketsDocument10 pagesEconomics MarketsGEORGENo ratings yet

- Mod 4 TaskDocument1 pageMod 4 Tasknot jedNo ratings yet

- Unit II - Monopolistic CompetitionDocument22 pagesUnit II - Monopolistic CompetitionSam Ebenezer .SNo ratings yet

- Lecture 12 - Chapter 16 - Monopolistic CompetitionDocument21 pagesLecture 12 - Chapter 16 - Monopolistic Competitionvuquangtruong13122002No ratings yet

- Perfect CompetitionDocument10 pagesPerfect CompetitionHuzaifa RashidNo ratings yet

- Micro Ch179PresentationDocument25 pagesMicro Ch179Presentationfoz100% (1)

- R16 The Firm and Market Structures PDFDocument37 pagesR16 The Firm and Market Structures PDFROSHNINo ratings yet

- Monopolistic Competition and Product DifferentiationDocument18 pagesMonopolistic Competition and Product DifferentiationSurya PanwarNo ratings yet

- Mono PlasticDocument6 pagesMono PlasticDua MasnoorNo ratings yet

- Imperfect Competition and Market Power ExplainedDocument38 pagesImperfect Competition and Market Power Explainedanu nitiNo ratings yet

- Final Exam (Answer) : ECO1132 (Fall-2020)Document13 pagesFinal Exam (Answer) : ECO1132 (Fall-2020)Nahid Mahmud ZayedNo ratings yet

- Economics Principles Problems and Policies Mcconnell 20th Edition Solutions ManualDocument16 pagesEconomics Principles Problems and Policies Mcconnell 20th Edition Solutions ManualAntonioCohensirt100% (39)

- ECO111-CHAPTER 16-Monopolistic CompetitionDocument26 pagesECO111-CHAPTER 16-Monopolistic CompetitionPhung Anh Do (K18 DN)No ratings yet

- Monopolistic CompetitionDocument17 pagesMonopolistic CompetitionAlok ShuklaNo ratings yet

- Pertemuan Ix 1Document8 pagesPertemuan Ix 1Rumiati 72No ratings yet

- MARKET EQUILIBRIUM economicsDocument20 pagesMARKET EQUILIBRIUM economicsmayureshbachhavchessNo ratings yet

- Micro EconomicsDocument6 pagesMicro Economicsnimitjain10No ratings yet

- Monopolistic Competition and OligopolyDocument47 pagesMonopolistic Competition and OligopolyAnuNo ratings yet

- Brown Modern Fashion PresentationDocument48 pagesBrown Modern Fashion PresentationStephane Kate CaracaNo ratings yet

- Market Structures: Imperfect Or: Monopolistic CompetitionDocument29 pagesMarket Structures: Imperfect Or: Monopolistic CompetitionHendrix NailNo ratings yet

- FORMS OF MARKETSDocument14 pagesFORMS OF MARKETSsridharvchinni_21769No ratings yet

- Class 7 PDFDocument34 pagesClass 7 PDFAzim HossainNo ratings yet

- Econ Finals Reviewer PDFDocument16 pagesEcon Finals Reviewer PDFMarianNo ratings yet

- Chapter 8 Profit Maximisation and Competitive SupplyDocument26 pagesChapter 8 Profit Maximisation and Competitive SupplyRitesh RajNo ratings yet

- Monopolistic Competition Attributes and EffectsDocument16 pagesMonopolistic Competition Attributes and EffectsPramod KanojiaNo ratings yet

- 5-7 - Market Structures and EfficiencyDocument83 pages5-7 - Market Structures and EfficiencySamiyah Irfan 2023243No ratings yet

- Presetation On Perfectly Competittive Market Vs Monopoly: Rafi Ahmed (11100100030)Document16 pagesPresetation On Perfectly Competittive Market Vs Monopoly: Rafi Ahmed (11100100030)Rafi AhmêdNo ratings yet

- Chap011 RevDocument12 pagesChap011 RevBlackbubbleNo ratings yet

- Microeconomics II Work SheetDocument31 pagesMicroeconomics II Work SheetTsion GetuNo ratings yet

- Chapter Monopolistic CompetitionDocument3 pagesChapter Monopolistic CompetitionRashed SifatNo ratings yet

- Eco 101 FinalDocument4 pagesEco 101 FinalShahidin ShirshoNo ratings yet

- Chap 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsDocument48 pagesChap 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsjeankerlensNo ratings yet

- Chapter 10Document24 pagesChapter 10prabhuthalaNo ratings yet

- CH 16 Monopolistic CompetitionDocument21 pagesCH 16 Monopolistic CompetitionMuhammad Fawad KhanNo ratings yet

- Features of monopolistic competitionDocument4 pagesFeatures of monopolistic competitionNagaraj BeeduNo ratings yet

- Chapter 12 FunalDocument9 pagesChapter 12 FunalQamar VirkNo ratings yet

- Lecture 4 Business EconomicsDocument15 pagesLecture 4 Business EconomicsTayyaba JawedNo ratings yet

- Activity No. 6 1Document8 pagesActivity No. 6 1Carlos Lois SebastianNo ratings yet

- Market StructureDocument18 pagesMarket StructureJude ConwayNo ratings yet

- 4 Market Structures ModifiedDocument4 pages4 Market Structures ModifiedDanaNo ratings yet

- COMPETITION AND DIFFERENTIATED PRODUCTSDocument19 pagesCOMPETITION AND DIFFERENTIATED PRODUCTSPowli HarshavardhanNo ratings yet

- Microeconomics Chapter 13Document23 pagesMicroeconomics Chapter 13202110782No ratings yet

- MANAGERIAL ECONOMICS: PRICING THEORYDocument117 pagesMANAGERIAL ECONOMICS: PRICING THEORYKhanal NilambarNo ratings yet

- Price and Output Determination Under Different Market StructuresDocument42 pagesPrice and Output Determination Under Different Market StructuresrajeshwariNo ratings yet

- CFO CIU 201 Lecture9Document20 pagesCFO CIU 201 Lecture9Waseq Emam NiloyNo ratings yet

- Nataliemoore MonopoliesDocument1 pageNataliemoore Monopoliessnehilhaldar1998No ratings yet

- Market Structure and Price Output DeterminationDocument11 pagesMarket Structure and Price Output DeterminationRekha BeniwalNo ratings yet

- PSR 07Document24 pagesPSR 07Nirmal mehtaNo ratings yet

- Summary of Austin Frakt & Mike Piper's Microeconomics Made SimpleFrom EverandSummary of Austin Frakt & Mike Piper's Microeconomics Made SimpleNo ratings yet

- Market EfficiencyDocument20 pagesMarket EfficiencyPrince AgrawalNo ratings yet

- International Trade and Capital FlowsDocument34 pagesInternational Trade and Capital FlowsPrince AgrawalNo ratings yet

- Aggregate OutputDocument25 pagesAggregate OutputPrince AgrawalNo ratings yet

- Monetary and Fiscal PolicyDocument29 pagesMonetary and Fiscal PolicyPrince AgrawalNo ratings yet

- Class Notes 11 - Fractions & Percentages Practice QuestionsDocument11 pagesClass Notes 11 - Fractions & Percentages Practice Questions4H Boodram ArvindaNo ratings yet

- Sourcing Winning Products Ebook by Warrick KernesDocument17 pagesSourcing Winning Products Ebook by Warrick KernesMusa MathyeNo ratings yet

- ZeroFire ProfileDocument7 pagesZeroFire ProfiledinduntobzNo ratings yet

- Exit Ticket Report: Es034: Engineering ManagementDocument25 pagesExit Ticket Report: Es034: Engineering ManagementDessa GuditoNo ratings yet

- WerehouseDocument41 pagesWerehouseRamon ColonNo ratings yet

- HSRP Online Appointment Transaction Receipt Rosmerta Safety Systems PVT - LTDDocument1 pageHSRP Online Appointment Transaction Receipt Rosmerta Safety Systems PVT - LTDTaj HackersNo ratings yet

- Media Metrix Desktop Reach Frequency December 2022Document4 pagesMedia Metrix Desktop Reach Frequency December 2022GAMING TECHNo ratings yet

- Saipem Sustainability 2018Document72 pagesSaipem Sustainability 2018dandiar1No ratings yet

- Manish Srivastava-TDS ConfigrationDocument14 pagesManish Srivastava-TDS ConfigrationTaneesha YadavNo ratings yet

- The Economics of Valentine's Day: Market Demand and SupplyDocument4 pagesThe Economics of Valentine's Day: Market Demand and SupplySiddhartha SspNo ratings yet

- Analisis Biaya ProduksiDocument12 pagesAnalisis Biaya ProduksiUmar jonoNo ratings yet

- Booklet - Business Immersion Program 2023Document34 pagesBooklet - Business Immersion Program 2023Kenneth ChandrawidjajaNo ratings yet

- Introduction To Research Methods A Hands On Approach 1st Edition Pajo Test BankDocument12 pagesIntroduction To Research Methods A Hands On Approach 1st Edition Pajo Test Bankethelbertsangffz100% (30)

- Mawdsley - From Billions To Trillions - Financing The SDGs in A World Beyond AidDocument5 pagesMawdsley - From Billions To Trillions - Financing The SDGs in A World Beyond AidCodruța Mihaela HăinealăNo ratings yet

- Hapag SCM DocumentDocument3 pagesHapag SCM DocumentMayank TripathiNo ratings yet

- Flower Carnival A Business Plan On FloweDocument26 pagesFlower Carnival A Business Plan On FloweJamesnjiruNo ratings yet

- Osha Compliance For Pest Management Professionals: Presented by Sheldon Primus, MPA, COSSDocument29 pagesOsha Compliance For Pest Management Professionals: Presented by Sheldon Primus, MPA, COSSSaqib AbbasiNo ratings yet

- DSE - MOBILE Registration FormDocument2 pagesDSE - MOBILE Registration FormTasneef ChowdhuryNo ratings yet

- O"5 Aodco.:of1 d"5, RL) Oos: - 6.oorpa6 G"iu O&od C56i) CD Bro5Document5 pagesO"5 Aodco.:of1 d"5, RL) Oos: - 6.oorpa6 G"iu O&od C56i) CD Bro5Prakash KumarNo ratings yet

- Subject Outlines MIHM 2016 V20.1Document75 pagesSubject Outlines MIHM 2016 V20.1Rahul Yadav100% (1)

- Passenger Terminal Expansion Works Materials CatalogueDocument82 pagesPassenger Terminal Expansion Works Materials CatalogueMariam MousaNo ratings yet

- Razaagha Ba Resume Deloitte 08292015Document1 pageRazaagha Ba Resume Deloitte 08292015api-301664020No ratings yet

- BOODMO - Trusted Online Portal For Spare Parts For The Carmakers in Indian MarketDocument10 pagesBOODMO - Trusted Online Portal For Spare Parts For The Carmakers in Indian MarketDeepam harodeNo ratings yet

- Reading The Market Supply and Demand 2 and QuasimodoDocument73 pagesReading The Market Supply and Demand 2 and QuasimodoZak Dave100% (2)

- The Startup Master PlanDocument25 pagesThe Startup Master PlanCharlene Kronstedt100% (1)

- Practice MCQ 4Document5 pagesPractice MCQ 4business docNo ratings yet

- Merger & AcquisitionDocument24 pagesMerger & Acquisition9990255764No ratings yet

- Endure Medical Cash Count ReportDocument3 pagesEndure Medical Cash Count ReportReger PagiosNo ratings yet

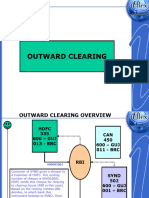

- 5-SETTLEMENT-Outward Clearing 1Document21 pages5-SETTLEMENT-Outward Clearing 1ola.cloudsNo ratings yet